- Automotive Components & Materials

- Air Intake System Market

Air Intake System Market Size, Share, Trends, Regional, Growth, Forecasts

Air Intake System Market By Component (Air Filter, Intake Manifolds & Pipe, Throttle Body & Air Control Uni), Engine Type (Gasoline, Diesel, Alternative Engine Fuel), Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Others), and Regional Analysis for 2025 to 2032

Air Intake System Market Share and Trends Analysis

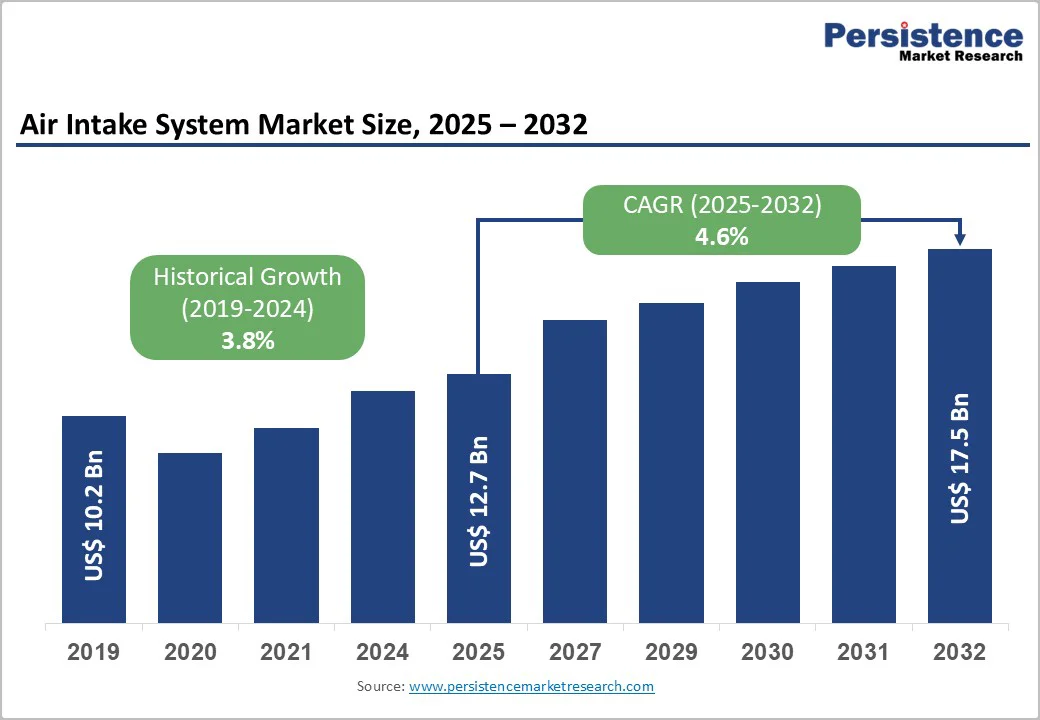

The global air intake system market size is valued at US$12.7 billion in 2025 and is projected to reach US$17.5 billion by 2032, growing at a CAGR of 4.64% between 2025 and 2032.

The stringent global emission regulations, such as the EU's Euro 7 standards, growing adoption of turbocharging technologies for better fuel efficiency, and strong vehicle production in emerging economies, especially in the Asia Pacific drive the market growth.

The air intake system market continues to serve as a critical enabler of vehicle performance optimization and environmental compliance, with technological innovations in lightweight materials, sensor integration, and advanced filtration systems reshaping competitive dynamics across all vehicle categories.

Key Industry Highlights:

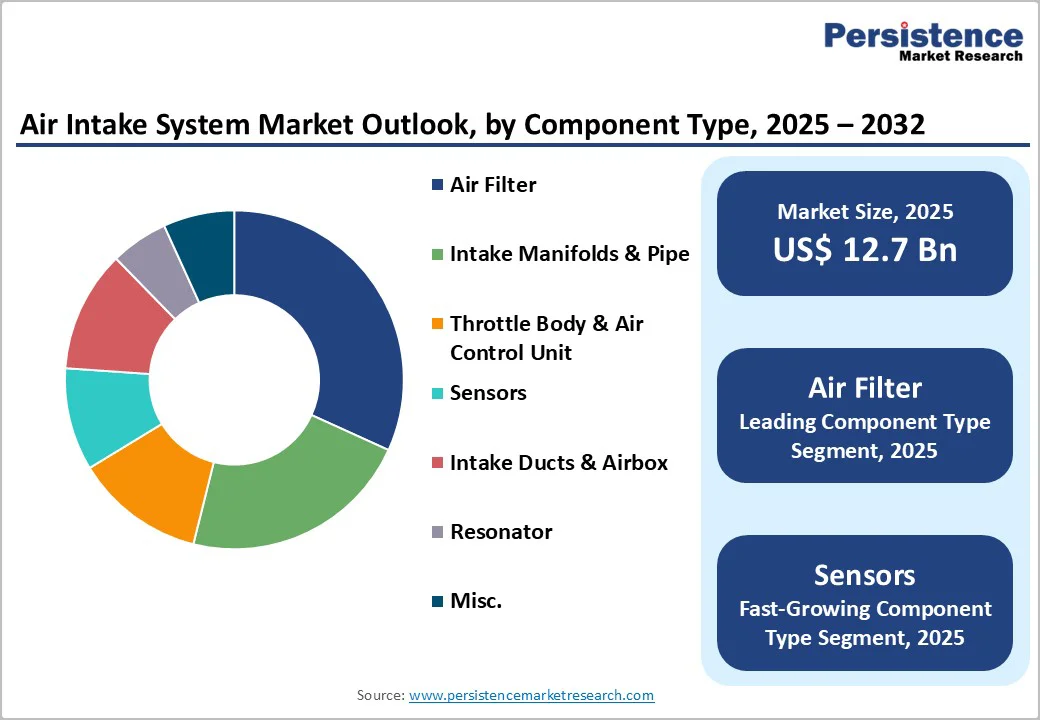

- Air filters lead with 32% market share, while sensor-integrated systems (MAF, MAP) record the fastest 7.4% CAGR, reflecting rising adoption of advanced engine control technologies and real-driving emissions compliance requirements.

- Gasoline engines dominate with a 63% share, whereas CNG/LPG engines grow fastest CAGR, supported by government-led clean mobility incentives, fueling infrastructure expansion, and emission reduction programs across emerging markets.

- Passenger vehicles maintain 55% market share, while light commercial vehicles drive the fastest growth, propelled by e-commerce logistics growth, last-mile delivery expansion, and the need for higher-efficiency light-duty fleets.

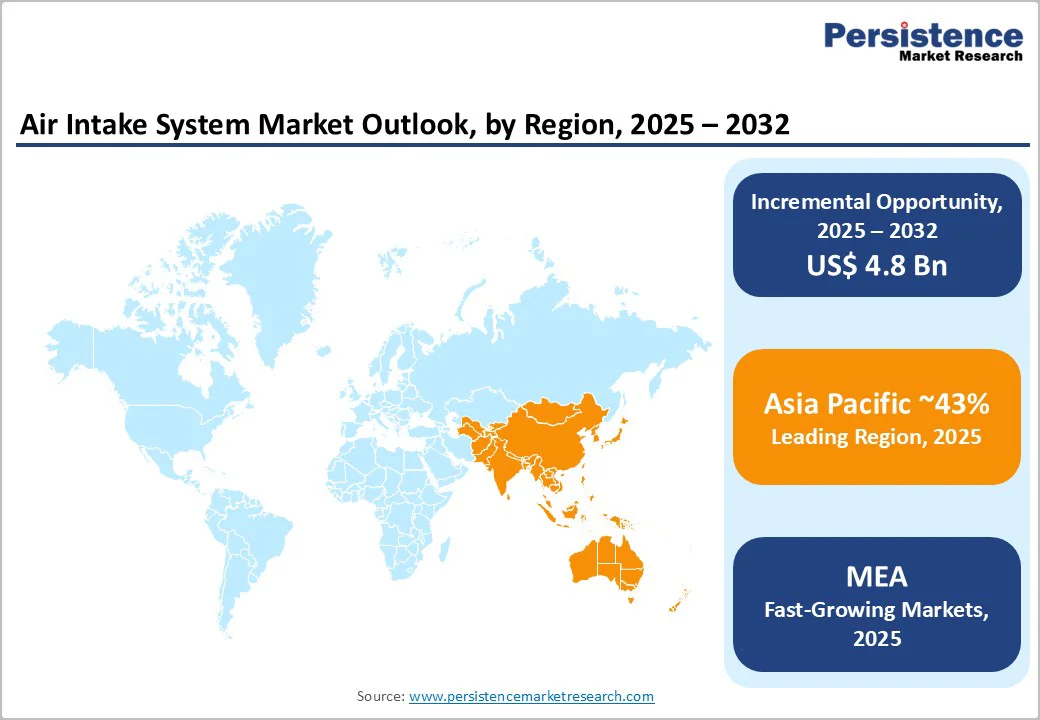

- Asia Pacific leads with 43% global share followed by North America accounting for 22% market share, and Europe 21% share, reflecting differences in production concentration, emission standards, and technology adoption maturity.

- Market leaders invest in lightweight composites, advanced sensor integration, emissions compliance technologies, and hybrid-specific intake solutions, establishing differentiation across OEM platforms and future propulsion architectures.

| Key Insights | Details |

|---|---|

| Air Intake System Market Size (2025E) | US$ 12.7 Billion |

| Market Value Forecast (2032F) | US$ 17.5 Billion |

| Projected Growth CAGR (2025 - 2032) | 4.6% |

| Historical Market Growth (2019 - 2024) | 3.8% |

Market Dynamics Analysis

Drivers - Stringent Emission Regulations and Environmental Compliance Requirements

Emission regulations represent the single most significant driver of the air intake system market's expansion, compelling automotive manufacturers worldwide to invest substantially in advanced technologies that optimize combustion efficiency.

The European Union's Euro 7 emission standard, effective from 2026 - 2027, is the strictest yet, requiring significant reductions in nitrogen oxides (NOx) and particulate matter while introducing real-world driving emissions (RDE) testing.

Petrol and diesel vehicles may face NOx limits around 30 mg/km, a reduction from Euro 6's 60-80 mg/km. In the U.S., CAFE standards and EPA regulations continue to require CO2 reductions, prompting demand for advanced air intake systems with variable valve timing and integrated exhaust gas recirculation (EGR).

These stringent standards are driving investment in premium intake manifolds and filtration systems, with regulatory compliance influencing 35-40% of innovation decisions among Tier-1 suppliers and supporting market growth through 2032.

Accelerating Vehicle Production and Market Expansion in Emerging Economies

Global vehicle production continues expanding, with developing nations, particularly China, India, and Brazil, accounting for increasingly larger shares of worldwide output. China emerged as the world's largest automotive market in 2022, producing over 26 million vehicles annually, with India's passenger car sales exceeding 3.6 million units and South Korea contributing over 3.2 million vehicles.

The shift in automotive manufacturing boosts demand for air intake systems, as each vehicle needs these components. The Asia Pacific region leads the global air intake system market with a 43% share, fueled by high-volume production and favorable investment policies.

Emerging markets benefit from lower labor costs and government incentives. The light commercial vehicle segment, crucial for last-mile logistics, is growing rapidly at a 5.4% CAGR, further driving air intake system demand as fleet operators focus on fuel efficiency and emissions compliance amid stricter urban regulations.

Restraints - Transition to Electric Vehicles and Declining Internal Combustion Engine Demand

The prominent growth in battery electric vehicles (BEVs) poses a significant long-term challenge to the traditional air intake system market. BEVs are expected to make up over 25% of the global automobile market by 2030, while hybrid electric vehicles (HEVs) and plug-in hybrids (PHEVs) will also see notable growth.

Although HEVs retain some internal combustion engine (ICE) components that require air intake systems, the overall shift toward electrification presents medium-to-long-term challenges for market growth. Manufacturers face uncertainty in R&D investments due to varying timelines for the phase-out of ICEs across regions and vehicle segments.

This uncertainty tempers growth projections and capital expenditures for traditional air intake systems, yet the existing fleet of ICE vehicles will continue to drive demand for maintenance and replacement parts through 2035 and beyond.

High Cost of Advanced Materials and Complex Manufacturing Processes

The development of lightweight, durable air intake systems for high-pressure turbocharging involves advanced composite materials, injection molding, and precision assembly. While these systems can reduce vehicle weight by up to 30% and improve corrosion resistance, they come with higher production costs. The integration of electronic components, such as MAF sensors and electronic throttle bodies, adds 15-25% to manufacturing costs.

Rising raw material prices for specialty polymers and aluminum, coupled with inflation in labor and energy, strain margins for Tier-1 suppliers and OEMs. This cost structure limits the adoption of premium air intake systems in entry-level and compact vehicles, while supply chain issues further complicate pricing competitiveness and investment in advanced technologies.

Opportunity - Hybrid Vehicle Market Expansion and Advanced Engine Integration Requirements

The hybrid electric vehicle market is set to grow from USD 119.08 billion in 2025 to USD 647.46 billion by 2034, representing a transformative opportunity for sophisticated air intake system suppliers. Hybrid powertrains require optimized air intake systems that balance the performance demands of internal combustion engines with integration constraints imposed by electric motors, battery systems, and regenerative braking architectures.

These dual-powerplant vehicles demand precisely calibrated air intake geometries, advanced filtration systems protecting both combustion chambers and electrical components from particulate contamination, and integrated sensor systems enabling seamless engine-motor transition management.

Manufacturers developing specialized air intake solutions for hybrid platforms can command premium valuations and secure long-term OEM supply agreements, as these systems represent differentiated performance enablers.

The hybrid vehicle market presents significant opportunities by 2032 as major OEMs, including Toyota, Honda, BMW, Mercedes-Benz, along with emerging Chinese manufacturers like BYD, Geely, and Li Auto, standardize hybrid technologies across their product lines.

Alternative Fuel Vehicle Infrastructure Development and CNG/LPG Market Growth

The global CNG and LPG vehicle market is expected to grow significantly at a CAGR of 6.8%, fueled by government mandates for emission reductions, cost benefits of fuel, and the development of refueling infrastructure. India leads this segment with a prominent number of CNG vehicles on the road, and the government targets to establish 10,000 CNG stations by 2030, while Africa is emerging as the fastest-growing territory at 10.2% CAGR through 2030.

Alternative fuel engines require specialized air intake system designs accommodating different combustion characteristics, pressure profiles, and temperature conditions relative to conventional gasoline and diesel configurations.

Liquid phase direct injection (LPDI) systems for LPG applications are emerging as the fastest-growing technology subsegment, creating opportunities for component suppliers to develop proprietary intake solutions commanding technology premiums.

Government subsidies, tax incentives, and strategic infrastructure investments in countries including India, Italy, Poland, South Korea, and African nations create favorable market conditions for alternative fuel vehicle adoption. This segment represents an estimated opportunity of USD 800 million to USD 1.2 billion within the broader air intake system market by 2032.

Category-wise Analysis

Component Insights

Air filters command a commanding 32% market share within the component-type segmentation, establishing this category as the market's leading segment. Air filters serve as fundamental engine protection components, filtering particulate matter, pollen, dirt, and other contaminants before air enters combustion chambers.

The air filter segment shows strong demand across all vehicle types, with a typical replacement needed every 15,000-30,000 miles. Paper-based filters dominate the market with a 62.32% share due to their low cost and OEM integration.

Synthetic fibers and nanofiber technologies are growing at a 7.37% CAGR, reflecting rising air quality concerns in urban areas and increased hygiene awareness post-pandemic. This segment's resilience is due to consistent replacement needs throughout a vehicle's lifecycle.

Advanced filtration technologies, including HEPA-grade filters removing 99.9% of particulate matter and activated carbon media reducing odor and chemical contaminants, enable market differentiation and premium pricing within this foundational component category.

Sensor-integrated air intake systems are the fastest-growing segment, expanding at a 7.4% CAGR compared to the overall market's 4.6%. Technologies like mass air flow (MAF) and manifold absolute pressure (MAP) sensors, along with integrated electronic control units, optimize engine performance by enhancing combustion efficiency and reducing emissions.

The rise of advanced driver-assistance systems (ADAS) and new Euro 7 emission standards drives demand for these sensors. Manufacturers are focusing on miniaturization, cost reduction, and AI-enabled diagnostics, making sensors key differentiators for premium vehicles and fleet management. This growth reflects the automotive industry's shift towards digitalization, creating opportunities for sensor specialists.

Engine Type Insights

Gasoline-powered vehicles command a dominant 63% market share within engine-type segmentation, reflecting the continued predominance of spark-ignition engines across global passenger vehicle fleets.

Gasoline engines power the vast majority of light-duty vehicles in North America and Europe, maintain significant market presence in Asia Pacific despite diesel popularity in commercial segments, and continue expanding in emerging markets as affordable personal mobility options.

Gasoline engine air intake systems benefit from mature supply chains, established manufacturing processes, and high-volume economies of scale, enabling cost-competitive solutions. However, turbocharger adoption increasingly standardizing across gasoline engines to simultaneously meet fuel efficiency mandates and power expectations, driving technology upgrades and premium air intake system adoption.

The segment faces modest competitive pressure from diesel and alternative fuel technologies, but maintains resilient demand through established vehicle parc and continued new vehicle production in this engine category.

Alternative fuel engines, especially compressed natural gas (CNG) and liquefied petroleum gas (LPG) power plants, are the fastest-growing segment with a 6.4% CAGR, outpacing the overall market. CNG engines comprise about 35% of this market, thanks to strong distribution networks, cost benefits, and expanding urban refueling infrastructures.

India leads global CNG adoption, while African markets are growing at a 10.2% CAGR due to natural gas reserves and government initiatives. These engines require specialized air intake systems to accommodate different combustion characteristics compared to conventional engines.

Vehicle Type Insights

Passenger vehicles dominate the vehicle-type segmentation with a commanding 55% market share, reflecting the category's overwhelming volume advantage in global vehicle production and sales. Passenger cars benefit from high-volume manufacturing platforms, established supply chains, and sophisticated cost management, enabling wide-scale deployment of advanced air intake systems.

Urbanization trends in emerging markets, rising middle-class populations, and increasing personal mobility preferences support continued passenger vehicle production growth, even as electrification accelerates. The segment encompasses diverse powertrain architectures, conventional gasoline and diesel, hybrid-electric, and plug-in hybrid configurations, requiring differentiated air intake solutions.

Premium and mid-segment passenger vehicles increasingly adopt turbocharging, variable intake manifolds, and advanced sensor arrays, driving technology sophistication and system value expansion within this dominant segment.

Light commercial vehicles (LCVs) are the fastest-growing vehicle segment, with a 5.4% CAGR, fueled by the rise of last-mile logistics and e-commerce delivery. LCVs, such as pickup trucks and vans, need durable air intake systems to handle tough conditions and varying payloads.

Fleet operators focus on fuel efficiency and emissions compliance to optimize costs and access urban delivery zones, leading to the adoption of advanced air intake technologies. The segment's growth is driven by the shift to distributed commerce and on-demand delivery services.

Regional Market Insights

Asia Pacific Air Intake System Market Trends

Asia Pacific dominates global air intake system markets, commanding a substantial 43% regional market share with accelerating growth at 5.4% CAGR, significantly exceeding global average expansion rates.

The region's dominance reflects high-volume vehicle production concentrated in manufacturing powerhouses, including China (21.4 million vehicles annually), India (3.6 million units), Japan, and South Korea, combined with favorable government policies attracting foreign direct investment and establishing competitive manufacturing ecosystems.

China emerged as the world's largest automotive market in 2022, producing over 26 million vehicles, establishing the foundation for sustained air intake system demand growth. India's rapidly expanding automotive sector, driven by rising middle-class populations, urbanization, and affordable personal mobility preferences, supports high-volume air intake component demand.

The region benefits from lower production costs, competitive labor economics, mature supply chain integration, and government incentives supporting industry development. Manufacturing capabilities in advanced filtration technologies, sensor integration, and composite materials position Asia Pacific suppliers as emerging technology innovators capable of competing with established European and North American manufacturers.

Alternative fuel vehicle adoption is strong in India, with government plans for 10,000 CNG stations by 2030 and Maruti Suzuki aiming to sell 600,000 factory-fitted CNG units in FY2025. However, challenges like environmental pollution, supply chain risks, and geopolitical tensions impact trade.

North America Air Intake System Market Share

North America maintains a prominent position within the global air intake system market, commanding approximately 22% global market share with particular strength in the United States, where mature automotive infrastructure, high vehicle ownership rates, and stringent emissions standards support consistent demand.

The U.S. market represents the region's dominant segment, characterized by large-scale light-duty vehicle production, established supply chain relationships between OEM manufacturers and Tier-1 suppliers, and sophisticated aftermarket distribution networks.

The North American air intake manifold market is projected to capture a 41% share by 2032, indicating strong regional momentum driven by investments to improve fuel economy and minimize energy losses across internal combustion engine platforms.

Stringent EPA and CAFE standards mandate continuous improvement in combustion efficiency, creating persistent demand for advanced air intake solutions. The region's light commercial vehicle segment demonstrates robust growth, driven by pickup truck popularity, e-commerce logistics expansion, and construction industry demand for capable commercial vehicles.

Regulatory harmonization efforts and alignment with international emission standards establish North America as a hub for technology innovation, particularly in developing advanced air intake systems. Increased requirements for emissions control, especially for NOx and particulate matter, boost R&D investments. However, the rise of electric vehicles, especially in California and northeastern states with strict zero-emission mandates, presents challenges.

Investment trends indicate a shift towards hybrid and alternative fuel vehicle air intake systems, with OEM partnerships focusing on next-generation efficiency technologies. The competitive landscape is dominated by established Tier-1 suppliers such as Bosch, Denso, Continental, and Mahle, who maintain strong OEM relationships while adapting to electrification.

Europe Air Intake System Market Insights

Europe represents a sophisticated, highly regulated market commanding approximately 21% global market share with steady-paced growth at a CAGR of 3.9%, reflecting mature automotive infrastructure, stringent emission regulations, and established manufacturing capabilities. The region encompasses major automotive production hubs in Germany, France, Italy, and Spain, supporting diverse OEM manufacturers and extensive Tier-1 supplier networks.

Germany's automotive intake manifold industry registers a dominant European share, driven by precision manufacturing capabilities and world-leading automotive engineering expertise, with strategic partnerships between major automakers and component suppliers advancing technology development.

Euro 7 emission standards implementation, set to take full effect from 2026 - 2027, represents the primary regulatory driver, mandating advanced combustion optimization, real-world driving emissions verification, and extended durability requirements.

The regulatory environment emphasizes lightweight material adoption, with carbon fiber and advanced composite intake manifolds gaining traction to reduce vehicle mass and improve fuel economy. The UK strategy to eliminate all internal combustion engine vehicles by 2035 drives investment in hybrid and plug-in hybrid electric vehicle air intake systems, creating differentiated market opportunities for suppliers capable of developing specialized hybrid intake solutions.

French and Italian markets show strong alternative fuel vehicle adoption, with Italy reaching 8% for CNG and LPG thanks to government incentives and infrastructure. Investment trends highlight a focus on compliance technologies, lightweight materials, and hybrid vehicle air intake systems, with European manufacturers using advanced manufacturing for high- precision components.

Competitive Landscape

The global air intake system market is moderately consolidated, with the top three to five players holding roughly 40-47% share. Leading Tier-1 suppliers such as Robert Bosch, Denso, Mann+Hummel, and Mahle maintain strong competitive advantages through deep OEM relationships, advanced R&D, and global manufacturing networks that accelerate technology deployment.

While OEM supply chains remain concentrated, the aftermarket segment is highly fragmented, enabling specialist brands like K&N Engineering and aFe to thrive through performance-focused products. Competitive differentiation increasingly depends on lightweight materials, sensor integration, emissions compliance, and cost-efficient engineering strategies.

Strategic Developments

- In April 2025, K&N Engineering introduced its NextGen Air Intake Systems for trucks, Jeeps, and SUVs, delivering up to 41 HP gains through redesigned filters, oversized intake tubes, a hybrid airbox, and quick-lock installation. The launch strengthens K&N’s position in performance aftermarket segments, targeting enthusiasts seeking improved airflow efficiency, engine responsiveness, and customization-focused upgrades.

- In July 2025, Donaldson Company formed a strategic partnership with Mighty Distributing to deliver OE-grade air, oil, fuel, and hydraulic filtration to heavy-duty Class 7-8 fleets, supported by customized inventory programs that enhance uptime, strengthen aftermarket penetration, and expand Donaldson’s reach into construction, agriculture, and vocational fleet segments.

Companies Covered in Air Intake System Market

- Robert Bosch GmbH

- Denso Corporation

- Mann+Hummel GmbH

- Mahle GmbH

- Sogefi SpA

- Continental AG

- Aisin Seiki Co., Ltd.

- K&N Engineering, Inc.

- Parker Hannifin Corp

- Donaldson Company Inc.

- Toyota Boshoku Corporation

- Hengst SE

- Cummins Inc.

- Valeo

- ACDelco Corporation

Frequently Asked Questions

The global Air Intake System Market is valued at US$12.7 billion in 2025 and represents a mature, expanding market segment serving all major vehicle categories across gasoline, diesel, hybrid, and alternative fuel powertrain platforms, expanding at a moderate growth.

The air intake system market is driven by stringent global emission regulations, increased turbocharging technology adoption, rising vehicle production in emerging economies, and innovations in lightweight materials and filtration systems, enhancing engine performance and regulatory compliance across vehicle categories.

The air intake system market is projected to expand at a CAGR of 4.64% from 2025 through 2032.

Primary market opportunities include the expansion of hybrid electric vehicles, development of alternative fuel infrastructure, integration of connected vehicle technologies for predictive maintenance, and the aftermarket sector focusing on customization and performance enhancements for personalized mobility solutions.

Dominant market participants include Tier-1 OEM suppliers Robert Bosch GmbH, Denso Corporation, Mann+Hummel GmbH, Mahle GmbH, Sogefi SpA, Continental AG, Aisin Seiki, and Parker Hannifin, commanding significant market share through established OEM relationships and manufacturing scale.