- Food Ingredients & Additives

- Locust Bean Gum Market

Locust Bean Gum Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Locust Bean Gum Market by Form (Powder, Particles, Gel, Flat Sheet), Application (Food and & Beverages, Pharmaceutical, Cosmetics and & Personal Care), End-User (Food Processing, Cosmetics Manufacturing, Pharmaceutical Manufacturing), and Regional Analysis for 2025-2032

Locust Bean Gum Market Share and Trends Analysis

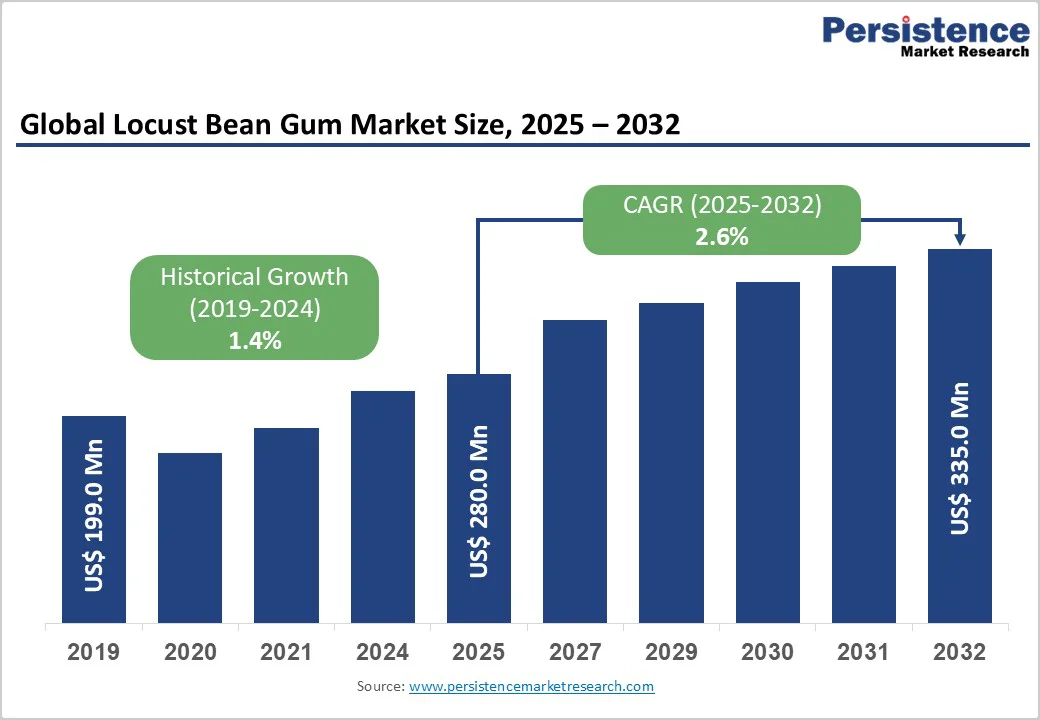

The global locust bean gum market size is likely to be valued at US$ 280.0 Mmillion in 2025, and is estimated to reach US$ 335.0 Mmillion by 2032, growing at a CAGR of 2.6% during the forecast period 2025−2032. Rising health consciousness, expanding applications in food, pharmaceuticals, and personal care, and industrial demand for natural hydrocolloids underpin market growth. Steady volume gains result from the product’s high thickening efficacy, consumer preference for clean-label stabilizers, and broader regulatory acceptance. Continuous innovation in plant-based formulations, alongside cost and supply chain optimization, further accelerates the transition from synthetic to natural gums.

Key Industry Highlights

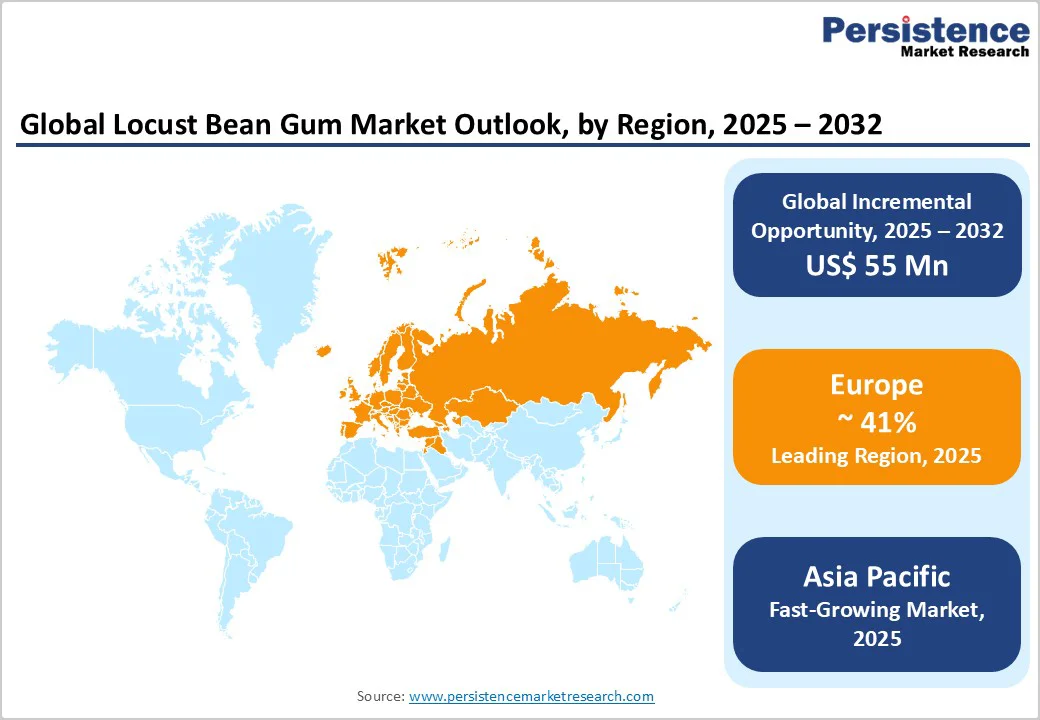

- Dominant Region: Europe’s leadsing position in the locust bean gum the market with about 41% of global share in 2025, powered by a countries like Germany, the U.K., Spain and France have established a robust demand base for locust bean gum across Germany, U.K., and France.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing segment regional market through 2032 due to the powerful convergence of rising domestic demand, supportive regulatory reforms, and significant advancements in extraction and processing technologies.

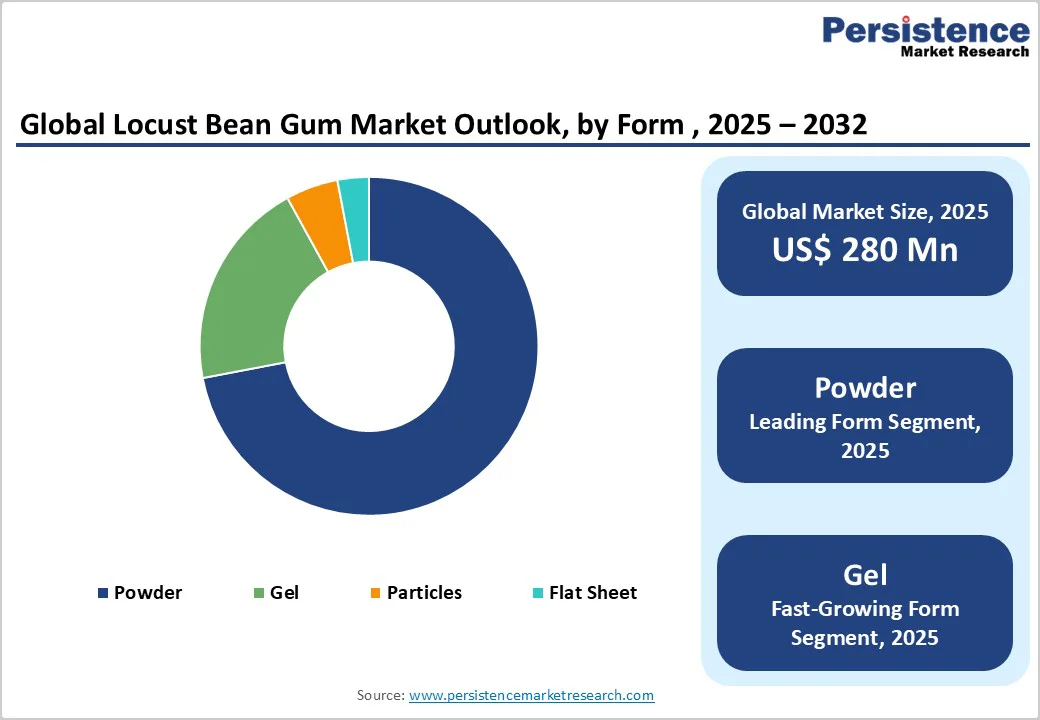

- Leading & Fastest-growing Form: Powder form is the leading segment with a 72% marketrevenue share in 2025, while. Powdered form is produced through advanced milling and drying techniques. Ggel form is poised to be the fastest- growing, aided by segment due to theirits increasing integration in specialized pharmaceutical, cosmetic, and industrial products.

- Leading & Fastest-growing Application: Food and & Bbeverages is the leading segmentdominates with 60% market share in 2025, fueled by .anPrimary drivers include increased consumption of dairy analogues, confectionery, and gluten-free bakery items. Pwhereas pharmaceutical is set to grow the fastest growing segment. Because of it sowing to the biocompatibility, non-toxicity, and functionality of locust bean gum as a versatile excipient.

| Report Attribute | Details |

|---|---|

|

Locust Bean Gum Market Size (2025E) |

US$ 280.0 Mn |

|

Market Value Forecast (2032F) |

US$ 335.0 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

2.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

1.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Natural Food Ingredients

The locust bean gum market is experiencing robust growth driven by a significant industry-wide shift toward natural and non-allergenic thickening agents. Across key food categories, including dairy products, bakery items, ice cream, and convenience foods, manufacturers are actively seeking cleaner ingredient alternatives that deliver the same functional performance without compromising product quality. Locust bean gum has emerged as the preferred choice in this transition, capitalizing on its proven gelling, stabilizing, and viscosity-enhancing properties to meet consumer demands for transparency and safety while maintaining the sensory characteristics that consumers expect.

This market expansion is further accelerated by the dual pressures of regulatory compliance and consumer expectations surrounding ingredient disclosure. Food producers face mounting scrutiny over ingredient transparency, prompting them to replace synthetic additives with plant-based alternatives that align with both regulatory requirements and evolving consumer preferences. By offering a clean-label solution that maintains product performance and shelf appeal, locust bean gum has solidified its position as a strategic formulation tool for modern food brands, wherein it is able to simultaneously address ingredient safety concerns, regulatory demands, and the competitive advantage of transparent labeling in today's consumer-conscious marketplace.

The driving force behind growth in the locust bean gum market is the pronounced consumer shift toward natural and non-allergenic thickeners in the food industry, especially within product categories such as dairy, bakery, ice cream, and convenience foods. Locust bean gum, renowned for its gelling, stabilizing, and viscosity-enhancing properties, has directly benefited from this movement, as manufacturers seek alternatives that meet cleaner ingredient profiles without compromising product quality.

furthermore amplifying locust bean gum’s market expansion as food producers seek alternatives to synthetic additives and address heightened regulatory and consumer scrutiny over ingredient transparency. This dynamic positions locust bean gum as a preferred solution for food brands looking to meet modern formulation and labeling demands while maintaining product quality and shelf appeal.

Supply Chain and Regulatory Constraints

The market for locust bean gum faces significant supply chain vulnerabilities stemming from geographic concentration in production. The vast majority of global locust bean gum supply originates from a limited number of Mediterranean producers, particularly Spain and Morocco, creating a bottleneck that exposes the entire market to production disruptions. Weather events, agricultural policy shifts, and harvest fluctuations in these key regions directly translate into supply volatility for global buyers, while changes in export tariffs or quota systems can trigger abrupt and widespread availability constraints. This geographic dependency underscores a critical risk factor for manufacturers dependent on steady locust bean gum sourcing.

Compounding supply chain challenges are stringent regulatory requirements that increase operational complexity and costs. Regulatory agencies worldwide mandate comprehensive documentation, rigorous testing protocols, and certification procedures to verify that locust bean gum meets established purity and safety standards before market entry. These compliance obligations require manufacturers and exporters to invest substantially in quality assurance infrastructure, implement robust testing regimens, and maintain continuous vigilance over evolving legislative standards across different jurisdictions. The combination of geographic supply constraints and escalating regulatory demands creates a complex operating environment where locust bean gum producers and distributors must simultaneously manage physical supply risks.

Supply chain and regulatory constraints in the locust bean gum market arise from several interconnected challenges across key producing and consuming regions. Chiefly, most of the world’s locust bean gum supply is sourced from Mediterranean countries such as Spain and Morocco, which makes the market highly susceptible to production fluctuations, weather-related risks, and changes in agricultural policies. When local harvests fall short or when governmental bodies change export tariffs or quota systems, global buyers can experience abrupt disruptions in supply availability.

Regulatory agencies require rigorous documentation and testing to ensure that locust bean gum batches meet purity and safety thresholds before they can be incorporated into consumer products. These requirements introduce additional operational and compliance costs for manufacturers and exporters, as they must maintain robust quality assurance protocols and adapt rapidly to evolving legislative standards.

Innovation in Extraction and Processing Technologies

Driven by the adoption of advanced bioprocessing methodologies, the locust bean gum market is undergoing a technological transformation. Traditional extraction processes, which rely on mechanical milling followed by water or acid extraction and multi-stage purification, delivered functional results but at significant operational and quality costs. These conventional approaches generated elevated impurity levels, required labor-intensive processing steps, and consumed substantial resources. Modern bioprocessing innovations, particularly enzymatic extraction and enhanced filtration systems, have fundamentally improved extraction efficiency, reduced contamination, and substantially lowered production costs while maintaining superior product quality. This technological shift represents a critical competitive advantage for producers capable of implementing these advanced methodologies.

These processing innovations have unlocked new market applications and sustainability benefits that expand commercial opportunities. By enabling consistent texture profiles and improved bioavailability, advanced extraction methods have opened locust bean gum to emerging product categories such as plant-based dairy alternatives and specialized nutraceutical formulations, where precise functional performance is non-negotiable. Simultaneously, these advanced techniques significantly reduce chemical usage and energy consumption, generating more sustainable production cycles that align with industry-wide commitments to environmental responsibility and responsible sourcing. This convergence of improved product performance, expanded application potential, and enhanced sustainability creates a compelling value proposition that strengthens locust bean gum's competitive position across both established and emerging market segments.

Category-wise Analysis

Form Insights

Powder form is the leading segment with approximately 72% of the market revenue share in 2025. Powdered form is produced through advanced milling and drying techniques, which result in a consistent particle size that facilitates uniform hydration and integration into diverse product formulations. For industrial processors, especially in Europe and North America, the standardization in powder texture ensures predictable outcomes in large-scale applications such as dairy stabilization, bakery texture improvement, and processed food manufacture.

Gel form is likely to be the fastest- growing segment from 2025 to 2032. This is mainly attributable to the Due to their increasing integration of gel locust bean gum in specialized pharmaceutical, cosmetic, and industrial products. These gel variants are pivotal in the development of hydrogel technologies for targeted drug delivery, wound care, and biomedical packaging, offering a moist environment that accelerates healing and controlled release. In personal care, gel-based formulations enhance hydration, improve bioadhesion to skin and tissue, and serve as effective carriers for active ingredients, which are highly valued in topical creams, masks, and medical devices.

Application Insights

Food and & Bbeverages is slated to be dominate the leading segment with an estimated 60% locust bean gum market revenue share in 2025. Primary drivers for the leadership of this segment include increased widening consumption of dairy analogues, confectionery, and gluten-free bakery items where locust bean gum serves as an essential texture modifier. Its neutral flavor and compatibility with other hydrocolloids likesuch as carrageenan, help replicate the texture of traditional dairy products without altering taste or nutrition. Additionally, pPowdered locust bean gum is often used in premium non-dairy ice creams and spreadable cheeses for enhanced smoothness and freeze-thaw stability, as well as clean-label formulations targeting health-conscious buyers.

Pharmaceutical is expected to be the fastest -growing applicationsegment between 2025 and 2032., Because of itsowing to the biocompatibility, non-toxicity, and functionality of locust bean gum as a versatile excipient. In capsule coatings, locust bean gumit provides efficient film formation, moisture barrier properties, and enhances the stability of active pharmaceutical ingredients, reducing the risk of premature degradation. This is particularly beneficial for pediatric and geriatric drug delivery where taste masking, prolonged release, and easy swallowing are prioritized.

End-User Insights

Food Pprocessing segment currently leads with an approximate 53% market share in 2025. Locust bean gum is widely adopted by leading food multinationals such as Nestlé, Danone and Unilever primarily for its roles as a texturizing, stabilizing, and gelling agent in various high-quality processed foods. These multinationals are increasingly prioritizing locust bean gum because it is naturally derived, non-allergenic, and aligns with consumer demands for transparent ingredient lists.

Pharmaceutical Manufacturing is anticipated to be the fastest-growing segment during the 2025-2032 forecast period. This is primarily Ddue to theingredient’s ability of the ingredient to differentiate products and improve therapeutic efficacy in oral and topical drug delivery systems. Locust bean gum is prized for its natural biocompatibility and safety profile, making it an attractive pharmaceutical excipient for sustained-release tablets, transdermal patches, bioadhesive gels, and wound care dressings.

Regional Insights

Europe Locust Bean Gum Market Trends

Europe’s leading position in the locust bean gum market leads with 41% of globalthe locust bean gum market share in 2025,. Major European economies such as countries like Germany, the U.K., Spain, and France have established a robust demand base for locust bean gum, especially in premium bakery and plant-based dairy sectors. Regulatory harmonization under the European Food Safety Authority (EFSA) ensures standardized quality and safety benchmarks for food additives, which facilitates broader industry adoption and cross-border trade of locust bean gum-containing products.

Spain’s role as a primary raw material supplier complements Europe’s dominance. The country’s Mediterranean climate supports extensive carob plantations and extraction facilities, ensuring stable and high-quality locust bean gum supply for regional processors. Investments in local production capacity and modern extraction technologies enable European suppliers to overcome some of the market’s inherent supply chain risks. The region’s sustained leadership is also attributed to the strong emphasis on quality assurance, with; producers in Europe frequently setting benchmarks for purity, consistency, and labeling standards, inspiring global adoption.

North America

North America commands approximately 34% of the global market in 2025, establishing itself as a dominant regional force driven by sophisticated food processing infrastructure and stringent regulatory oversight. The United States anchors this leadership position, with locust bean gum deeply embedded across critical food categories including dairy products, bakery goods, and functional beverages. These applications leverage locust bean gum's exceptional texturizing and stabilizing capabilities to deliver clean-label formulations that resonate strongly with health-conscious consumers increasingly focused on ingredient transparency. The region's advanced manufacturing ecosystem and consumer sophistication have created ideal conditions for locust bean gum adoption, positioning it as a preferred alternative to synthetic additives across premium and mainstream product tiers.

Market growth in North America is further catalyzed by consumer demand for natural, non-GMO ingredients and industry-wide clean-label momentum. Consumers across the region demonstrate pronounced preferences for plant-based, minimally processed ingredients, which favors locust bean gum over synthetic or loosely regulated alternatives. Industry certifications have accelerated ingredient adoption among both premium and mass-market brands seeking competitive differentiation. Major ingredient suppliers such as Ingredion and CP Kelco have strengthened their regional market position through strategic investments in research and development and supply chain resilience, enabling them to innovate novel formulations while ensuring stable, reliable ingredient access for food and beverage manufacturers. This combination of regulatory alignment, consumer preferences, and supplier innovation has solidified North America's status as a high-growth market for locust bean gum.

North America, accounting for about 34% of the global locust bean gum market in 2025, has emerged as a significant consumer mainly due to its advanced food processing and strong regulatory frameworks. The United States is the regional leader, leveraging locust bean gum extensively in segments such as dairy, bakery, and functional beverages. Such applications benefit immensely from the texturizing and stabilizing abilities of locust bean gum, which provide clean-label solutions that appeal to health-conscious and ingredient-aware consumers.

Consumer preferences in North America emphasize non-GMO, natural ingredients, further fueling the uptake of locust bean gum over synthetic or less-regulated options. Industry-led initiatives promoting clean-label and organic certification have accelerated ingredient adoption in premium and mainstream brands.Leading companies, including Ingredion and CP Kelco, have driven regional innovation through investments in R&D and supply chain resilience, ensuring stable access and supporting novel formulations within food and beverage manufacturing.?

Asia Pacific Locust Bean Gum Market Trends

Asia Pacific is positioned to become the fastest-growing regional market for locust bean gum through 2032, driven by a powerful confluence of rising consumer demand, supportive regulatory environments, and technological advancement. Key markets including China, Japan, India, and ASEAN nations are experiencing accelerated consumption of processed foods, functional beverages, and modern bakery products, where locust bean gum plays a critical functional role in texture modification, product stability, and clean-label formulation. This regional growth trajectory reflects fundamental demographic and economic shifts reshaping consumer behavior across the Asia Pacific landscape, positioning locust bean gum as an essential ingredient for manufacturers targeting these emerging consumption patterns.

Regional market expansion is further underpinned by urbanization, rising disposable incomes, and shifting dietary preferences toward Western-style convenience foods. As urban populations expand and household incomes increase across Asia Pacific, consumers are progressively adopting packaged foods, ready-to-eat products, and value-added formulations traditionally associated with developed markets. This dietary transition creates substantial growth opportunities across dairy and bakery sectors where manufacturers increasingly rely on the ingredient to meet consumer expectations for product quality, shelf stability, and ingredient transparency. The convergence of demographic tailwinds, regulatory support for natural food additives, and proven processing innovations positions Asia Pacific as a high-potential growth frontier, with locust bean gum well-positioned to gain significantly as regional food manufacturing scales to meet surging consumer demand for modern, processed food products.

Competitive Landscape

The global locust bean gum market structure demonstrates moderate concentration with a bifurcated competitive landscape comprising dominant multinational players alongside a diverse base of regional and specialized suppliers. Industry leaders, including CP Kelco, Tate & Lyle, Brenntag AG, and Ingredion, collectively control approximately 47% of the global market share, leveraging significant competitive advantages that reinforce their market positions. These tier-one competitors maintain leadership through proprietary extraction technologies, expansive application portfolios spanning multiple food sectors, and resilient, vertically-integrated supply chains that enable them to serve global customers with consistent quality and reliability. Their scale advantages, research capabilities, and established customer relationships create formidable barriers to entry while allowing them to invest continuously in innovation and market expansion.

The remaining market share is distributed among regional producers, specialized suppliers, and emerging competitors who collectively represent substantial fragmentation and opportunity. This distributed competitive structure creates a dynamic market environment where established leaders must defend market share against nimble regional players offering localized supply advantages, specialized product formulations, or competitive pricing. This balanced competitive dynamic benefits end-users through diverse sourcing options, technological advancement, and pricing competition, while simultaneously creating pathways for emerging suppliers to establish regional footholds and gain market traction through differentiation strategies or geographic specialization.

The global locust bean gum market exhibits a moderately concentrated structure, with a handful of leading companies holding significant influence but also many regional and niche suppliers contributing to overall fragmentation. Top players such as CP Kelco, Tate & Lyle, Brenntag AG, and Ingredion collectively command approximately 47% of the total market share, leveraging advanced extraction technologies, diverse application portfolios, and robust supply chains to maintain their leadership positions.

Key Industry Developments

- In November 2025, Bühler Group's New Chocolate Challenge has crowned three cocoa-free startups, Foreverland, Green Spot Technologies, and Kawa Project, as winners from over 50 applicants, each offering innovative climate-resilient chocolate alternatives. Foreverland ferments carob waste (90% of which is typically discarded for locust bean gum extraction) to create Choruba, reducing water consumption by 90% and emissions by 80% compared to conventional chocolate. Green Spot Technologies upcycles food waste by fermenting fava bean fibers and grape skins into functional ingredients, while Kawa Project transforms spent coffee grounds into alkalized cocoa powder substitutes.

- In October 2025, the Africa Pavilion at the From Seeds to Foods exhibition showcased over 160 products from 40+ sub-Saharan African countries, highlighting the continent's agricultural biodiversity and market potential. Featured highlights include world-award-winning chocolate from São Tomé and Príncipe, soumbala (fermented African locust bean paste), fonio grain, Penja pepper with Protected Geographical Indication status, and nutrient-rich baobab, moringa, and traditional wild foods. In 2024: Tate & Lyle PLC in November of 2024 completed its acquisition of CP Kelco, a supplier of pectin, specialty gums and other ingredients.

- In August 2025, research published in Nature demonstrated that modifying fish gelatin with 0.3% locust bean gum significantly enhances its gelling properties, thermal stability, and viscosity in acidic environments (pH 2-7), particularly for applications such as acid gel gummies. This modification creates a denser gel network through electrostatic and hydrogen bonding interactions, overcoming the traditional limitations of fish gelatin in acidic conditions and offering a robust alternative to mammalian gelatin for clean-label confectionery.

Companies Covered in Locust Bean Gum Market

- Batory Foods

- Cargill, Incorporated

- Carob S.A.

- CP Kelco

- DuPont de Nemours, Inc.

- E. A. Calvó S.L.

- Euroduna Food Ingredients GmbH

- Fiberstar, Inc.

- FMC Corporation

- Gerkens Cacao Nederland B.V.

- Gumix International S.L.

- Hawkins Watts Limited

- Ingredion Incorporated

Frequently Asked Questions

The global locust bean gum market is projected to reach US$ 280.0 million in 2025.

The main market drivers of the growth of the Locust Bean Gum market areinclude growing health consciousness, expanding applications in pharmaceuticals increased demand for clean-label and plant-based ingredients, and versatility in food and beverage applications.

The locust bean gum market is poised to witness a CAGR of 2.6% from 2025 to 2032.

Rapidly growing food and pharmaceutical sectors in China, India, and ASEAN are unlocking significant opportunities.

Cargill, CP Kelco, DuPont de Nemours Inc., and Botary Foods. are some of the key players in the locust bean gum market.