- Food Ingredients & Additives

- Gum Arabic Market

Gum Arabic Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Gum Arabic Market by Product Type (Acacia Senegal, Acacia Seyal), by Nature (Organic, Conventional), by End Use (Food & Beverages, Pharmaceuticals & Nutraceuticals, Personal Care & Cosmetics, Animal Nutrition, Paints & Inks, Others), by Regional Analysis, 2026-2033

Gum Arabic Market Size and Share Analysis

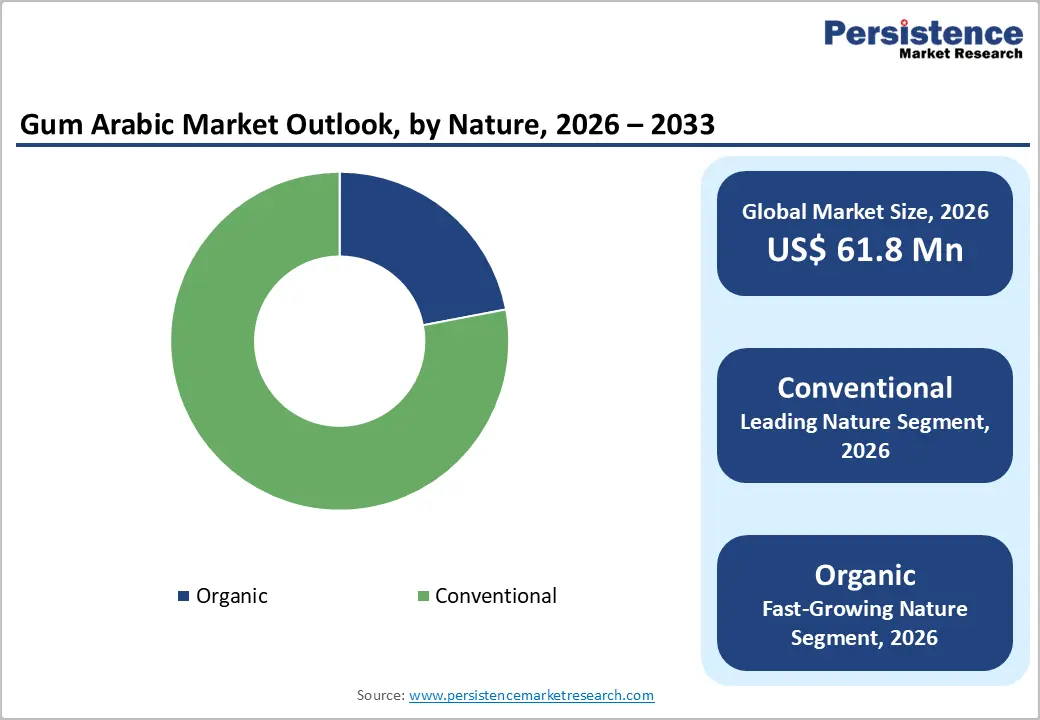

The global Gum Arabic Market size is expected to be valued at US$ 61.8 million in 2026 and projected to reach US$ 94.8 million by 2033, growing at a CAGR of 6.3% between 2026 and 2033

The market is experiencing a steady upward trajectory primarily due to the global shift towards natural, plant-based stabilizers and the increasing inclusion of gum arabic as a soluble fiber in health-focused food products. As the food industry moves away from synthetic additives, the demand for "clean label" emulsifiers has surged, making this natural resin indispensable for beverage stability and confectionery glazes. Furthermore, the rising adoption of Gum Arabic in pharmaceutical coatings and high-end cosmetics as a film-forming agent provides a robust foundation for long-term growth.

Key Industry Highlights

- Leading Region: North America leads the global Gum Arabic market with a 46% share, supported by early adoption of alternative wine formats, regulatory flexibility, and a strong outdoor and convenience-driven consumption culture.

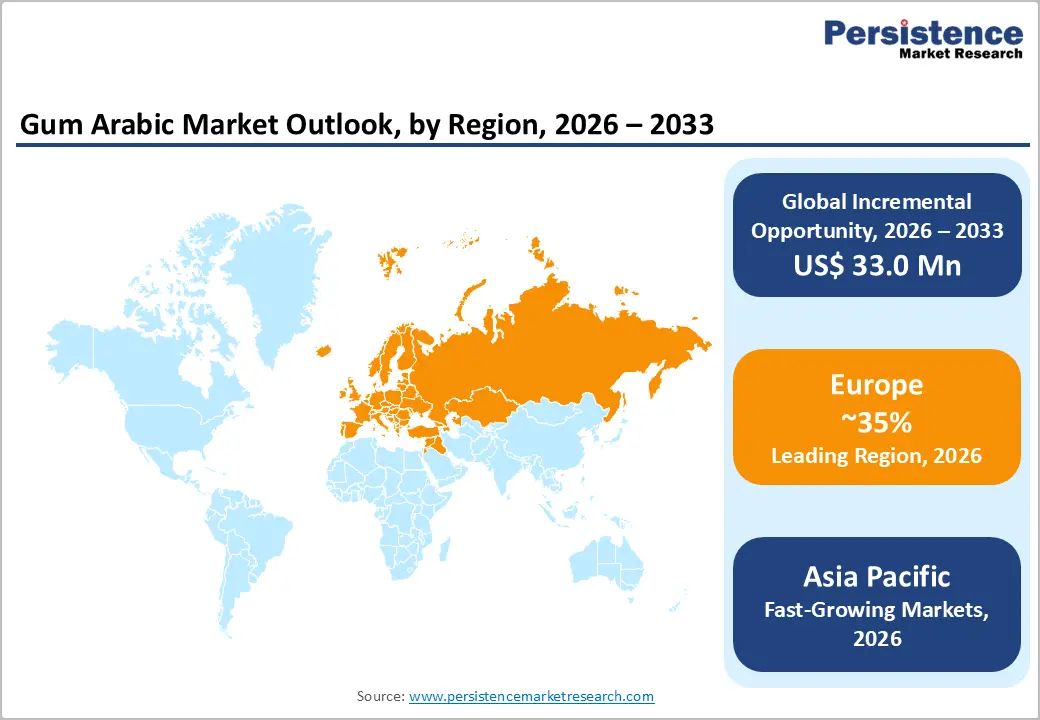

- Leading Region: Europe dominates the market with a 35% share in 2025, supported by advanced processing technology and the headquarters of global leaders like Nexira.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, driven by the rapid expansion of the food, beverage, and pharmaceutical sectors in China and India.

- Dominant Segment: The Conventional nature segment held a 78% market share in 2025, reflecting its widespread use in large-scale industrial and standard food applications.

- Fastest Growing Segment: The Organic segment is experiencing the highest growth rate as health-conscious consumers in developed markets demand certified natural and clean-label products.

- Key Market Opportunity: The integration of gum arabic as a Prebiotic dietary fiber in the functional food sector offers significant revenue potential due to rising awareness of gut health.

- Key Development: In September 2024, the European Union supported the continuation of gum Arabic production in Sudan through a funded initiative aimed at strengthening output capacity and improving value-chain sustainability.

| Key Insights | Details |

|---|---|

|

Global Gum Arabic Market Size (2026E) |

US$ 61.8 Mn |

|

Market Value Forecast (2033F) |

US$ 94.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Dynamics

Driver – Growing Demand for Clean Label Ingredients and Natural Stabilizers

The fundamental driver propelling the Gum Arabic Market is the aggressive global consumer preference for Clean label ingredients. Consumers are increasingly scrutinizing labels for artificial emulsifiers like Brominated Vegetable Oil (BVO) or synthetic thickeners, prompting major food giants like PepsiCo and The Coca-Cola Company to utilize Gum Arabic as a primary natural alternative. According to the U.S. Food and Drug Administration (FDA), gum arabic is recognized as a safe, natural dietary fiber, which allows manufacturers to make health claims on packaging. This regulatory support, combined with the ingredient's unmatched ability to stabilize oil-in-water emulsions in citrus-based beverages, ensures a consistent demand. As manufacturers re-formulate thousands of products to meet "natural" certifications, the market experiences a direct volume surge across the Sahel region's supply chains.

Restraints – Geopolitical Instability in Key Producing Regions and Supply Chain Volatility

The Gum Arabic Market faces significant barriers due to its high geographic concentration in the "Gum Belt" of Sub-Saharan Africa, particularly in Sudan, Chad, and Nigeria. Sudan historically accounts for a vast majority of the global production of Acacia Senegal; however, ongoing civil unrest and internal conflicts have severely disrupted harvesting and logistics. Organizations like the United Nations Conference on Trade and Development (UNCTAD) have noted that such instability leads to sharp price fluctuations and inconsistent supply quality. When trade routes are blocked or ports are inaccessible, global buyers face shortages, forcing some industrial users to consider lower-quality synthetic hydrocolloids or alternative gums like Guar or Xanthan, which can dampen the premium growth of the natural market.

Opportunity – Strategic Integration into the Flourishing Plant-Based and Vegan Food Movement

A significant opportunity for market participants lies in the rapid expansion of the vegan and dairy-alternative sectors. As the global vegan population grows, there is an urgent need for plant-based stabilizers that can mimic the creaminess of dairy in nut milks and plant-based yogurts. Gum Arabic is uniquely positioned to fill this gap due to its neutral flavor profile and excellent mouthfeel enhancement. Companies like Kerry Group plc. are already experimenting with gum-based solutions to stabilize high-protein plant beverages, which often suffer from sedimentation. By marketing gum arabic as a non-GMO, sustainable, and vegan-friendly hydrocolloid, producers can capture high-value contracts with emerging food-tech startups in Europe and North America that are focused on replicating traditional dairy textures without animal products.

Category-wise Analysis

By Product Type, Acacia Senegal dominates the global market

The Acacia Senegal segment is the leading segment within the Product Type category, currently dominating the market with superior functionality. Known in the industry as "Hard Gum," it is the gold standard for high-end applications due to its excellent emulsifying properties and high solubility. It is the primary choice for the beverage industry, specifically for carbonated drinks and syrup concentrates. In 2025, the Conventional nature of this product held a significant share, but the transition toward Organic variants is accelerating. The Acacia Seyal segment, while less expensive, serves a vital role in the confectionery and industrial sectors where lower viscosity is required. While Acacia Senegal remains the quality leader, Acacia Seyal is often used in blends to manage production costs in high-volume processed foods.

By Nature, organic gum arabic is expected to show promising growth in the global market

The Conventional nature segment is currently the dominant segment, holding a 78% market share in 2025. This dominance is driven by its widespread availability and lower price point, which makes it accessible for large-scale industrial use in paints, inks, and basic food processing. Most of the traditional production in the Sudan and Sahel regions is categorized as conventional. However, the Organic segment is identified as the fastest-growing segment. The surge in demand for Organic gum arabic is direct evidence of the "clean label" trend in developed markets. Food manufacturers in Europe and the USA are willing to pay a premium for certified organic gums to meet the strict labeling requirements of health-conscious consumers. This shift is encouraging producers in Chad and Senegal to seek international organic certifications to tap into these high-margin revenue pockets.

Region-wise Insights

North America Gum Arabic Market Trends and Insights

North America remains a critical hub for the Gum Arabic Market, driven by the region's massive food processing industry and the stringent regulatory environment of the United States. The U.S. FDA's decision to include gum arabic in the definition of dietary fiber has been a monumental catalyst, allowing manufacturers to market the ingredient as a health-positive additive. This has led to a surge in innovation within the functional beverage and snack bar segments.

In the U.S., the "clean beauty" movement is also driving demand in the Personal Care & Cosmetics sector, where gum arabic is used as a natural film-former in masks and lotions. The innovation ecosystem in North America focuses heavily on finding synergistic blends of gum arabic with other natural stabilizers to reduce costs while maintaining the "natural" label. Major players like AEP Colloids and TIC Gums (a Kerry company) are leading the charge in providing tailored gum solutions for local manufacturers who are increasingly avoiding synthetic ingredients.

Europe Gum Arabic Market Trends and Insights

Europe is the leading region in the global Gum Arabic Market, accounting for a 35% market share in 2025. The region's leadership is underpinned by the presence of world-class processing facilities and the headquarters of major players like Nexira and Alland & Robert in France. European manufacturers are the primary exporters of refined, high-quality gum arabic to the rest of the world. The European Food Safety Authority (EFSA) has long supported the use of gum arabic (coded as E414), and the region has some of the highest standards for Organic and sustainable sourcing.

In countries like Germany, the U.K., and France, the demand is heavily skewed toward Organic and high-grade Acacia Senegal for the premium confectionery and pharmaceutical industries. Performance analysis shows that European consumers are the most willing to pay a premium for ethically sourced products, leading to the rapid adoption of sustainability certifications. Regulatory harmonization within the EU ensures that gum arabic remains a staple ingredient across the continent's diverse food landscape, from traditional bakeries to modern molecular gastronomy.

Asia Pacific Gum Arabic Market Trends and Insights

Asia Pacific is recognized as the fastest-growing region for the Gum Arabic Market during the forecast period. This rapid growth is fueled by the massive expansion of the food and beverage sectors in China, India, and the ASEAN countries. As the middle class in these nations grows, there is a burgeoning demand for processed convenience foods and branded beverages, both of which rely heavily on stabilizers like gum arabic. China and Japan are also seeing a significant uptick in the use of gum arabic within the cosmetics industry, driven by the popularity of "natural" and "herbal" skincare products.

India presents a unique market dynamic with its large manufacturing advantages and growing pharmaceutical sector. The country is a major consumer of gum arabic for tablet coatings and traditional ayurvedic formulations. Regional growth is also supported by the increasing number of local processing plants that aim to reduce the dependency on European re-exporters.

Market Competitive Landscape

The global Gum Arabic Market is characterized by a concentrated structure at the processing level and a highly fragmented supply chain at the harvesting level. A few key players, such as Nexira, Alland & Robert, and Kerry Group plc., dominate the global refining and distribution networks. these companies maintain their leadership through extensive R&D investments, focusing on developing specialized grades of gum with specific viscosities or fiber contents. Key differentiators for these leaders include their ability to provide consistent quality, long-term supply contracts despite geopolitical risks, and robust sustainability certifications.

Emerging business model trends involve direct partnerships with local cooperatives in the Gum Belt to ensure a more traceable and ethical supply chain. Many market leaders are shifting away from being simple commodity traders to becoming "solution providers," offering custom hydrocolloid blends that include gum arabic along with pectin or guar gum. The market is also seeing the entry of local African processing companies that aim to add value within the continent rather than exporting raw tears, a trend supported by organizations like the African Development Bank.

Key Developments:

- In September 2024, the European Union supported the continuation of gum Arabic production in Sudan through a funded initiative aimed at strengthening output capacity and improving value-chain sustainability. The project was implemented by Agence Française de Développement (AFD) in collaboration with Sudan’s Forest National Corporation, reinforcing supply security and sustainable sourcing of gum Arabic for global food and beverage applications.

Companies Covered in Gum Arabic Market

- Agrigum International Limited

- Kerry Group plc.

- Alland & Robert

- Morouj Commodities UK Ltd

- Nexira

- Polygal AG

- AEP Colloids

- Kapadia Gum Industries Pvt. Ltd.

- CARAGUM International S.A

- C.E. Roeper

- Others

Frequently Asked Questions

The global Gum Arabic market is projected to be valued at US$ 61.8 Mn in 2026.

The demand is primarily driven by the "clean label" movement in the Food & Beverages industry and the ingredient's rising popularity as a Prebiotic dietary fiber in the health and wellness sector.

The Global Gum Arabic market is poised to witness a CAGR of 6.3% between 2025 and 2032

A major opportunity lies in expanding into the Organic segment and developing specialized formulations for the high-growth plant-based dairy and vegan food industries.

Key players include global leaders such as Nexira, Alland & Robert, Kerry Group plc., and Agrigum International Limited, who dominate the processing and distribution landscape.