- Sensors & Controls

- Industrial Wireless Sensor Network Market

Industrial Wireless Sensor Network Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Wireless Sensor Network market by Component (Hardware, Software, Services), Sensor / Network Type (Temperature Sensors, Pressure Sensors, Level Sensors, Flow Sensors, Humidity Sensors, Gas/Chemical/Environmental, Misc. (Motion/Position/Light)), Technology Type (WirelessHART, ISA100, Zigbee Mesh, Wi-Fi WLAN, Bluetooth BLE, Cellular LPWAN, NB-IoT, LTE-M, 5G, Others, Proprietary, Hybrid), Industry (Manufacturing/Industrial, Energy & Utilities, Oil & Gas/Petrochemical, Automotive & Transportation, Food/Beverage,), and Regional Analysis for 2026 - 2033

Industrial Wireless Sensor Network Market Size and Trends Analysis

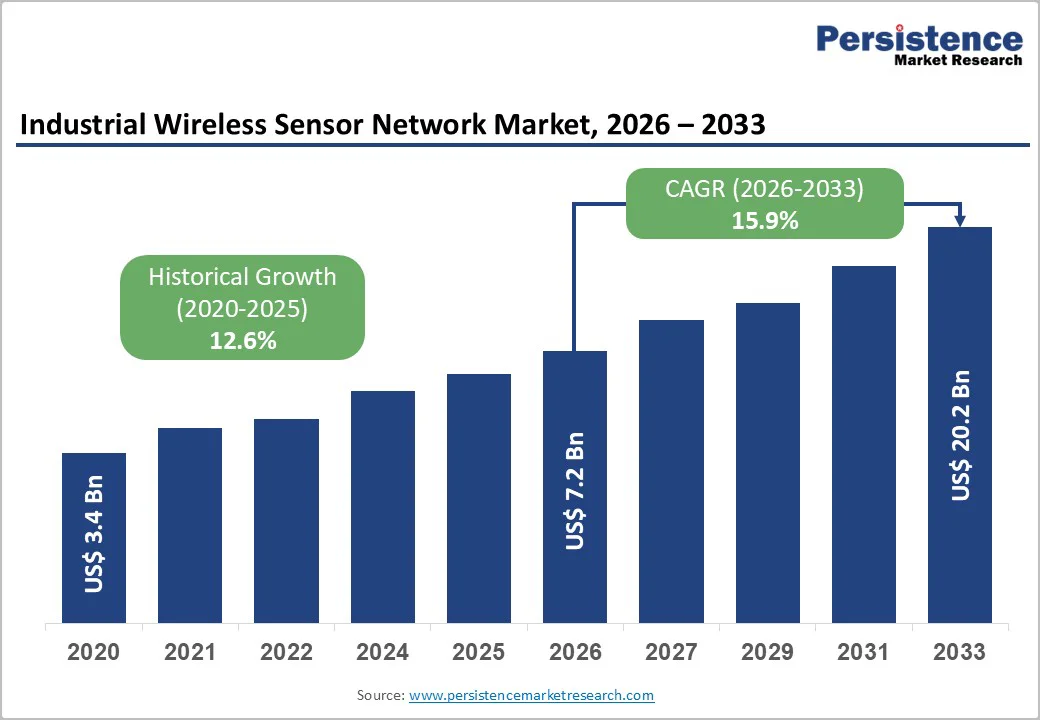

The global industrial wireless sensor network market size is likely to be valued at US$7.2 billion in 2026 and is projected to reach US$20.2 billion by 2033, growing at a CAGR of 15.9% between 2026 and 2033. The historical CAGR from 2020 to 2026 was 12.6%, indicating acceleration in growth momentum as manufacturing enterprises prioritise real-time operational monitoring and predictive maintenance capabilities.

Primary growth catalysts include structural demand from smart factory deployments, government-backed Industry 4.0 initiatives across North America, Europe, and the Asia-Pacific region, and the transition toward energy-efficient, batteryless sensor architectures. The industrial wireless sensor network market is characterised by rapid convergence between broadband connectivity standards (Wi-Fi 6, 5G) and specialised industrial protocols (WirelessHART, ISA100), driven by substantial government investment in manufacturing modernisation and digital infrastructure development.

Key Industry Highlights:

- Government-Backed Digitalisation Initiatives: Government mandates, such as India's PLI scheme and Germany's "Industrie 4.0," are significantly increasing capital investment in industrial wireless sensor networks, driving widespread IoT integration across manufacturing operations.

- Predictive Maintenance Driving Adoption: With validated returns, such as a 35-45% reduction in unplanned downtime, sectors like automotive and oil & gas are adopting wireless sensor networks to optimise equipment life and reduce operational costs.

- 5G and Energy-Harvesting Innovations: The rollout of 5G networks and advances in energy-harvesting sensor technology are enabling high-density, low-maintenance sensor deployments in remote industrial locations, reshaping market operational efficiency.

- Key Market Segments: Temperature sensors dominate sensor-type revenue at 24%, while pressure sensors, driven by safety-compliance and real-time monitoring needs in hazardous environments, exhibit the fastest growth.

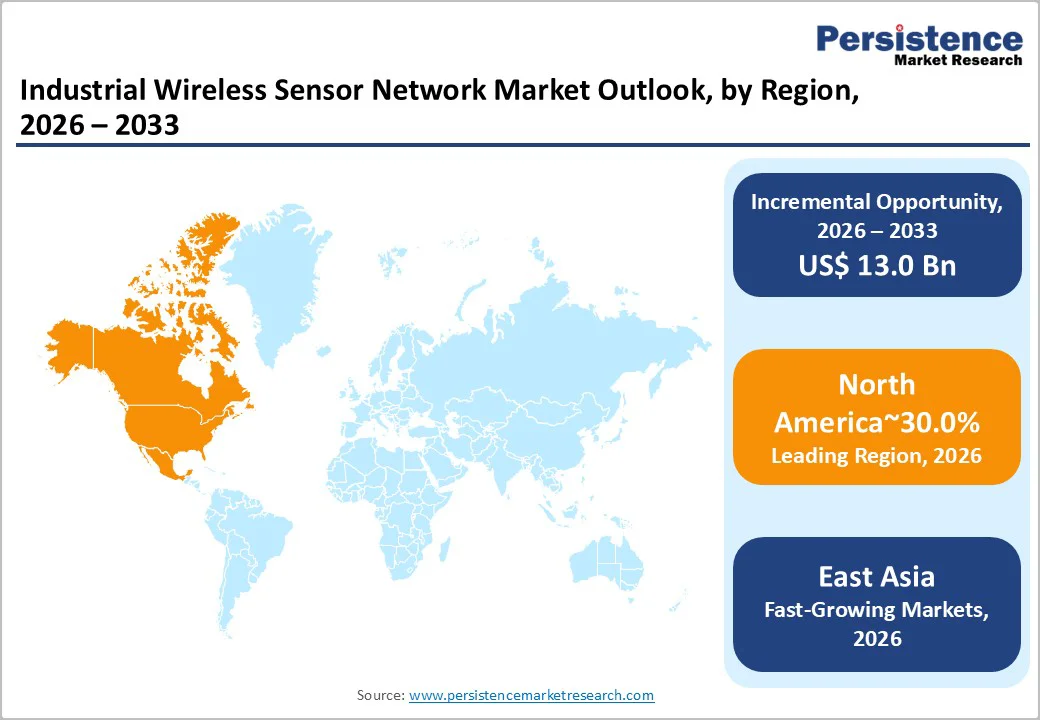

- Region-Specific Growth: North America leads the market with a 30% share, driven by strong manufacturing modernisation programs, while East Asia, led by China, is expected to grow at 23.6% CAGR, fueled by government initiatives and smart city projects.

- Edge AI and Self-Healing Networks: The integration of edge AI and self-healing network protocols is opening new opportunities for autonomous asset management, enhancing the market’s appeal in industries demanding minimal human intervention.

- Cybersecurity Challenges: As wireless sensor deployments expand, complex cybersecurity requirements, especially in critical infrastructure sectors, are increasing costs and hindering adoption among small and medium enterprises, particularly in developing economies.

| Key Insights | Details |

|---|---|

| Industrial Wireless Sensor Network market Size (2026E) | US$ 7.2 Bn |

| Market Value Forecast (2033F) | US$ 20.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.6% |

Market Dynamics

Drivers - Government-Mandated Manufacturing Modernisation and Industry 4.0 Investment Programs

Across developed and emerging economies, government initiatives targeting manufacturing digitalisation are driving substantial capital allocation to industrial wireless sensor infrastructure. India's Production-Linked Incentive (PLI) scheme approved 806 projects representing rupees 1.76 lakh crore in realised investments by March 2025, directly embedding IoT and sensor network deployments into manufacturing operations; these government-backed PLI participants generated total sales exceeding rupees 16.5 lakh crore by June 2025. Germany's "Industrie 4.0" initiative has accelerated sustained investment in IoT-enabled manufacturing systems, creating multiplier effects across the European industrial wireless sensor network ecosystem.

India's SAMARTH Centres (Smart Advanced Manufacturing and Rapid Transformation Hubs) operate four government-established facilities that provide workforce training and Industry 4.0 technology awareness to industries and MSMEs, with 10 additional cluster Industry 4.0 experience centres approved under a hub-and-spoke model that establishes nationwide innovation infrastructure.

The industrial wireless sensor network market benefits directly from government policy frameworks, reducing capital barriers to deployment. Credit-linked capital subsidies help MSMEs upgrade to connected machinery, and INR 60,000 crore is allocated over five years to modernize approximately 1,000 Industrial Training Institutes. India's IndiaAI Mission, approved in March 2024 with an allocation of Rs 10,370 crore over five years, is building national compute grids and AI datasets to enhance wireless sensor network deployment through edge-AI capabilities for real-time anomaly detection and predictive maintenance optimization.

Predictive Maintenance ROI Validation and Operational Resilience Imperatives

Quantified economic returns from predictive maintenance deployments are validating investments in wireless sensor networks across manufacturing segments. The U.S. Department of Energy documents 70–75% reductions in equipment breakdowns through sensor-enabled predictive maintenance, with 35–45% reductions in unplanned downtime and a potential 10x return on investment within 18–24 months of deployment.

Manufacturing facilities implementing predictive analytics across critical production lines report 40% reductions in emergency maintenance calls, 15% increases in overall equipment effectiveness (OEE), and a 20–30% increase in equipment lifespan through early fault detection. Deloitte's 2025 Smart Manufacturing Survey indicates that 78% of respondents allocate more than 20% of their overall improvement budgets to smart manufacturing initiatives, including wireless sensor networks, and 88% expect investments to continue or increase in the next fiscal year.

Predictive maintenance implementation reduces maintenance labour requirements by 18–25% and reduces maintenance costs by 20–50% compared to reactive maintenance methodologies. These quantifiable performance metrics are driving adoption of industrial wireless sensor networks across the automotive, oil & gas, chemicals, and discrete manufacturing sectors, with vibration sensors for rotating-asset monitoring growing at a 19.4% CAGR as predictive-maintenance frameworks mature from pilot implementations to corporate-wide standardisation.

The convergence of sensor miniaturization, edge-AI processing, and 5G connectivity is enabling real-time equipment health dashboards that provide maintenance teams with actionable intelligence, thereby reinforcing the structural growth of the industrial wireless sensor network market.

5G Deployment Infrastructure and Energy-Harvesting Sensor Technology Maturation

The global rollout of 5G networks is enabling unprecedented wireless sensor connectivity density and data-transmission reliability critical for the industrial wireless sensor network market expansion. India achieved 5G launch across all states and union territories by October 2024, with 4.98 lakh 5G Base transceiver stations installed nationwide, covering 99.6% of districts and 365 million 5G subscribers by July 2025, representing 35% penetration. This digital infrastructure foundation is creating the backhaul capacity necessary for large-scale wireless sensor deployment in manufacturing operations. Concurrent advancements in energy-harvesting sensor technology are addressing the persistent maintenance burden of battery-dependent wireless nodes.

Energy-harvesting solutions utilising thermoelectric, photovoltaic, and piezoelectric generation from ambient heat, light, vibration, and electromagnetic sources enable zero-maintenance, battery-free sensor deployments suitable for remote, hard-to-access industrial locations. E-peas' Ambient Energy Managers would allow sensors to self-recharge from environmental energy sources, eliminating routine battery-change cycles and enabling supercapacitor-based power storage for extended autonomous operation even during power-supply interruptions.

This technological convergence between 5G backhaul infrastructure and energy-harvesting sensor architectures is fundamentally reshaping the economics of the Industrial Wireless Sensor Network Market, enabling sustainable deployments in hazardous areas, offshore installations, and distributed manufacturing facilities where traditional wired infrastructure and battery logistics are operationally prohibitive.

Restraint - Cybersecurity Complexity and Real-Time Threat Detection Costs

Security architecture requirements introduce substantial complexity and capital expenditure into industrial wireless sensor network deployments. Wireless network architectures inherently expose sensor data flows to interception, spoofing, and denial-of-service attacks; industrial manufacturing environments prioritise uninterrupted operational continuity, requiring real-time threat detection and response capabilities that exceed typical IT-grade security solutions.

Nozomi Networks' Guardian Air™ wireless spectrum sensor, designed to enable continuous monitoring of Bluetooth, Wi-Fi, cellular, LoRaWAN, Zigbee, and WirelessHART protocols, is part of the advanced security infrastructure required for enterprise deployments. Integration of such specialised monitoring platforms with existing SCADA, MES, and ERP systems incurs non-trivial capital and operational costs, deterring adoption of Industrial Wireless Sensor Networks among cost-sensitive manufacturers.

Regulatory compliance frameworks, including the National Institute of Standards and Technology (NIST) Industrial Wireless Guidelines, mandate encryption, authentication, and network segmentation requirements that increase system complexity and demand specialised cybersecurity expertise within manufacturing organisations. This security-infrastructure investment barrier is particularly acute for small and medium enterprises (SMEs), which collectively represent 90% of Indian manufacturing companies but face resource constraints in cybersecurity architecture design and maintenance.

Opportunities - Edge AI Integration and Self-Healing Network Architectures for Autonomous Asset Management

The convergence of edge artificial intelligence and industrial wireless sensor networks is creating substantial market opportunities for autonomous asset-management systems that require minimal human intervention. Embedded edge AI enables real-time anomaly detection, equipment-status classification, and failure-prediction modelling on sensor cluster heads and gateways without requiring cloud-platform latency penalties, supporting mission-critical closed-loop control applications. Federated learning approaches, distributing machine-learning model training across sensor clusters without centralizing sensitive operational data, enable privacy-preserving, distributed intelligence architectures aligned with data-localisation regulations increasingly prevalent across manufacturing jurisdictions.

Self-healing network protocols dynamically reconfigure wireless sensor network topology in response to node failures, link degradation, or electromagnetic interference, maintaining operational continuity without manual intervention. This autonomous network resilience is particularly valuable for distributed manufacturing facilities spanning multiple geographic locations where centralized network management is operationally infeasible.

The industrial wireless sensor network market is positioned to expand through software-defined sensor orchestration platforms, enabling manufacturers to dynamically adjust monitoring granularity, data-transmission frequency, and analytical sophistication based on real-time equipment conditions.

Emerson's May 2025 Project Beyond initiative, integrating AI orchestration and zero-trust security into a software-defined operations platform, exemplifies this architectural shift toward autonomous, intelligent Industrial Wireless Sensor Network systems that unify legacy automation islands and enable data-driven decision-making with minimal operator engagement.

Standardisation Convergence and Matter-Compliant Gateway Ecosystems Supporting Interoperability

The emergence of Matter protocol as a universal standard for smart-home and industrial device connectivity is reducing fragmentation within industrial wireless sensor network ecosystems and enabling simplified interoperability architectures. Matter-compliant gateway development represents an opportunity for wireless sensor vendors to position products within standardised, cloud-agnostic ecosystems that reduce customer lock-in and accelerate adoption velocity through simplified system integration.

International electrotechnical standardisation organisations, including the International Electrotechnical Commission (IEC), are advancing wireless industrial standards, including WirelessHART and ISA100.11a, toward broader industry acceptance, with WirelessHART commanding over 30 million installed field devices globally and ISA100.11a expanding adoption at 36% growth over the past two years. This standardisation convergence reduces customer risk associated with proprietary wireless protocols, addressing historical manufacturer hesitation to deploy large-scale Industrial Wireless Sensor Network systems, absent industry consensus on interoperability standards.

The Industrial Wireless Sensor Network Market will expand as competing vendors coalesce around common protocols, reducing switching costs and enabling portable sensor applications across heterogeneous manufacturing environments. Nozomi Networks' integration of wireless spectrum monitoring into its Vantage platform exemplifies this ecosystem opportunity, providing unified visibility across diverse wireless technologies, including Bluetooth, Wi-Fi, cellular, Zigbee, and WirelessHART, within a single integrated security and monitoring architecture.

Category-wise Analysis

Component Insights

Hardware components represent the dominant component-segment revenue within the Industrial Wireless Sensor Network Market in 2026, capturing 52.0% of global sales. Hardware encompasses sensor nodes, RF transceivers, gateways, repeaters, and ancillary electronic modules constituting the physical infrastructure for wireless data collection and transmission. The dominance of hardware revenue reflects the capital-intensive nature of wireless sensor network deployments, requiring substantial upfront investment in sensor procurement, installation infrastructure, and backbone networking equipment to enable enterprise-scale monitoring across manufacturing facilities.

Sensor node miniaturisation and cost reduction, driven by competition among semiconductor manufacturers, including STMicroelectronics, Intel, and specialised IoT-component suppliers, are sustaining hardware revenue growth despite declining unit costs. STMicroelectronics' November 2025 launch of the ISM6HG256X three-in-one motion sensor integrating dual-range accelerometers and a precision gyroscope exemplifies ongoing hardware innovation targeting compact, multi-functional sensor designs that reduce bill-of-materials costs while maintaining industrial-grade reliability.

Gateway hardware incorporating edge-processing capabilities, advanced filtering, and cybersecurity functions commands a premium price, reflecting enhanced functionality and supporting sustained hardware revenue growth despite commoditization pressure on basic sensor modules.

Sensor/ Network Insights

Temperature sensors are the largest revenue contributor among sensor types in the Industrial Wireless Sensor Network Market in 2026, capturing 24.0% of global sales. Temperature measurement is fundamental to process control, environmental monitoring, and equipment health assessment across nearly all manufacturing verticals, including chemicals, food & beverage, pharmaceuticals, and discrete manufacturing. Thermal monitoring enables early detection of process deviations, cooling-system failures, and equipment overload conditions that could otherwise escalate into catastrophic failures or safety incidents.

Pressure sensors are the fastest-growing sensor type in the industrial wireless sensor network market, driven by mandatory safety compliance requirements and real-time pipeline integrity monitoring across the oil & gas, chemical, and utilities sectors.

Pressure sensor adoption accelerates in hazardous operating environments, where wired pressure-transmitter installation through classified zones is cost-prohibitive and operationally complex. Wireless pressure sensors enable monitoring of pipeline integrity, wellhead pressure, storage-vessel conditions, and process-control setpoints without the extensive cabling, conduit, and infrastructure installation required for legacy wired pressure-transmitter systems.

Technology Type Insights

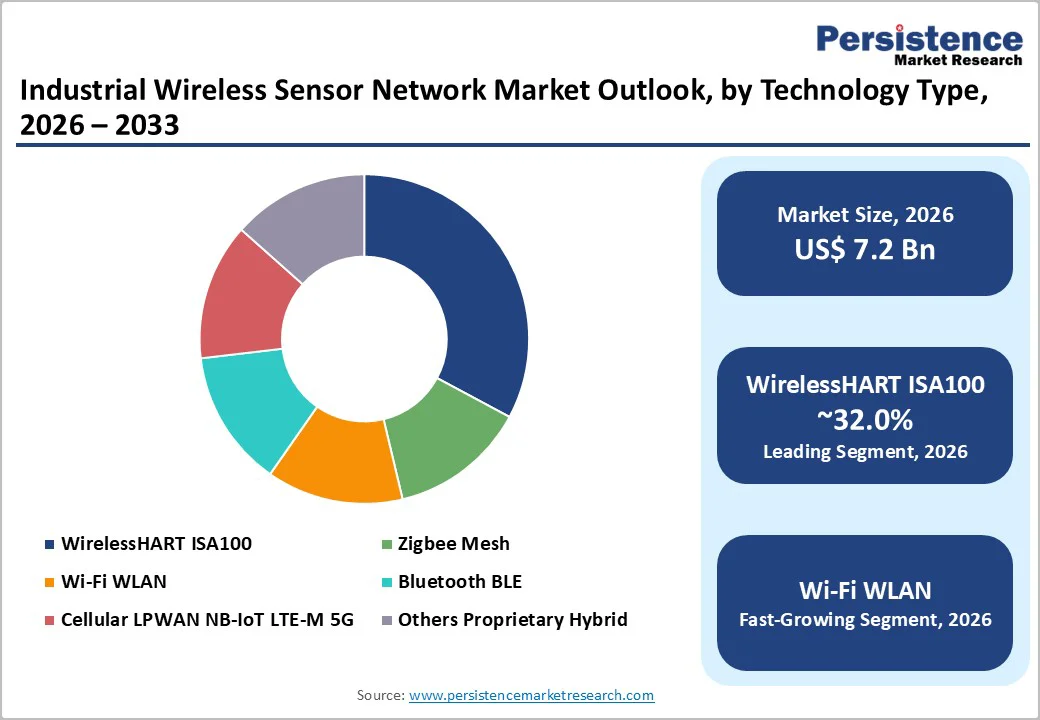

WirelessHART ISA100 represents the dominant technology standard within the Industrial Wireless Sensor Network Market in 2026, commanding 32.0% of global market revenue. These deterministic wireless standards were purpose-designed for closed-loop process control, supervisory monitoring, and regulatory-compliant field-device communication in process automation industries.

WirelessHART's industry dominance stems from backward compatibility with legacy wired HART protocol infrastructure deployed across petroleum refining, chemical processing, power generation, and water utilities, enabling cost-effective wireless retrofits without requiring complete sensor replacement.

WirelessHART deployment benefits from over 30 million installed field devices globally and established industry acceptance, reducing customer risk associated with emerging wireless standards. ISA100.11a standard provides complementary coverage for flexible industrial applications requiring broader channel allocation and less deterministic latency tolerance than WirelessHART closed-loop control deployments.

Wi-Fi WLAN is the fastest-growing technology segment in the Industrial Wireless Sensor Network Market, driven by the maturation of industrial-grade Wi-Fi infrastructure, integration with edge-computing platforms, and cost-effective broadband connectivity supporting data-intensive applications. Industrial-grade Wi-Fi 6 (802.11ax) deployment enables manufacturers to converge sensor networks, real-time video monitoring, mobile-worker communication, and enterprise IT connectivity onto a unified wireless infrastructure, reducing total-cost-of-ownership relative to maintaining segregated wireless networks.

Regional Insights and Trends

North America Industrial Wireless Sensor Network Market Trends

North America is the largest market, accounting for approximately 30% of global revenue. The United States leads the region, driven by mature manufacturing infrastructure modernisation programs, substantial capital availability for digital transformation, and an advanced telecommunications backbone supporting industrial wireless sensor network deployments.

The U.S. industrial wireless sensor market is expanding rapidly with high Industrial Internet of Things (IIoT) solution penetration among advanced manufacturers. Government support through initiatives, including the National Institute of Standards and Technology (NIST) Industrial Wireless Guidelines, developed collaboratively with IEEE through structured working groups, has provided best-practice frameworks for designing, selecting, deploying, and securing industrial wireless systems in factory environments. These guidelines have been adopted by industry and academia and have influenced standards development. These government-sponsored guidance documents reduce deployment risk and accelerate adoption velocity by establishing consensus technical standards and security architectures.

Canada's growing satellite-launch activities and research infrastructure investments are diversifying opportunities beyond U.S. defence-oriented applications, creating emerging demand for wireless sensor networks supporting satellite ground systems and space-technology research infrastructure.

North American manufacturers demonstrate strong investment capacity, with 78% allocating more than 20% of their improvement budgets to smart manufacturing initiatives, including wireless sensor networks. Major multinational manufacturers-including General Electric, Emerson, Siemens North America, Rockwell Automation, and Honeywell-maintain substantial engineering and product development infrastructure across the region, supporting rapid innovation and market-specific solution development.

East Asia Industrial Wireless Sensor Network Market Market Trends

East Asia represents the second-largest industrial wireless sensor network market, accounting for approximately 22% of global revenue and projected to have the fastest growth rates through 2033. China dominates regional revenue, driven by unprecedented manufacturing-sector digitalisation and government mandates for Industry 4.0 adoption aligned with "Made in China 2025" strategic objectives. China's wireless sensor network market is projected to grow at 23.6% CAGR, substantially exceeding global averages, propelled by government investment in smart city infrastructure, industrial automation deployment, and large-scale connected-infrastructure projects.

Chinese manufacturing hubs across electronics, automotive, and consumer-goods industries are adopting wireless sensors for predictive maintenance, process optimisation, and quality assurance at scale. Government initiatives, including the Industrial Internet Consortium and state-level Industry 4.0 centres, are accelerating wireless sensor adoption across SME clusters that historically operated with limited automation infrastructure.

Domestic technology companies, including Huawei and Xiaomi, are implementing comprehensive Industrial Wireless Sensor Network solutions across manufacturing operations, establishing reference implementations that validate technology value propositions and accelerate broader adoption across regional competitors.

Europe Industrial Wireless Sensor Network Market Trends

Europe accounts for a sizeable share of revenue, with a distinct emphasis on regulatory compliance, sustainability frameworks, and defence industrial modernisation. Germany leads European adoption through sustained implementation of the "Industrie 4.0" initiative and an advanced manufacturing ecosystem centred on the automotive, chemicals, and machinery industries. The European Electronic Communications Code (EECC) provides standardised regulatory frameworks for wireless network deployment, and the Radio Spectrum Policy Group's guidance harmonises spectrum allocation across EU member states to support coordinated expansion of Industrial Wireless Sensor Networks.

Competitive Landscape

The global Industrial Wireless Sensor Network (IWSN) market is moderately fragmented with oligopolistic influence, driven by a mix of major automation companies, semiconductor manufacturers, and specialized sensor providers.

Leading players such as ABB Ltd., Schneider Electric, Emerson Electric Co., Yokogawa Electric Corporation, Analogue Devices Inc., and Texas Instruments hold strong positions due to their broad product portfolios, established industrial customer base, and deep integration with industrial control and automation systems. These companies dominate large-scale deployments across manufacturing, energy, oil & gas, and process industries, leveraging advanced wireless standards, reliable sensing technologies, and industrial-grade connectivity solutions.

Competition intensifies as firms such as STMicroelectronics, Banner Engineering, Endress+Hauser, and NXP Semiconductors innovate in low-power sensing, edge intelligence, and ruggedised wireless modules tailored to harsh industrial environments. Growing adoption of IIoT, demand for predictive maintenance, and rising investments in cyber-secure wireless infrastructure continue to shape the competitive dynamics. Overall, the market reflects a fragmented landscape with strong leadership concentration among top-tier automation and semiconductor companies.

Key Industry Developments

- April 21, 2025, Microsoft Power BI was recognised as a Leader in the Forrester Wave™: Industrial Wireless Sensor Networks, Q2 2025. The platform achieved the highest score among all vendors in generative AI functionality and secured top scores in 17 additional evaluation criteria. Forrester highlighted Microsoft’s continuous innovation, strong partner ecosystem, and the ability of Power BI to meet nearly all enterprise BI requirements, reinforcing its leadership position in the global Industrial Wireless Sensor Network market.

- On November 18, 2025, Microsoft announced Fabric IQ at Microsoft Ignite 2025, marking a major evolution of its Industrial Wireless Sensor Network by introducing a unified semantic intelligence layer integrated with Power BI and Microsoft Fabric. Fabric IQ enhances BI capabilities with ontology-driven semantic modelling, real-time intelligence, graph-based insights, and autonomous Operations Agents, enabling enterprises to convert unified data into real-time business understanding and automated decision-making.

Companies Covered in Industrial Wireless Sensor Network Market

- STMicroelectronics

- ABB Ltd. / ABB (considered the same, kept as ABB Ltd.)

- Endress+Hauser Management AG

- Banner Engineering Corp.

- Schneider Electric

- Emerson Electric Co.

- Yokogawa Electric Corporation

- NXP Semiconductors

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Advantech Co., Ltd.

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Intel Corporation

Frequently Asked Questions

The global Industrial Wireless Sensor Network market is projected to be valued at US$ 7.2 Bn in 2026.

The WirelessHART ISA100 segment is expected to account for approximately 32.0% of the global Industrial Wireless Sensor Network market by Technology Type in 2026.

The market is expected to witness a CAGR of 15.9% from 2026 to 2033.

The Industrial Wireless Sensor Network market growth is driven by government-backed digitalization initiatives, predictive maintenance adoption, 5G deployment, and advancements in energy-harvesting sensor technologies.

Key market opportunities in the Industrial Wireless Sensor Network market include Edge AI integration for autonomous asset management, self-healing network architecture, and the development of Matter-compliant gateways to enhance interoperability across standardized ecosystems.

The key players in the Industrial Wireless Sensor Network market include Microsoft Corporation, Salesforce, Qlik, SAP SE, Oracle Corporation, and IBM Corporation.