- Specialty & Fine Chemicals

- Asia Pacific Polyol Esters Market

Asia Pacific Polyol Esters Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Asia Pacific Polyol Esters Market by Ester Type (Trimethylolpropane (TMP) Esters, Pentaerythritol (PE) Esters, Dipentaerythritol (DiPE) Esters, Neopentyl Glycol (NPG) Esters, Glycerol Esters, and Others), Product Type (Natural and Synthetic), Application (Refrigeration & Air-Conditioning Lubricants, Industrial Lubricants, and Others), and Regional Analysis for 2026 - 2033

Asia Pacific Polyol Esters Market Size and Share Analysis

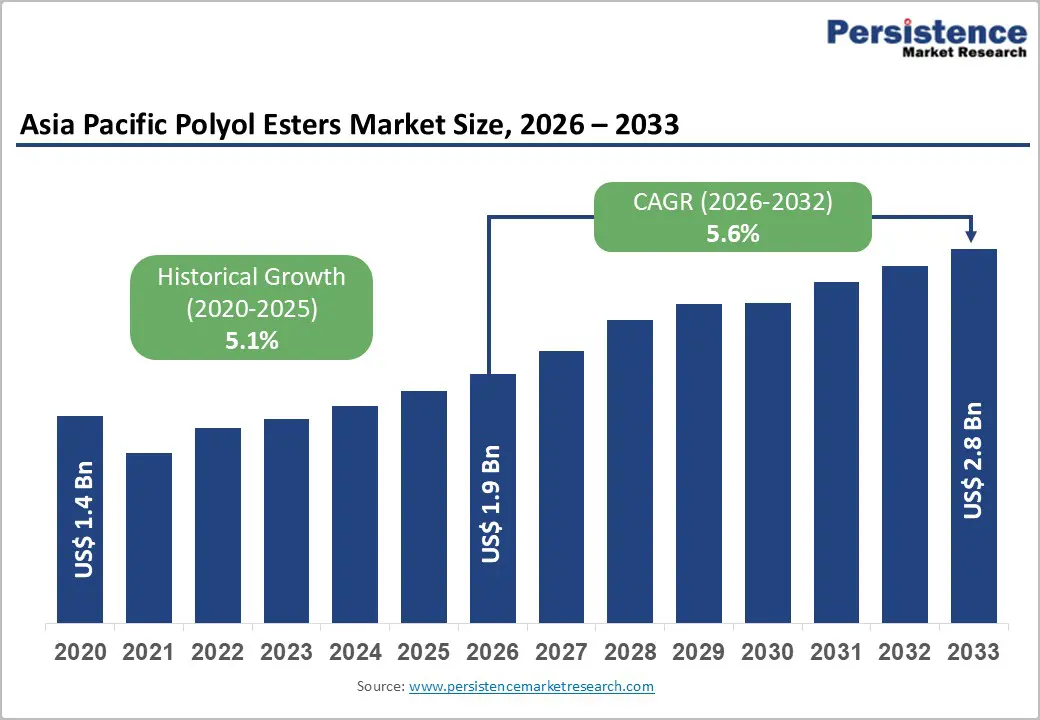

The Asia Pacific polyol ester market size is likely to be valued at US$ 1.9 billion in 2026 and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

Asia Pacific is experiencing a rapid market expansion driven by the accelerating transition from ozone-depleting HCFCs (hydrochlorofluorocarbons) to environmentally safer alternatives, and burgeoning demand for high-performance synthetic lubricants. Rising environmental awareness, coupled with government support for sustainable manufacturing practices, is also compelling industries to adopt polyol ester-based lubricants.

Key Market Highlights:

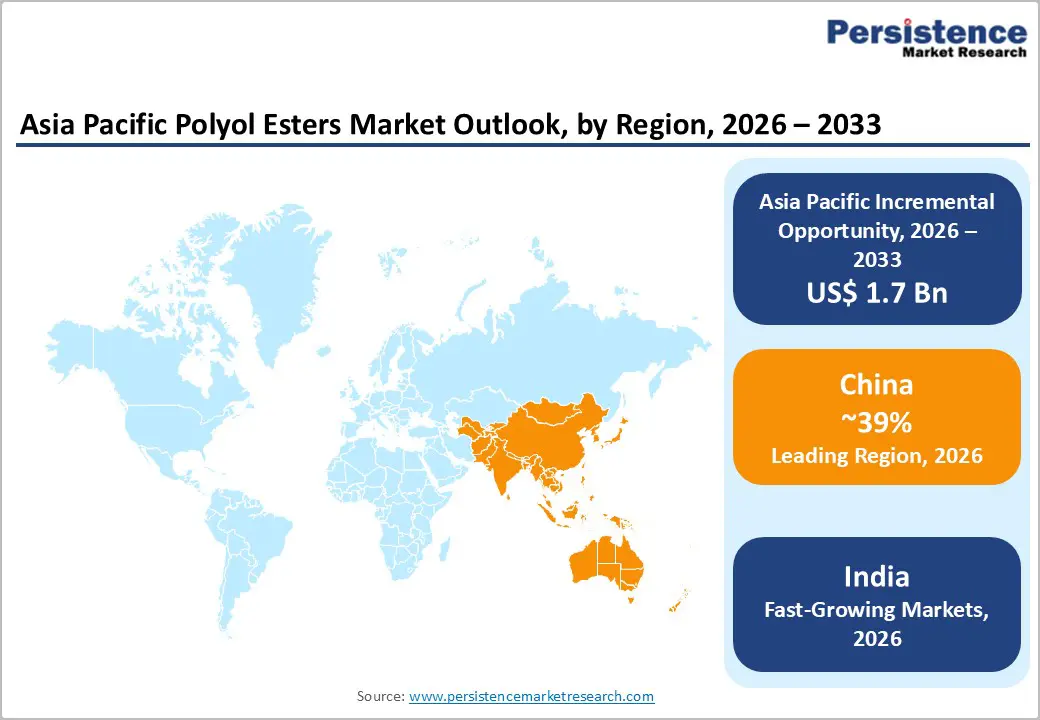

- Leading Region: China leads the Asia Pacific Polyol Esters Market, holding the dominant position with an estimated 41% market share in 2026, driven by its large industrial base, strong manufacturing capacity, and early adoption of environmentally compliant synthetic lubricants.

- Fastest Growing Region: India stands out as the fastest-growing market, projected to expand at a CAGR of 6.9% from 2026 to 2033, driven by rapid industrialization, rising refrigeration demand, and the shift toward environmentally friendly lubricants.

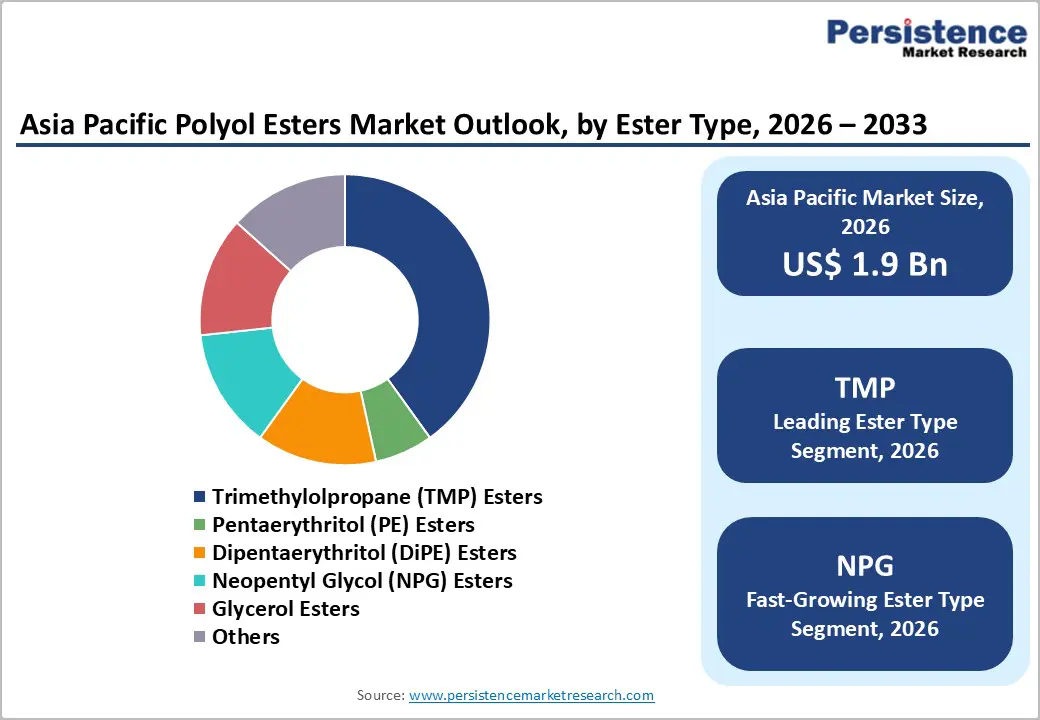

- Dominant Ester Type: Trimethylolpropane (TMP) Esters represent the fastest-growing ester type, supported by superior thermal stability, established supply chains, and regulatory compatibility with modern HFC refrigerants, capturing approximately 32% market share and reinforced dominance through 2033.

- Dominant Application: Refrigeration and Air-Conditioning Lubricants command the dominant application segment with 39% market share, driven by HCFC-to-HFC refrigerant transition regulatory requirements and widespread system modernization across Asia Pacific residential, commercial, and industrial sectors.

- Key Market Opportunity: Bio-based Polyol Ester Development and Electric Vehicle Thermal Management applications represent the primary market opportunities, with emerging demand from sustainable manufacturing initiatives.

| Key Insights | Details |

|---|---|

|

Asia Pacific Polyol Esters Market Size (2026E) |

US$ 1.9 Bn |

|

Market Value Forecast (2033F) |

US$ 2.8 Bn |

|

Projected Growth CAGR(2026-2033) |

5.6% |

|

Historical Market Growth (2020-2025) |

5.1% |

Market Dynamics

Drivers - Regulatory Phase-Out of Ozone-Depleting Refrigerants and Adoption of Next-Generation Alternatives

The Montreal Protocol's implementation in the Asia Pacific is serving as a primary catalyst for polyol ester market expansion. According to regulatory frameworks established by the protocol, the region achieved a 67.5% reduction in HCFC consumption by 2025, with a complete phase-out mandated by 2030. This regulatory mandate has necessitated the replacement of mineral oil-based lubricants with polyol ester-based refrigeration lubricants that demonstrate superior miscibility with HFC refrigerants such as R-410A and emerging low-GWP alternatives, including R-32.

Polyol esters, particularly those synthesized from trimethylolpropane (TMP) and pentaerythritol (PE) polyols, offer exceptional chemical stability, thermal performance, and compatibility with these modern refrigerants. Consequently, the mandatory transition across commercial refrigeration, air-conditioning systems, and industrial cooling applications throughout China, India, Japan, and ASEAN nations is generating substantial demand for polyol ester lubricants, reinforcing market growth throughout the forecast period.

Rising Demand for Synthetic Lubricants in Aviation, Automotive, and Industrial Machinery Sectors

The robust expansion in aerospace, automotive manufacturing, and industrial sectors in Asian economies is driving significant demand for high-performance polyol ester-based lubricants. The global aviation synthetic ester lubricants market is projected to grow at a 6.7% CAGR through 2031, with the Asia Pacific region representing a critical growth engine due to increased aircraft manufacturing in China and expanding commercial aviation operations across the region. Polyol ester-based aviation turbine oils (ATOs) provide exceptional thermal stability, oxidation resistance, and cleanliness standards essential for modern turbine engines operating under extreme temperature conditions.

The automotive sector's acceleration toward lightweight materials and fuel efficiency is increasing demand for synthetic ester-based engine oils and transmission fluids that reduce engine wear and extend maintenance intervals. Industrial applications spanning compressors, hydraulic systems, and heavy machinery similarly benefit from polyol esters' superior lubricity and thermal performance, creating a diversified demand base supporting sustained market growth.

Restraints - High Production Costs and Competition from Alternative Synthetic Base Stocks

Despite favorable market conditions, the polyol ester market faces significant cost-related challenges limiting broader adoption, particularly in price-sensitive segments. Polyol ester production requires sophisticated synthesis processes involving the esterification of high-purity polyols with specialized carboxylic acids, resulting in manufacturing costs substantially exceeding conventional mineral oils and competing with alternative synthetic base stocks, including polyalphaolefins (PAOs) and polyalkylene glycols (PAGs).

Raw material procurement costs, particularly for premium-grade polyols sourced from oleochemical suppliers and specialty chemical manufacturers, constitute a substantial portion of total production expenses. Consequently, polyol ester-based lubricants command premium pricing, limiting market penetration in cost-conscious industrial segments and hindering adoption among small-to-medium enterprises lacking capital reserves for performance-driven lubricant investments.

Opportunity - Bio-Based Polyol Ester Development and Renewable Resource Integration

The acceleration toward circular economy principles and carbon footprint reduction targets is creating substantial opportunities for bio-based polyol ester formulations derived from renewable feedstocks. Regulatory initiatives across the Asia Pacific region, including China's "Made in China 2025" strategy emphasizing green manufacturing and India's commitment to renewable energy targets, are incentivizing manufacturers to develop sustainable polyol ester products.

Notably, China's recent breakthrough at Anhui Putan's CO2-based polycarbonate polyol production facility, the world's largest facility with 50,000 tons annual capacity (Phase 1) and planned expansion to 300,000 tons, demonstrates the region's commitment to sustainable polyol innovation.

Bio-based polyol esters from fatty acids and renewable polyols offer comparable or superior performance characteristics while reducing dependency on fossil fuels and enabling compliance with European Union and emerging ASEAN environmental standards mandating 45%+ renewable carbon content. Manufacturers investing in this opportunity segment can differentiate their product portfolios, capture environmentally conscious customer segments, and position themselves advantageously within increasingly regulated markets.

Electric Vehicle Expansion and Evolving Lubrication Requirements

Asia Pacific’s unprecedented adoption of electric vehicles (EVs), with China accounting for over 60% of global EV sales and expanding manufacturing capabilities in India, Japan, and South Korea, is creating emerging demand for specialized polyol ester-based lubricants. EV thermal management systems, electric motor lubrication, and transmission fluid requirements differ fundamentally from traditional internal combustion engine vehicles, necessitating lubricants with enhanced electrical conductivity, thermal performance, and compatibility with advanced materials.

Polyol esters exhibit superior heat transfer and oxidative stability, essential in the demanding thermal environments of EV powertrains and battery thermal management systems. Furthermore, the expanding infrastructure for autonomous vehicles and advanced driver assistance systems demands next-generation synthetic ester lubricants optimized for variable operating conditions. This emerging application segment presents substantial growth opportunities for polyol ester manufacturers capable of developing proprietary formulations tailored to EV manufacturers' evolving technical specifications.

Category-wise Analysis

Ester Type Insights

Trimethylolpropane (TMP) Esters represent the dominant segment within the Asia Pacific Polyol Ester market, capturing approximately 33% market share due to their exceptional thermal stability, superior oxidative resistance, and established manufacturing infrastructure. TMP esters are synthesized through the condensation of trimethylolpropane polyols with mono-functional carboxylic acids, yielding lubricants characterized by low volatility, minimal varnish formation, and extended service intervals, critical performance attributes driving adoption across refrigeration compressors, air-conditioning systems, and industrial machinery applications.

The well-established supply chain for TMP polyols, supported by major manufacturers including BASF, Dow, and regional producers, ensures cost-effective sourcing and scalable production capacity. Regulatory compatibility with HFC refrigerants and demonstrated performance in extreme-temperature applications reinforce TMP esters' market leadership. The segment's dominance is expected to persist throughout the forecast period, supported by continued infrastructure modernization across the Asia Pacific refrigeration sectors and sustained industrial lubrication demand.

Product Type Insights

Synthetic polyol esters account for approximately 87% of the Asia Pacific Polyol Ester market, reflecting established performance advantages, extensive application validation, and regulatory precedent supporting their deployment across critical industrial sectors. Synthetic polyol esters demonstrate superior thermal stability, exceptional oxidation resistance, and biodegradability exceeding 60-90% according to OECD 301B standardized testing protocols, positioning them as preferred alternatives to conventional mineral oils and conventional ester formulations.

The segment encompasses trimethylolpropane (TMP) esters, pentaerythritol (PE) esters, and specialty formulations optimized for specific applications. Conversely, natural polyol esters derived from renewable vegetable oils and oleochemical feedstocks represent an emerging 15% segment, characterized by lower production volumes but accelerating adoption driven by environmental regulations and consumer preference for sustainably sourced lubricants. Regulatory frameworks increasingly incentivizing renewable content and biodegradable formulations are expected to expand the natural polyol ester segment's market share during the forecast period.

Application Insights

Refrigeration and air-conditioning lubricants constitute the largest application segment, capturing approximately 50% of the Asia Pacific Polyol Ester market, reflecting the sector's scale, regulatory mandates, and critical lubrication requirements. Polyol ester-based refrigeration lubricants provide exceptional miscibility with HFC refrigerants including R-410A and emerging low-GWP alternatives, ensuring reliable oil return from evaporators to compressors across temperature gradients and pressure differentials. The segment encompasses commercial refrigeration systems in retail and food storage, residential and light commercial air-conditioning units, and industrial cooling applications across manufacturing facilities.

Regulatory compliance with the Montreal Protocol's HCFC phase-out schedule and the Kigali Amendment's HFC phase-down mandate across the Asia Pacific region drives sustained demand for compatible polyol ester lubricants. Additionally, the modernization of cooling infrastructure in rapidly urbanizing regions of China, India, and ASEAN nations, driven by rising temperatures, construction expansion, and consumer demand for climate-controlled environments, reinforces this segment's market prominence and growth trajectory.

Regional Insights

China Polyol Esters Market Trends

China dominate the Asia Pacific polyol esters market, accounting for an estimated 41% market share in 2026, supported by its massive industrial base and leadership in manufacturing, automotive production, and refrigeration equipment. The country’s strong position is underpinned by stringent environmental regulations aimed at phasing out ozone-depleting and high–global-warming-potential refrigerants, accelerating the shift toward polyol ester–based lubricants compatible with next-generation refrigerants.

China’s expanding electric vehicle (EV) ecosystem, coupled with rapid growth in cold-chain logistics, data centers, and industrial automation, is further boosting demand for high-performance synthetic lubricants. Additionally, the presence of large domestic chemical producers and vertically integrated supply chains enables cost-efficient production and broad market penetration. Government-led initiatives promoting energy efficiency, carbon reduction, and green manufacturing have encouraged widespread adoption of environmentally friendly lubricants across industrial and commercial sectors.

India Polyol Esters Market Trends

India is expected to be the fastest-growing polyol esters market in Asia Pacific, registering a robust CAGR of 6.9% from 2026 to 2033, driven by rapid industrialization, expanding automotive production, and rising adoption of modern refrigeration and air-conditioning systems. The country’s transition away from HCFC-based refrigerants, in alignment with global environmental commitments, is creating strong demand for polyol ester lubricants that offer superior thermal stability and compatibility with low-GWP refrigerants. Growth in sectors such as cold storage, food processing, pharmaceuticals, and data centers is significantly increasing the need for reliable and energy-efficient lubrication solutions.

Rising awareness of sustainability, combined with supportive government initiatives such as “Make in India” and energy-efficiency standards, is encouraging domestic manufacturing and greater penetration of synthetic lubricants. Although the market remains relatively fragmented, increasing investments by global and regional lubricant manufacturers are improving product availability and technical adoption. These factors position India as a key growth engine for the regional polyol esters market over the forecast period.

South Korea Polyol Esters Market Trends

South Korea is expected to witness significant growth in the Asia Pacific polyol esters market over the forecast period, primarily due to market maturity and limited incremental demand from core end-use industries. The country has already achieved high penetration of advanced refrigeration technologies and synthetic lubricants, leaving less room for rapid volume expansion. While environmental regulations and efficiency standards remain stringent, most industrial players have already transitioned to compliant lubricant systems, resulting in replacement-driven rather than expansion-driven demand.

Significant growth in traditional automotive manufacturing and modest expansion in industrial output are constraining new opportunities for polyol ester consumption. Although emerging applications such as electric vehicles and advanced electronics manufacturing provide some support, these segments are not expected to offset the overall maturity of the market. As a result, South Korea’s polyol esters market is likely to grow at a subdued pace, characterized by stable demand, incremental technological upgrades, and a focus on performance optimization rather than large-scale capacity expansion.

Competitive Landscape for the Polyol Esters Market

Asia Pacific polyol ester market exhibits a moderately consolidated structure characterized by the dominance of three to five major multinational chemical corporations controlling approximately 45-50% combined market share, complemented by a diversified base of 50+ regional and specialty manufacturers serving localized market segments. ExxonMobil, BASF, Shell, Dow, and Lanxess collectively represent the market's dominant players, leveraging established production infrastructure, extensive distribution networks, and advanced R&D capabilities.

Market entrants and regional players, including Wilmar International, Kao Corporation, KLK Oleo, Mitsubishi Chemical, NOF Corporation, and emerging Chinese manufacturers such as Shandong Xinfa Ruijie New Material Technology, employ strategies focused on cost optimization, regional market penetration, and specialized application development. The competitive landscape is characterized by continuous R&D investments in bio-based polyol ester formulations, advanced additive chemistry, and application-specific optimization. Strategic acquisitions, joint ventures, and capacity expansion initiatives reflect industry participants' commitment to capturing growth opportunities.

Key Market Developments:

- In January 2025, Anhui Putan New Materials Technology Co., Ltd. achieved operational status for its revolutionary CO2-based polycarbonate polyol production facility, representing the world's largest facility of its type with 50,000 tons annual capacity.

- In March 2024, BASF Announces Expansion of Synthetic Ester Production Capacity in China. BASF announced a significant investment to expand its synthetic ester production capacity in China, targeting the region's accelerating demand for high-performance lubricants driven by industrial modernization and automotive sector expansion.

Companies Covered in Asia Pacific Polyol Esters Market

- ExxonMobil

- Lanxess

- BASF

- Shell

- DowPol Chemicals (Dow)

- Cargill

- Wilmar International

- NOF Corporation

- Kao Corporation

- Mitsubishi Chemical

- KLK Oleo

- Emery Oleochemicals

- Calumet Specialty Products

- Shandong Xinfa Ruijie New Material Technology

- AVI-OIL (India) Ltd.

Frequently Asked Questions

The Asia Pacific Polyol Ester market is projected to reach US$ 2.8 Bn by 2032, growing at a 5.6% CAGR from 2025 to 2032, driven by regulatory compliance with refrigerant phase-out mandates and expanding industrial lubricant demand across the region.

The primary demand drivers include the adoption of compatible polyol ester-based refrigeration lubricants, expanding air-conditioning and refrigeration infrastructure, growth in aviation and automotive sectors requiring high-performance synthetic lubricants, and increasing environmental regulations promoting biodegradable and renewable-based polyol ester formulations.

Trimethylolpropane (TMP) Esters represent the dominant ester type, capturing approximately 32% market share, supported by exceptional thermal stability, superior oxidation resistance, well-established manufacturing infrastructure, and regulatory compatibility.

China leads the Asia Pacific Polyol Esters Market, holding the dominant position with an estimated 41% market share in 2026, driven by its large industrial base, strong manufacturing capacity, and early adoption of environmentally compliant synthetic lubricants.

Bio-based Polyol Ester Development and Electric Vehicle Thermal Management Applications represent the primary growth opportunities, driven by environmental regulations mandating renewable content and biodegradability.

Leading market participants include ExxonMobil Corporation, BASF SE, Shell Global, Dow Inc., Lanxess AG, Cargill Incorporated, Wilmar International Limited, Kao Corporation, Mitsubishi Chemical Corporation, KLK OLEO, Emery Oleochemicals Group, Calumet Specialty Products Partners, and NOF Corporation.