- Metals & Minerals

- Aluminum Pigment Market

Aluminum Pigment Market Size, Share, and Growth Forecast, 2026 - 2033

Aluminum Pigment Market By Form (Powder, Paste/Aqueous Dispersion, Others), Product Type (Leafing Aluminum Pigments, Non-Leafing Aluminum Pigments, Others), Application, and Regional Analysis for 2026 - 2033

Aluminum Pigment Market Size and Trends Analysis

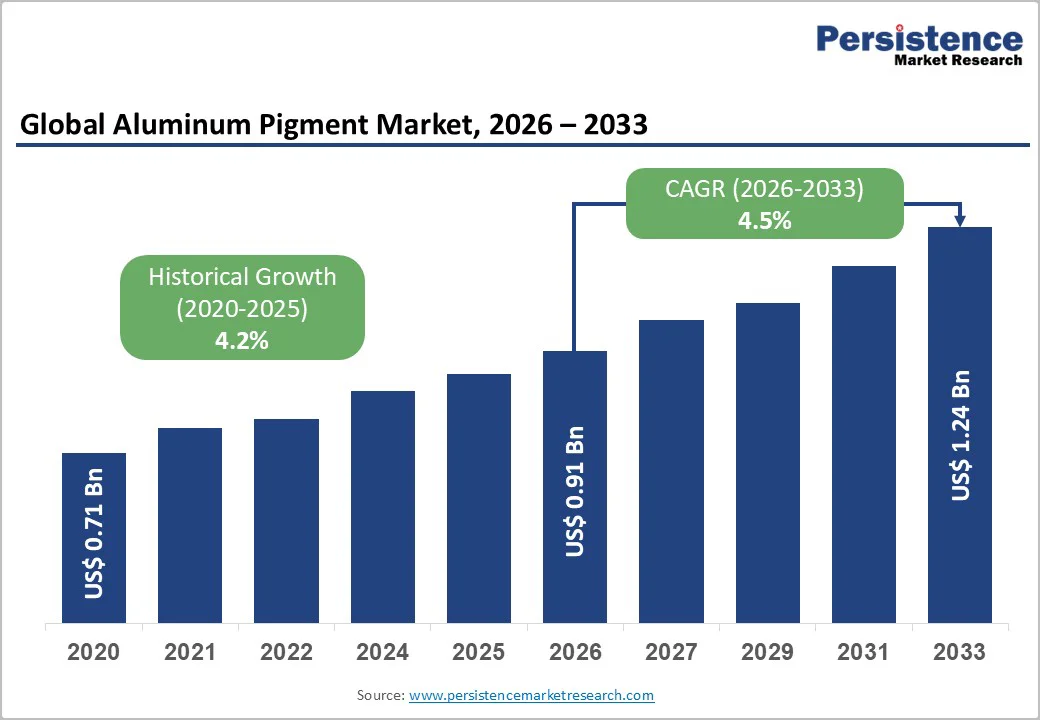

The global aluminum pigment market size is likely to be valued at US$0.91 billion in 2026 and is expected to reach US$1.66 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by rising demand for metallic finishes in automotive and consumer goods, a regulatory preference for low-VOC and waterborne coating systems that favor aluminum effect pigments, and the expanding use of reflective pigments in energy-efficient roofing and packaging. Asia Pacific remains the dominant growth engine.

Key Industry Highlights

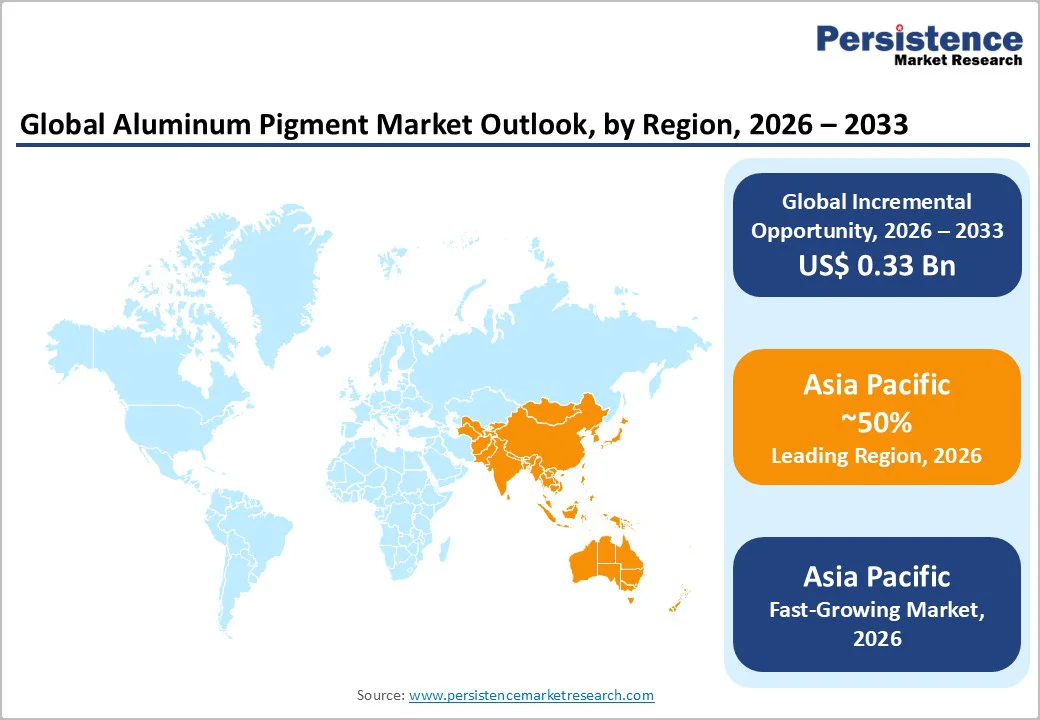

- Leading Region: Asia Pacific to remain the largest regional market with an estimated 50% share in 2026, driven by large-scale automotive production, extensive plastics manufacturing, and expanding packaging applications.

- Fastest-growing Region: Asia Pacific to record the fastest growth trajectory, supported by capacity expansions, high-volume OEM demand, and increasing adoption of waterborne-compatible pigments.

- Investment Plans: Manufacturers across North America, Europe, and Asia Pacific are prioritizing waterborne-compatible aluminum pastes, sustainable atomized feedstock, and surface-treated pigments, with multiple announced projects between 2024 and 2025 focused on capacity expansions of 10 to 20% for dispersions and high-purity non-leafing flakes.

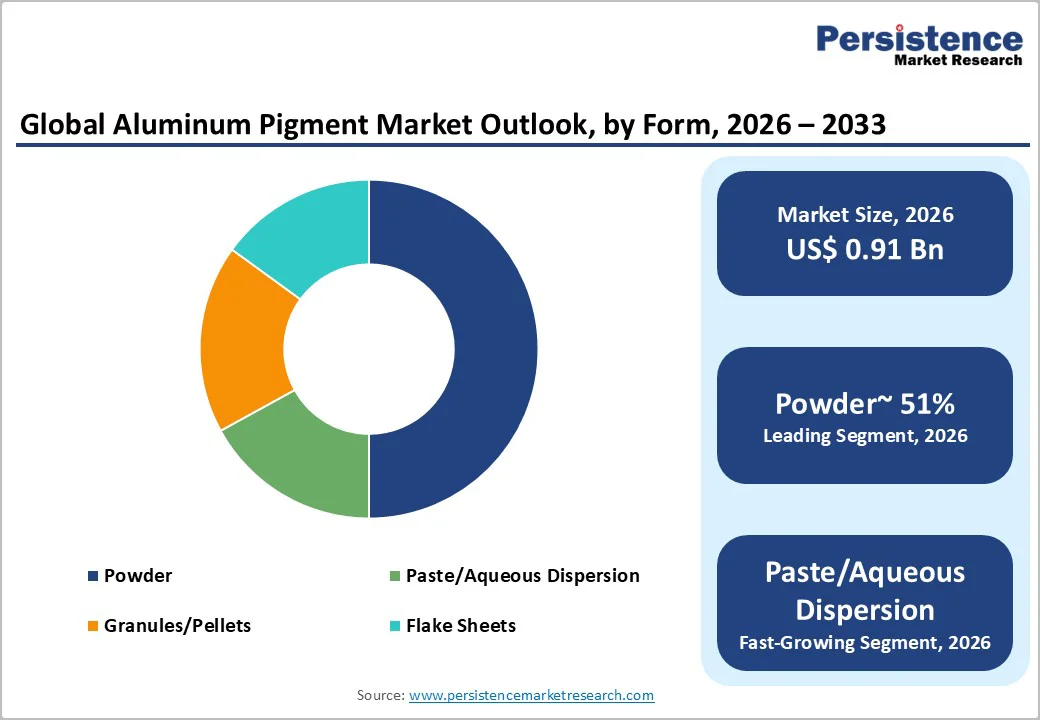

- Dominant Form Insights: Powder-form aluminum pigments to lead the global market with an estimated 51% volume share in 2026, reflecting their cost efficiency, stability, and widespread use across coatings, plastics, printing, and industrial applications.

- Leading Product Type: Leafing aluminum pigments are expected to dominate the product segment in 2026, driven by strong demand in decorative coatings, packaging inks, and industrial finishes, and are projected to account for over 50% of the market.

| Key Insights | Details |

|---|---|

| Aluminum Pigment Market Size (2026E) | US$0.91 Bn |

| Market Value Forecast (2033F) | US$1.24 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automotive and Industrial Coatings Demand for Premium Metallic Finishes

Aluminum pigments play a crucial role in producing high-quality metallic and pearlescent automotive finishes that continue to be preferred by both consumers and OEMs. Growth in exterior automotive OEM coatings and the refinish sector supports sustained demand for engineered aluminum flake and paste pigments.

Industry analyses consistently highlight automotive coatings as a major end-use category contributing to the market’s mid-single-digit growth. The shift toward powder and waterborne low-VOC formulations strengthens the requirement for advanced aluminum pigments capable of delivering a strong visual effect while maintaining environmental compliance. The current market projection relies on the documented CAGR associated with the established baseline.

Regulatory Push toward Low-VOC/Waterborne Systems and Energy-Efficient Applications

Tightening VOC limits across the EU, U.S., and multiple emerging economies continue to drive a transition from solvent-borne to waterborne and high-solids coating systems. Aluminum pigments engineered for waterborne compatibility therefore capture an additional share within compliant formulations.

Regulatory frameworks such as the EU Decopaint Directive reinforce long-term reformulation cycles that favor aqueous-ready and powder-compatible pigments. Meanwhile, reflective aluminum pigments used in cool-roof coatings and packaging contribute to energy-efficiency goals by improving thermal reflectance. Analysts frequently attribute one to two percentage points of incremental growth to these regulatory and sustainability-driven application areas.

Expansion of Cosmetics, Packaging, and Specialty Plastics

Cosmetics (metallic eye shadows, lip products), flexible packaging, and high-end plastics constitute expanding demand verticals for aluminum effect pigments. These applications leverage aluminum pigments for sparkle, visual depth, luster, and functional barrier properties. Premium personal-care launches and the adoption of metallic laminates in packaging lift consumption of higher-margin paste and granule formats.

These sectors are often cited as among the fastest-growing end uses, supported by ongoing premiumization and product distinction trends. Compared with the cyclical nature of automotive demand, cosmetics and packaging offer more stable year-round consumption, contributing to improved margin stability for producers.

Barrier Analysis - Raw Material Price Volatility and Energy Intensity

Production of aluminum pigments requires high-purity aluminum feedstock and energy-intensive atomization and milling processes. Volatility in aluminum metal pricing and energy costs compresses margins and creates uncertainties in product pricing.

Fluctuations in primary and secondary aluminum supply directly influence the availability of the high-spec alloy feedstock required for premium pigment grades. Sharp input cost spikes can reduce pigment margins by several percentage points and place pressure on supply reliability for producers operating complex or specialized production lines.

Environmental, Safety, and Handling Compliance, Substitution Risks

Aluminum pigments require stringent handling due to dust-control considerations, potential flammability under certain conditions, and solvent compatibility requirements. Stricter workplace safety rules raise compliance costs for manufacturers and users.

Substitution pressure also exists from advanced organic pearlescent pigments and emerging effect nanoparticles, which can replace aluminum pigments in certain cosmetic or specialty applications. These combined factors limit market entry for smaller producers and encourage consolidation among companies with capital to invest in compliant and low-emission production systems.

Opportunity Analysis - Asia Pacific Manufacturing Scale and New Capacity Additions

Asia Pacific represents the highest-volume regional market and is expected to deliver most of the incremental global demand through the early 2030s. Growth in automotive production, coatings manufacturing, plastics processing, and packaging makes the region a central opportunity for aluminum pigment suppliers.

APAC’s expanding industrial base supports investments in local paste production, granule manufacturing, and joint ventures that reduce logistics costs and strengthen regional supply chains. Conservative estimates suggest that APAC’s incremental opportunity could reach several hundred million dollars in value over the long term.

Waterborne and Powder Coating Formulations

The global transition to low-VOC coatings generates significant scope for engineered aluminum pigments, particularly aqueous dispersions, surface-treated flakes, and powder-compatible grades. Formulators increasingly require pigments that offer high optical stability, fine particle distribution, and durable performance within waterborne and powder systems.

Suppliers capable of meeting these needs often achieve premium pricing of 10 to 20% above commodity-grade powders. Even modest conversion from solvent-borne to waterborne coatings creates a substantial incremental revenue opportunity measured in the tens of millions of dollars for producers with specialized dispersion technologies.

Category-wise Analysis

Form Insights

In 2026, powder pigments are expected to represent more than 51% of total market share, reflecting their central role in mainstream manufacturing environments. Powder-form aluminum pigments continue to hold the largest global volume share and remain foundational across coatings, plastics, and printing applications.

Their strong position is supported by long-established supply chains, straightforward storage requirements, and the ability to blend efficiently into solventborne and high-solids formulations. Industries such as general industrial coatings, architectural paints, and commodity plastics frequently rely on dry powder pigments as they offer cost-effective performance and predictable metallic effects.

For instance, many extrusion-grade plastics and offset printing inks still prefer powders due to ease of incorporation and thermal stability.

Pastes and aqueous dispersions are likely to be the fastest-growing segment in 2026, as end-use industries transition toward environmentally aligned and higher-precision formulations. Waterborne coatings, premium cosmetics, automotive OEM finishes, and specialized plastics increasingly require aluminum pigments that deliver controlled dispersion and minimal airborne dust.

Pastes offer tighter particle distribution and consistent optical effects, which are valuable in applications such as high-end automotive metallic basecoats and cosmetic shimmer formulations. Aqueous dispersions are also gaining traction in packaging inks designed for low-VOC compliance.

Published forecasts typically show pastes and dispersions growing 100 to 200 basis points faster than traditional powders, supported by their compatibility with emerging waterborne and low-solvent systems.

Product Type Insights

Leafing aluminum pigments are estimated to account for over 50% share in the market in 2026, due to their ability to create good, mirror-like metallic effects by orienting near the surface of the coating layer. This optical behavior is essential for decorative paints, metallic inks, industrial equipment finishes, and traditional automotive refinishes.

Applications such as reflective road marking paints, premium packaging foils, and decorative household items rely heavily on leafing pigments to achieve sharp brilliance and high reflectivity. Manufacturers with robust milling and particle-shape control, such as those supplying leafing grades for reflective industrial coatings, have held long-term dominance in this segment.

The continued popularity of conventional metallic finishes supports sustained demand for leafing grades.

Non-leafing and surface-treated aluminum pigments are likely to post the fastest growth in 2026, due to their versatility and compatibility with modern performance requirements. Unlike leafing grades, non-leafing pigments disperse uniformly within coatings, enabling softer metallic effects for automotive plastics and protective topcoats.

Surface treatments such as silane, polymer coatings, and encapsulation improve chemical stability, moisture resistance, and UV durability. These pigments are increasingly used in waterborne automotive coatings, premium packaging inks, scratch-resistant powder coatings, and weather-stable plastics. Ongoing innovation, particularly for exterior automotive trim and consumer electronics, positions this segment as the most dynamic and future-ready within the market.

Regional Insights

North America Aluminum Pigment Market Trends - Premium Automotive, Aerospace, and Waterborne-Compatible Pigment Advancements

North America remains a high-value market distinguished by mature automotive coatings, aerospace finishing systems, and engineered plastics applications. Although overall growth is more moderate compared with Asia Pacific, the region’s stringent OEM performance standards sustain demand for premium aluminum pigments with controlled particle morphology and high optical stability.

The U.S. accounts for the majority of regional consumption due to its strong automotive manufacturing base, refinish sector, industrial coatings production, and the presence of several specialty pigment suppliers. Regulatory frameworks, including U.S. VOC limits, energy-efficiency programs, and workplace safety rules, continue to accelerate reformulation toward waterborne, low-solvent, and powder-compatible pigment systems.

The competitive landscape features established producers enhancing dispersion technologies and expanding region-specific grades tailored for automotive OEMs and aerospace coatings. Recent developments reflect an emphasis on sustainability and waterborne compatibility.

For example, in February 2025, a leading U.S. pigment manufacturer announced an upgrade to its Midwest plant to expand capacity for waterborne-ready aluminum pastes targeting automotive basecoats.

In July 2024, a North American coatings supplier formed a partnership with a specialty metals producer to co-develop low-emission pigments for industrial equipment coatings. These investments highlight the region’s strategic focus on technical capability, shorter lead times, and environmentally aligned formulations.

Europe Aluminum Pigment Market Trends - High-Spec Coatings Innovation Driven by VOC Policies and Sustainability Standards

Europe continues to serve as a global hub for high-specification coatings and pigment technology development. Markets in Germany, the U.K., France, Italy, and Spain support strong demand from automotive OEM coatings, industrial finishing, packaging inks, and decorative applications.

Strict environmental policies, including VOC directives and solvent-reduction frameworks under EU regulations, drive ongoing transitions to advanced non-leafing, surface-treated, and aqueous-compatible aluminum pigment grades. European manufacturers lead in surface-treatment innovation, offering high-durability flakes engineered for UV stability, scratch resistance, and improved dispersion behavior in waterborne systems.

Innovation is consistently showcased across regional exhibitions and technical conferences, where European producers highlight developments in abrasion-resistant pigments, polymer-encapsulated aluminum flakes, and low-carbon metallic effects for luxury packaging.

Recent examples illustrate this momentum: in March 2025, a Germany-based pigment manufacturer launched a new line of ultra-low-VOC aqueous dispersions for premium packaging inks; in late 2024, a major U.K. coatings group announced a collaborative R&D program focused on recycled aluminum feedstock tailored for automotive refinishes.

Investments across Europe increasingly emphasize low-carbon supply chains, reduced-emission atomization technologies, and localized production strategies aligned with EU sustainability requirements.

Asia Pacific Aluminum Pigment Market Trends - Leading Growth Driven by Industrial Expansion, Waterborne Adoption, and Advanced Pigment Production

Asia Pacific stands as the largest and fastest-growing regional market with an estimated 50% of market share, driven by rapid industrialization, high automotive manufacturing output, fast-expanding plastics production, and the scale of the packaging sector. China commands the largest share, both as a consumer and producer, supported by a strong domestic pigment manufacturing ecosystem.

Japan and South Korea contribute high-value, precision-engineered pigments for automotive and electronics applications, while India continues to record strong annual demand growth driven by capacity expansions, joint ventures, and the emergence of sustainable atomization projects. ASEAN economies provide strategic hubs for export-oriented manufacturing and flexible production networks serving regional demand.

Regulatory conditions vary widely, with countries implementing VOC and environmental standards at different paces, creating a mix of conventional solvent borne markets and rapidly growing waterborne opportunities. Competitive dynamics include global manufacturers, established Chinese producers, and cost-efficient emerging players.

Recent developments highlight the region’s investment-driven trajectory. In January 2025, a leading Chinese pigment producer announced a new production line for high-purity non-leafing flakes used in next-generation automotive coatings.

During mid-2024, a Japanese chemicals company introduced a polymer-coated aluminum pigment series for electronics housings requiring enhanced corrosion resistance. In India, a 2025 joint venture between a domestic metals company and a European pigment supplier focused on expanding sustainable paste production for industrial coatings. These investments reinforce Asia Pacific’s position as the most dynamic regional growth center.

Competitive Landscape

The global aluminum pigment market is moderately consolidated and consists of global specialty leaders supported by a wide set of regional manufacturers. The top tier of producers controls a significant portion of the premium segment, while regional companies compete across mid-range and cost-sensitive applications.

The supply base includes firms specializing in waterborne-compatible pigments, advanced surface treatments, and high-spec flakes, alongside large regional producers supplying bulk powders and granules.

Leading companies emphasize product differentiation through surface treatments and engineered dispersions, vertical integration to improve feedstock security, and expansion of regional production to support local supply chains. Sustainability certification, tailored service models, and licensing of specialty pigment technologies are becoming increasingly central elements of competitive strategy.

Key Industry Developments

- In December 2024, ECKART and Runaya announced a joint venture to build a sustainable spherical atomized aluminum granules facility in Odisha, India, aiming to supply high-end effect pigments for aerospace, solar, and premium coating applications.

- In January 2024, ALTANA AG completed the acquisition of Silberline Manufacturing Co., thereby expanding its effect-pigment business globally and strengthening regional production capabilities in North America and Asia.

Companies Covered in Aluminum Pigment Market

- Silberline Manufacturing Co.

- Carl Schlenk AG

- Toyal Aluminum (Toyo Aluminium K.K.)

- Sun Chemical Corporation

- Zhangqiu Metallic Pigment Co., Ltd.

- Altana AG

- Sino-Dragon Metallic Pigment Co. Ltd.

- Asahi Kasei Chemicals Corporation

- AVL Metal Powders n.v.

- Nippon Light Metal Holdings Co., Ltd.

- Carlfors Bruk AB

- Metaflake Ltd.

- ESPI Metals

- Meilian Chemical Co., Ltd.

- ECKART GmbH

- Rusolut Metallic Pigments

- Wuhan Wenlin Technology Co., Ltd.

- Henan Yuanyang Aluminium Industry Co., Ltd.

- Arasan Aluminium Industries Pvt. Ltd.

- Metallic Pigments Manufacturing Company (MPMC)

Frequently Asked Questions

The global aluminum pigment market size is estimated to be US$0.91 billion in 2026.

By 2033, the aluminum pigment market is expected to reach US$1.24 billion.

Key trends include the shift toward waterborne and low-VOC formulations, rapid growth in pastes and aqueous dispersions, expansion of surface-treated non-leafing pigments, and increased emphasis on sustainable aluminum feedstock.

Powder-form aluminum pigments hold the leading share, accounting for 52% of global volume due to their stability, storage benefits, and established use across coatings, plastics, and printing applications.

The aluminum pigment market is projected to grow at a CAGR of 4.5% between 2026 and 2033.

Major companies include Silberline Manufacturing Co., Carl Schlenk AG, Sun Chemical Corporation, Toyal America/Toyo Aluminium, and Zhangqiu Metallic Pigment Co. Ltd.