- Smart Packaging

- 3D Printed Packaging Market

3D Printed Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

3D Printed Packaging Market by Material (Plastics, Paper & Paperboard, Others), Technology (Stereolithography/SLA, Fused Deposition Modeling/FDM, Others), Application, and Regional Analysis for 2026 - 2033

3D Printed Packaging Market Size and Trends Analysis

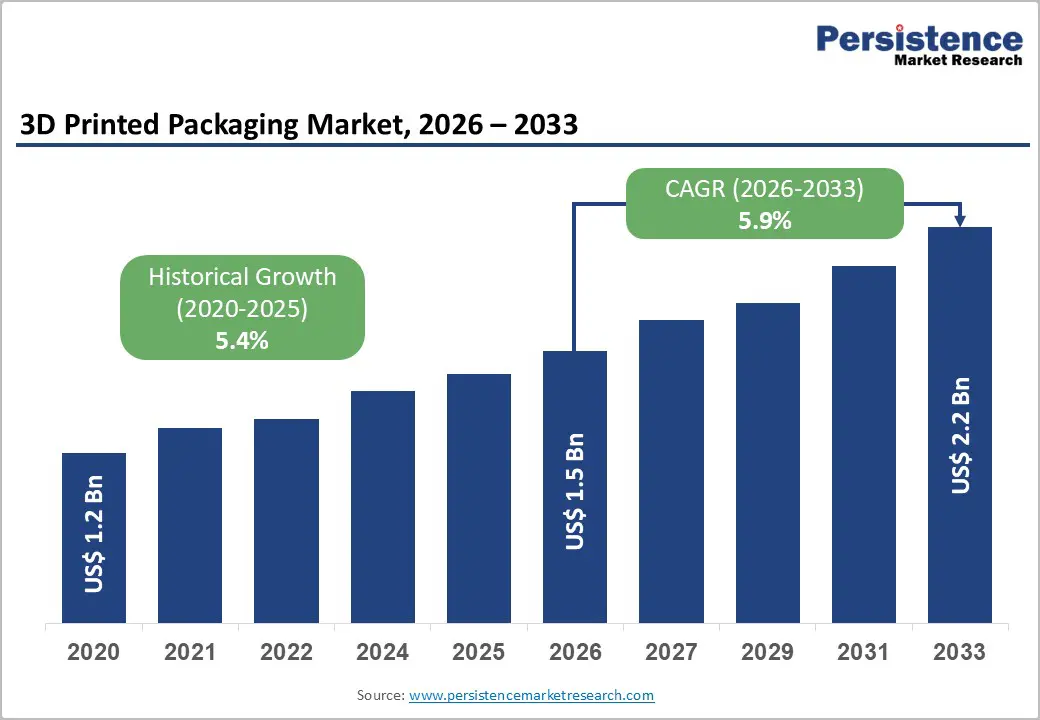

The global 3D printed packaging market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by rising demand for on-demand and highly customized packaging solutions, continuous material innovation including biobased and recyclable feedstocks, and the industrialization of select 3D printing technologies that reduce per-unit costs for low- to mid-volume production.

Supply-chain resilience strategies and sustainability mandates are increasing buyer willingness to pilot and scale 3D-printed packaging solutions. The market remains concentrated around industrial printer OEMs, advanced material formulators, and an expanding network of contract manufacturers serving food, cosmetics, and pharmaceutical end-users.

Key Industry Highlights

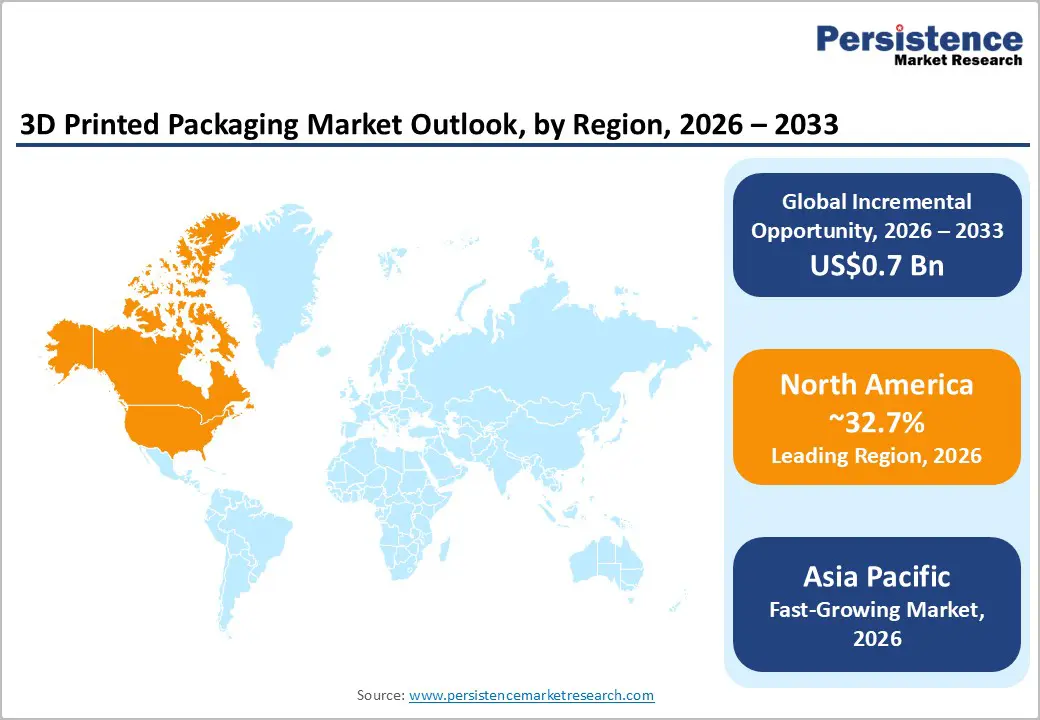

- Leading Region: North America is projected to lead the market, accounting for over 32.7% of market share in 2026, supported by strong U.S. market leadership, advanced additive manufacturing infrastructure, and early adoption by consumer brands and packaging converters.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by expanding manufacturing capacity, cost advantages, and rapid uptake by FMCG and electronics brands across China, Japan, India, and ASEAN countries.

- Investment Plans: Investment activity is concentrated in biobased and recyclable materials, production-grade polymer printing systems, and digital, on-demand packaging platforms, with North America and Europe attracting the highest share of technology and sustainability-focused capital.

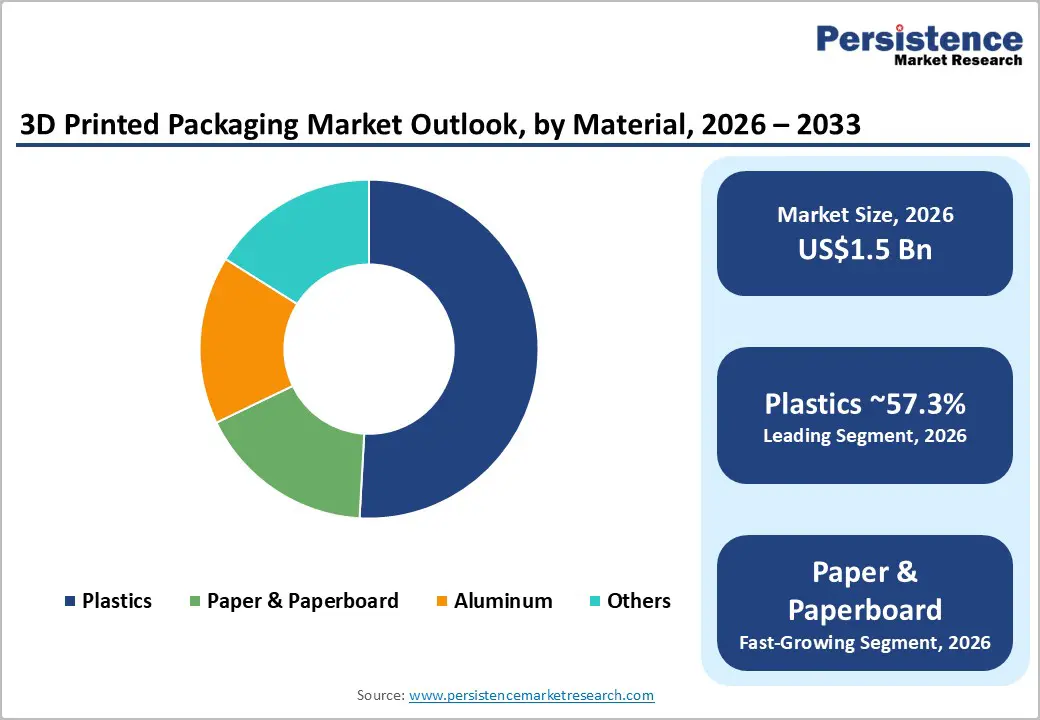

- Dominant Material: The plastics segment is expected to dominate the material segment, representing more than 57.3% of market share in 2026, due to strong mechanical performance and compatibility with established 3D printing technologies.

- Leading Technology: The Stereolithography (SLA) segment is the leading technology segment, accounting for approximately 21.4% of market share, driven by demand for high-resolution, premium, and visually critical packaging applications.

| Key Insights | Details |

|---|---|

| 3D Printed Packaging Market Size (2026E) | US$1.5 Bn |

| Market Value Forecast (2033F) | US$2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Circularity Pressures Enabling Material Innovation

Evolving environmental regulations and retailer-driven sustainability targets for recyclable and compostable packaging are encouraging designers and procurement teams to evaluate 3D printing as a viable manufacturing pathway. Additive manufacturing enables geometry-efficient designs that minimize material waste and support the use of biobased feedstocks derived from agricultural residues, starch, cellulose, and lignin. These materials demonstrate increasing technical feasibility for food-grade and compostable packaging applications. For companies seeking to reduce over-packaging, lower material usage, and improve transport efficiency, 3D printing offers rapid prototyping and short-run production capabilities. This shortens time-to-market for eco-redesigns while supporting corporate sustainability objectives, strengthening the overall adoption case.

Production Readiness of Industrial Additive Technologies

Industrial 3D printing platforms such as jetting, Multi Jet Fusion, P3/DLP, and high-throughput FDM variants have achieved significant improvements in printing speed, repeatability, and material compatibility. These advancements are narrowing the cost differential between additive manufacturing and traditional tooling for short-run packaging applications. Production-grade workflows, certified materials, and advanced quality assurance systems reduce unit variability and shorten qualification cycles. As a result, brands, particularly in cosmetics and premium food, are increasingly replacing limited injection-molded runs with directly printed packaging. This transition improves agility, enables rapid SKU introductions, and enhances launch economics for seasonal and customized products.

Consumer Demand for Personalization and Premiumization

In the mature and saturated consumer markets, packaging has become a critical differentiation lever. 3D printing enables highly personalized and structurally distinctive packaging designs without the long lead times or minimum order quantities associated with conventional tooling. Features such as tactile finishes, integrated secondary functions, and custom structural inserts enhance shelf appeal and user experience. Early adoption in cosmetics and specialty beverages demonstrates a higher per-unit willingness to pay for limited-edition and bespoke packaging. This creates a sustainable economic window where 3D printed packaging can capture higher margins despite elevated production costs, making personalization a persistent growth driver.

Barrier Analysis - Cost Structure and Economies of Scale

High capital requirements for industrial 3D printing systems and elevated per-unit material costs compared with high-volume tooling remain key structural barriers. For mass-market, low-margin categories such as commodity beverages and packaged staples, additive manufacturing cannot yet match the unit economics of injection molding or roll-to-roll converting. This imposes a practical ceiling on adoption, confining near-term growth to low- to mid-volume, premium, regulatory-sensitive, or bespoke packaging applications. In cost comparisons, representative small bottle inserts produced via 3D printing can cost 2-10 times more per unit than tooling-amortized alternatives, depending on volume and finishing requirements.

Regulatory and Food/Pharma Safety Qualification

Food-contact and pharmaceutical packaging applications require rigorous validation, including biocompatibility testing, extractables and leachables analysis, and full supply-chain traceability. Achieving regulatory clearance demands certified materials and highly stable production processes, which can be both time-intensive and capital-intensive. These requirements slow adoption in regulated end-use segments and increase supplier switching costs for brand owners. The resulting risk includes delayed commercial rollouts, often extending over several months or years, and the need for additional capital investment to meet compliance and quality assurance standards.

Opportunity Analysis - Biobased and Recyclable Feedstocks with Premium Pricing

Growing consumer willingness to pay for sustainable packaging, combined with advances in printable biopolymers, presents a compelling revenue opportunity. Suppliers capable of offering certified biobased materials, validated food and pharmaceutical compatibility, and reliable supply chains are positioned to capture premium margins. This opportunity is most pronounced in Europe and North America, where sustainability regulations and retailer-led initiatives are most advanced.

On-Demand Manufacturing and Near-Shoring for Supply Resilience

Brands reassessing supply-chain resilience are increasingly exploring distributed 3D printing hubs to reduce transit times, inventory risks, and import dependency. If brands reallocate 5-10% of short-run, high-SKU packaging production to localized 3D printing partners, the incremental market potential could reach tens to hundreds of millions of dollars over the forecast period. The business case is strongest for time-sensitive launches, localized personalization, and regions with high logistics costs or tariff exposure. Successful execution requires standardized quality control, digital inventory management, and networked production platforms.

Category-wise Analysis

Material Insights

The plastics segment is anticipated to account for more than 57.3% of the market share in 2026, making it the dominant material segment. Their leadership is underpinned by a favorable balance of mechanical strength, impact resistance, barrier performance, and compatibility with established additive manufacturing technologies such as multi-jet fusion, FDM, and selective laser sintering.

Commonly used polymers, including nylon, PET-based materials, and specialty photopolymers, enable consistent dimensional accuracy and repeatability. Plastic-based packaging is widely adopted for protective inserts, tamper-evident closures, customized cosmetic shells, bottle holders, and rigid secondary packaging for electronics and pharmaceuticals. The maturity of polymer processing ecosystems, combined with relatively streamlined certification pathways for non-food applications, reinforces plastics’ continued dominance despite growing sustainability scrutiny.

The paper and paperboard segment is expected to be the fastest-growing material segment through 2033. Growth is driven by regulatory pressure to reduce single-use plastics and rising consumer preference for recyclable and fiber-based packaging formats. Advances in printable cellulose composites, molded-fiber additive processes, and binder-jetting techniques allow the production of complex geometries, shock-absorbing structures, and customized cushioning inserts. The adoption is accelerating in food and beverage packaging, such as protective trays and cup carriers, as well as in consumer goods, where brands are prioritizing sustainability-led packaging differentiation.

Technology Insights

Stereolithography (SLA) and related photopolymerization technologies are anticipated to account for approximately 21.4% of market share, positioning them as the leading technology segment. SLA is favored for its exceptional surface finish, high dimensional accuracy, and ability to produce fine details, thin walls, and complex aesthetic features. These attributes make it particularly attractive for visible, premium packaging applications such as luxury cosmetics, fragrances, and limited-edition promotional packaging. Multi-material and color-capable photopolymer systems further enhance design flexibility. Reduced post-processing requirements and mold-like aesthetics strengthen SLA’s role in high-margin, small-batch production where visual quality and brand perception are critical.

Production-oriented polymer systems are anticipated to be the fastest-growing technology segment during the forecast period, supported by increasing adoption in functional packaging applications. Technologies such as multi-jet fusion and advanced industrial FDM platforms offer higher throughput, improved mechanical consistency, and lower per-part costs at small-to-medium batch sizes compared with legacy prototyping systems. These platforms are widely used to manufacture protective nests, customized internal packaging, logistics inserts, and secondary packaging components for electronics and industrial goods. Continued advancements in materials science, automation, build-volume scalability, and software-driven process optimization are accelerating the transition of these systems from prototyping environments to limited-scale and distributed production models.

Regional Insights

North America 3D Printed Packaging Market Trends - Mass Customization Ecosystems and FDA-Compliant Materials Innovation

North America is projected to hold 32.7% of the market share in 2026, positioning the region as the global market leader. The U.S. is the primary contributor, supported by a dense and mature ecosystem that includes industrial printer manufacturers such as HP and 3D Systems, materials innovators such as BASF Forward AM, and a large base of service bureaus, including Protolabs and Shapeways. This vertically integrated ecosystem accelerates commercialization by shortening development cycles from design to production. Growth is driven by strong demand for mass personalization and short-run packaging from consumer brands in cosmetics, nutraceuticals, and electronics. Major U.S. retailers and brand owners, such as Estée Lauder, Nike, and premium DTC brands, have increasingly experimented with 3D-printed secondary packaging and inserts to support limited editions and influencer-led campaigns. Sustainability initiatives by retailers such as Walmart and Target, which emphasize waste reduction and packaging right-sizing, further support the adoption of additive packaging for internal protective structures and on-demand formats.

Regulatory rigor enforced by the U.S. Food and Drug Administration (FDA) and Health Canada creates higher entry barriers, particularly for food and pharmaceutical applications. However, this rigor also establishes durable competitive advantages for certified suppliers that can meet traceability, material safety, and documentation requirements. As a result, investment activity is increasingly concentrated in biobased polymer development, FDA-compliant photopolymers, and digital inventory platforms that enable distributed, on-demand packaging production closer to end markets.

Europe 3D Printed Packaging Market Trends - Sustainability-Led Regulation and Circular Materials Development

Europe represents a significant share of the 3D printed packaging market, underpinned by strong regulatory alignment and leadership in sustainability-driven innovation. Germany, the U.K., France, and Spain are the most active national markets, each benefiting from advanced manufacturing capabilities, strong packaging machinery sectors, and close collaboration between industry and public research institutions.

Germany’s leadership is reinforced by industrial players such as EOS and Trumpf, which supply high-precision additive systems used by packaging converters and brand owners. The European Union’s extended producer responsibility (EPR) frameworks and packaging waste directives are actively reshaping material choices across the region. These policies incentivize investment in recyclable polymers, mono-material designs, and printable fiber-based packaging solutions. In response, companies such as Henkel, DS Smith, and Smurfit Kappa have increased R&D activity in additive manufacturing for packaging prototyping and short-run functional components, particularly for protective inserts and transport packaging.

Public funding initiatives and cross-border research programs further strengthen Europe’s commercialization capabilities. Programs supported by Horizon Europe and national innovation agencies have accelerated the development of circular materials suitable for additive processes. Strategic acquisitions, particularly involving specialty material startups and digital manufacturing platforms, are improving scale readiness. As regulatory harmonization reduces fragmentation, Europe is increasingly positioned as a proving ground for compliant, sustainability-first 3D printed packaging solutions that can later be scaled globally.

Asia Pacific 3D Printed Packaging Market Trends - Cost-Advantaged Manufacturing Scale and Precision-Led Adoption

Asia Pacific is likely to be the fastest-growing regional market for 3D printed packaging, driven by large-scale manufacturing capacity, expanding domestic consumer brands, and structural cost advantages in materials and production. China leads the region in volume adoption, supported by extensive additive manufacturing infrastructure and strong domestic printer manufacturers such as Farsoon and UnionTech. Chinese electronics and consumer goods exporters increasingly use 3D printed packaging components for customized protection and rapid design iteration.

Japan’s market is characterized by precision-driven applications and strong integration with high-value industries. Companies such as Ricoh and Mitsubishi Chemical are actively advancing high-resolution printing materials suitable for premium packaging, particularly in cosmetics and electronics. In India and across ASEAN countries, adoption is accelerating in premium FMCG and personal care packaging, driven by the rise of digitally native brands and growing demand for differentiation in crowded retail environments.

Regulatory maturity varies significantly across the region, resulting in uneven adoption patterns. While Japan and Australia maintain relatively stringent material and food-contact standards, emerging Southeast Asian markets are still developing certification frameworks. Despite this, growth potential remains strong. As local material suppliers scale biobased and recyclable feedstocks and governments increase support for advanced manufacturing under initiatives such as “Make in India” and regional Industry 4.0 programs, Asia Pacific is expected to transition rapidly from experimentation to broader commercial deployment.

Competitive Landscape

The global 3D printed packaging market is characterized by a concentrated group of industrial printer manufacturers and advanced material suppliers, complemented by a fragmented network of regional service bureaus and packaging converters. Leading OEMs account for a substantial share of installed capacity and ecosystem influence, while smaller providers compete through application-specific expertise and localized manufacturing. Strategic partnerships across hardware, materials, and finishing services are increasingly critical for delivering end-to-end, compliant packaging solutions.

Recent strategic developments include collaborations between printer manufacturers and packaging specialists to commercialize end-use cosmetic packaging, technology launches focused on expanding production-grade materials, and consolidation among European packaging groups to strengthen sustainable packaging portfolios. These initiatives reduce adoption risk, accelerate certification, and expand commercial scalability.

Leading companies emphasize technology partnerships, material certification, and targeted vertical strategies focused on cosmetics, pharmaceuticals, and food. Integrated offerings combining hardware, materials, software, and quality assurance are central to lowering buyer switching costs and accelerating market penetration.

Key Industry Developments

- In July 2025, Stratasys bolstered its polymer additive manufacturing portfolio by acquiring assets from Nexa3D, expanding high-speed DLP options applicable to molds, trays, and functional packaging components, and strengthening its offering for rapid packaging innovation.

- In April 2025, 3D Systems Corporation launched the Figure 4® 135 3D printer and Figure 4 Tough 75C FR Black material at RAPID+TCT, targeting precision, high-mix, low-volume applications and improving performance options for specialized packaging components.

Companies Covered in 3D Printed Packaging Market

- HP Inc.

- Stratasys Ltd.

- 3D Systems Corporation

- Materialise NV

- EOS GmbH

- Carbon, Inc.

- Protolabs Inc.

- Formlabs, Inc.

- Desktop Metal, Inc.

- Markforged, Inc.

- Nexa3D

- BASF SE

- Evonik Industries AG

- Arkema S.A.

- SABIC

- GE Additive

- SLM Solutions Group AG

- Ricoh Company, Ltd.

Frequently Asked Questions

The global 3D printed packaging market is valued at US$1.5 billion in 2026.

By 2033, the 3D printed packaging market is expected to reach US$2.2 billion.

Key trends include the rise of on-demand and localized manufacturing, increasing use of biobased and recyclable materials, growing demand for personalized and premium packaging, and the industrialization of production-grade additive manufacturing systems.

By material type, plastics are the leading segment, accounting for more than 57.3% of market share, due to their mechanical performance, barrier properties, and compatibility with major additive manufacturing technologies.

The 3D printed packaging market is projected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players include HP Inc., Stratasys Ltd., 3D Systems Corporation, Materialise NV, and EOS GmbH.