- Technology

- Artificial Intelligence (AI) Chipsets Market

Artificial Intelligence (AI) Chipsets Market Size, Share, and Growth Forecast, 2025 - 2032

Artificial Intelligence (AI) Chipsets Market Chipset Type (Graphics Processing Units, Central Processing Units, Others), Computing Technology (Cloud AI Computing, Edge AI Computing), AI Workload Type, End-user, and Regional Analysis for 2025 - 2032

Artificial Intelligence (AI) Chipsets Market Size and Trends Analysis

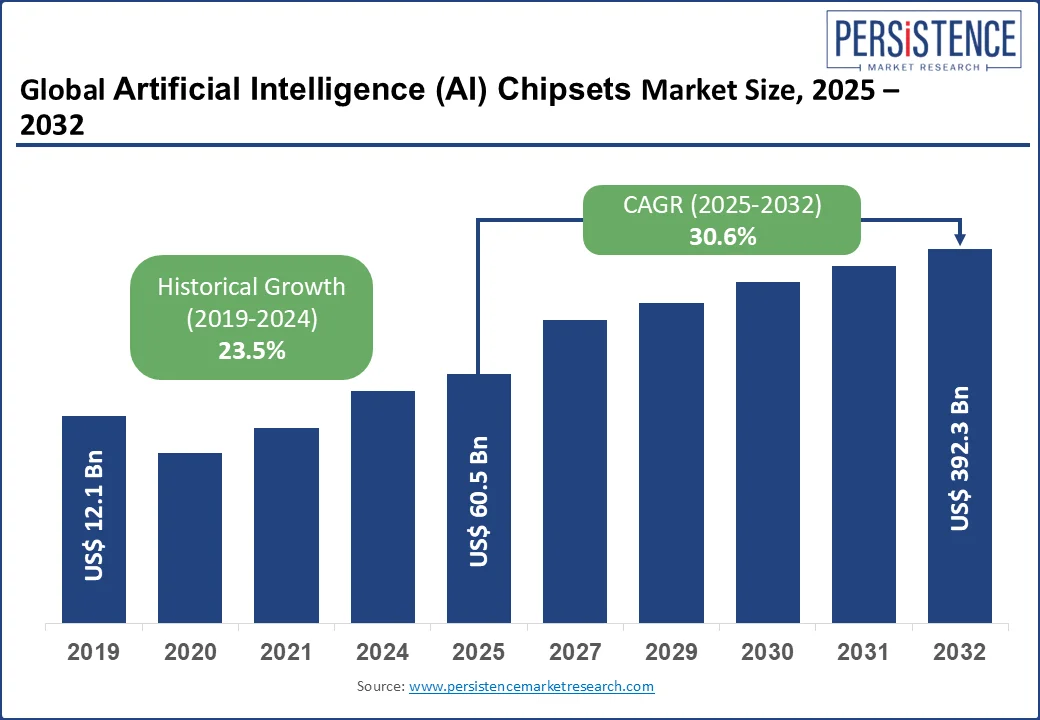

The global Artificial Intelligence (AI) chipsets market size is likely to be valued at US$ 60.5 Bn in 2025 and is estimated to reach US$ 392.3 Bn in 2032, growing at a CAGR of 30.6% during the forecast period 2025 - 2032. AI chipsets are specialized hardware designed to accelerate AI-related tasks such as machine learning (ML), deep learning (DL), and neural network processing. The Artificial Intelligence (AI) chipsets market is driven by rapid adoption of AI across industries, rising demand for edge computing, and continuous innovations in chip architecture to support data-intensive applications.

Key Industry Highlights:

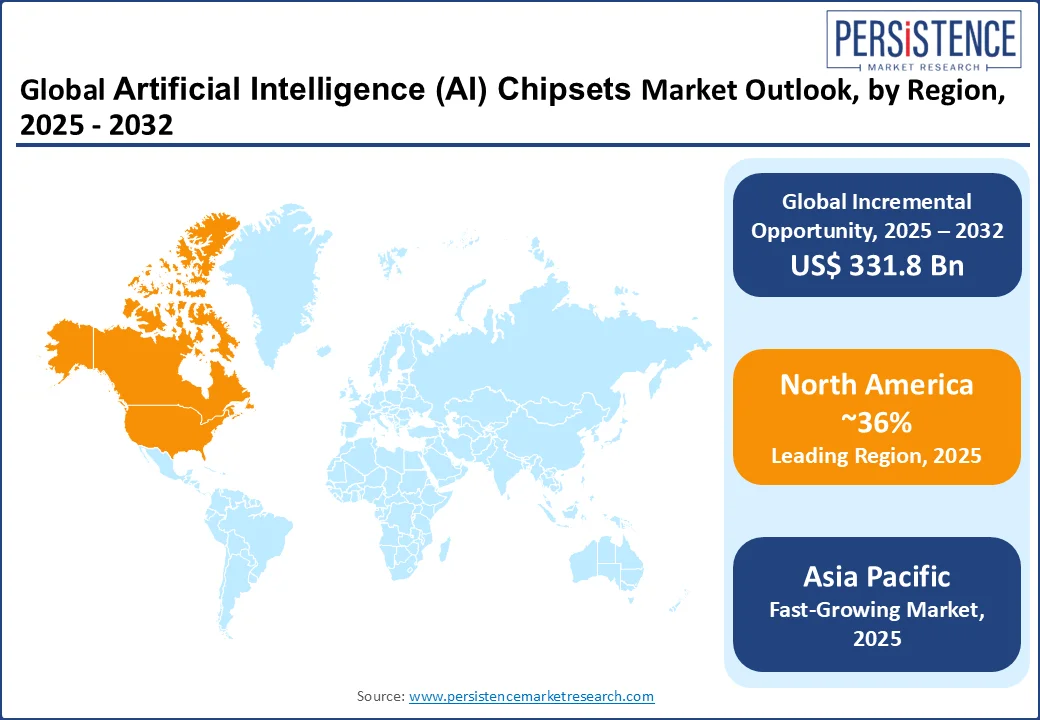

- Artificial Intelligence (AI) Chipsets: North America holds an estimated share of over 36% in 2025, due to its strong tech ecosystem, substantial R&D investments, and dominance of key players such as NVIDIA, Intel, and AMD.

- Emergence of AI Infrastructure in APAC: Asia Pacific is witnessing rapid growth, driven by rising demand for smart devices, government-led digitalization initiatives, and increasing investments in AI infrastructure and data centers.

- Investment Opportunities in Europe: Europe’s AI chip market is formed by low-power computing mandates and the €43B European Chips Act, which focuses on supply chain security and green innovation in sectors such as automotive and industrial automation.

- Leading Chipset Type: Graphics processing units (GPUs) are anticipated to capture the largest market share with approximately 35% due to their parallel processing capabilities, which are ideal for efficiently handling complex AI and machine learning workloads.

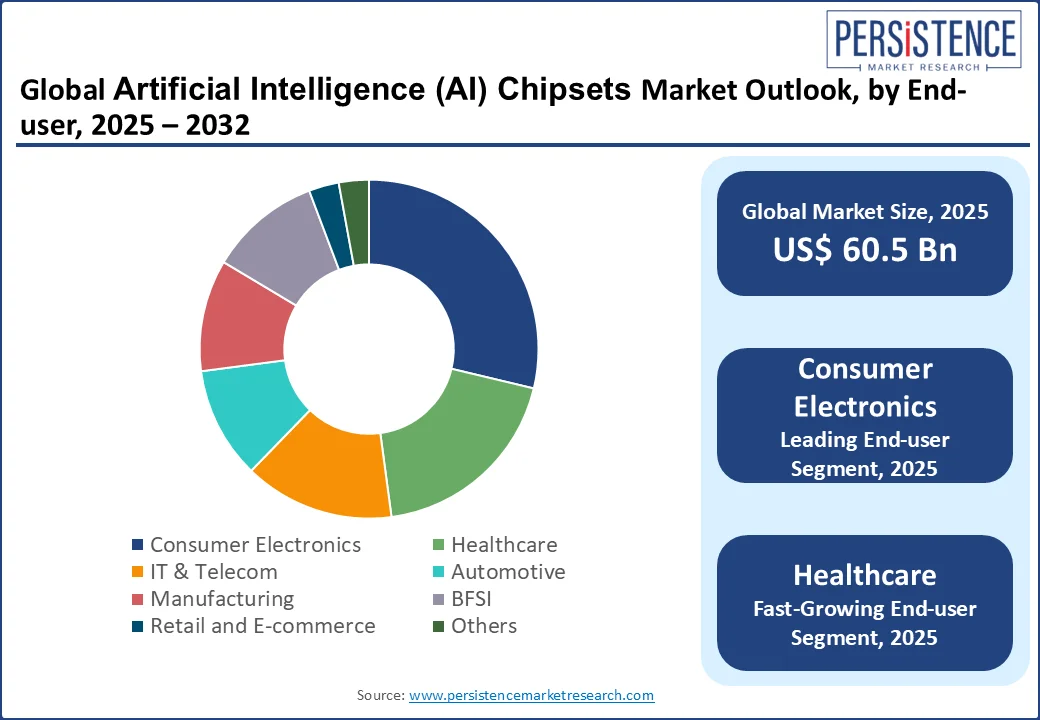

- Dominant End-user Category: Consumer electronics is projected to dominate the end-user segment with an estimated share of 30% driven by growing demand for smart features in devices such as smartphones, smart TVs, and wearables, requiring efficient on-device AI processing.

- Trend: The industry is shifting toward application-specific integrated circuits (ASICs) to improve performance, power efficiency, and workload optimization, with companies such as Google, Meta, and Tesla designing in-house chips to reduce dependency on third-party vendors.

|

Global Market Attribute |

Key Insights |

|

Artificial Intelligence (AI) Chipsets Market Size (2025E) |

US$ 60.5 Bn |

|

Market Value Forecast (2032F) |

US$ 392.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

30.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

23.5% |

Market Dynamics

Driver - Surging Adoption of Edge Computing Fuels AI Chipset Demand

The growing adoption of edge computing is significantly boosting demand for Artificial Intelligence (AI) chipsets. By enabling real-time data processing close to the data source, edge computing reduces reliance on cloud servers and supports latency-sensitive applications such as IoT devices, autonomous vehicles, industrial automation, and smart cities. This shift is pushing the need for high-performance, energy-efficient AI chipsets that can operate under power constraints while ensuring localized intelligence.

According to the Eclipse Foundation (March 2024), 33% of organizations had adopted edge computing in 2023, with 30% planning deployments and 27% actively evaluating platforms over the next two years. In March 2025, Axelera AI unveiled Titania, a high-performance, energy-efficient, and scalable AI inference chiplet. The development of this chiplet builds on Axelera AI’s innovative approach to Digital In-Memory Computing (D-IMC) architecture, which provides near-linear scalability from the edge to the cloud.

Restraint - Geopolitical Restrictions and Export Controls

Export control regulations imposed by the U.S. Bureau of Industry and Security (BIS) since 2022 have significantly disrupted the AI chipsets market. By early 2025, these rules extended to around 120 countries, limiting access to advanced AI chips, chip-making tools, and technologies. Major players such as AMD and NVIDIA have faced severe setbacks. AMD expects to lose US$ 1.5 Bn in 2025 revenue, while NVIDIA could lose up to US$ 5.5 Bn due to bans on selling high-end GPUs such as the B200 and H20 in China.

The U.S. coordination with allies such as the Netherlands has blocked the export of advanced chip-manufacturing equipment such as ASML’s EUV lithography systems, further hindering China’s semiconductor production capabilities. These measures are straining global supply chains, increasing compliance burdens, and forcing chipmakers to redesign their production and sales strategies. As a result, market expansion has slowed, and innovation in AI chip development is becoming more complex and fragmented.

Opportunity - Advances in Chip Architecture to Create Ample Opportunities

Emerging architectures such as neuromorphic computing, which mimics the human brain’s neural structure, and specialized AI accelerators such as TPUs and NPUs are enabling faster processing of complex datasets for machine learning (ML), deep learning (DL), and generative AI.

For instance, the European Innovation Council (EIC) Work Programme 2024 report states that from EUR 50 Mn (US$ 54.50 Mn), at least 30% is allocated to the Quantum Technology components. These advancements allow AI chipsets to handle the growing demands of data-intensive applications, such as real-time analytics and autonomous systems, creating new market opportunities for industries such as healthcare, automotive, and smart cities.

Key Trend

Trend - Shift to ASICs & Custom Chips

Unlike general-purpose processors such as CPUs and GPUs, ASICs are tailored for specific tasks such as AI inference and training, offering superior speed, lower latency, and reduced power consumption. This has fueled a strong trend toward adopting ASICs, as they are well-suited to handle the growing complexity of AI applications, including deep learning, natural language processing, and computer vision, all of which require specialized hardware for intensive computational workloads.

The U.S. Department of Defense, through DARPA, partnered with Intel in 2021 under the SAHARA (Structured Array Hardware for Automatically Realized Applications) program to automate the conversion of defense-relevant FPGAs into secure, domestically manufactured structured embedded Application-Specific Integrated Circuits (eASICs) built on Intel’s 10 nm process, delivering enhanced performance, reduced power consumption, and integrated security countermeasures for defense and commercial systems.

In January 2024, TSMC announced the introduction of its SoIC (System-on-Integrated-Chips) 3D-IC chip stacking services, enabling tight integration of memory (HBM stacks) and logic dies in a single package, to deliver significantly enhanced performance and energy efficiency tailored to next-generation AI workloads.

Category-wise Analysis

Chipset Type Insights

Based on chipset type, the market for artificial intelligence (AI) chipsets is segmented into graphics processing units, central processing units, field-programmable gate arrays, application-specific integrated circuits, neural processing units, and others. Among these, graphics processing units (GPUs) are expected to lead the market with around 35% share due to their massively parallel architecture, which efficiently handles matrix-heavy computations essential for deep learning and neural network training. Their scalability, high memory bandwidth, and widespread adoption in data centers and AI model development further drive demand.

Application-specific integrated circuits (ASICs) are rapidly gaining traction in hyperscale data centers and AI inference tasks due to their high efficiency and low power usage. Designed for specialized functions such as deep learning and large language models, ASICs offer performance advantages over general-purpose processors. Tech giants such as Google, Amazon, Meta, and Tesla are developing in-house AI ASICs to enhance performance and reduce reliance on suppliers such as NVIDIA. In March 2025, Meta tested its first custom AI training chip as part of this shift.

End-user Insights

Based on end-user, the market is segmented into consumer electronics, healthcare, IT & Telecom, automotive, manufacturing, BFSI, retail & e-commerce, and others. Among these, consumer electronics is anticipated to lead with the highest market share of approximately 30% driven by the high adoption of AI-enabled smartphones, smart TVs, and wearables. These devices rely on specialized chipsets for real-time image processing, voice recognition, and on-device AI tasks. The demand for energy-efficient, high-performance chips and innovations in gaming and AR/VR further fuel this dominance.

Healthcare is rapidly adopting AI chipsets to power diagnostic tools, medical imaging, and personalized treatment systems that require real-time data processing. These high-performance chips enable advanced applications such as AI-driven disease detection, drug discovery, and robotic surgeries in hospitals. Additionally, the rise of wearable health devices and remote monitoring solutions fuels demand for low-latency, energy-efficient AI chips tailored to healthcare’s stringent accuracy and reliability standards.

Regional Insights

North America Artificial Intelligence (AI) Chipsets Market Trends

North America dominates the market with an estimated share of over 36% in 2025, due to its advanced technological infrastructure, significant government and private sector investments, and the presence of leading tech companies driving innovation. The region has built a robust ecosystem for AI research and development, with major players such as NVIDIA, Intel, and Google investing heavily in next-generation AI chip architectures and expanding domestic production capabilities.

For instance, in April 2025, NVIDIA announced plans to invest up to US$ 500 Bn over four years to build AI chips and supercomputing infrastructure domestically, including relocating some chip production and packaging to new facilities in Arizona and Texas. Intel is also investing over US$100 Bn to increase domestic chip manufacturing capacity and capabilities. This investment is supported by nearly US$ 8 Bn in U.S. CHIPS Act funding and will help ensure American leadership in this industry.

These large-scale initiatives not only boost manufacturing and supply chain resilience but also accelerate innovation by providing access to advanced computing resources. This environment reinforces North America’s role as the leading region for AI chipsets and supports their deployment across key industries, ensuring the region remains at the forefront of AI adoption and development.

Asia Pacific Artificial Intelligence (AI) Chipsets Market Trends

Asia Pacific is rapidly becoming the fastest-growing region, driven by robust advancements in AI research, accelerating digital transformation across industries, and proactive government support for AI-focused initiatives. Countries including China, India, South Korea, and Japan are channeling major investments into AI infrastructure and semiconductor manufacturing to reduce reliance on imports and gain technological self-sufficiency. The region is witnessing strong demand for AI chipsets that offer low-latency data processing, real-time decision-making, high energy efficiency, and support for edge computing applications.

In June 2025, China began mass production of the world’s first non-binary AI chip at Beihang University using a Hybrid Stochastic Number (HSN) system that enhances energy efficiency and fault tolerance for critical applications such as flight systems and aircraft navigation signaling, a technological leap. South Korea allocated KRW 27.3 Bn (US$ 19.9 Mn) to develop micro data centers using domestically developed AI chips for SMEs, hospitals, and public services. This highlights the growing regional need for AI chipsets that enable localized, secure, and scalable AI deployments in data-sensitive and infrastructure-light environments.

Europe Artificial Intelligence (AI) Chipsets Market Trends

Europe has emerged as a strategically significant region, serving as both a key consumer market and an increasingly proactive innovator in AI hardware development. While Europe produces only a small share of the world’s advanced chips, it plays a critical role through companies such as ARM, Infineon, STMicroelectronics, and Graphcore, which are advancing AI accelerators, edge AI chips, and automotive-grade processors. As the region is still heavily dependent on U.S. companies such as NVIDIA for the powerful chips used to train advanced AI models, to reduce this reliance, the European Commission is pushing for AI chip production to be in Europe. This in-house production plan ties into the EU’s Chips Act, which aims to raise Europe’s share of the global chip market to 20% by 2030. A review of the plan in 2026 will look at what gaps need to be filled to make Europe more competitive.

Competitive Landscape

The global Artificial Intelligence (AI) chipsets market is consolidated, with major players such as NVIDIA, Intel, AMD, and Qualcomm dominating the landscape. Hyperscalers and innovative startups bring additional fragmentation and competition. These companies are focused on creating high-performance, energy-efficient chipsets to power AI workloads ranging from edge computing to large data centers. Strategic moves such as acquisitions, partnerships, and the development of custom AI accelerators are shaping the market, while tech giants such as Apple and Tesla are building in-house AI chips to reduce reliance on external suppliers.

Key Industry Developments

- In January 2025, Palladyne AI Corp. secured a new contract from the Air Force Research Laboratory (AFRL) to migrate its Pilot AI software platform to next-generation U.S.-made AI chipsets over 26 months starting from early 2025. The Pilot platform, designed for unmanned aerial systems, integrates real-time multi-sensor fusion and adaptive sensor management to enhance situational awareness.

- In December 2024, Google launched "Willow," a quantum chip capable of solving a complex problem in just five minutes, a task that would take the world’s fastest supercomputer 10 septillion years.

- In October 2024, AMD unveiled new AI-integrated chipsets across its Ryzen, Instinct, and Epyc product lines to compete with Intel and NVIDIA. The Ryzen AI Pro 300 Series, featuring Zen 5 and XDNA 2 architectures, powers Microsoft Copilot+ enterprise laptops and is expected to appear in over 100 platforms by 2025. AMD also introduced the Instinct MI325X accelerator for high-performance AI workloads, with shipping scheduled for early 2025, and previewed its upcoming MI350 and MI400 series.

Companies Covered in Artificial Intelligence (AI) Chipsets Market

- NVIDIA

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm

- Amazon (AWS)

- SK HYNIX INC.

- Graphcore

- Cerebras Systems

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- Baidu, Inc.

- Mythic Inc.

Frequently Asked Questions

The Artificial Intelligence (AI) chipsets market is projected to be valued at US$ 60.5 Bn in 2025.

The rising demand for high-performance, energy-efficient hardware to support edge computing and real-time data processing across industries drives the Artificial Intelligence (AI) chipsets market.

The Artificial Intelligence (AI) chipsets market is poised to witness a CAGR of 30.6% from 2025 to 2032.

Surging demand for edge AI, specialized ASICs for healthcare and automotive, and increased investments in cloud and data center infrastructure for AI workloads present key market opportunities.

NVIDIA, Advanced Micro Devices, Inc., Intel Corporation, Google, Qualcomm, Amazon (AWS), SK HYNIX INC., and Graphcore are among the leading key players.