- Technology

- Artificial Intelligence (AI) in Cybersecurity Market

Artificial Intelligence (AI) in Cybersecurity Market Size, Share, and Growth Forecast, 2025 - 2032

Artificial Intelligence (AI) in Cybersecurity Market By Security Type (Network Security, Endpoint Security, Others), Offering (Hardware, Software, Services), Technology (Machine Learning (ML), Others), End-user Industry (BFSI, IT & Telecom, Others), and Regional Analysis for 2025 - 2032

Artificial Intelligence (AI) in Cybersecurity Market Share and Trends Analysis

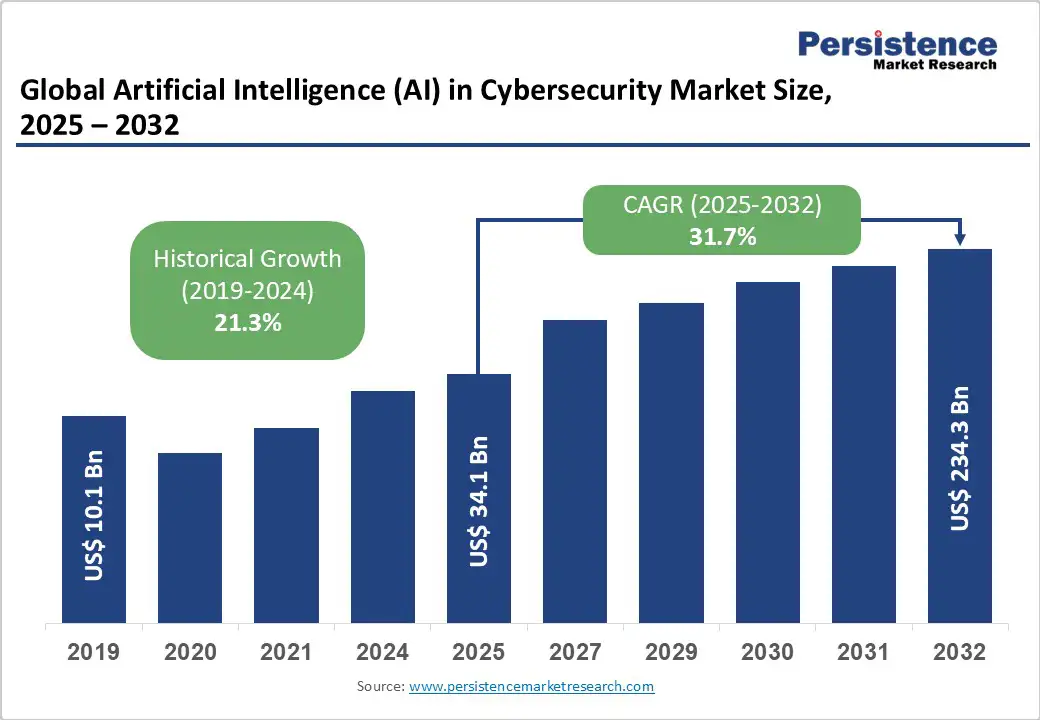

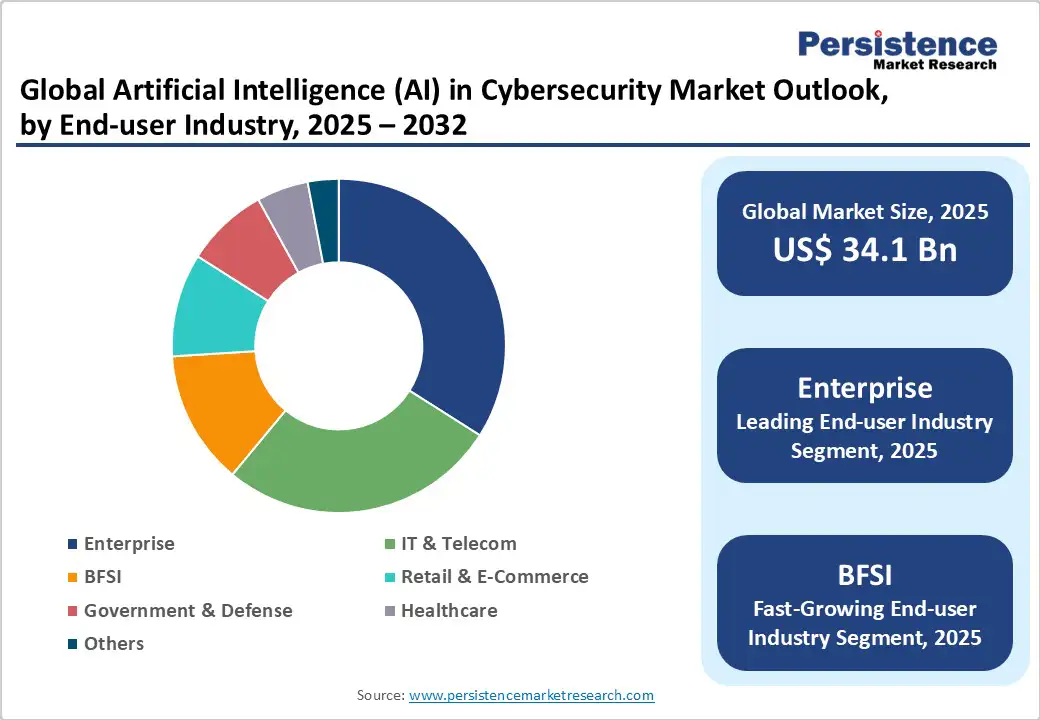

The global artificial intelligence (AI) in cybersecurity market size is likely to be valued at US$34.1 billion in 2025. It is estimated to reach US$234.3 billion by 2032, growing at a CAGR of 31.7% during the forecast period 2025 - 2032, driven by increasing cyber threats and the adoption of AI for real-time threat detection and response.

Market growth is underpinned by the proliferation of connected devices, regulatory pressures, and advancements in AI technologies such as machine learning and natural language processing, which enable enhanced cyber defense.

Key Industry Highlights

- Dominant & Fastest-growing Security Types: Software solutions are poised to dominate the market, with an estimated 45% market share in 2025.

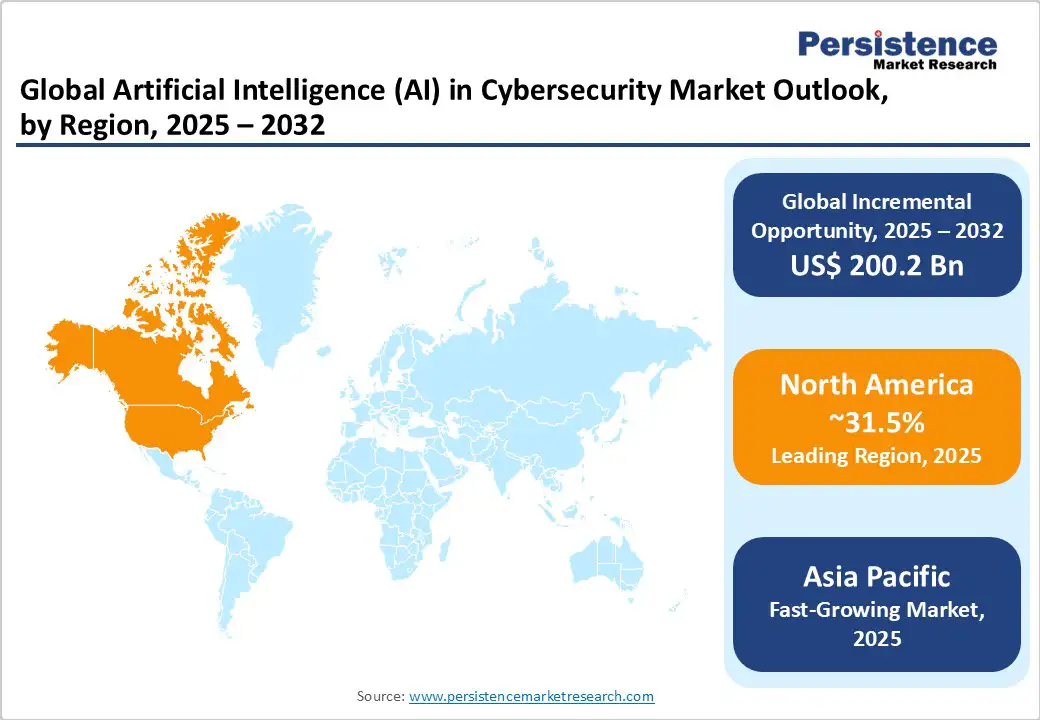

- Leading Region: North America is expected to hold a 31.5% market share in 2025, driven by the U.S.'s leadership in technology and regulatory frameworks.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, due to digital transformation drives and government support.

- Fastest-growing Offering Type: Hardware is the fastest-growing segment, driven by IoT and edge computing.

- Notable Development: In September 2025, Terra Security raised US$30 million in a Series A funding round to further develop its AI-driven continuous penetration testing platform using dozens of adaptive “ethical hacker-style” AI agents.

| Key Insights | Details |

|---|---|

|

Artificial Intelligence (AI) in Cybersecurity Market Size (2025E) |

US$34.1 Bn |

|

Market Value Forecast (2032F) |

US$234.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

31.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

21.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Frequency and Sophistication of Cyberattacks

The global surge in cyberattack activity, such as ransomware, phishing, and insider threats, signals a new era of risk, where attackers employ AI and advanced social engineering techniques to bypass traditional defenses. Notably, ransomware incidents reported by agencies such as the U.S. Cybersecurity and Infrastructure Security Agency (CISA) have doubled over the last two years, reflecting both increased frequency and sophistication of methods deployed by cybercriminals. Organizations are responding by investing in AI-powered cybersecurity platforms that can ingest and analyze terabytes of diverse data sources in real-time, enabling instant anomaly detection and automated responses to evolving threats. This paradigm shift is redefining enterprise security architecture and serves as a direct catalyst for robust market expansion, as businesses intensify their spending to safeguard digital assets amid a climate of escalating risks.

The dramatic proliferation of the Internet of Things (IoT) is transforming the global cyber risk landscape, with industry research from the International Telecommunication Union (ITU) anticipating over 30 billion connected devices globally by 2027. Each new connected device, ranging from industrial sensors to consumer wearables, introduces new attack vectors and often operates with minimal inherent security. This complexity necessitates sophisticated, AI-driven cybersecurity solutions that can protect networks and endpoints in highly distributed environments. The industrial and enterprise sectors are grappling with the challenge of scaling security as heterogeneous device ecosystems multiply. The implementation of AI technologies optimized for real-time, adaptive threat detection is accelerating market growth, embedding intelligent security into the backbone of next-generation manufacturing, healthcare, energy, and smart cities.

High Initial Investments and Operational Costs

Adopting AI-powered cybersecurity requires substantial upfront expenditure across hardware, advanced software licenses, integration services, and ongoing operations, posing a critical barrier for small and mid-sized businesses. Maintaining state-of-the-art security solutions further entails expenses related to system upgrades, threat intelligence subscription, and the hiring of specialized personnel. Data from Forrester reveals that 38% of firms cite budget constraints as the primary hurdle to AI security adoption, underscoring the need for new pricing models, such as pay-per-use frameworks and modular service offerings, to enable more sustainable deployments and broaden market accessibility.

Integrating AI-driven security solutions with legacy IT infrastructure and disparate cybersecurity tools remains an industry-wide challenge, often resulting in fragmented visibility and suboptimal threat response. Industry analysts indicate that upward of 42% of cybersecurity failures stem from integration difficulties, as inconsistent data standards and non-standardized communication protocols impede smooth workflow and holistic protection. Addressing these integration bottlenecks demands further innovation around interoperability standards, API design, and unified security management platforms to minimize security gaps and foster streamlined, efficient operations.

Digital Transformation of Emerging Economies

Major economies, such as India, China, and the ASEAN bloc, are undergoing historic digital expansions, marked by government investments in cloud infrastructure, smart manufacturing, and next-gen financial services. These regions present unprecedented opportunities for AI-driven cybersecurity, buoyed by accelerating internet penetration and policy emphasis on building cyber resilience. The Asia Pacific AI in cybersecurity market, in particular, is becoming a multi-billion-dollar opportunity for vendors offering scalable, language-agnostic, and region-specific AI security tools, especially in the banking, healthcare, and public infrastructure sectors.

As enterprises transition critical workloads to the cloud, the demand for AI-enhanced security-as-a-service platforms is rapidly intensifying. These solutions provide cost-effective, highly scalable defenses against cloud-specific threats, including data leakage, advanced persistent threats, and configuration vulnerabilities. Generative AI models are further revolutionizing cybersecurity by simulating new classes of attack vectors, predicting threat evolution, and automating rapid incident response scenarios. The adoption of generative AI in cybersecurity is producing measurable improvement in detection rates and shortening breach containment times, especially for highly targeted enterprise environments. Firms investing in these advanced tools are gaining competitive differentiation, as generative AI becomes integral to future-ready platforms, creating a vibrant, fast-growing subset within the larger AI cybersecurity market.

Category-wise Analysis

Offering Insights

Software solutions are expected to dominate the market, accounting for approximately 45% of the total revenue share in 2025, due to their inherent flexibility, rapid deployment capabilities, and robust ability to integrate with analytics and visualization frameworks. Innovations in AI-powered software platforms, featuring advanced machine learning, natural language processing, and autonomous decision engines, are driving automation across detection, analysis, and active defense layers in enterprise IT ecosystems.

Hardware, such as dedicated AI processors and edge devices, is the fastest-growing offering segment, with more than 32% CAGR expected through 2032. Their role in enabling real-time cyber defense at the edge is escalating, especially for systems handling sensitive industrial or mission-critical data streams.

Security Type Insights

Network security stands central, forecast to comprise around 37% of the AI in cybersecurity market revenue share in 2025. The demand for AI-enhanced network firewalls, intrusion prevention solutions, and encrypted virtual private networks (VPNs) is surging as organizations fortify infrastructure against increasingly sophisticated threat campaigns.

With the migration toward cloud platforms and hybrid architectures, the cloud security segment is positioned for exceptional growth from 2025 through 2032. Advanced AI enables continuous monitoring, real-time anomaly detection, and adaptive security controls specifically tailored to the dynamic nature of cloud computing environments.

End-user Industry Insights

Enterprises represent the largest segment of end-users, harnessing AI to secure complex, geographically distributed networks, endpoints, and applications against a multifaceted threat landscape. Their ability to invest at scale and adapt solutions to stringent regulatory frameworks underlines their predominant market position.

The banking, financial services, and insurance (BFSI) sector is anticipated to achieve a CAGR of approximately 27% between 2025 and 2032, propelled by the critical need to detect fraud, enforce risk controls, and maintain compliance in environments managing vast volumes of confidential financial data.

Regional Insights

North America Artificial Intelligence (AI) in Cybersecurity Market Trends

North America is projected to retain its commanding position with an estimated 31.5% of the AI in cybersecurity market share in 2025, driven by a mature ICT infrastructure, widespread high-speed connectivity, and early adoption of advanced cyber defense technologies, including generative AI, supervised machine learning, and natural language processing within enterprise-grade security solutions.

North America’s leadership is further enabled by a robust regulatory environment, steered by the California Consumer Privacy Act (CCPA), White House Executive Orders on AI, and other federal mandates, which set clear guidelines for data protection and incentivize investments in AI-driven threat detection and governance. The market is powered by substantial R&D and venture capital funding, a concentration of global leaders, such as AWS, IBM, Palo Alto Networks, CrowdStrike, and Fortinet, and high-value partnerships between government, academic, and private sector entities.

Europe Artificial Intelligence (AI) in Cybersecurity Market Trends

The Europe AI in cybersecurity market is experiencing robust and sustained expansion, underpinned by stringent regulatory requirements, including the GDPR, NIS Directive, and the landmark EU AI Act, which collectively enforce rigorous data protection, transparency, and cross-border harmonization across member states.

Core innovation clusters located in Germany, the U.K., and France are driving market growth, benefiting from major government investments such as the U.K.’s US$200 Million annual allocation for AI-based cyber defense and the European Commission’s Horizon Europe program, which channels over US$1 Billion yearly into AI research and security infrastructure. These nations lead in developing and deploying AI cybersecurity solutions for critical infrastructure and the rapidly growing IoT ecosystem, positioning themselves at the vanguard of threat detection and response capabilities. Managed AI security services and compliance platforms are particularly strong growth drivers, with over 70% of the U.K.

SMEs rely on third-party providers for automated threat detection, incident response, and compliance audits, leveraging the scalability and cost-effectiveness of outsourced solutions that can reduce operational costs while dramatically improving threat visibility and response times.

Asia Pacific Artificial Intelligence (AI) in Cybersecurity Market Trends

Asia Pacific is leading the global acceleration of the AI in cybersecurity market, with an estimated CAGR of 33% from 2025 to 2032, driven by major government-backed cyber resilience strategies and soaring investments from domestic and multinational enterprises in digital transformation. Rapid digitalization in China, India, and Indonesia is fueling widespread adoption of cloud services, IoT devices, and AI-based security platforms across industrial manufacturing, healthcare, and financial services, where operational technology networks are increasingly shielded by advanced machine learning and agentic AI systems.

Regulatory evolution in data privacy and security, such as Singapore’s PDPA, India’s DPDP Bill, and China’s Cybersecurity Law, promotes deeper collaboration among local enterprises, global tech vendors, and government agencies, pushing the adoption of scalable, localized AI security solutions. Notably, region-specific innovations in the form of multi-agent orchestration and governance-by-design are bridging technology gaps and facilitating compliance with diverse sovereignty laws, ensuring Asia Pacific rapidly emerges as a global hub for AI-driven cyber defense and threat intelligence.

Competitive Landscape

The global artificial intelligence (AI) cybersecurity market is moderately consolidated, with around half of the market share controlled by global leaders such as IBM, AWS, Fortinet, and Darktrace, which are recognized for their comprehensive product suites and significant R&D investments.

The remainder consists of a highly fragmented ecosystem of specialized vendors that deliver targeted, innovative solutions addressing niche avenues such as generative AI, privacy-preserving ML, and vertical-specific threat defense. Market competition is fierce, with frequent strategic alliances, acquisitions, and geographic expansion, fueling continuous advancements in the breadth and depth of AI cybersecurity offerings globally.

Key Industry Developments

- In July 2025, Google’s AI agent Big Sleep detected and prevented a critical SQLite zero-day vulnerability (CVE-2025-6965), marking the first instance of an AI proactively thwarting a cybersecurity threat in real time using predictive threat intelligence.

- In July 2025, Accenture and Microsoft announced a co-investment in generative AI cybersecurity tools, aiming to modernize security operations, protect data, streamline migrations, and enhance identity management, helping clients reduce costs, improve efficiency, and counter advanced cyber threats.

- In June 2025, IBM integrated watsonX.governance and Guardium AI Security into a unified solution for generative AI risk management, offering AI agent monitoring, automated red-teaming, compliance with frameworks such as the EU AI Act, and discovery of new AI use cases across cloud, code, and embedded systems.

Companies Covered in Artificial Intelligence (AI) in Cybersecurity Market

- IBM Corporation

- Amazon Web Services, Inc.

- Fortinet, Inc.

- Darktrace

- SentinelOne, Inc.

- Palo Alto Networks, Inc.

- Cylance Inc. (BlackBerry)

- Acalvio Technologies, Inc.

- Intel Corporation

- Micron Technology, Inc.

- Check Point Software Technologies

- FireEye, Inc.

Frequently Asked Questions

The artificial intelligence (AI) in cybersecurity market is projected to reach US$34.1 Billion in 2025.

The increasing frequency and sophistication of cyberattacks and the rapid adoption of IoT and connected devices are driving the market.

The artificial intelligence (AI) in cybersecurity market is poised to witness a CAGR of 31.7% from 2025 to 2032.

The expansion of cloud-native and SaaS security solutions and the integration of generative AI for advanced threat intelligence are key market opportunities.

IBM Corporation, Amazon Web Services, Inc., and Fortinet, Inc. are some of the key players in the artificial intelligence (AI) in cybersecurity market.