- Semiconductor Materials & Components

- MEMS Pressure Sensors Market

MEMS Pressure Sensors Market Size, Trends, Share, and Growth Forecast 2026 - 2033

MEMS Pressure Sensors Market by Sensor Technology (Piezoresistive, Capacitive, Optical, Others), by Pressure Type (Absolute, Gauge, Differential, Sealed Gauge), by Sales Channel (Direct Sales, Distributors, Online Platforms, OEM Contracts), End-user (Automotive, Consumer Electronics, Industrial, Others), by Regional Analysis, 2026 - 2033

MEMS Pressure Sensors Market Size and Trend Analysis

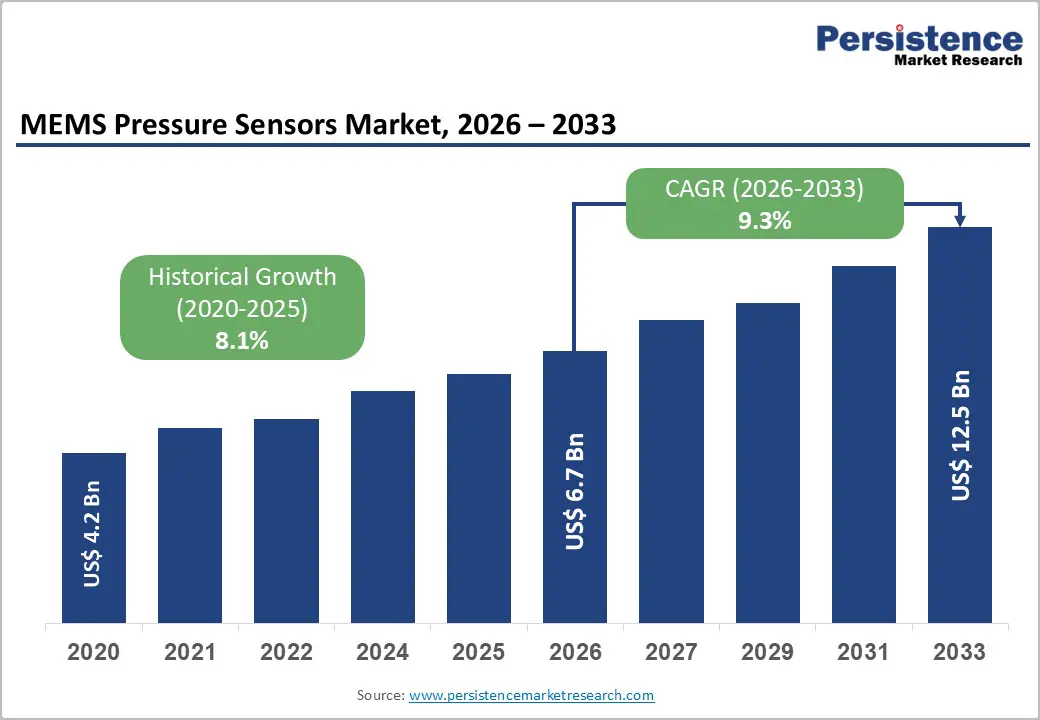

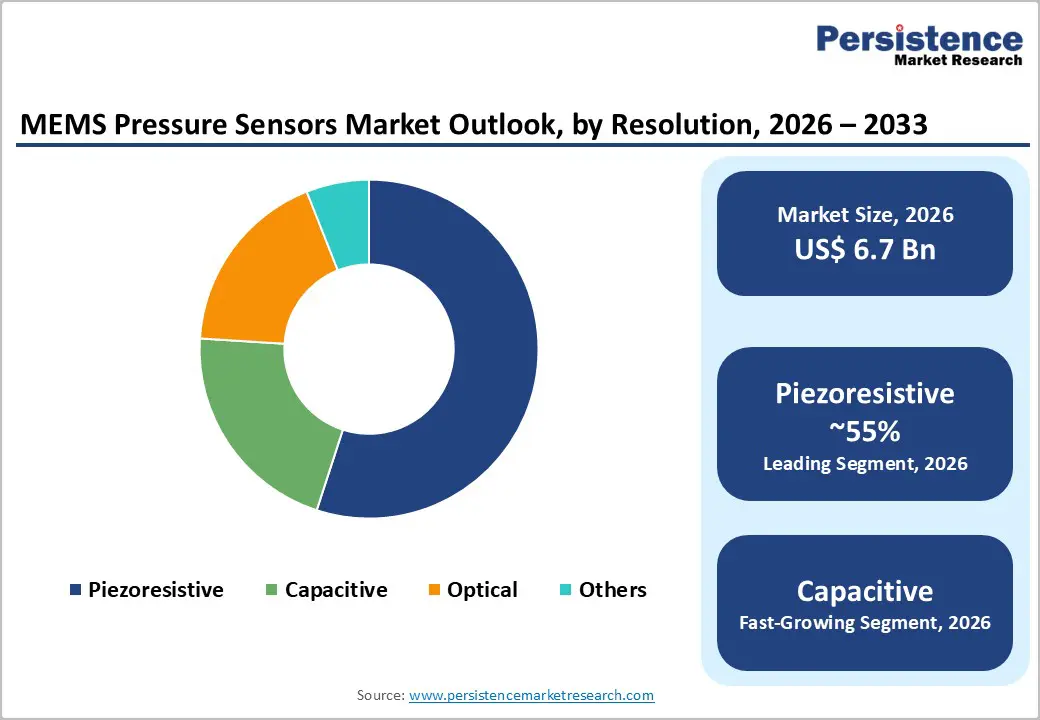

The global MEMS pressure sensors market size is likely to be valued at US$ 6.7 billion in 2026 and is expected to reach US$ 12.5 billion by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 and 2033.

Strong adoption of compact, low-power pressure-sensing in automotive, consumer electronics, and industrial IoT applications is the primary driver of growth, as OEMs increasingly embed multi-sensor modules for real-time monitoring and control.

Key Industry Highlights:

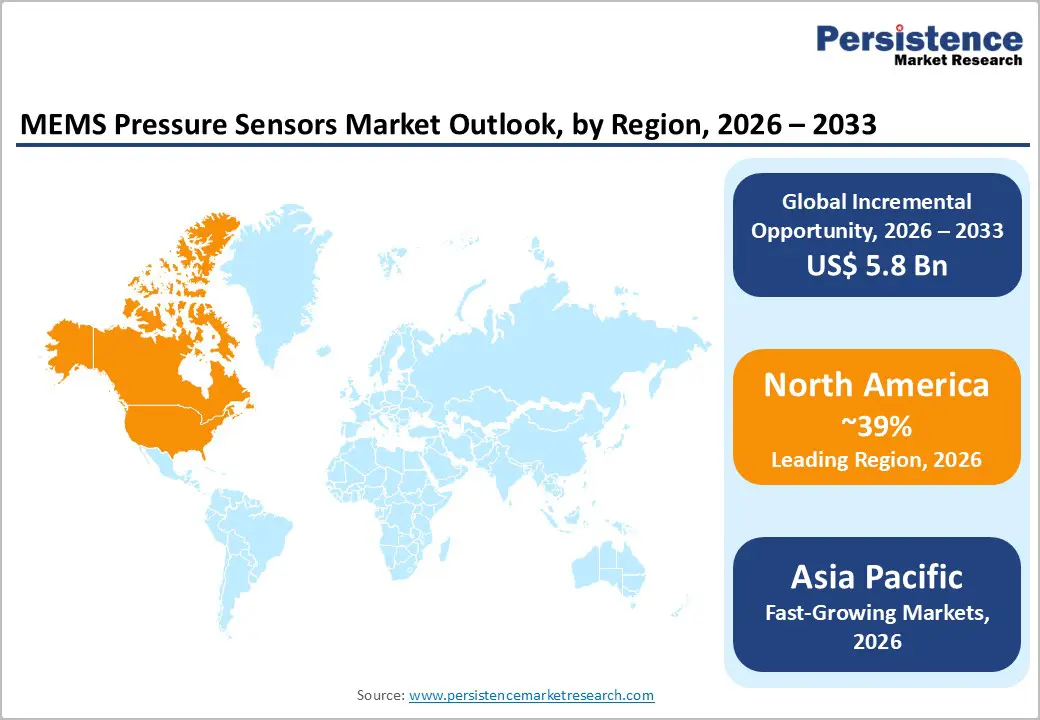

- Leading Region: North America is a leading region in the MEMS Pressure Sensors Market, holding a 39% share, supported by stringent vehicle safety regulations, established industrial and aerospace sectors, and a strong presence of global sensor manufacturers and Tier-1 suppliers across the U.S. and Canada.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 11.2%, driven by large-scale automotive and consumer electronics production in China, Japan, South Korea, and ASEAN, coupled with expanding EV, IoT, and smart manufacturing initiatives that significantly raise sensor content per device.

- Leading Segment: The automotive segment dominates end-use demand, accounting for 40% share of the global MEMS Pressure Sensors Market, due to widespread utilization in TPMS, engine and exhaust management, braking, and HVAC systems, along with accelerating adoption in electrified and connected vehicles worldwide.

- Fastest-Growing Segment: Piezoresistive sensor technology and absolute pressure type are leading segments, benefiting from their versatility, robustness, and broad deployment in automotive, industrial, and consumer barometric sensing, thereby capturing the largest shares within the sensor technology and pressure type categories globally.

- Key opportunities lie in AI-enabled smart sensors and EV-focused pressure-sensing solutions, where integrated microcontrollers, advanced diagnostics, and software intelligence enable differentiated offerings for mobility, industrial IoT, and wearables, supporting higher value capture beyond commoditized sensor hardware.

| Key Insights | Details |

|---|---|

| MEMS Pressure Sensors Market Size (2026E) | US$ 6.7 Billion |

| Market Value Forecast (2033F) | US$ 12.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 9.3% |

| Historical Market Growth (2020 - 2025) | 8.1% |

Market Dynamics

Drivers - Mandatory Automotive Safety Regulations and TPMS Adoption Drive Sustained Demand for MEMS Pressure Sensors Worldwide

Stringent automotive safety regulations mandating the use of tire pressure monitoring systems (TPMS) are a major growth driver for the MEMS Pressure Sensors Market, particularly across North America, Europe, and China. In the United States, TPMS has been compulsory for all new passenger vehicles since 2007, while the European Union introduced similar mandates in 2014. These regulations compel automotive OEMs to integrate pressure sensors into every wheel as well as related safety and control systems. As a result, demand for compact, reliable, and highly integrated MEMS pressure sensors continues to rise.

Leading manufacturers such as Bosch and Infineon are commercializing advanced TPMS solutions, including Bosch’s SMP290 and Infineon’s XENSIV™ SP49, which integrate pressure sensing, acceleration sensing, microcontrollers, and wireless communication in a single module. The growing adoption of advanced driver assistance systems (ADAS) and electric vehicles further increases demand, as precise pressure monitoring is essential for vehicle safety, energy efficiency, driving-range optimization, and overall performance.

Rapid Expansion of Consumer Electronics and Industrial IoT Ecosystems Accelerates MEMS Pressure Sensor Penetration

The rapid expansion of smartphones, wearables, smart home devices, and industrial IoT platforms is significantly driving the adoption of MEMS pressure sensors across both consumer and industrial applications. In consumer electronics, MEMS pressure sensors are widely used to enable altitude detection, indoor navigation, and advanced health and fitness tracking features. For example, STMicroelectronics reports that its MEMS pressure sensors fabricated using VENSENS monolithic technology are deployed in billions of smartphones, tablets, and wearable devices worldwide.

In industrial environments, pressure sensors play a critical role in predictive maintenance, real-time condition monitoring, and safety systems for pumps, compressors, and process equipment, aligning closely with Industry 4.0 initiatives. Their compact size, low power consumption, and improved temperature compensation make MEMS pressure sensors ideal for battery-powered devices and harsh operating conditions. As IoT adoption expands across factories, logistics networks, and smart infrastructure, demand for reliable and scalable pressure sensing solutions continues to strengthen.

Restraint - Intense Pricing Pressure and Commoditization Challenge Profitability in High-Volume MEMS Pressure Sensor Applications

As MEMS pressure sensors become standard components in high-volume applications such as smartphones, wearables, and entry-level automotive platforms, manufacturers increasingly face pricing pressure and margin erosion. A large number of global and regional suppliers now offer barometric and low-range pressure sensors with similar performance specifications, leading to intense competition and commoditization. This environment results in frequent price reductions, particularly in consumer electronics and lower-end industrial segments, where cost sensitivity is high.

To remain competitive, suppliers must continuously improve wafer yields, optimize packaging processes, and reduce testing and assembly costs. While these measures help protect margins, they can limit the ability of companies to invest in next-generation or niche high-performance sensor designs. As a result, long-term profitability increasingly depends on differentiation through higher integration levels, embedded software, application-specific customization, and system-level support rather than hardware performance alone.

Design Complexity and Reliability Requirements Limit Deployment in Harsh and Safety-Critical Operating Environments

MEMS pressure sensors used in demanding applications such as automotive powertrains, aerospace systems, oil and gas operations, and industrial process control must operate reliably under extreme temperatures, high vibration, and exposure to contaminants. Meeting these requirements creates significant technical and design challenges for sensor manufacturers. Ensuring long-term accuracy, minimal signal drift, and stable performance over extended lifecycles requires advanced packaging, calibration, and compensation techniques, all of which increase development time and cost.

In addition, sensors deployed in safety-critical applications must comply with strict certification standards, such as ASIL requirements for automotive systems and aerospace and industrial quality standards. Achieving compliance often involves extensive testing and validation, which can delay product launches and increase engineering complexity. These challenges raise entry barriers and limit the number of vendors capable of serving high-reliability market segments, constraining supply despite strong underlying demand.

Opportunity - Electrification and Software-Defined Vehicle Architectures Create New High-Value Use Cases for Pressure Sensors

The rapid shift toward battery electric vehicles, plug-in hybrids, and software-defined vehicle architectures is creating strong new growth opportunities for MEMS pressure sensors across multiple automotive subsystems. In electric vehicles, pressure sensors are increasingly used in battery packs, coolant loops, HVAC systems, and thermal management modules to support efficient heat control and safety monitoring. Advanced brake-by-wire and regenerative braking systems also rely heavily on precise pressure feedback to ensure consistent performance and safety.

Leading suppliers such as Bosch, Infineon, and Melexis are introducing embedded pressure sensor modules designed to support a wide range of automotive functions, from hybrid powertrain management to intelligent tire and chassis systems. As OEMs move toward connected, automated, and software-driven vehicle platforms, demand is rising for domain-oriented sensor solutions that combine hardware, software, and diagnostics. This trend allows sensor vendors to build deeper, long-term partnerships with automotive Tier-1 suppliers and OEMs.

AI-Enabled Edge Intelligence Transforms MEMS Pressure Sensors into Smart, Context-Aware Sensing Platforms

The growing integration of microcontrollers and advanced signal-processing capabilities directly into MEMS pressure sensors is enabling AI-enabled smart sensing at the edge. With on-sensor intelligence, pressure sensors can perform local data processing, event detection, and power optimization without relying heavily on cloud connectivity. Bosch Sensortec reports shipping more than a billion integrated MEMS sensors and is targeting ten billion intelligent sensors, highlighting the scale of this transformation.

Edge intelligence reduces system-level energy consumption, minimizes data transmission costs, and improves real-time responsiveness in IoT, industrial, and consumer applications. This shift allows sensor manufacturers to move beyond hardware sales and generate additional revenue through software, algorithms, firmware, and development tools. High-value applications such as wearables, smart buildings, robotics, and industrial automation increasingly prioritize contextual insights over raw data, creating strong differentiation opportunities for suppliers offering intelligent, application-ready pressure sensing solutions.

Category-wise Analysis

By Sensor Technology Insights

Piezoresistive MEMS pressure sensors represent the leading technology segment, accounting for an estimated 55% share of the global MEMS Pressure Sensors Market. Their dominance is driven by strong robustness, high linearity, and the ability to operate accurately across a wide pressure range. These characteristics make piezoresistive sensors particularly suitable for demanding applications such as automotive engine management, braking systems, industrial hydraulics, and high-pressure process control.

Unlike some alternative technologies, piezoresistive designs perform reliably in harsh environments involving temperature fluctuations, vibration, and mechanical stress. In addition, their compatibility with standard CMOS manufacturing processes allows for easy integration of signal conditioning, diagnostics, and safety features on the same chip. This integration supports cost-effective, high-volume production while meeting stringent safety and reliability requirements. As a result, piezoresistive MEMS sensors continue to outperform capacitive and optical technologies in most mainstream automotive and industrial use cases.

By Pressure Type Insights

Absolute pressure sensors hold the largest share within the pressure type segment, accounting for approximately 45% of global demand. Their dominance is driven by widespread use in barometric pressure measurement, altitude sensing, and manifold air pressure monitoring in vehicles. In consumer electronics, absolute pressure sensors enable accurate elevation tracking and indoor navigation in smartphones, smartwatches, and fitness wearables.

Major suppliers such as STMicroelectronics and Bosch ship these sensors in large volumes to global device manufacturers. In automotive and industrial applications, absolute pressure sensors are preferred in systems that require reference to a vacuum or standard atmospheric pressure, including engine air intake, environmental monitoring, and process control. Their versatility, accuracy, and reliability across different operating conditions reinforce their adoption over gauge, differential, and sealed gauge sensors, particularly in high-volume and multi-application environments.

By Sales Channel Insights

OEM contracts represent the leading sales channel in the MEMS Pressure Sensors Market, accounting for an estimated 50% of total shipments. Major sensor manufacturers secure long-term supply agreements with automotive OEMs, consumer electronics brands, and industrial equipment producers. Large integrated device manufacturers such as Bosch, STMicroelectronics, Infineon, and NXP Semiconductors work closely with Tier-1 suppliers to co-develop customized pressure sensor solutions optimized for system-level performance, integration, and cost efficiency.

This collaborative approach is especially important in automotive safety systems, smartphones, and industrial automation platforms, where reliability and long-term availability are critical. Multi-year OEM contracts provide volume stability and predictable revenue streams for suppliers. In contrast, distributors and online sales channels mainly serve smaller customers, prototyping needs, and aftermarket demand, playing a secondary but supportive role in the overall market structure.

By End-user Insights

The automotive sector is the largest end-use segment, accounting for approximately 40% of the global MEMS Pressure Sensors Market. This leadership is supported by high sensor content per vehicle and by strict regulatory requirements governing safety, emissions, and fuel efficiency. Modern vehicles incorporate numerous pressure sensors across TPMS, engine and exhaust systems, transmissions, braking systems, and HVAC modules. The shift toward electric and hybrid vehicles further increases sensor requirements due to the additional battery, thermal management, and power-electronics systems.

Regulatory mandates combined with the rising adoption of advanced driver assistance systems ensure continued growth in automotive pressure sensor demand. Compared with industrial, consumer, and healthcare segments, automotive applications generate higher value per unit due to stringent quality, safety, and reliability standards. As vehicle architectures become more complex and software-driven, pressure sensors will remain essential components, reinforcing the automotive industry’s dominant position in the market.

Regional Insights

North America MEMS Pressure Sensors Market Trends

North America remains a major demand center for the MEMS Pressure Sensors Market, supported by stringent safety regulations, strong automotive production, and advanced industrial infrastructure. The United States mandates TPMS in light vehicles and enforces strict emissions and safety standards, driving consistent demand for pressure sensors in powertrain, chassis, and safety systems. The region also benefits from a robust innovation ecosystem comprising semiconductor manufacturers, automotive Tier-1 suppliers, and industrial automation companies.

Growing investments in connected and autonomous vehicles, along with the modernization of manufacturing and energy infrastructure, further support demand for high-performance pressure sensing solutions. Companies such as Honeywell, Sensata Technologies, and Amphenol maintain strong regional footprints through local R&D, manufacturing, and OEM partnerships, reinforcing North America’s position as a technologically advanced and innovation-driven market.

Europe MEMS Pressure Sensors Market Trends

Europe is a strategically important market for MEMS pressure sensors, characterized by a strong automotive industry, strict regulatory frameworks, and a focus on safety and sustainability. Countries such as Germany, the U.K., France, and Spain host leading automotive OEMs and Tier-1 suppliers that rely heavily on pressure sensors for engine optimization, exhaust after-treatment, TPMS, and advanced chassis systems. EU-wide regulations on CO emissions, vehicle safety, and environmental monitoring create steady demand across automotive, industrial, and energy applications.

The region also benefits from a dense network of sensor manufacturers, including Infineon Technologies and STMicroelectronics, which operate major design and manufacturing facilities across Europe. Harmonized standards and cross-border R&D programs support the development of high-reliability pressure sensors for automotive, industrial, and healthcare markets. Europe’s push toward vehicle electrification, renewable energy, and smart infrastructure further underpins long-term market growth.

Asia Pacific MEMS Pressure Sensors Market Trends

Asia Pacific is the fastest-growing region in the MEMS pressure sensors market, driven by large-scale manufacturing and strong demand across automotive, consumer electronics, and industrial sectors. China serves as a global production hub for smartphones, wearables, vehicles, and factory automation equipment, generating significant demand for MEMS pressure sensors. Government support for new energy vehicles, smart manufacturing, and IoT infrastructure, combined with expanding local semiconductor capabilities, accelerates adoption.

Japan and South Korea contribute through high-end automotive and electronics exports, where pressure sensors are widely used in premium vehicles, cameras, smartphones, and industrial machinery. Rapid growth in automotive and electronics manufacturing in India and ASEAN countries adds new momentum, supported by cost-competitive production and rising domestic consumption. Global companies such as Bosch, NXP Semiconductors, and Goertek leverage Asia Pacific for high-volume manufacturing and regional R&D, making it the primary volume driver for the global supply chain.

Competitive Landscape

The MEMS Pressure Sensors Market is moderately concentrated, with a mix of large integrated device manufacturers and specialized sensor companies competing across automotive, consumer, industrial, and medical applications. Global leaders such as Bosch Sensortec, STMicroelectronics, Infineon Technologies, Honeywell International, Sensata Technologies, and NXP Semiconductors differentiate themselves through broad product portfolios, advanced MEMS fabrication capabilities, and strong co-development relationships with OEMs.

Key competitive strategies include expanding AI-enabled and smart sensor offerings, investing in automotive safety and industrial-grade solutions, and adopting platform-based designs that can be customized quickly for different applications. Selective acquisitions and partnerships are also used to enhance technology capabilities and market reach. Meanwhile, emerging players focus on niche applications, cost leadership, or innovative packaging and integration approaches. Overall, competition is shaped by scale, technology depth, system-level expertise, and the ability to support long-term OEM requirements.

Key Market Developments

- In September 2023: Infineon Technologies AG launched the XENSIV™ SP49 MEMS tire pressure monitoring sensor, designed for next-generation TPMS. The solution integrates auto-position detection, blowout monitoring, and wireless connectivity, supporting smarter, safer, and regulation-compliant tire systems for global automotive OEMs.

- In June 2025: Bosch introduced the SMP290 MEMS tire pressure sensor featuring integrated Bluetooth Low Energy, enabling long-life wireless TPMS and direct smartphone connectivity. This innovation enables advanced smart-tire applications across passenger-car, electric-vehicle, and commercial-vehicle platforms.

Companies Covered in MEMS Pressure Sensors Market

- First Sensor AG

- Bosch Sensortec GmbH

- Honeywell International Inc.

- Murata Manufacturing Co. Ltd.

- ROHM Co. Ltd.

- Amphenol Corporation

- InvenSense Inc.

- Sensata Technologies Inc.

- NXP Semiconductors N.V.

- Goertek Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Melexis N.V.

- TE Connectivity Ltd.

- Omron Corporation

Frequently Asked Questions

The global MEMS Pressure Sensors Market is projected to reach approximately US$ 12.5 Billion by 2033, up from around US$ 6.7 Billion in 2026, reflecting a forecast CAGR of about 9.3% during 2026 - 2033.

Key demand drivers include regulatory mandates for TPMS and vehicle safety, proliferation of smartphones and wearables using barometric sensors, and rapid deployment of MEMS pressure sensors in industrial IoT and Industry 4.0 applications for real‑time monitoring and predictive maintenance.

The automotive segment is the leading end‑use category, accounting for an estimated ~40% share of the market due to extensive use of pressure sensors in TPMS, engine management, braking systems, and emerging electrified vehicle platforms worldwide.

North America is a leading regional market, supported by stringent vehicle safety and emissions regulations, strong automotive and aerospace industries, and significant adoption of industrial automation and advanced sensing technologies, particularly in the U.S.

A major opportunity lies in developing AI‑enabled intelligent MEMS pressure sensors and specialized solutions for electric and software‑defined vehicles, which combine advanced diagnostics, embedded processing, and connectivity to deliver higher value and differentiation.

Prominent companies include First Sensor AG, Bosch Sensortec GmbH, Honeywell International Inc., Murata Manufacturing Co. Ltd., ROHM Co. Ltd., Amphenol Corporation, InvenSense Inc., Sensata Technologies Inc., NXP Semiconductors N.V., Goertek Inc., STMicroelectronics N.V., Infineon Technologies AG, Melexis N.V., TE Connectivity Ltd., and Omron Corporation.