- Metals & Minerals

- Aluminum Die Casting Market

Aluminum Die Casting Market Size, Share, and Growth Forecast, 2025 - 2032

Aluminum Die Casting Market by Production Process Type (Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, Gravity Die Casting), Application (Transportation, Industrial, Telecommunication, Energy, Consumer Durables), and Regional Analysis for 2025 - 2032

Aluminum Die Casting Market Size and Trends Analysis

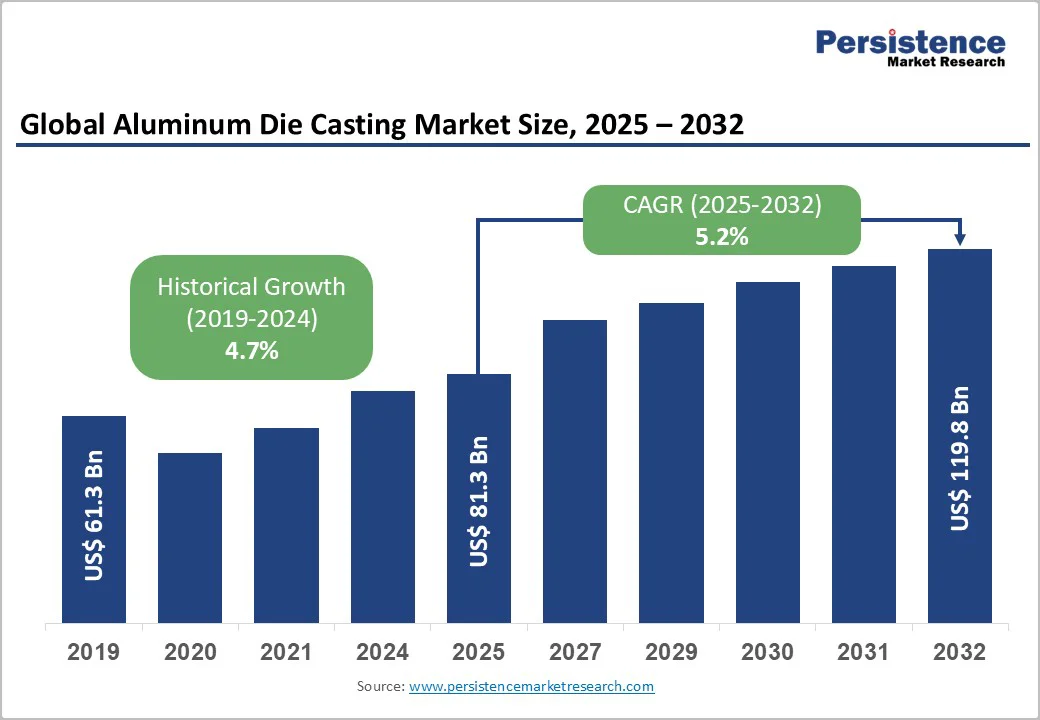

The global aluminum die casting market size is likely to be valued at US$81.3 Bn in 2025 and reach US$119.8 Bn by 2032, registering a CAGR of 5.7% during the forecast period 2025 - 2032. Driven by the rising demand for lightweight materials in transportation, advancements in casting technologies, and increasing adoption of sustainable manufacturing solutions, the aluminum die casting market has experienced robust growth. The industry expansion is further supported by global efforts to reduce vehicle emissions and enhance energy efficiency across industrial applications.

Key Industry Highlights:

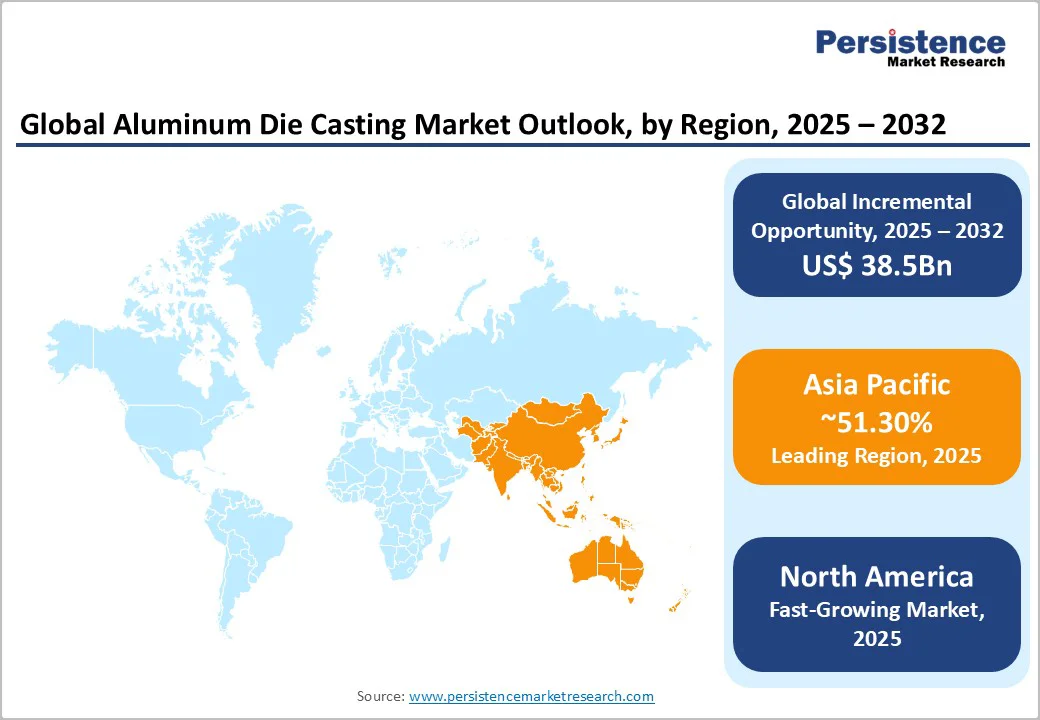

- Leading Region: Asia Pacific is likely to register a 51.30% market share in 2025, driven by rapid industrialization, high automotive production volumes, and widespread adoption of advanced casting technologies in countries such as China and India.

- Fastest-growing Region: North America is poised to experience fastest growth, propelled by increasing investments in electric vehicle (EV) production, advanced manufacturing infrastructure, and supportive government policies.

- Dominant Production Process Type: Pressure die casting is expected to account for approximately 73% of the share in 2025, driven by its critical role in high-volume production for automotive and industrial applications.

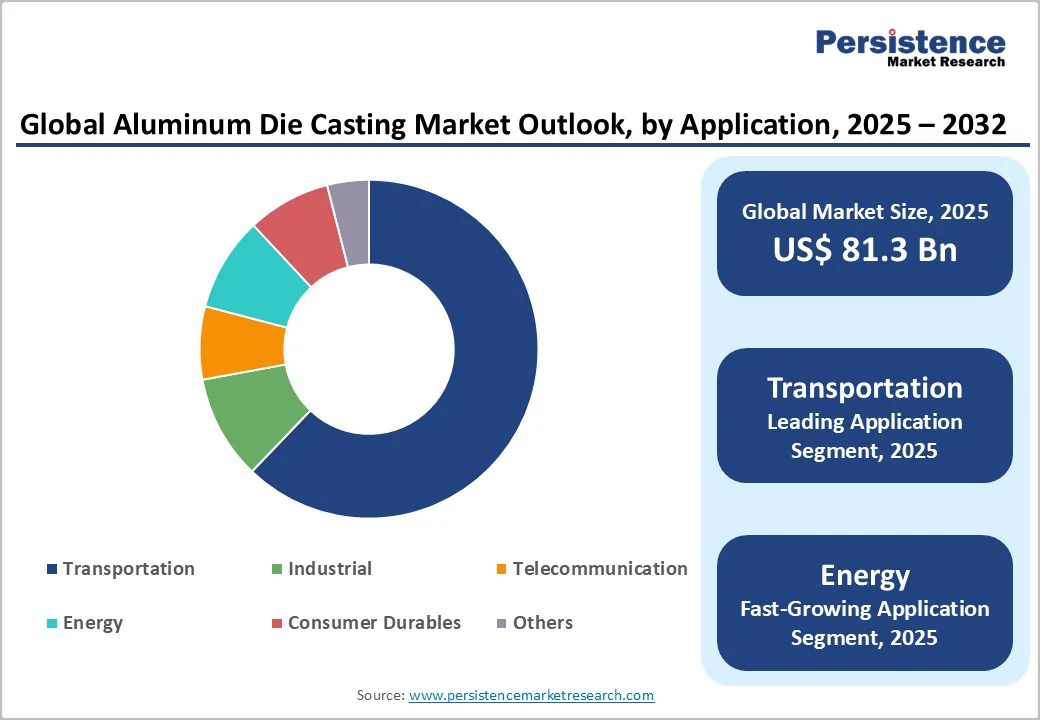

- Leading Application Type: Transportation leads with a 62.4% share, reflecting its widespread use in automotive and aerospace manufacturing.

| Key Insights | Details |

|---|---|

|

Aluminum Die Casting Market Size (2025E) |

US$81.3 Bn |

|

Market Value Forecast (2032F) |

US$119.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.7% |

Market Dynamics

Drivers - Rising Demand for Lightweight Materials and Technological Advancements Push Demand

The global surge in demand for lightweight materials, particularly in the transportation sector, is a primary driver of the aluminum die casting market. According to the International Energy Agency (IEA), the automotive industry faces stringent emission standards, with global CO2 regulations targeting a significant reduction in vehicle emissions by the end of the decade. Aluminum die casting, renowned for its lightweight and durable properties, is crucial for manufacturing components such as engine blocks, transmission housings, and structural frames, thereby reducing vehicle weight considerably compared to steel-based alternatives. China’s Ministry of Industry and Information Technology reported that lightweight materials, including aluminum, have improved fuel efficiency in electric vehicles (EVs), highlighting the need for advanced die-casting solutions.

Technological advancements in die-casting processes are significantly boosting market growth. Modern systems, such as high-pressure die-casting machines from companies such as Ryobi Limited, offer enhanced precision, reduced cycle times, and improved material efficiency. A study published in the International Journal of Advanced Manufacturing Technology found that automated die-casting systems lowered defect rates compared to traditional methods. Innovations such as real-time process monitoring and IoT-enabled casting equipment further enhance production efficiency, particularly in high-volume manufacturing settings across Asia Pacific.

Government initiatives and increased funding for advanced manufacturing are key growth drivers. In China, programs such as Made in China have expanded investments in high-precision die-casting technologies, increasing demand for automated systems. In India, initiatives such as the Atmanirbhar Bharat program promote domestic manufacturing, encouraging the adoption of aluminum die-casting for automotive and industrial applications. These policies, coupled with growing EV production, are driving market expansion in the region.

Restraints - High Initial Costs and Skilled Personnel Requirements Restrict Adoption

The high initial cost of aluminum die-casting equipment remains a significant barrier, particularly for small- and medium-sized enterprises (SMEs). Advanced die-casting machines, equipped with automation and real-time monitoring, require substantial upfront investment. Ongoing costs for molds, maintenance, and quality control further increase the total cost of ownership. In regions such as Sub-Saharan Africa and parts of Latin America, where manufacturing budgets are limited, these financial constraints restrict access to advanced die-casting technologies, even amidst growing industrial demand. The World Bank has noted that high capital costs can deter smaller manufacturers, highlighting cost as a barrier to adoption in many markets.

The requirement for skilled personnel to operate and maintain die-casting systems also hinders market growth. Operating advanced systems, such as vacuum and high-pressure die-casting machines, demands specialized training. A recent survey by the Asia Pacific Manufacturing Association reported a shortage of certified technicians in the region, with a majority of manufacturers citing a lack of skilled labour as a challenge. This skills gap, combined with high training costs, limits the adoption of advanced die-casting systems in developing markets, slowing market expansion.

Opportunities - Innovation in Automation and Sustainable Casting Boosts Consumption

The development of automated and energy-efficient aluminum die-casting systems presents significant growth opportunities, enabling deployment in high-volume production and resource-constrained environments. These systems address the limitations of traditional casting methods, making them ideal for industries requiring precision and scalability. For example, Chongqing CHAL Precision Aluminium’s recently launched automated high-pressure die-casting system reduces cycle times, supporting its use in both automotive and industrial settings. As manufacturers prioritize cost-effective and sustainable solutions, demand for such systems is rising, particularly in the Asia Pacific’s expanding industrial base.

The growing popularity of sustainable die-casting processes, such as vacuum die casting, provides another avenue for market expansion. These processes reduce material waste and energy consumption, aligning with global sustainability goals. A recent study in the Journal of Cleaner Production found that vacuum die-casting systems lowered energy usage compared to traditional methods, driving demand in environmentally conscious markets. The integration of digital platforms for process optimization and predictive maintenance further enhances market potential. Companies such as GF Casting Solutions are incorporating IoT-enabled systems into their equipment, enabling real-time analytics and improved efficiency, supporting growth in both developed and emerging regions.

Segmental Insights

By Production Process Type

The global aluminum die casting market is segmented into pressure die casting, vacuum die casting, squeeze die casting, and gravity die casting. Pressure die casting is a dominant, accounting for approximately 73% share in 2025, due to its critical role in producing high-volume, precision components for automotive and industrial sectors. Advanced pressure die-casting systems, such as those from BUVO Castings, are widely adopted for their speed and cost-effectiveness, making them essential in large-scale manufacturing. On the other hand, vacuum die casting is the fastest-growing segment, and is known its for high-quality, defect-free components in aerospace and energy applications. Innovations in vacuum casting technologies, such as those from Consolidated Metco, offer superior material integrity and reduced porosity, boosting adoption in high-performance industries.

By Application Type

The global Aluminum Die Casting market is divided into Transportation, Industrial, Telecommunication, Energy, and Consumer Durables. Transportation leads with a 62.40% share in 2025, driven by its widespread use in automotive and aerospace manufacturing. Aluminum die-cast components, such as engine parts and chassis, are critical for lightweight vehicle designs, with over 2 million tons of aluminum castings used annually in the global automotive sector.

Energy is the fastest-growing segment, fueled by rising demand for lightweight and durable components in renewable energy systems, such as wind turbines and solar panel frames. The increasing adoption of aluminum die-casting in energy infrastructure, supported by companies such as Chongqing CHAL Precision Aluminium, drives growth in this segment.

Regional Insights

North America Aluminum Die Casting Market Trends

North America is the fastest-growing region in the global Aluminum Die Casting market, driven by surging demand for lightweight automotive components, advanced manufacturing infrastructure, and increasing electric vehicle (EV) production. The U.S. dominates the region, with the U.S. Department of Transportation reporting a notable increase in EV production, necessitating robust die-casting solutions. Companies such as Alcast Technologies and Madison-Kipp Corporation offer innovative systems to meet automotive manufacturing needs.

Consumer preferences are shifting toward automated and sustainable die-casting systems, such as Consolidated Metco’s high-pressure casting machines, which enhance production efficiency and material quality. Stringent EPA regulations prioritize environmental sustainability, encouraging the adoption of energy-efficient casting technologies. Favorable incentives, such as the U.S. government’s Advanced Manufacturing Partnership, further drive market growth by supporting investments in lightweight material production.

Europe Aluminum Die Casting Market Trends

Europe’s market is led by Germany, the U.K., and France, driven by regulatory support and high manufacturing volumes. Germany holds a significant share, supported by strong sales from companies such as Martinrea Honsel Germany GmbH and GF Casting Solutions. The EU’s Industrial Strategy fosters innovation and compliance, promoting the adoption of advanced pressure and vacuum die-casting systems.

In the U.K., market growth is driven by demand for lightweight automotive components, with products such as Endurance Technologies’ high-precision castings gaining traction. France sees increased demand for aerospace-related die-casting, with FAIST Group offering specialized solutions. Regulatory support for sustainable manufacturing practices across Europe enhances market prospects.

Asia Pacific Aluminum Die Casting Market Trends

Asia Pacific dominates the global aluminum die casting market, expected to account for 51.3% share in 2025, driven by rapid industrialization, high automotive production, and growing adoption of advanced technologies in China and India. China remains a key growth engine, where initiatives such as Made in China 2025 boost demand for high-precision, automated die-casting systems. Domestic manufacturers such as Chongqing CHAL Precision Aluminium cater to local needs with cost-effective solutions for urban and rural settings.

In India, market expansion is supported by industrial upgrades and government programs such as Atmanirbhar Bharat, which promote domestic manufacturing. Japan’s market is characterized by demand for high-precision die-casting tools for automotive and electronics, with companies such as Ryobi Limited gaining share. Increased industrial spending, digital manufacturing platforms, and emphasis on lightweight materials make the Asia Pacific the leading hub for market growth.

Competitive Landscape

The global aluminum die casting market is highly competitive, with global and regional players competing through innovation, competitive pricing, and reliability. The rise of automated and sustainable casting systems intensifies competition, as companies strive to meet stringent regulatory standards and manufacturing demands. Strategic partnerships, mergers, and regulatory approvals are key differentiators in this dynamic market.

Key Developments:

- August 2024: A recently developed die casting machine for giga casting, which uses aluminum alloy to integrally mold body structure parts for battery electric vehicles (BEVs), was introduced by UBE Machinery Corporation, Ltd., the main company of the UBE Group's machinery business.

- In October 2023: Alloy Enterprises introduced its aluminum cold plate component with the strategic aim of expanding production capabilities. This launch supports increased manufacturing capacity, enabling the company to meet growing demand across automotive, industrial, and energy-efficient thermal management applications.

Companies Covered in Aluminum Die Casting Market

- Alcast Technologies

- BUVO Castings

- Chongqing CHAL Precision Aluminium Co., Ltd.

- Consolidated Metco, Inc.

- Endurance Technologies Limited

- FAIST Group

- GF Casting Solutions

- GIBBS

- Martinrea Honsel Germany GmbH

- Madison-Kipp Corporation

- Ryobi Limited

Frequently Asked Questions

The aluminum die casting market is projected to reach US$81.3 Bn in 2025.

Rising demand for lightweight materials, technological advancements in die-casting, and government initiatives for sustainable manufacturing are key drivers.

The aluminum die casting market is poised to witness a CAGR of 5.7% from 2025 to 2032.

Innovations in automated and sustainable die-casting systems present significant growth opportunities.

Alcast Technologies, BUVO Castings, and Ryobi Limited are among the leading players.