- Medical Devices

- Global Medical Cyclotron Market

Global Medical Cyclotron Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Medical Cyclotron Market by Product (Cyclotron 10-12 MeV, Cyclotron 16-18 MeV, Cyclotron 19-24 MeV, Cyclotron 24 MeV and Above), by Application (Cardiology, Cancer Treatment, Neurology, and Infectious Diseases) by End User (Hospitals, Diagnostic Imaging Centers, and Academic and Research Institutions), and Regional Analysis from 2026 to 2033.

Medical Cyclotron Market Size and Trend Analysis

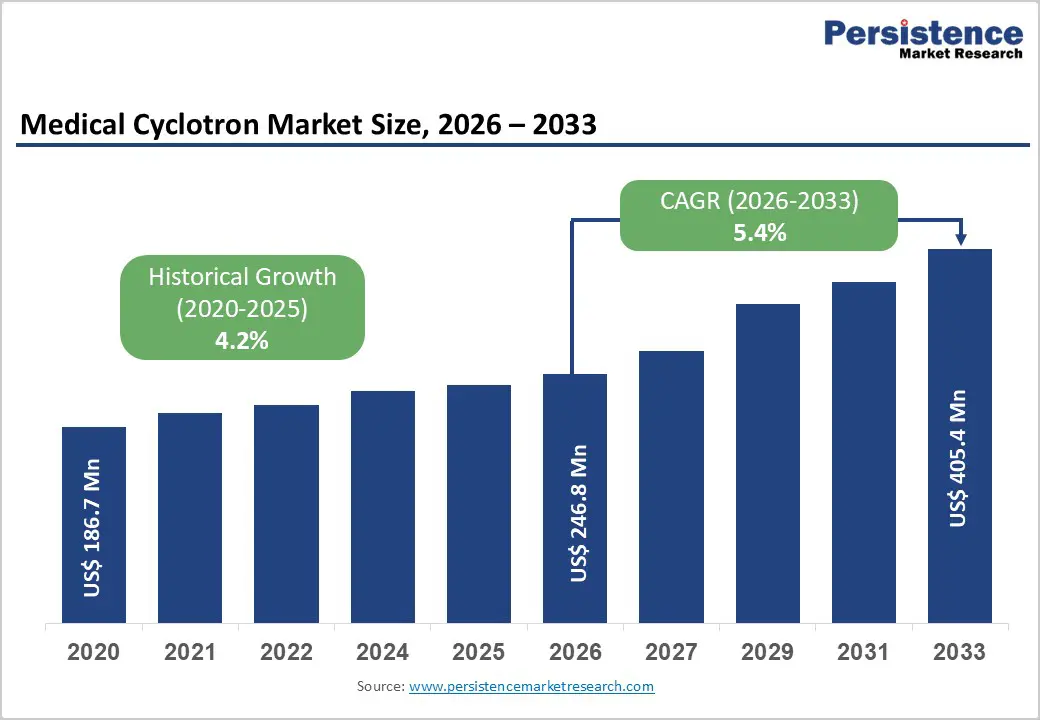

The global medical cyclotron market size is estimated to grow from US$ 246.8 Mn in 2026 to US$ 405.4 Mn by 2033. The market is projected to record a CAGR of 5.4% from 2026 to 2033.

Global demand for medical cyclotron systems is rising steadily, driven by the expanding adoption of PET imaging, growing investments in nuclear medicine and life sciences research, and a strong shift toward precision diagnostics and molecular imaging. The rising prevalence of cancer, cardiovascular diseases, and neurological disorders has significantly increased demand for cyclotron-produced radioisotopes such as fluorine-18 and carbon-11 used in PET/CT and PET/MRI applications. Expansion of hospitals, diagnostic imaging centers, academic research institutions, and radiopharmaceutical manufacturing facilities, combined with higher R&D spending and improved access to advanced imaging infrastructure, is accelerating market growth. Continuous innovation in cyclotron design, including compact systems, higher beam stability, automation, and improved target technologies, is enhancing isotope yield, operational efficiency, and safety. Additionally, growing adoption of theranostics, decentralized radioisotope production models, reduced dependency on external isotope supply chains, and rising awareness of early disease detection are further propelling market expansion globally.

Key Industry Highlights

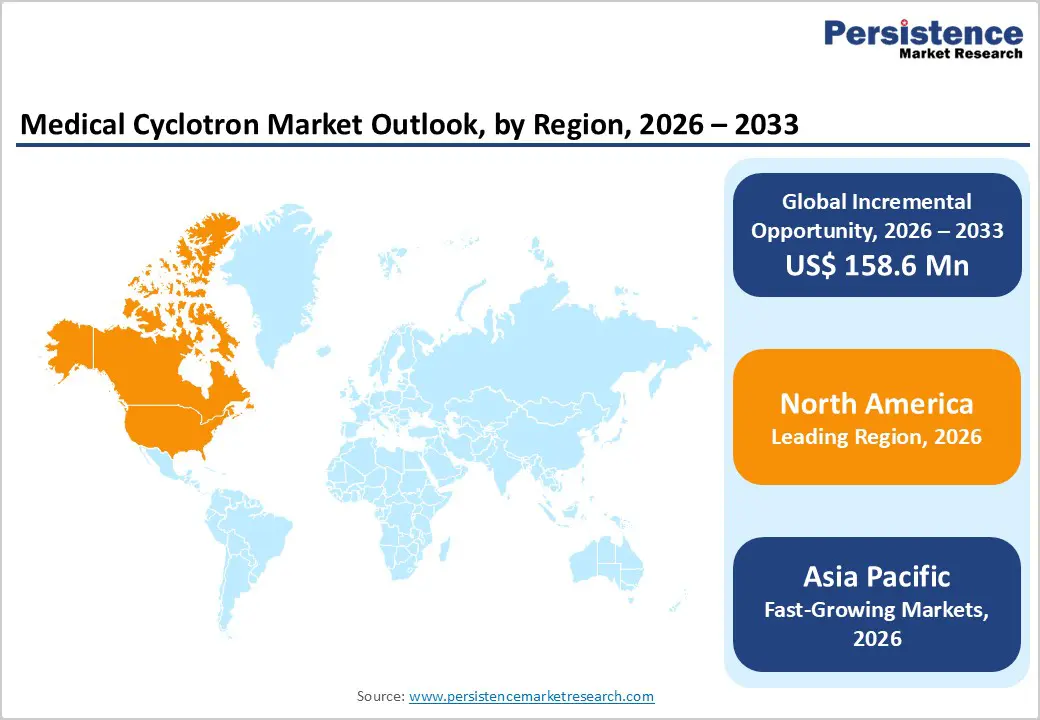

- Leading Region: North America holds the largest share at 47.8%, supported by a mature healthcare ecosystem, high penetration of PET imaging, strong presence of cyclotron manufacturers, robust R&D funding, favorable regulatory frameworks, and early adoption of advanced nuclear medicine technologies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, increasing cancer diagnosis rates, rising PET imaging installations, and growing government and private investment in nuclear medicine.

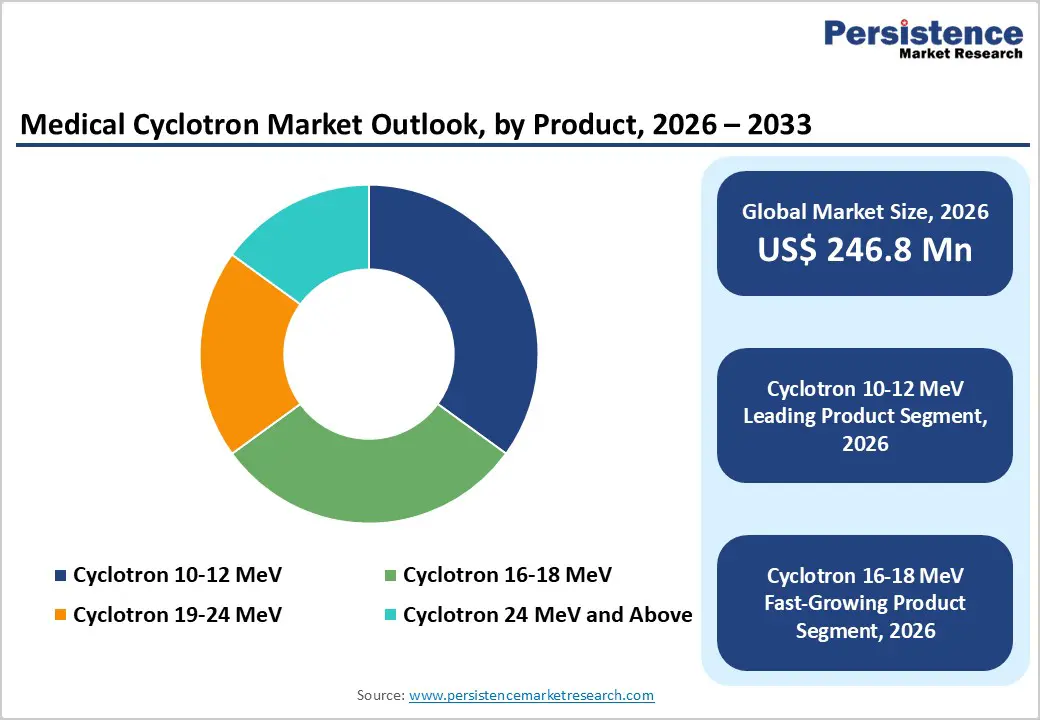

- Leading Product Segment: Cyclotron 10–12 MeV systems dominate the market due to their cost efficiency, compact design, and widespread use in routine PET radioisotope production.

- Fastest-Growing Product Segment: Cyclotron 24 MeV and above systems are expanding rapidly as demand increases for multi-isotope production and advanced theranostic applications.

- Leading Application Segment: Oncology remains the top application due to high utilization of PET imaging for cancer diagnosis, staging, and treatment monitoring.

- Fastest-Growing Application Segment: Neurology is scaling quickly as rising focus on early detection of neurodegenerative disorders and advanced molecular imaging drives adoption.

| Global Market Attributes | Key Insights |

|---|---|

| Medical Cyclotron Market Size (2026E) | US$ 246.8 Mn |

| Market Value Forecast (2033F) | US$ 405.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Rising Demand for PET Imaging, Radiopharmaceutical Production, and Precision Diagnostics Driving Medical Cyclotron Market Growth

The global medical cyclotron market is experiencing strong growth, driven by the rising adoption of PET imaging, expanding radiopharmaceutical production, and increasing emphasis on precision diagnostics. The growing global burden of cancer, cardiovascular diseases, and neurological disorders has significantly increased demand for cyclotron-produced radioisotopes, particularly fluorine-18, carbon-11, and other short-lived isotopes used in PET/CT and PET/MRI imaging. Medical cyclotrons enable onsite or near-site isotope production, addressing supply chain limitations associated with short half-lives and improving diagnostic reliability.

Continuous advancements in cyclotron technology, including compact designs, higher beam stability, improved target systems, and automation, are enhancing operational efficiency and isotope yield. Strong public and private investment in nuclear medicine infrastructure, especially in hospitals and diagnostic imaging centers, is accelerating system adoption. Additionally, expanding applications of theranostics and personalized medicine are increasing reliance on advanced molecular imaging, further strengthening demand. Favorable reimbursement for PET procedures in developed markets, coupled with growing awareness of early disease detection, supports sustained growth. Overall, rising diagnostic volumes, technological innovation, and expanding nuclear medicine capabilities are positioning the medical cyclotron market for long-term global expansion.

Restraints – High Capital Costs, Regulatory Complexity, and Infrastructure Requirements Limiting Market Penetration

The medical cyclotron market faces notable restraints related to high capital investment, regulatory complexity, and operational challenges. Medical cyclotrons require substantial upfront expenditure for system procurement, shielding, facility construction, and installation, which can limit adoption among smaller hospitals and imaging centers. Ongoing operational costs, including maintenance, skilled personnel, radiation safety compliance, and consumables, further increase the total cost of ownership.

Regulatory requirements for cyclotron installation and operation are stringent, involving licensing, radiation safety approvals, environmental clearances, and compliance with nuclear regulatory authorities. These processes are time-consuming and vary significantly across regions, creating delays and increasing project risk. Additionally, the need for specialized infrastructure, including hot cells, radiochemistry labs, and trained nuclear medicine professionals, poses challenges in emerging and resource-limited markets. Competition from centralized radioisotope suppliers and alternative imaging modalities can also impact demand in certain regions. Collectively, high costs, regulatory hurdles, and infrastructure constraints may slow adoption rates, particularly outside mature healthcare markets.

Opportunity – Expansion of Theranostics, Compact Cyclotron Adoption, and Emerging Market Infrastructure Development

The medical cyclotron market presents significant growth opportunities driven by the expansion of theranostics, increasing adoption of compact cyclotron systems, and rapid healthcare infrastructure development in emerging economies. Growing interest in theranostic applications combining diagnostic imaging and targeted radionuclide therapy is driving demand for diverse and high-purity radioisotopes, creating new use cases for higher-energy and multi-isotope cyclotrons. Technological innovation is enabling the development of compact, cost-efficient cyclotrons suitable for hospital-based and decentralized production models, lowering entry barriers and expanding addressable markets.

Emerging regions such as Asia Pacific, Latin America, and the Middle East are investing heavily in cancer care, diagnostic imaging, and nuclear medicine capabilities, creating strong long-term demand. Government initiatives supporting domestic radioisotope production, public–private partnerships, and healthcare modernization further enhance market access. Additionally, integrating automation, digital monitoring, and AI-driven optimization into cyclotron operations is improving efficiency and reducing operational complexity. Strategic collaborations between equipment manufacturers, radiopharmaceutical producers, and healthcare providers are accelerating adoption. These trends collectively position the medical cyclotron market for sustained growth and expanded global penetration.

Category-wise Analysis

By Product, Cyclotron 10–12 MeV Leads Due to Cost Efficiency and High PET Isotope Demand

The cyclotron 10–12 MeV segment is projected to lead the global medical cyclotron market in 2026, accounting for nearly 35.0% of total revenue. This dominance is primarily driven by its widespread use in producing fluorine-18 and other short-lived radioisotopes essential for PET imaging across oncology, cardiology, and neurology. These systems are widely adopted by hospitals and diagnostic imaging centers due to their compact design, lower installation costs, and suitability for decentralized, onsite isotope production. Additionally, Cyclotron 10–12 MeV systems benefit from simpler regulatory requirements, high operational reliability, and compatibility with automated radiopharmaceutical synthesis modules. Continuous advancements in target technology, system automation, and energy efficiency are improving isotope yield and operational uptime. Expanding PET/CT infrastructure and rising demand for early and accurate disease diagnosis globally are expected to sustain this segment’s leadership.

By Application, Oncology Leads Driven by Rising Cancer Burden and PET-Based Precision Diagnostics

The oncology segment is expected to dominate the global medical cyclotron market in 2026, capturing approximately 50.0% of revenue share, supported by the growing global cancer burden and increasing reliance on PET imaging for diagnosis, staging, and treatment monitoring. Cyclotron-produced radioisotopes, particularly fluorine-18, play a central role in oncology imaging by enabling high-resolution tumor visualization and personalized treatment planning. Continuous advancements in radiotracer development, including targeted imaging agents and theranostics, are further expanding oncology applications. Increased investment in cancer research, favorable reimbursement for PET procedures, and growing adoption of PET/CT and PET/MRI systems are reinforcing demand. The need for reliable and localized radioisotope production due to short half-lives further strengthens oncology’s leadership position.

By End User, Hospitals Lead Owing to Integrated Nuclear Medicine Infrastructure and High Patient Volume

Hospitals are projected to account for nearly 35.0% of the global medical cyclotron market revenue in 2026, driven by advanced clinical infrastructure, availability of skilled nuclear medicine professionals, and integrated diagnostic capabilities. Large hospitals and tertiary care centers increasingly invest in on-site cyclotrons to ensure uninterrupted radioisotope supply and optimized imaging workflows.

Hospitals also benefit from higher patient throughput, established reimbursement systems, and strong involvement in clinical research and academic collaborations. Integration of cyclotrons with PET imaging systems, automated radiopharmaceutical production, and digital workflow solutions further enhances efficiency. Continued investment in hospital-based nuclear medicine departments supports sustained market leadership.

Region-wise Insights

North America Medical Cyclotron Market Trends

North America is expected to maintain a leading position in the global medical cyclotron market, accounting for approximately 47.8% of total market value in 2026, driven primarily by the United States. The region benefits from a mature healthcare ecosystem, strong nuclear medicine infrastructure, and high adoption of PET imaging technologies. A dense concentration of hospitals, diagnostic imaging centers, and academic research institutions supports sustained demand for cyclotron installations. Robust R&D funding, favorable reimbursement frameworks, and streamlined regulatory pathways accelerate the adoption of advanced cyclotron systems and radiopharmaceuticals.

North America also leads in radiotracer innovation, clinical trials, and theranostics development, reinforcing long-term market growth. Public–private partnerships and government-backed initiatives supporting cancer diagnostics and molecular imaging further strengthen regional leadership. Additionally, widespread adoption of hybrid imaging systems, automation in isotope production, and digital workflow optimization enhance operational efficiency. Expansion of outpatient imaging centers and decentralized isotope production models continues to drive cyclotron demand. These factors collectively position North America as the most mature and revenue-dominant regional market.

Europe Medical Cyclotron Market Trends

The European medical cyclotron market is projected to grow steadily, supported by strong healthcare systems, advanced academic research, and high adoption of nuclear medicine technologies. Countries such as Germany, France, the U.K., Italy, and the Nordic region are key contributors, driven by well-established PET imaging networks and government-supported healthcare frameworks. European manufacturers and research institutions are actively investing in next-generation cyclotron technologies, energy-efficient systems, and sustainable isotope production.

Regulatory harmonization across the EU facilitates cross-border collaboration, clinical trials, and standardized distribution of radiopharmaceuticals. Public funding and academic–industry partnerships play a crucial role in advancing innovation and clinical adoption. Growing focus on early cancer diagnosis, neurological disorders, and cardiovascular imaging continues to drive demand. Additionally, Europe’s emphasis on cost-effective healthcare delivery and centralized isotope production hubs supports moderate but consistent market expansion. The integration of digital health solutions and automation further enhances efficiency across nuclear medicine facilities.

Asia Pacific Medical Cyclotron Market Trends

The Asia Pacific medical cyclotron market is expected to register the fastest CAGR of around 9.7% between 2026 and 2033, driven by rapid healthcare infrastructure development and increasing demand for advanced diagnostic imaging. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing significant growth in PET imaging capacity and nuclear medicine investments. Government initiatives supporting cancer screening, healthcare modernization, and domestic radiopharmaceutical production are accelerating the adoption of cyclotrons. The rising prevalence of cancer and neurological disorders, coupled with increasing awareness of early diagnosis, fuels market expansion.

Local manufacturing capabilities, cost-effective systems, and strategic collaborations with global players further enhance accessibility. Expansion of hospital networks, growth of private diagnostic imaging centers, and increasing clinical research activity strengthen long-term demand. Additionally, favorable demographics, improving reimbursement coverage, and rapid adoption of digital health platforms position the Asia Pacific as the most dynamic and high-growth region in the global medical cyclotron market.

Market Competitive Landscape

The global medical cyclotron market is highly competitive, with strong participation from IBA (Ion Beam Applications S.A.), GE HealthCare, Siemens Healthineers AG, and Sumitomo Heavy Industries (SHI). These companies leverage established global distribution networks, advanced cyclotron technologies, integrated radiopharmaceutical production capabilities, and long-standing relationships with hospitals, diagnostic imaging centers, and research institutions to strengthen their market positions.

Key players are increasingly focused on developing compact and high-energy cyclotron systems, improving operational efficiency, reliability, and isotope yield, and expanding applications across oncology, cardiology, and neurology. Strategic priorities include portfolio expansion through R&D and strategic acquisitions, lifecycle upgrades of installed cyclotron systems, cost optimization via modular and energy-efficient designs, and strengthening partnerships with healthcare providers and nuclear medicine centers to enhance access, adoption, and onsite radioisotope production.

Key Industry Developments:

- In September 2025, GE HealthCare, in partnership with the University of Oklahoma (OU) and Cyclomedical International, announced plans to install a new cyclotron at the OU Health campus, representing a significant advancement in regional capabilities for precision medicine, theranostics, and radiopharmaceutical research and production.

- In November 2024, construction began on a medical cyclotron facility at the National Institute of Science Education and Research (NISER), Bhubaneswar, to support local production of PET radioisotopes. The facility aims to reduce reliance on external supply chains and improve access to advanced molecular imaging and precision diagnostics across the region.

- In September 2024, BEST Cyclotron Systems, Inc. (BCSI), a subsidiary of TeamBest Global (TBG), announced the development of its B-11 cyclotron, designed to produce radioisotopes for medical, research, and other specialized applications. BCSI designs, manufactures, and installs a broad range of cyclotron systems for medical, industrial, and research use, with energy capabilities spanning from 1 MeV to 70 MeV.

Companies Covered in Global Medical Cyclotron Market

- Pfizer

- Eli Lilly and Company

- AbbVie, Inc.

- Teva Pharmaceutical Industries Ltd.

- Johnson & Johnson

- Sanofi

- GSk plc.

- Bayer AG

- TONIX Pharmaceuticals Holdings Corp

- Virios Therapeutics, Inc.

- Aptinyx Inc.

- FSD Pharma

- Others

Frequently Asked Questions

The global medical cyclotron market is projected to be valued at US$ 246.8 Mn in 2026.

Rising cancer prevalence, expanding PET/CT imaging volumes, and growing demand for cyclotron-produced medical radioisotopes drive the global medical cyclotron market.

The global medical cyclotron market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Adoption of compact cyclotrons, growth of theranostics, and expansion of PET infrastructure in emerging markets present major opportunities.

IBA (Ion Beam Applications S.A.), GE HealthCare, Siemens Healthineers AG, and Sumitomo Heavy Industries (SHI) are some of the key players in the medical cyclotron market.