- Inks, Coatings, Adhesives & Sealants (ICAS)

- Asia Pacific Lamination Adhesive Market

Asia Pacific Lamination Adhesive Market Size, Share, and Growth Forecast, 2026 - 2033

Asia Pacific Lamination Adhesive Market by Resin Type (Polyurethane (PU), Acrylic, and Others), Application Type (Solvent-based, Water-based, and Solvent-less), End-user (Packaging, Automobile & Transportation, Housing & Interior decor, Industrial, and Others), and Country Analysis for 2026 - 2033

Asia Pacific Lamination Adhesive Market Size and Trends Analysis

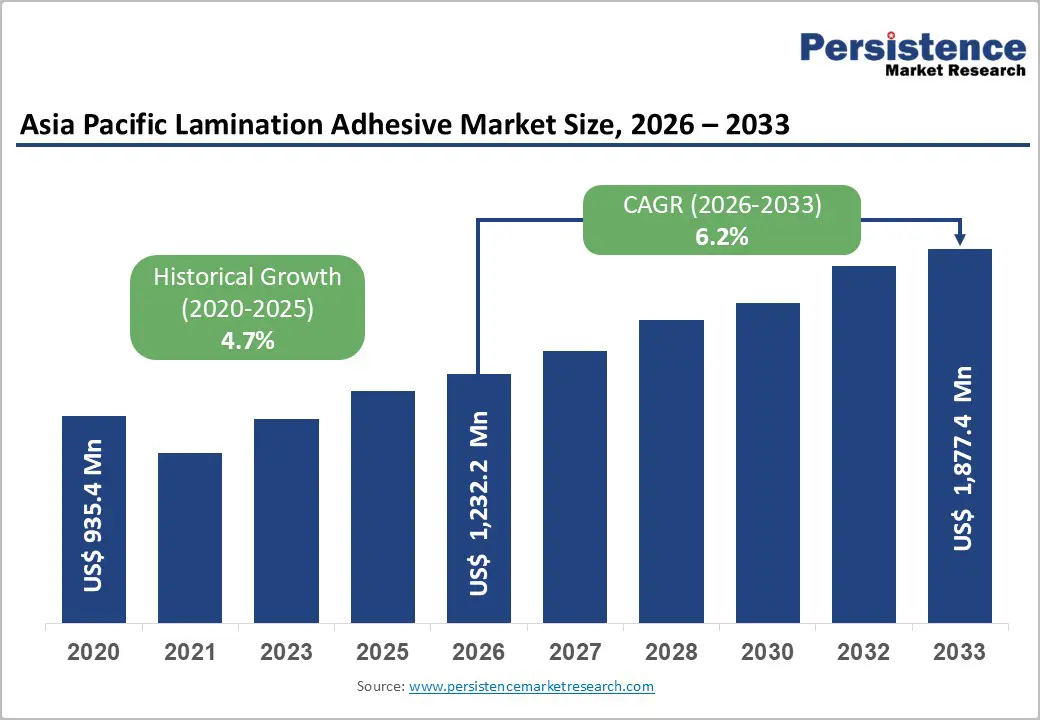

The Asia Pacific lamination adhesive market size is likely to be valued at USD 1.23 billion in 2026 and is projected to reach roughly USD 1.88 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033 (values converted from user-provided million figures). Strong growth is underpinned by the expansion of flexible packaging, rising automotive and transportation output, and the shift toward more sustainable water-based and acrylic chemistries across major economies such as China, India, Japan, and South Korea.

Regulatory pressure on volatile organic compounds (VOCs) and plastic waste is accelerating migration from traditional solvent-heavy systems to low-VOC laminating technologies, supporting above-GDP growth in value-added lamination adhesives. China remains the core demand center, but India, South Korea, and ASEAN markets are set to capture a rising share of incremental regional consumption through 2033, especially in packaging and mobility applications.

Key Industry-Highlights:

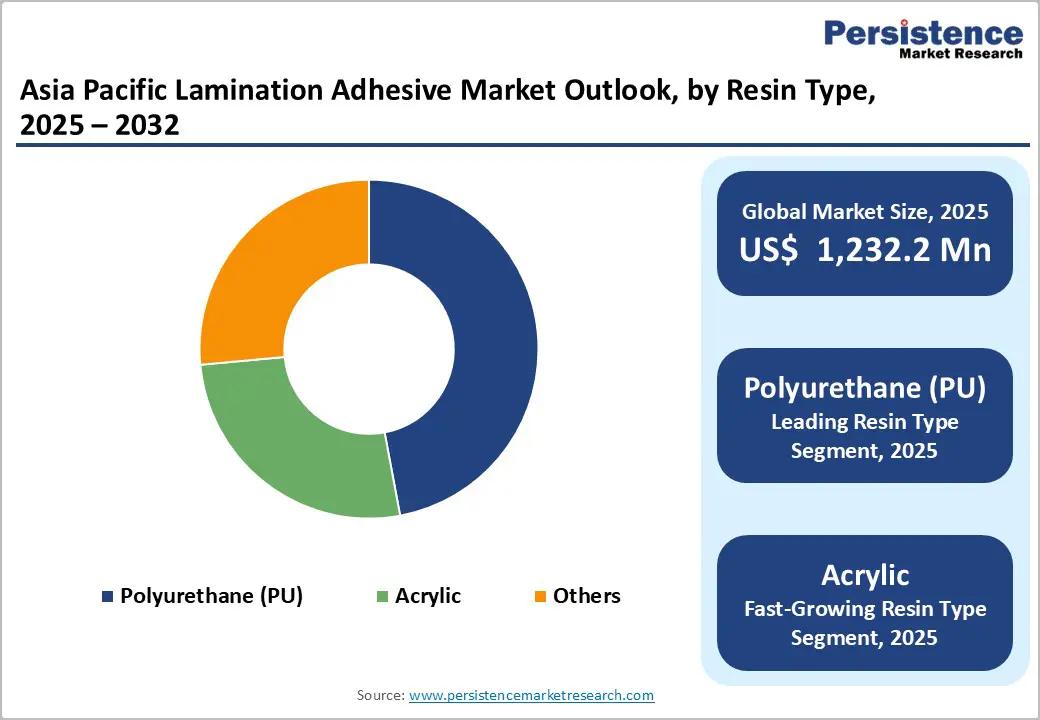

- Resin Analysis: Polyurethane remains the leading resin, with over 48% revenue share in 2026, while acrylic resins are the fastest-growing at about 7.1% CAGR driven by low-VOC, high-clarity packaging requirements.

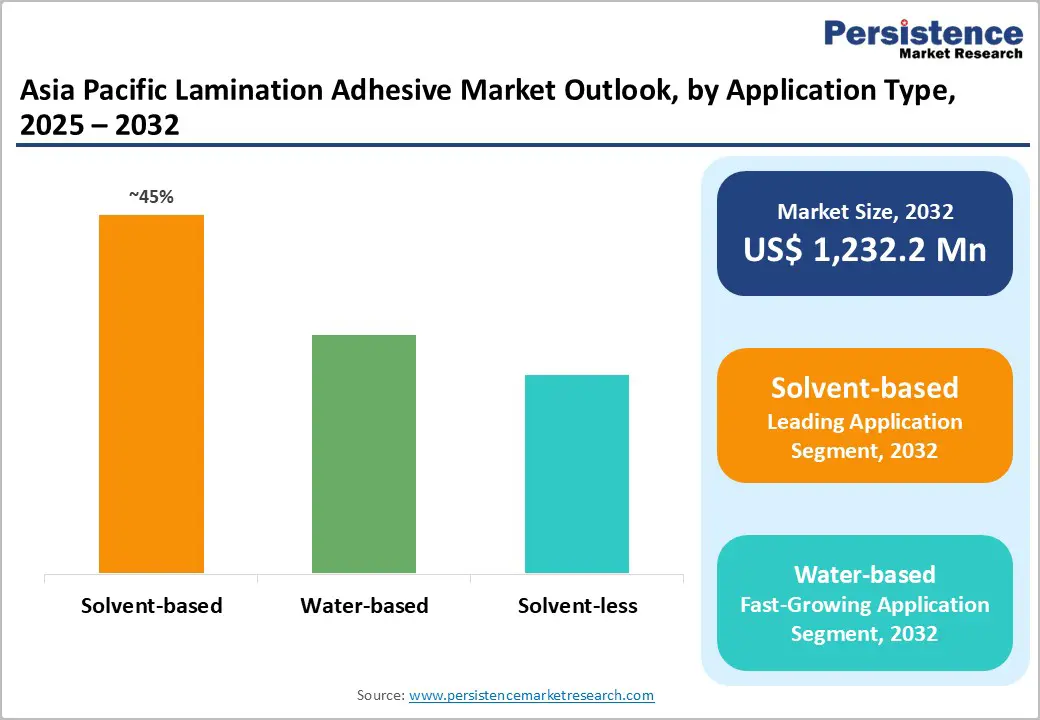

- Leading Application: Solvent-based technologies dominate with more than 45% share, but water-based laminating adhesives are growing at around 7.3% CAGR, propelled by environmental regulations and corporate sustainability targets.

- Leading End-user: Packaging accounts for over 70% of demand, underpinned by China’s CNY 1.15 trillion packaging sector and India’s packaging market, which is heading toward USD 170 billion by 2030.

- Fast-growing End-user: Automobile & transportation is the fastest-growing end-use, supported by China’s production of 26.1 million cars and Japan’s 7.8 million units, plus a regional automotive aftermarket CAGR of 5.7% through 2033.

- China commands more than 48% of regional lamination adhesive revenues, while South Korea leads growth, benefiting from a dynamic packaging and chemical sector and adhesives market CAGR above 5%.

| Key Insights | Details |

|---|---|

| Asia Pacific Lamination Adhesive Market Size (2026E) | US$ 1,232.2 Mn |

| Market Value Forecast (2033F) | US$ 1,877.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Drivers - Expansion of Flexible Packaging and Food & Beverage Sectors

Flexible packaging is the single most important volume driver for laminating adhesives in the Asia Pacific, as converters increase multilayer film usage for food, beverage, personal care, and e-commerce applications. In China, the flexible packaging market is estimated at USD 47 billion in 2024 and is projected to reach nearly USD 57 billion by 2029 at a CAGR of 3.7%, underscoring sustained structural demand for laminating solutions. The broader Chinese packaging industry generated around CNY 1.15 trillion in revenue in 2023, reinforcing its global leadership in packaging output.

India’s packaging market, valued at about USD 101 billion in 2025, is expected to grow at over 10% CAGR to 2030, with flexible formats accounting for the majority of incremental units. These trends translate directly into higher consumption of polyurethane (PU) and acrylic lamination adhesives for pouches, sachets, and high-barrier structures, particularly in food, dairy, snacks, and frozen products. As brand owners premiumize packaging and target longer shelf life, demand shifts from commodity bonding solutions toward high-performance solvent-based and water-based laminating systems with superior optical and mechanical properties, lifting value growth ahead of pure tonnage growth.

Automotive and Transportation Production Growth in Asia Pacific

Automotive and transportation are emerging as strategically important growth pillars for lamination adhesives, particularly in China, Japan, South Korea, and India. In 2023, China produced approximately 26.1 million passenger cars, while Japan produced about 7.77 million units, highlighting the region’s central role in global vehicle manufacturing. Beyond OEM assembly, the Asia Pacific automotive aftermarket is forecast to grow from around USD 171 billion in 2024 to over USD 280 billion by 2033 at a CAGR of 5.7%, sustaining long-term demand for adhesives and sealants in interiors, trims, and replacement components. Laminating adhesives are increasingly used in lightweight interior panels, decorative films, headliners, and thermal/acoustic insulation, supporting OEM lightweighting and fuel-efficiency objectives.

As electric vehicles (EVs) and advanced driver-assistance systems (ADAS) penetration rises in China, Korea, and Japan, the need for multi-material bonding films, foils, nonwovens, and composites further deepens adhesive intensity per vehicle. This structural linkage to vehicle parc expansion, model proliferation, and higher functional requirements in interiors underpins robust medium-term demand growth for high-performance lamination adhesives in transportation applications.

Restraint - Environmental, Health, and Safety Constraints on Solvent-Based Systems

A large portion of installed lamination capacity in the Asia Pacific remains solvent-based, especially in legacy packaging lines, but VOC emissions and worker-exposure risks are drawing heightened regulatory scrutiny. Japan’s Packaging Recycling Act and broader waste-reduction framework impose strict requirements on packaging materials and labeling, encouraging reductions in hazardous substances and promoting recyclability. Similar trends are visible in China and India, where packaging policies increasingly target plastic waste and emissions across the value chain.

Compliance with air-emission limits, solvent recovery, and occupational safety standards raises capex and operating costs for converters reliant on high-solvent laminating adhesives, particularly small and mid-size plants. These constraints can slow capacity additions in traditional technologies and create barriers to entry in some markets, thereby moderating overall volume growth even as higher-value sustainable products expand.

Opportunities - Rapid Growth of Water-Based and Solvent-less Technologies

The strongest medium-term upside lies in water-based and solvent-less lamination adhesives, which directly address regulatory and brand-owner sustainability requirements. Asia Pacific laminated adhesives as a whole are projected to grow at over 6% CAGR through the latter 2020s, but low-VOC technologies are expected to expand materially faster as adoption spreads from Japan and South Korea to China, India, and ASEAN.

Japan’s green packaging market alone is forecast to grow at a CAGR of about 5.2% between 2026 and 2034, providing a sizable pull for environmentally benign laminating chemistries in food, beverage, and personal care packaging. As large FMCG and beverage brands commit to recyclable and mono-material packaging, they increasingly specify adhesives compatible with polyolefin-based structures and mechanical recycling, which favors modern acrylic and PU dispersions. Capturing even a modest incremental share of the region’s fast-growing packaging spend, India’s packaging market is projected to reach nearly USD 170 billion by 2030. In high-value green adhesives, this could translate into several hundred million dollars of incremental annual revenue potential for leading suppliers by the early 2030s.

Category-wise Analysis

Resin Type Insights - Polyurethane Dominance and Acrylic Acceleration Reshape Asia Pacific Resin Portfolio

In the Asia Pacific lamination adhesive market, resin type analysis shows polyurethane (PU) as the dominant segment, while acrylic is the fastest-growing category. Polyurethane-based lamination adhesives are projected to account for over 48% of regional revenue by 2026, underscoring their critical role in high-performance flexible packaging, industrial laminates, and transportation applications. PU systems provide superior adhesion across diverse substrates, including PET, BOPP, aluminum foil, and paper, as well as high heat, chemical, and moisture resistance. These properties are particularly valuable in Asia Pacific, where demand for retortable food pouches, multilayer barrier films, and metallized packaging continues to rise, driven by urbanization and expanding food processing industries. Additionally, PU’s established presence in the broader regional adhesives market, especially in construction and automotive, ensures strong supply chain integration and technical expertise.

Meanwhile, acrylic-based lamination adhesives are expected to grow at the fastest CAGR of approximately 7.1%, supported by increasing demand for optical clarity, color stability, and low-odor formulations. Acrylic systems align with the region’s shift toward water-based and low-VOC solutions, particularly in packaging, labels, and electronics applications where regulatory compliance and sustainability are becoming decisive purchasing factors.

Application Insights

In the Asia Pacific lamination adhesive market, solvent-based lamination technology continues to dominate, projected to maintain over 45% revenue share in 2026, supported by the region’s extensive installed base of solvent-based coating and drying lines across China, India, South Korea, and Southeast Asia. Converters in these countries have decades of operational expertise with polyurethane (PU) solvent systems, particularly in high-volume food, beverage, and personal care flexible packaging. Solvent-based adhesives deliver strong bond integrity, high chemical resistance, and reliable performance at elevated line speeds, making them well-suited for multi-layer laminates requiring durability and barrier performance. Given that many production facilities are already optimized for solvent processing, incremental formulation improvements often present a more cost-effective path than full technology replacement.

However, water-based lamination technology is emerging as the fastest-growing segment, with an expected CAGR of approximately 7.3%. Growth is driven by tightening environmental regulations on VOC emissions and increasing sustainability commitments from global brand owners. Advances in water-borne PU and acrylic dispersion technologies now enable competitive bond strength, clarity, and processing efficiency, encouraging adoption in China, India, and export-oriented ASEAN markets seeking safer, lower-emission production alternatives.

Country Insights and Trends

China Anchors Regional Lamination Adhesives through Packaging Scale and Mobility Investments

China will remain the anchor market, accounting for nearly half of Asia Pacific lamination adhesive revenues by 2026, based on its 48.4% regional share. Applying this share to the regional market implies lamination adhesive sales of roughly USD 0.6 billion in China in 2026, with further growth expected to track or slightly exceed the regional CAGR as high-value applications gain traction. China also accounts for about 16% of global flexible packaging revenue, underscoring its centrality in global packaging supply chains.

The domestic packaging industry generated around CNY 1.15 trillion in revenue in 2023, supported by rising demand for packaged food, e-commerce logistics, and healthcare, all of which use multilayer laminates bonded by high-performance adhesives. On the mobility side, China produced about 26.1 million passenger cars in 2023, the highest in the world, and continues to scale EV production and exports. These factors drive steady demand for laminating adhesives in interior panels, decorative films, and protective laminates across the automotive and transportation sectors. Regulatory initiatives on plastic waste, recycling, and VOC control are gradually pushing converters toward lower-emission water-based and solvent-free systems, creating an opportunity to upgrade the technology mix. Competition is intense, with global leaders such as Dow, Henkel, 3M, and H.B. Fuller competing alongside large domestic chemical and adhesive companies that leverage proximity to local converters. Are investment opportunities particularly strong in eco-designed PU and acrylic laminating systems that enable recyclable packaging structures and support automotive lightweighting.

India Accelerates Lamination Adhesives Growth via Packaging Expansion and Regulatory Reform

India is one of the fastest-growing lamination adhesive demand centers in the Asia Pacific, supported by rapid expansion in packaging and automotive production and an increasingly supportive regulatory framework. The Indian packaging market is valued at about USD 101 billion in 2025 and is projected to reach nearly USD 170 billion by 2030 at a CAGR above 10%, with flexible formats accounting for close to two-thirds of total units. Brickwork Ratings estimates the market at roughly INR 6.7 trillion in FY 2024, with growth of about 6.7% CAGR to FY 2028, confirming robust, multi-year momentum. This directly translates into strong growth for lamination adhesives in food, beverage, personal care, and pharmaceutical packaging, particularly PU and acrylic chemistries optimized for high-speed pouching and multi-layer barrier structures.

India has firmly positioned itself as a leading automotive exporter with strong near-term growth momentum. Automobile exports increased by 19% in FY25, surpassing 5.3 million units, driven by rising global demand for passenger vehicles, two-wheelers, and commercial vehicles. Domestically, the automotive sector continues to scale, with total vehicle production reaching 28.4 million units in FY 2023-24. This expanding production base strengthens demand for laminating adhesives used in vehicle interiors, trims, and specialty films.

The regulatory landscape is becoming more stringent under the Plastic Waste Management Rules and Extended Producer Responsibility (EPR) mandates, which promote higher recycled content and sustainable packaging solutions. These regulations are accelerating the shift toward low-VOC, recyclable, and environmentally compliant adhesive systems.

The market remains moderately fragmented, with global adhesive manufacturers competing alongside regional formulators and packaging converters, many of whom operate integrated film production and adhesive application lines. Key investment opportunities lie in localized manufacturing of water-based laminating adhesives, establishment of technical service centers to optimize converter processes, and collaborative product development with major FMCG companies and automotive OEMs focused on reducing carbon footprints in packaging and vehicle components.

Japan Drives Premium Lamination Adhesives through Green Regulations and Innovation Ecosystems

Japan stands as a premium, innovation-led laminating adhesive market, supported by strict environmental regulations, advanced packaging standards, and highly developed automotive and electronics industries. The country is a leader in sustainable packaging, with the green packaging market projected to reach approximately USD 22-25 billion by the mid-2030s, expanding at a CAGR of about 5-5.3% from the mid-2020s. Policy frameworks such as the Plastic Resource Circulation Strategy and the Packaging Recycling Act are designed to curb single-use plastics, enhance recycling rates, and reduce plastic waste emissions by nearly 25% by 2030. These measures are accelerating the transition toward water-based and solvent-free laminating adhesive technologies.

Packaging activity remains strong, with shipment volumes rising to 19.2 million tons, reflecting a 3.8% year-on-year increase and signalling steady growth momentum in Japan’s packaging sector. In parallel, the automotive industry, producing around 7.77 million passenger cars in 2023, along with robust electronics and industrial manufacturing, sustains consistent demand for high-performance laminates used in interiors, labels, and protective films.

Collaboration between domestic converters and global adhesive manufacturers is intensive, particularly in developing advanced polyurethane (PU) and acrylic systems that meet stringent requirements for low odor, minimal migration, and high thermal stability, in line with strict food safety and automotive standards. The competitive landscape is intense, featuring multinational adhesive suppliers and diversified domestic chemical and ink companies focused on product innovation, operational efficiency, and carbon reduction. Strategic investment opportunities lie in recyclable laminating technologies, bio-based and low-carbon adhesive chemistries, and collaborative innovation models that enable Japanese brand owners to achieve ambitious sustainability goals while maintaining performance and production efficiency.

Competitive Landscape

The Asia Pacific lamination adhesives market exhibits a relatively high degree of concentration, shaped by the presence of both global multinational corporations and well-established regional manufacturers. Key industry leaders frequently identified in the competitive landscape include Dow, Henkel AG & Co. KGaA, 3M, Toyo Ink Group, hubergroup, Ashland, H.B. Fuller, Bostik (a subsidiary of Arkema), BASF SE, and Avery Dennison.

These companies cater to diverse end-use industries, including flexible packaging, automotive, and industrial lamination, supported by extensive product portfolios, global raw material sourcing capabilities, and strong technical service networks. At the same time, the market remains highly competitive at the country level, where numerous mid-sized and domestic formulators compete on pricing, customization, and local distribution advantages particularly in major manufacturing hubs such as China, India, and South Korea.

Key Industry Developments:

- On March 25, 2025, DIC Malaysia launched DUALAM™, a solvent-free adhesive featuring an advanced dual coating system. The new solution is designed to enhance coating efficiency, bonding strength, and sustainability in flexible packaging applications across Asia Pacific.

- In September 2024, Covestro introduced new adhesive solutions for the automotive and footwear industries at the annual China adhesive industry conference. The company emphasized localization strategies to better serve Asia Pacific customers, alongside digital R&D initiatives aimed at accelerating innovation and improving development efficiency.

- On July 9, 2024, Trinseo unveiled LIGOS™ A 9200, an innovative dry lamination adhesive for sustainable flexible packaging. This high-solids acrylic waterborne emulsion enhances performance, operational efficiency, and environmental sustainability for packaging converters.

- On March 14, 2024, Jowat inaugurated a new manufacturing facility in China, strengthening its presence in the world’s largest adhesive market. The expansion reinforces customer proximity, boosts regional supply capabilities, and enhances innovation capacity.

- In 2020, Bostik launched the HERBERTS™ 700 product series, a range of high-performance, solvent-free polyurethane lamination adhesives designed for food packaging, industrial, and medical markets in Asia Pacific, supporting sustainable production and high-quality performance standards.

Companies Covered in Asia Pacific Lamination Adhesive Market

- Henkel AG & Co. KGaA

- Dow

- H.B. Fuller

- Bostik

- Arkema

- BASF SE

- 3M

- Ashland

- Covestro

- Toyochem

- DIC Corporation

- Sika AG

- Pidilite Industries

- Jowat SE

- Avery Dennison

- Coim Group

- Uflex Limited

- Mitsubishi Chemical Group

- Wacker Chemie AG

- Samhwa Paints

- Other Market Players

Frequently Asked Questions

The Lamination Adhesive market is estimated to be valued at US$ 1,232.2 Mn in 2026.

The key demand driver for the Lamination Adhesive market is the rapid growth of flexible packaging, particularly in the food, beverage, pharmaceutical, and personal care industries.

In 2026, China will dominate the market with an exceeding 48% revenue share in the Asia Pacific lamination adhesive market.

Among resin types, polyurethane (PU) has the highest preference, capturing beyond 48% of the market revenue share in 2026, surpassing other resin types.

Henkel AG & Co. KGaA, Dow, H.B. Fuller, Bostik, Arkema, BASF SE, 3M, and Ashland are a few leading players in the Lamination Adhesive market.