- Medical Devices

- Medical Robots Market

Medical Robots Market Size, Share and Growth Forecast, 2026 - 2033

Medical Robots Market by Product Type (Surgical Robotic Systems, Rehabilitation Robotic Systems, Others), Application (Minimally Invasive Surgery, Others), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis for 2026 - 2033

Medical Robots Market Share and Trends Analysis

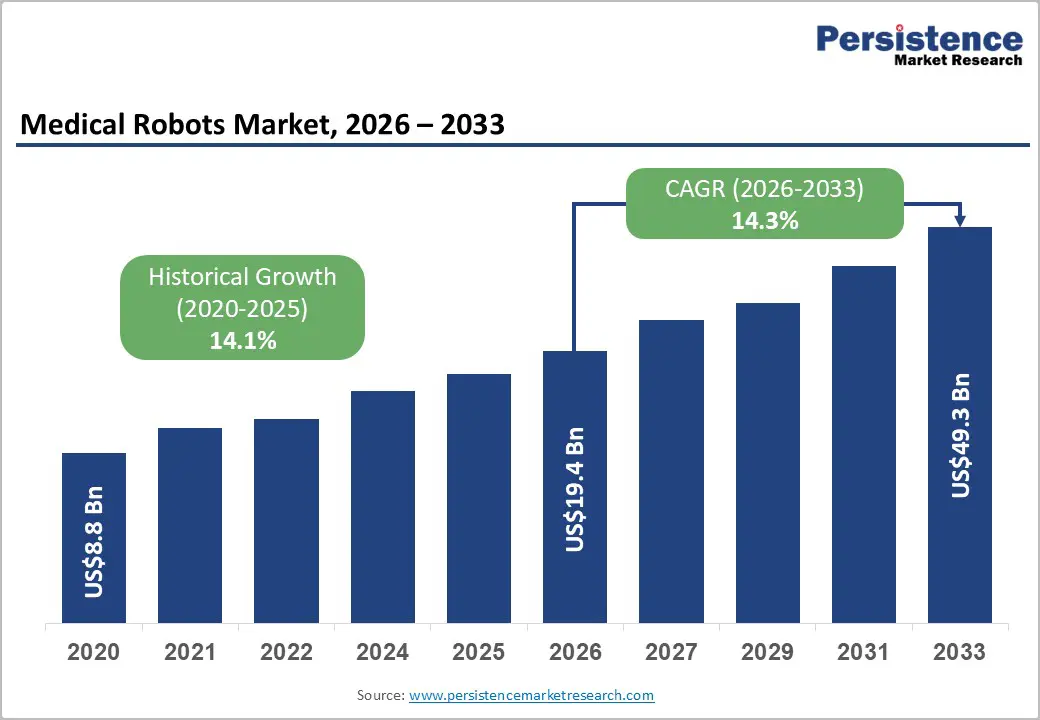

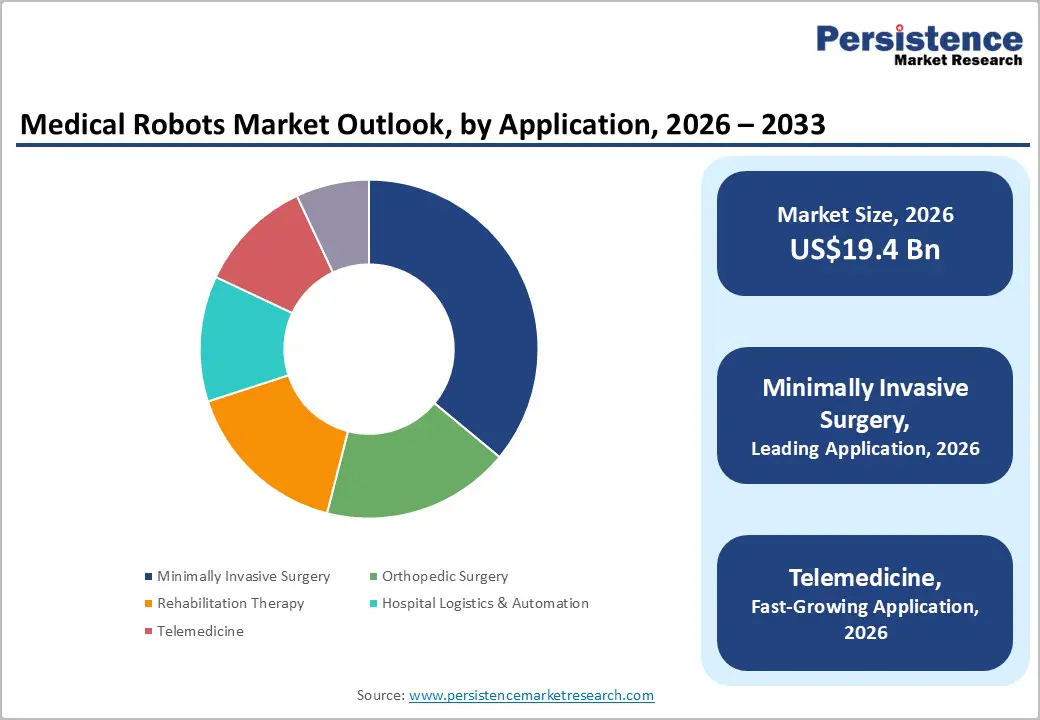

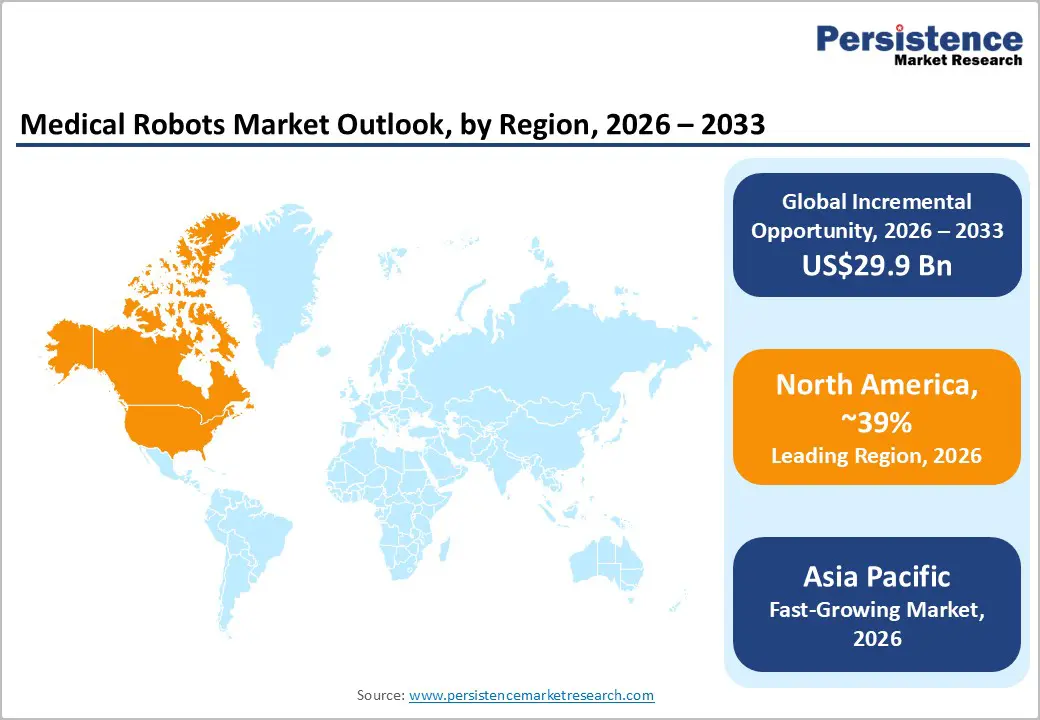

The global medical robots market size is likely to be valued at US$19.4 billion in 2026 and is projected to reach US$49.3 billion by 2033, growing at a CAGR of 14.3% during the forecast period from 2026 to 2033, driven by rising adoption of minimally invasive surgical robots, increasing healthcare workforce shortages, and growing hospital investments in digital infrastructure.

Advancements in artificial intelligence, imaging analytics, and robotic-assisted surgery technologies are accelerating adoption across healthcare systems. In addition, aging populations and the rising prevalence of neurological and musculoskeletal disorders are supporting demand for robotic rehabilitation and hospital automation solutions across the broader healthcare robotics industry.

Key Industry Highlights:

- Dominant Product Type: Surgical robotic systems are set to command around 41% of the revenue share in 2026, while rehabilitation robotic systems are likely to grow the fastest through 2033, driven by rising neurological rehabilitation demand.

- Leading Application: Minimally invasive surgery is expected to lead the market in 2026, while telemedicine applications are projected to witness the fastest growth through 2033 due to expanding remote healthcare adoption.

- Dominant End-user: Hospitals are anticipated to account for nearly 48% of market revenue in 2026, while home healthcare settings are likely to register the fastest growth during 2026 - 2033.

- Regional Leadership: North America is poised to dominate with an estimated 39% share in 2026, supported by advanced healthcare infrastructure, strong robotic surgery adoption, and favorable regulatory support.

- Technology Trends: AI-integrated robotic systems, minimally invasive surgical robots, and hospital automation technologies continue to strengthen long-term market expansion.

- Competitive Environment: Competitive dynamics include AI integration, robotic surgery platform expansion, orthopedic robotics innovation, and strategic partnerships focused on digital healthcare advancement.

DRO Analysis

Driver - Rising Adoption of Robotic-Assisted Minimally Invasive Procedures

The growing preference for robotic-assisted minimally invasive procedures remains the primary growth driver for the robotic surgery systems market. According to the U.S. Centers for Disease Control and Prevention (CDC) and the World Health Organization (WHO), chronic diseases such as cardiovascular disorders, cancer, obesity, and orthopedic conditions continue to increase surgical volumes globally. Hospitals are increasingly adopting robotic-assisted platforms to improve surgical precision, reduce postoperative complications, shorten hospitalization periods, and lower readmission rates.

Data published by the U.S. Food and Drug Administration (FDA) indicates continued growth in robotic-assisted surgery approvals across gynecology, urology, thoracic, and colorectal procedures. The American Hospital Association further highlights rising capital investments in digital operating rooms and automation technologies. These trends are strengthening demand for AI medical robots market solutions capable of integrating imaging, navigation, and analytics functionalities into surgical workflows.

Restraint - High Capital Costs and Complex Regulatory Compliance Requirements

High acquisition and maintenance costs continue to restrict broader adoption of robotic platforms, particularly among mid-sized hospitals and healthcare facilities in emerging economies. Advanced robotic surgical systems often require substantial upfront investment, including infrastructure upgrades, software integration, annual servicing contracts, and physician training programs. According to the U.S. Government Accountability Office (GAO) and healthcare procurement assessments published by the European Commission, robotic-assisted surgery platforms can significantly increase procedural costs during initial deployment phases.

In addition, manufacturers must comply with stringent regulatory pathways established by agencies such as the FDA, the European Medicines Agency (EMA), and Japan’s Pharmaceuticals and Medical Devices Agency (PMDA). Delays associated with clinical validation, cybersecurity testing, interoperability standards, and post-market surveillance increase commercialization timelines. These structural barriers continue to limit the rapid penetration of next-generation healthcare robots across cost-sensitive healthcare systems.

Opportunity - Expansion of Hospital Automation and AI-Integrated Healthcare Robotics

The integration of artificial intelligence, machine learning, and automation technologies into healthcare infrastructure presents a major long-term opportunity for the medical robotic systems market forecast. Hospitals are increasingly deploying robotic technologies beyond surgery into pharmacy automation, logistics management, telepresence, and infection control. According to the International Federation of Robotics (IFR), healthcare service robotics deployment continues to rise due to staffing shortages and increasing operational efficiency requirements.

Governments across Asia Pacific and Europe are also expanding digital healthcare funding programs to support the adoption of robotics in public hospitals. AI-enabled robotic systems capable of predictive diagnostics, autonomous navigation, and workflow optimization are gaining traction in large healthcare networks. This trend is creating new revenue opportunities for manufacturers operating in the hospital automation robots segment, particularly in emerging healthcare markets where infrastructure modernization initiatives are accelerating between 2026 and 2033.

Category-wise Analysis

Product Type Insights

Driven by growing demand for precision-led procedures, surgical robotic systems are expected to account for nearly 41% of global market revenue in 2026. Adoption remains strongest across urology, orthopedics, and gynecology, where robotic-assisted surgery helps reduce complications, improve visualization, and shorten patient recovery time. Industry competition intensified in 2025 as Johnson & Johnson MedTech accelerated development of its Ottava robotic platform, underscoring continued investment in next-generation digital surgery technologies.

While surgical systems dominate current spending, rehabilitation robotic systems are forecast to record the fastest growth through 2033 as healthcare providers expand neurological recovery and elderly mobility programs. Rising stroke prevalence and musculoskeletal disorders are increasing the demand for robotic exoskeletons and AI-assisted therapy systems. This shift became increasingly visible in 2025 as rehabilitation centers across Japan and Europe expanded adoption of robotic gait-training technologies to support aging populations and long-term rehabilitation care.

Application Insights

Accounting for nearly 36% of market revenue in 2026, minimally invasive surgery is expected to remain the leading application segment within the minimally invasive surgical robots market. Hospitals continue expanding robotic-assisted colorectal, orthopedic, and laparoscopic procedures as demand rises for shorter hospital stays, lower infection risks, and faster recovery outcomes. Growing investment in robotic operating room infrastructure across the U.S., Germany, and China is further reinforcing segment dominance.

Beyond surgery, healthcare systems are rapidly increasing investments in remote care technologies, positioning telemedicine as the fastest-growing application segment through 2033. Demand for telepresence robots is rising across hospitals, elderly care facilities, and emergency response settings to improve specialist accessibility and patient monitoring. In 2026, VSee Health introduced an autonomous AI-powered telehealth robot designed for virtual rounds and emergency consultations, reflecting the accelerating convergence of robotics and connected healthcare delivery.

End-user Insights

Large multispecialty hospitals continue to anchor demand across the healthcare robotics industry, with the hospitals segment projected to contribute nearly 48% of global market revenue in 2026. Strong capital investment capabilities and rising focus on operational efficiency are accelerating adoption of robotic surgery, pharmacy automation, infection control, and smart logistics systems. Healthcare providers are increasingly integrating robotics into core clinical workflows to improve patient outcomes while reducing workforce burden.

Home healthcare settings are emerging as the fastest-growing end-user segment through 2033, as aging populations increase demand for remote rehabilitation and assisted living solutions. Portable rehabilitation robots, AI-powered caregiving systems, and remote monitoring technologies are becoming more accessible across home care environments. Reflecting this trend, Samsung Electronics expanded development initiatives for AI-enabled home care robotics in 2025 to strengthen support for elderly and chronic care patients.

Regional Insights

North America Medical Robots Market Trends

North America is projected to account for nearly 39% of the global medical robots market revenue in 2026, supported by advanced healthcare infrastructure, favorable reimbursement systems, and rapid adoption of robotic-assisted surgery technologies. The region continues to lead innovation in AI-enabled surgical robotics, rehabilitation systems, and hospital automation, while rising outpatient procedure volumes and aging demographics are sustaining long-term market expansion.

U.S. Medical Robots Market Trends

The U.S. is expected to contribute around 32% of the regional market share, driven by strong hospital investments and continued FDA support for robotic-assisted technologies. Hospitals are rapidly integrating AI-powered robotics into surgical and clinical workflows to improve precision and efficiency. Reflecting this momentum, Mayo Clinic expanded robotic-assisted surgery programs across specialty care centers in 2025, reinforcing the country’s leadership in precision healthcare innovation.

Canada Medical Robots Market Trends

Canada is expected to account for an estimated 11% share of the regional market share in 2026, supported by rising investments in telehealth robotics and smart hospital infrastructure. Healthcare providers are increasingly adopting robotic systems to improve specialist access in remote communities and address workforce shortages. Government-backed digital healthcare initiatives are also accelerating the deployment of robotic rehabilitation and virtual care technologies across the country.

Europe Medical Robots Market Trends

Europe continues to strengthen its position in the next-generation healthcare robots landscape through rising healthcare digitization, strong public healthcare systems, and growing demand for robotic-assisted minimally invasive procedures. Hospitals across the region are increasingly deploying robotic technologies for surgery, rehabilitation, and logistics automation as workforce shortages and elderly care demands continue to rise.

Germany Medical Robots Market Trends

Leading the regional market, Germany is projected to account for nearly 28% of Europe’s market revenue in 2026, supported by advanced manufacturing capabilities and high robotic surgery adoption rates. The country continues to invest heavily in digital operating room infrastructure and AI-assisted healthcare technologies. In 2025, Siemens Healthineers expanded collaborations focused on robotic imaging and intervention technologies, further strengthening Germany’s role in healthcare automation innovation.

U.K. Medical Robots Market Trends

The U.K. is estimated to hold around 19% of the regional market share in 2026, driven by rising NHS investments in robotic-assisted surgery and healthcare modernization initiatives. Hospitals are increasingly adopting robotic systems to improve patient outcomes and reduce surgical backlogs, particularly in orthopedic and colorectal procedures. The growing deployment of robotic rehabilitation technologies across elderly and neurological care programs is also supporting market expansion.

Asia Pacific Medical Robots Market Trends

Asia Pacific is expected to register the fastest regional growth through 2033, fueled by healthcare infrastructure expansion, rising government healthcare spending, and increasing adoption of robotic-assisted medical technologies. Demand for robotic surgery, telemedicine platforms, and AI-driven hospital automation systems is rising rapidly as healthcare accessibility improves across major Asian economies.

China Medical Robots Market Trends

China is anticipated to account for nearly 34% of the Asia Pacific market in 2026, supported by rapid hospital modernization and strong government backing for domestic robotic manufacturing. Healthcare providers are steadily expanding robotic-assisted surgical capabilities across large urban hospitals, while local companies continue strengthening AI-integrated robotic platforms. In 2025, MicroPort MedBot expanded the commercialization of robotic surgery systems across major Chinese healthcare networks, highlighting the country’s growing competitiveness in medical robotics.

Japan Medical Robots Market Trends

Closely following, Japan is projected to contribute around 26% of the regional market in 2026, driven by its advanced robotics ecosystem and aging population. The country remains a leader in robotic rehabilitation, elderly care robotics, and smart hospital technologies designed to address long-term healthcare workforce challenges. Continued government support for healthcare automation and rehabilitation innovation is further accelerating robotic adoption across clinical and home care environments.

Competitive Landscape

The global medical robots market is moderately consolidated, with major companies including Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, and Stryker Corporation holding a significant share of global revenue. These players continue to strengthen their market position through strong hospital networks, regulatory expertise, and investments in AI-enabled surgical robotics, imaging integration, and digital surgery platforms.

Meanwhile, companies such as Zimmer Biomet, Cyberdyne Inc., and Hocoma AG are expanding across orthopedic robotics and rehabilitation technologies. While high regulatory and capital requirements limit new entrants, growing demand for AI-driven healthcare automation is creating opportunities for software-focused robotics and digital health companies. Strategic partnerships and technology collaborations are expected to intensify as competition increasingly shifts toward intelligent robotic healthcare ecosystems.

Key Industry Developments:

- In September 2025, Stryker Corporation announced strategic investments in orthopedic robotic navigation technologies to strengthen procedural accuracy and digital surgery capabilities. The initiative supported growing demand for robotic orthopedic interventions across North America and Europe.

- In April 2025, Zimmer Biomet Holdings, Inc. announced that its RibFix Advantage® Fixation System had received CE Mark certification, marking the first CE Mark for an intrathoracic rib fixation system.

Companies Covered in Medical Robots Market

- Intuitive Surgical

- Medtronic

- Stryker Corporation

- Johnson & Johnson MedTech

- Zimmer Biomet

- Siemens Healthineers

- GE HealthCare

- ABB Ltd.

- Omnicell Inc.

- Cyberdyne Inc.

- Hocoma AG

- Smith+Nephew

- Asensus Surgical

- Curexo Inc.

Frequently Asked Questions

The global medical robots market is projected to reach US19.4 billion in 2026.

Rising adoption of robotic-assisted surgery, hospital automation, and AI-enabled healthcare technologies drives the market.

The medical robots market is expected to grow at a CAGR of 14.3% from 2026 to 2033.

Growth opportunities are emerging in telemedicine robotics, rehabilitation systems, and AI-powered hospital automation solutions.

Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, and Stryker Corporation are key players in the medical robots market.