- Smart Packaging

- Latin America Rigid Industrial Packaging Market

Latin America Rigid Industrial Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Latin America Rigid Industrial Packaging Market by Product Types (Drums, Industrial Bulk Containers, Others), Materials (Plastic/HDPE, Polypropylene (PP), Others), End-use Industry, and Regional Analysis for 2026 - 2033

Latin America Rigid Industrial Packaging Market Size and Trends Analysis

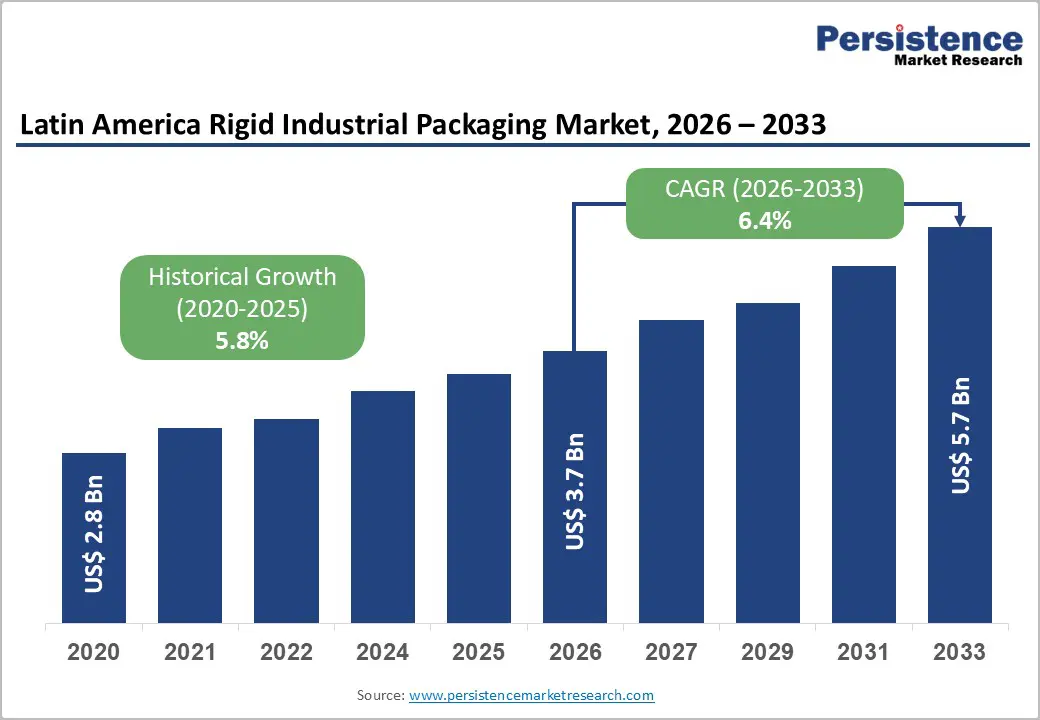

The Latin America rigid industrial packaging market size is likely to be valued at US$3.7 billion in 2026 and is expected to reach US$5.7 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033 is driven by rapid industrialization, expansion in sectors such as chemicals, automotive, food & beverage, and pharmaceuticals, and the rising emphasis on product safety and compliance with stringent transportation regulations.

Expanding trade within regional blocs such as MERCOSUR, along with rising foreign direct investment in manufacturing hubs, is boosting demand for durable and reusable packaging solutions. Sustainability initiatives are prompting companies to adopt recyclable, high-performance materials, while the pursuit of greater logistical efficiency continues to shape purchasing decisions. A key growth driver is the growing need for secure bulk-handling and storage solutions in mining and energy operations across Brazil, Mexico, and Chile.

Key Industry Highlights

- Leading Region: Brazil is projected to account for 35.2% of the market share, driven by its dominant agriculture, chemical, and pharmaceutical sectors.

- Fastest-Growing Region: Mexico is experiencing rapid growth due to nearshoring trends, infrastructure projects, and industrial expansion.

- Investment Plans: Major players, such as ALPLA Group and ORBIS Corporation, have expanded or established new facilities in Toluca and Monterrey, Mexico, to meet the increasing demand for drums, IBCs, and bulk containers.

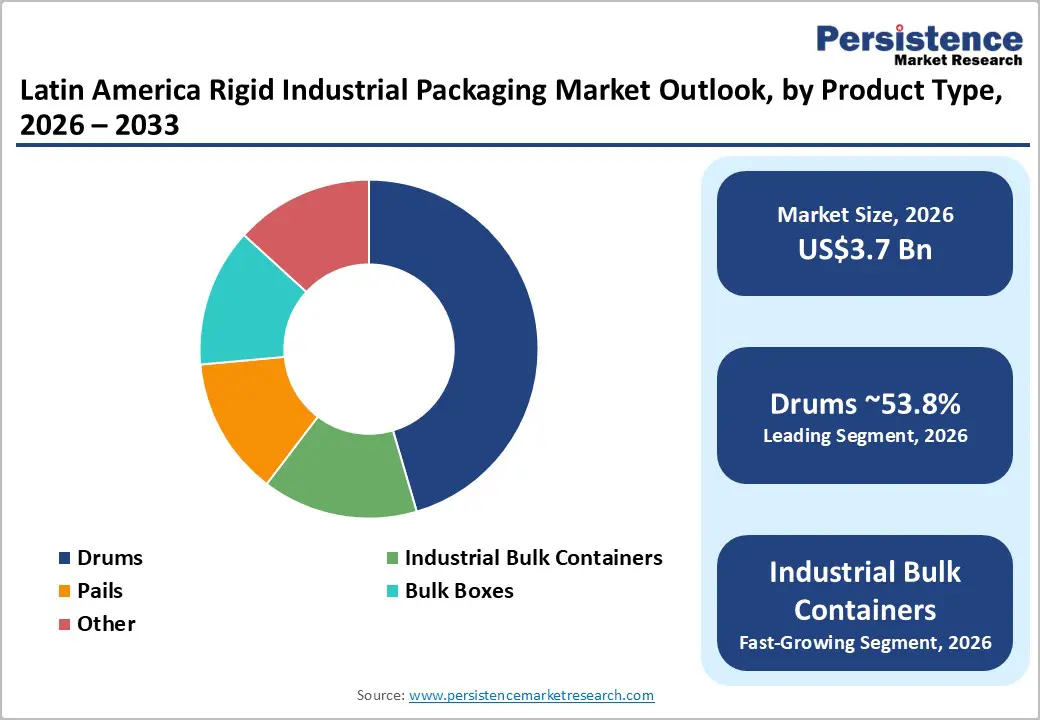

- Dominant Product Type: Drums are anticipated to hold 53.8% market share, widely used across chemical, agricultural, and pharmaceutical industries for durable bulk transport.

- Leading End-use Industry: Agriculture is estimated to hold 41.1% market share, driven by Brazil’s large-scale agricultural exports and demand for secure packaging of fertilizers, pesticides, and seeds.

| Key Insights | Details |

|---|---|

| Latin America Rigid Industrial Packaging Market Size (2026E) | US$3.7 Bn |

| Market Value Forecast (2033F) | US$5.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Escalating Demand for Bulk Chemical & Hazardous Material Transport Compliance

The Latin American rigid industrial packaging market is increasingly propelled by the requirement for regulatory-compliant hazardous material containment and bulk chemical transportation solutions, especially in the chemicals, petrochemicals, and agrochemical sectors. Durable formats such as drums, IBCs, and industrial crates are prioritized to meet strict cross-border hazardous goods packaging standards and ensure leak-proof, impact-resistant logistics across export corridors in Brazil and Mexico.

This demand is further strengthened by expanding chemical processing capacities and the need to safeguard high-value industrial consignments during long-haul transit. Enhanced safety compliance requirements from regional trade partners, particularly under agreements such as USMCA, heighten the adoption of certified industrial packaging systems.

Adoption of Recyclable & High-Performance HDPE and Composite Rigid Packaging

Sustainability initiatives and circular economy-aligned rigid industrial packaging solutions are steering market growth as manufacturers in Latin America opt for recyclable HDPE, reinforced polymer drums, and composite containers that combine strength with environmental responsibility. Industrial buyers increasingly prefer reusable bulk containers with low lifecycle cost to reduce total ownership while aligning with corporate ESG targets and government waste-reduction mandates.

This shift is particularly visible in sectors such as agrochemicals and food processing, where material integrity and recyclability directly influence supply chain efficiency. As an example, high-density polyethylene (HDPE) containers are gaining traction for their moisture and chemical resistance and ease of recycling in industrial logistics applications across regional hubs. A major petrochemical producer in São Paulo switched to reusable HDPE IBCs with RFID tracking for bulk solvent shipments to international customers, cutting material waste and improving inventory traceability throughout the supply chain.

Inefficiencies from Rigid Container Shape Constraints and Logistics Imbalance

The Latin American rigid industrial packaging market faces structural restraints due to the fixed form-factor inefficiencies of rigid containers in multi-modal logistics networks, where non-adjustable shapes and sizes lead to underutilized cargo space and elevated bulk storage and freight handling inefficiencies. Particularly for irregular or volumetrically light products, the rigidity of drums, IBCs, and pails results in higher per-unit transportation costs and a larger storage footprint than adaptable alternatives, limiting adoption in tightly optimized supply chains.

This inefficiency becomes pronounced in intra-regional trade corridors with varying transport modalities (road, rail, ports), where container load factors directly affect shipment economics. Moreover, these design constraints can force over-packaging or require secondary cushioning materials to protect sensitive industrial goods, further driving up ancillary logistics costs.

Volatile Polymer Resin Input Prices and Import Dependency Pressure

A significant restraint for the Latin American rigid industrial packaging market is the volatility of polymer resin pricing and dependence on imported resin supply chains, which creates unpredictable cost structures for manufacturers of HDPE, PP, and composite industrial containers.

Fluctuating raw material costs, driven by global crude oil movements and foreign exchange volatility, lead to inconsistent production margins and compel manufacturers to either absorb price swings or pass them on to industrial buyers, dampening demand in price-sensitive sectors such as chemicals and agriculture. In Mexico, Brazil, and emerging Latin American economies, reliance on external resin suppliers also exposes local rigid packaging players to supply lead-time disruptions and inventory shortages during global logistic stress periods, making long-term procurement planning challenging and restraining stable market growth.

Opportunity Analysis - Expansion of Circular Economy and Refurbishment Service Models

The Latin American rigid industrial packaging market has a growing opportunity in circular economy-aligned reuse and refurbishment service models for IBCs, steel drums, and bulk containers, as industrial buyers seek to lower lifecycle costs and minimize waste.

Companies can invest in returnable rigid container cleaning and redistribution networks to support closed-loop systems, generating recurring revenue while meeting sustainability commitments. This shift toward refurbishable industrial packaging solutions with lifecycle services appeals to export-oriented chemical, pharmaceutical, and food producers aiming for long-term supply chain resilience. Partnering with logistics and recycling specialists can accelerate adoption and strengthen regional infrastructure for reuse.

Smart & IoT-Enabled Rigid Packaging for Supply Chain Transparency

There is a rising demand for IoT-enabled rigid industrial packaging solutions with embedded sensors and real-time tracking systems that enhance visibility across multi-modal logistics in Latin America. Integrating RFID/GPS-connected IBCs and drums with temperature and tamper monitoring helps industrial customers in chemicals, agrochemicals, and pharmaceuticals meet stringent traceability expectations and reduce loss/damage risk during long-distance transport.

This trend toward digitally enhanced industrial packaging products positions suppliers to offer premium, value-added services and differentiate in a competitive landscape. Early adopters of smart packaging tech can secure partnerships with large exporters requiring end-to-end asset visibility. A regional packaging company piloted RFID-integrated drums with real-time location and condition monitoring for a Brazilian chemical exporter, significantly decreasing product loss claims and improving customer satisfaction within six months.

Category-wise Analysis

Product Type Insights

The drums segment dominates the Latin America rigid industrial packaging market, accounting for a 53.8% market share, anchored by its central role in bulk containment and transport of industrial liquids and semi-solids. Drums, whether plastic (HDPE) or metal, are widely used for chemicals, solvents, oils, and agrochemicals due to their high durability, leak resistance, reusability, and stackability, which are critical in long-haul logistics and storage operations. Their robust construction provides excellent chemical resistance and mechanical strength, making them ideal for hazardous and non-hazardous materials alike in sectors such as agriculture, chemicals, and energy.

As they safely meet industrial safety standards and are compatible with standardized pallet systems and forklifts, drums reduce operational handling complexity for supply chain partners. For example, chemical distributors in Brazil increasingly rely on UN-certified HDPE drums to ship bulk fertilizers and industrial solvents across regional markets, ensuring compliance and minimizing product loss during transport.

Industrial bulk containers (IBCs) are the fastest-growing product type in rigid industrial packaging, driven by surging demand from the chemical and pharmaceutical sectors for large-volume, secure, and compliant containment systems. Unlike traditional drums, IBCs offer higher volumetric efficiency and can handle volumes typically between 500 and 1,000, making them especially attractive for businesses transporting bulk liquids and materials with minimal handling cycles.

The design facilitates easy integration into automated and semi-automated filling/emptying processes, lowering labor costs and improving throughput for manufacturers and logistics providers. The trend toward IoT and sensor-enabled tracking in IBCs is appealing to pharmaceutical and specialty chemical producers seeking end-to-end supply chain visibility. This combination of operational efficiency, scalability, and technology integration is accelerating IBC adoption faster than other rigid formats.

End-use Industry Insights

The agriculture sector is expected to be the largest end-use industry for rigid industrial packaging in Latin America, capturing 41.1% of market share. The region’s strong agricultural base, anchored by Brazil, Argentina, and Mexico, necessitates reliable containment for fertilizers, pesticides, seeds, and other bulk agricultural inputs.

Rigid containers such as drums, pails, and bulk boxes provide secure protection against contamination, moisture, and spillage, preserving product quality throughout storage and transport. The heavy reliance on bulk fertilizers and agrochemicals, coupled with expanding commodity export volumes, drives demand for packaging that supports large-scale logistics and efficient handling. For instance, Brazilian agrochemical producers use UV-stabilized HDPE drums and IBCs to transport liquid fertilizers across domestic and international markets, maintaining operational continuity through climatic variations typical of Latin America.

The automotive sector is emerging as the fastest-growing end-use industry for rigid industrial packaging amid a resurgence in manufacturing and assembly investments across Mexico and Brazil. Growth in automotive production increases the need for durable packaging solutions for fluids (lubricants, coolants), coatings, adhesives, and parts that require robust protection through complex multi-tier supply chains.

Rigid containers such as pails, drums, and IBCs are increasingly adopted to safeguard high-value automotive components and consumables against contamination and mechanical damage during transit and storage. Automotive manufacturers are emphasizing just-in-time delivery and reduced supply chain friction, making standardized, reusable rigid packaging formats preferred to minimize downtime and handling costs. For example, parts suppliers in Mexico’s automotive corridor are shifting toward customized rigid pails and IBCs to streamline inbound logistics to assembly plants, reflecting accelerated uptake in this segment compared to traditional industrial buyers. While specific Latin American automotive packaging figures are emerging, this trend aligns with broader global industrial packaging growth patterns.

Country Insights

Brazil

Brazil is projected to lead the market, accounting for approximately 35.2% of the market share in 2026, largely driven by its expansive agriculture and food export sectors that rely on durable packaging for bulk transport and logistics. The country’s extensive industrial base, covering chemicals, petrochemicals, and pharmaceutical manufacturing, further fuels demand for high-performance drums, IBCs, and pallets that ensure product safety and compliance during domestic distribution and export shipment. Key industrial hubs such as São Paulo and Rio de Janeiro act as major consumption centers where packaging manufacturers and distributors operate extensive supply networks. Brazil’s pharmaceutical sector, for example, has been ramping up exports of medicinal products and intermediates, increasing the need for rugged IBCs and UN-certified containers for safe handling.

Several companies have shaped Brazil’s rigid packaging landscape. Greif Inc., a global industrial packaging supplier, has introduced high-performance drums and containers for agrochemical and chemical distributors seeking enhanced durability and lighter-weight formats. Local and multinational players, including ALPLA Group and Unipac Embalagens Ltda., maintain strong manufacturing footprints in the country, producing HDPE drums and bulk containers for agricultural inputs and export goods. These developments reinforce Brazil’s dominant position while encouraging the adoption of sustainable and reusable packaging solutions, as exporters optimize logistics efficiency and reduce environmental impact.

Mexico

Mexico is likely to be the fastest-growing market, propelled by infrastructure development, nearshoring trends, and rising industrial demand from manufacturing clusters. Expanding sectors such as automotive, food processing, and chemicals require reliable packaging solutions for both domestic supply chains and export logistics. Mexico’s proximity to North America enhances integration with global value chains, boosting demand for intermediate bulk containers (IBCs), rigid crates, and industrial drums that meet export standards and improve supply chain visibility. Recent developments illustrate this momentum. ORBIS Corporation expanded its operations with a new manufacturing facility in Monterrey, addressing growing demand for pallets and bulk containers in the construction and chemical industries. Similarly, ALPLA Group invested in a large-volume industrial container and IBC production facility in Toluca, strengthening regional manufacturing capacity and accelerating market growth by providing standardized packaging solutions to key industrial sectors. These strategic expansions not only fuel Mexico’s market growth but also improve regional supply chain resilience by reducing lead times and enhancing product availability.

Competitive Landscape

The Latin America rigid industrial packaging market is moderately consolidated, with a mix of global industrial packaging leaders and regional manufacturers competing for market share across Brazil, Mexico, and other Latin American countries. Key global players such as Greif Inc., ALPLA Group, ORBIS Corporation, Mauser Group, and Berry Global dominate through extensive distribution networks, advanced manufacturing capabilities, and a wide portfolio of drums, IBCs, pails, and bulk containers. These companies focus on high-performance, sustainable, and reusable packaging solutions to meet the evolving needs of agriculture, chemicals, pharmaceuticals, and automotive sectors. Regional players such as Unipac Embalagens Ltda., Resilux Brasil, and Plastipak Packaging maintain strong local footprints, offering customized HDPE and polypropylene solutions tailored to domestic industrial requirements.

Recent strategic developments include capacity expansions, technology-driven upgrades such as IoT-enabled containers for supply chain traceability, and acquisitions aimed at strengthening regional presence. For instance, ALPLA Group invested in a large-volume industrial container and IBC production facility in Toluca, Mexico, while ORBIS Corporation opened a new manufacturing plant in Monterrey to meet growing demand for bulk containers. Across the market, competitive strategies revolve around enhancing operational efficiency, adopting circular-economy-aligned packaging, and providing value-added services to differentiate in a price-sensitive yet quality-driven environment, positioning these companies to capitalize on the region’s rising demand for industrial and export-oriented packaging.

Key Industry Developments

- In January 2025, Mauser Group expanded its reconditioning and refurbishment services for industrial drums and IBCs in Brazil, supporting circular economy initiatives and increasing the adoption of reusable rigid packaging among export-oriented chemical producers.

Companies Covered in Latin America Rigid Industrial Packaging Market

- Greif Inc.

- ALPLA Group

- ORBIS Corporation

- Mauser Group

- Berry Global Inc.

- Schütz GmbH & Co. KGaA

- DS Smith Plc

- Time Technoplast Ltd.

- Schoeller Allibert Group

- Brambles Limited

- Plastipak Packaging Inc.

- Rehrig Pacific Company

- Unipac Embalagens Ltda.

- RPC Group (Berry Global)

- Industrial Container Services (ICS)

- Hoover Container Solutions

- Myers Industries Inc.

- Bulk Handling Australia Group

Frequently Asked Questions

The market size is projected to be approximately US$3.7 billion in 2026.

The Latin America rigid industrial packaging market is expected to reach around US$5.7 billion by 2033.

Key trends include the adoption of reusable and recyclable HDPE drums and IBCs, IoT-enabled containers for supply chain traceability, circular economy-based refurbishment services, and growth in automotive and chemical sector packaging demand.

Drums are the leading segment, accounting for 53.8% market share.

The Latin America rigid industrial packaging market is expected to grow at a CAGR of approximately 7.1% between 2026 and 2033.

Major companies include Greif Inc., ALPLA Group, ORBIS Corporation, Unipac Embalagens Ltda., and Mauser Group.