ID: PMRREP3192| 196 Pages | 26 Nov 2025 | Format: PDF, Excel, PPT* | Healthcare

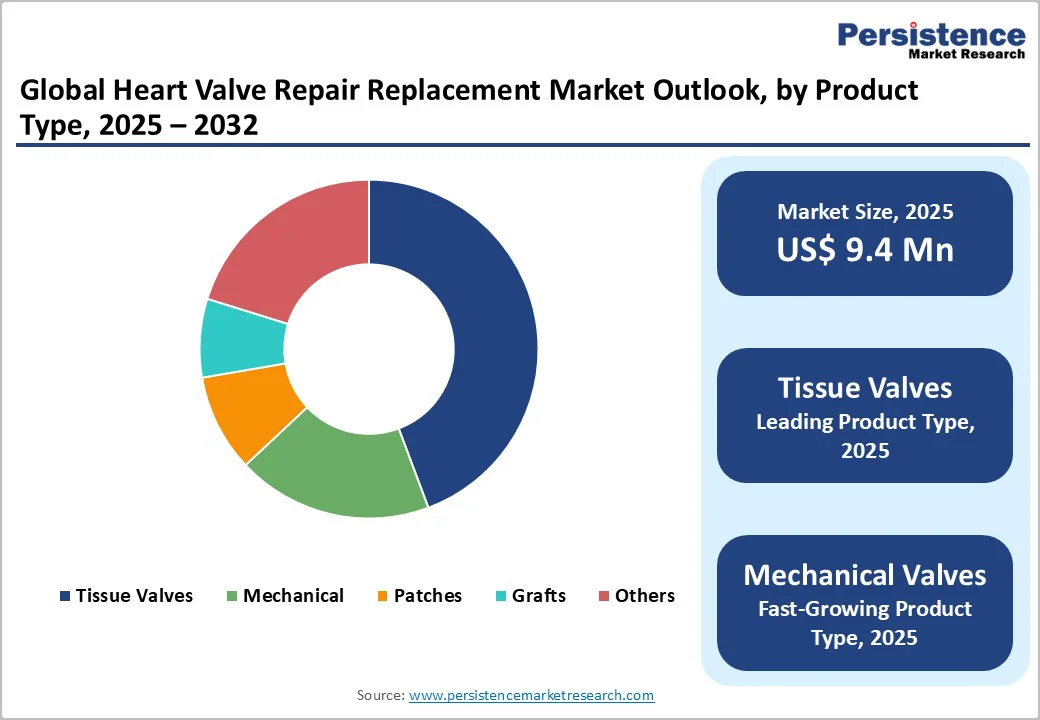

The global heart valve repair and replacement market size is valued at US$9.4 billion in 2025 and projected to reach US$18.8 billion at a CAGR of 10.4% during the forecast period from 2025 to 2032. Global demand for heart valve repair and replacement is increasing due to the rising prevalence of valvular heart diseases, such as aortic stenosis and mitral regurgitation, particularly among the growing geriatric population.

Advancements in transcatheter procedures (TAVR, TMVR), sutureless valves, and robotic-assisted cardiac surgeries are improving treatment outcomes and expanding access to high-risk patients. Moreover, increased healthcare investments, favorable reimbursement policies, and the expansion of cardiac care infrastructure in developing regions are further propelling market growth.

| Key Insights | Details |

|---|---|

|

Heart Valve Repair and Replacement Market Size (2025E) |

US$9.4 Bn |

|

Market Value Forecast (2032F) |

US$18.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.1% |

The growing incidence of valvular heart diseases (VHDs), including aortic stenosis, mitral regurgitation, and congenital defects, is a key driver of the heart valve repair and replacement market. The risk of VHD increases significantly with age, contributing to rising procedural volumes globally. For instance, in October 2025, according to the Cardiovascular Research Foundation (PREVUE VALVE study), there are currently at least 4.7 million people aged 65–85 years in the U.S. living with moderate or greater VHD, and 10.6 million with clinically significant disease, and most are unaware of their condition. The study highlights that VHD prevalence rises sharply with advanced age, underscoring the urgent need for enhanced screening, early diagnosis, and access to timely surgical or transcatheter interventions worldwide.

Continuous innovations in heart valve repair and replacement technologies are transforming cardiac care by improving procedural safety, durability, and patient recovery. Emerging techniques such as transcatheter aortic valve replacement (TAVR) and transcatheter mitral valve repair (TMVR) are increasingly preferred for high-risk and elderly patients unsuitable for open-heart surgery. Additionally, the development of sutureless and tissue-engineered valves enables shorter operative times, shorter hospital stays, and improved hemodynamic performance.

The high cost of heart valve replacement and repair procedures remains a major restraint to market growth, particularly in emerging economies. The expense of valve prostheses, advanced imaging and navigation systems, and post-operative care significantly increases overall treatment costs. Additionally, the high reliance on imports for implantable devices and the lack of reimbursement coverage in several low- and middle-income countries further limit adoption. This financial barrier restricts access for large segments of the population, slowing penetration of advanced cardiac interventions despite the growing clinical need for valve replacement therapies.

Moreover, despite their hemodynamic advantages and reduced need for anticoagulation, bioprosthetic and tissue valves face significant durability challenges that limit their long-term reliability. These valves are prone to calcification, structural valve deterioration (SVD), and leaflet tearing, typically requiring re-intervention within 10–15 years of implantation. The issue is particularly concerning among younger and more active patients.

Rapid progress in tissue engineering and biomaterial science is creating significant opportunities in the heart valve repair and replacement market. The development of polymeric, bioresorbable, and tissue-engineered valves aims to overcome limitations of conventional mechanical and bioprosthetic valves by enhancing durability, biocompatibility, and endothelialization. These next-generation valves mimic native tissue function while reducing the need for lifelong anticoagulation therapy.

The rising clinical adoption of transcatheter mitral valve repair (TMVR) and transcatheter tricuspid valve replacement (TTVR) is boosting the market growth within structural heart interventions. These technologies are expanding treatment access for patients who are inoperable or at high surgical risk due to comorbidities. For instance, in June 2025, Foldax Inc. reported positive one-year results from its India clinical trial of the TRIA™ Mitral Valve, demonstrating strong safety, durable hemodynamic performance, and significant improvements in quality of life. The findings, presented at New York Valves 2025 and published in the Journal of the American College of Cardiology (JACC), mark the first multicenter, one-year clinical outcomes for a polymer heart valve globally, highlighting the growing potential of polymer-based valve technologies in next-generation cardiac repair solutions. Ongoing clinical trials and FDA Breakthrough Device designations for next-generation TMVR and TTVR systems highlight accelerating innovation and regulatory support.

By Product Type, Tissue Valve Dominates Globally Due to Their Superior Biocompatibility, Reduced Need for Lifelong Anticoagulation, and Growing Adoption in Elderly Patient Populations

The tissue valve segment is projected to dominate the global heart valve repair and replacement market in 2025, accounting for 44.3% of revenue. The segment’s strong performance is primarily driven by the rising adoption of bioprosthetic valves, which offer superior biocompatibility, natural hemodynamic performance, and eliminate the need for lifelong anticoagulation therapy, unlike mechanical valves. These valves are increasingly preferred among the elderly population and low-risk patients, owing to their safer profile and shorter recovery time. Continuous innovations in tissue engineering, anti-calcification treatment, and valve durability have enhanced long-term outcomes. Furthermore, the integration of tissue-based valves into transcatheter procedures, such as for transcatheter aortic valve replacement (TAVR) and transcatheter mitral valve replacement (TMVR), has expanded their applicability.

The transcatheter procedure segment is projected to dominate the global heart valve repair and replacement market in 2025, accounting for 41.2% of revenue. This is due to its minimally invasive nature, which significantly reduces hospital stay, surgical risk, and recovery time compared to open-heart surgery. The rising adoption of transcatheter aortic valve replacement (TAVR) and the growing clinical acceptance of transcatheter mitral valve replacement (TMVR) are driving the adoption, supported by favorable clinical trial results and expanding regulatory approvals. Increasing preference among elderly and high-risk patients, coupled with ongoing technological advancements in catheter-based delivery systems and next-generation valve designs, continues to accelerate the shift toward transcatheter procedures worldwide.

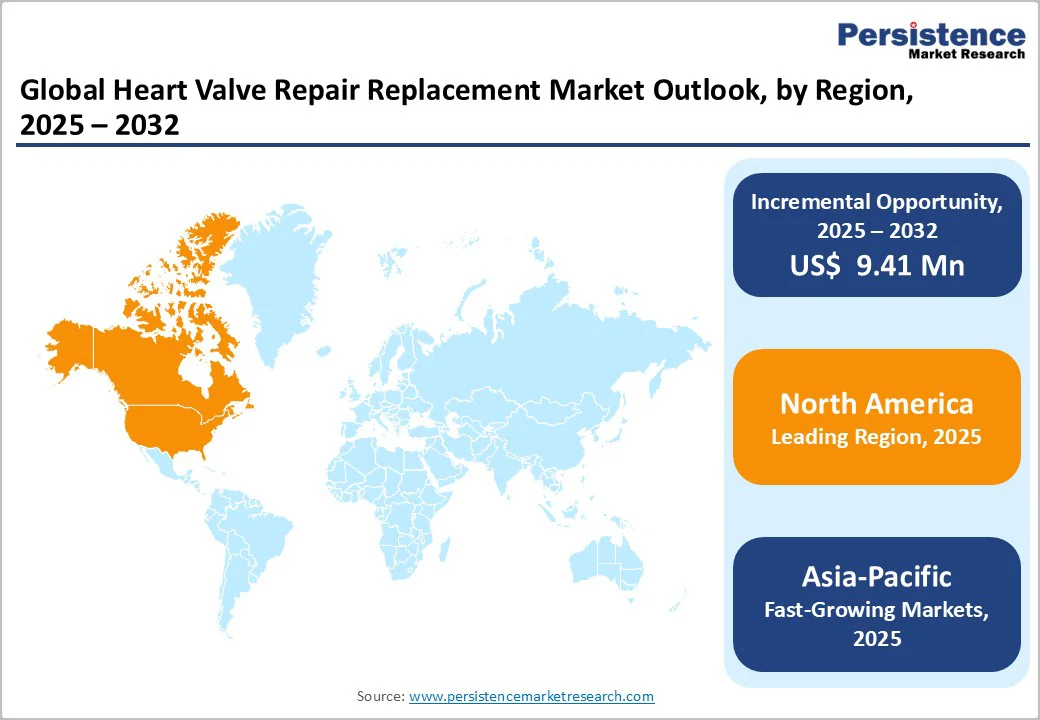

The North American market is expected to dominate globally with a value share of 40.1% in 2025, with the U.S. leading the region due to the high procedural volume of surgical and transcatheter valve interventions. Strong reimbursement policies for transcatheter aortic valve replacement (TAVR), transcatheter mitral valve replacement (TMVR), and minimally invasive repair procedures, coupled with early FDA approvals and rapid clinical adoption of next-generation bioprosthetic and transcatheter valves, continue to accelerate growth.

For instance, in February 2025, researchers at the Georgia Institute of Technology introduced an advanced 3D-printed bioresorbable heart valve designed to promote tissue regeneration in both adult and pediatric patients. Unlike standard animal-tissue valves, this implant is custom-made to the patient's anatomy, delivered via catheter, and later absorbed by the body as new native tissue forms. The region also benefits from well-established cardiac centers, high awareness and diagnosis rates, a large ageing population, and the presence of key device manufacturers engaged in continuous research and development (R&D) and clinical trials.

Europe is expected to achieve steady growth, driven by the rising prevalence of valvular heart diseases, particularly among the ageing population, and strong adoption of minimally invasive and transcatheter procedures across major countries such as Germany, France, and the U.K. For instance, in May 2024, University Hospitals of North Midlands NHS Trust in the UK became the first centre in the country to use a next-generation transcatheter valve implant for Aortic Stenosis via the Transcatheter Aortic Valve Implantation (TAVI) route. The new valve offers improved positioning clarity and reduced complication risk, strengthening the case for broader adoption of minimally invasive valve therapies across Europe. Increasing availability of CE-approved devices, supportive reimbursement frameworks, and growing participation in multicenter clinical trials are accelerating technology adoption. In addition, the presence of leading manufacturers and research collaborations focused on next-generation repair and replacement valves continues to drive the region’s market growth.

The Asia Pacific market is expected to register a relatively higher CAGR between 2025 and 2032, fueled by the rapid expansion of healthcare infrastructure, rising awareness of valvular heart diseases, and a growing geriatric population in countries such as China, Japan, and India. The increasing adoption of transcatheter and minimally invasive cardiac procedures, along with improved access to advanced devices through government initiatives and local manufacturing partnerships, is driving market growth. For instance, in August 2025, India adopted a next-generation motorised TAVR delivery system (Vitaflow Liberty), with pioneering cases performed in Coimbatore and Chennai, Tamil Nadu.

The device, designed with high radial strength for challenging bicuspid anatomies and a motorised deployment mechanism, enables single-operator, micro-precision placement with real-time retrieval and repositioning, reducing malposition and paravalvular leak risk. Moreover, expanding investments by global players and clinical collaborations are accelerating the regional adoption of next-generation valve technologies.

The global heart valve repair and replacement market is highly competitive, with major players such as Medtronic, Abbott, Edwards Lifesciences Corporation, Boston Scientific Corporation, and Artivion, Inc are dominating the landscape. These companies maintain strong market positions through comprehensive product portfolios, global distribution networks, and continuous advancements in transcatheter and minimally invasive cardiac technologies.

Key strategies include the development of next-generation TAVR and TMVR systems, tissue-engineered and polymeric valves, and robotic-assisted surgical platforms to enhance procedural precision and patient recovery. Moreover, major players are engaging in strategic collaborations, mergers and acquisitions, clinical trial partnerships, and product launches to expand indications and geographic reach.

The global heart valve repair and replacement market is projected to be valued at US$ 9.4 Bn in 2025.

Rising prevalence of valvular heart diseases and rapid technological advancements such as TAVR, TMVR, and minimally invasive surgical techniques are driving the global heart valve repair and replacement market.

The global heart valve repair and replacement market is poised to witness a CAGR of 10.4% between 2025 and 2032.

Advancements in tissue-engineered and polymeric valve technologies, growing adoption of transcatheter mitral and tricuspid valve therapies (TMVR and TTVR) are creating significant growth opportunities in the heart valve repair and replacement market.

Medtronic, Abbott, Edwards Lifesciences Corporation, Boston Scientific Corporation, and Artivion, Inc are some of the key players in the heart valve repair and replacement market.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Mn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Product Type

By Procedure

By Indication

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author