- Food Ingredients & Additives

- Food Grade Xanthan Gum Market

Food Grade Xanthan Gum Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Food Grade Xanthan Gum Market by Function (Thickener, Stabilizer, Texturizing Agent), End-user (Bakery & Confectionery, Meat & Poultry, Sauces & Dressings, Beverages, Dairy Products), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Food Grade Xanthan Gum Market Share and Trends Analysis

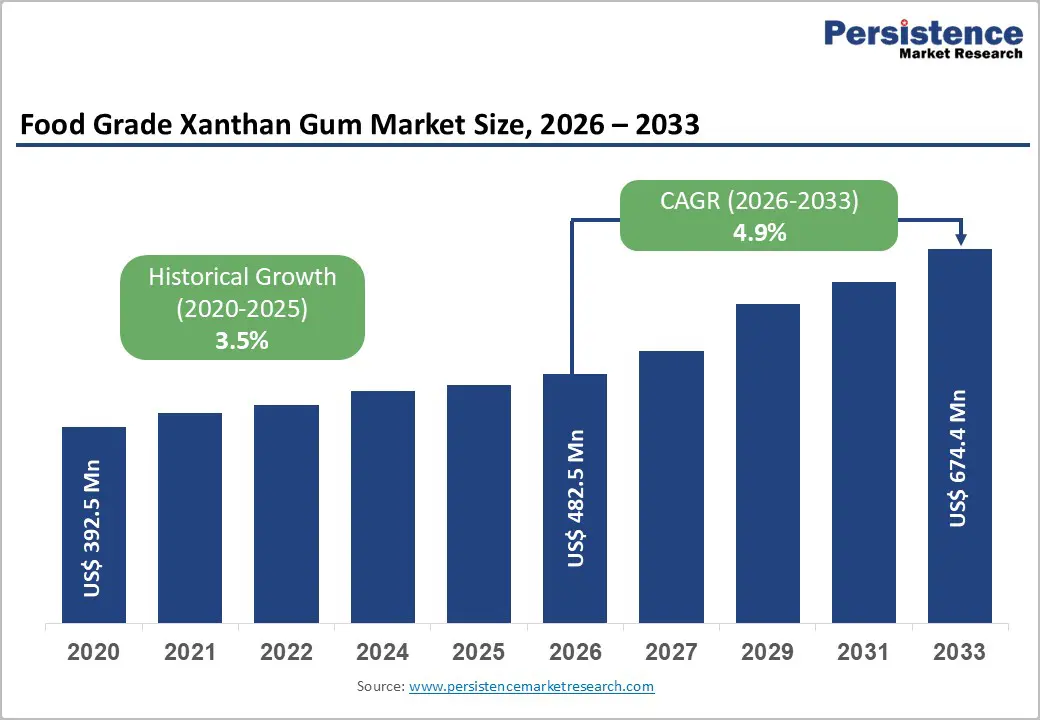

The global food grade xanthan gum market size is expected to be valued at US$ 482.5 million in 2026 and projected to reach US$ 674.4 million by 2033, growing at a CAGR of 4.9% between 2026 and 2033. The global food grade xanthan gum market is evolving at the intersection of clean-label innovation, plant-based formulation science, and industrial food processing efficiency.

As manufacturers reformulate products to meet gluten-free, low-fat, and vegan demands, xanthan gum is emerging as a critical multifunctional ingredient. Its ability to deliver stability, texture, and consistency across diverse applications positions it as the backbone of modern food formulation. At the same time, advancements in fermentation technology and hydrocolloid blending are reshaping product performance standards. Regional production hubs and shifting consumption patterns are further redefining supply-demand dynamics. This convergence of health-driven demand and functional performance is accelerating both volume growth and value creation across the market.

Key Industry Highlights:

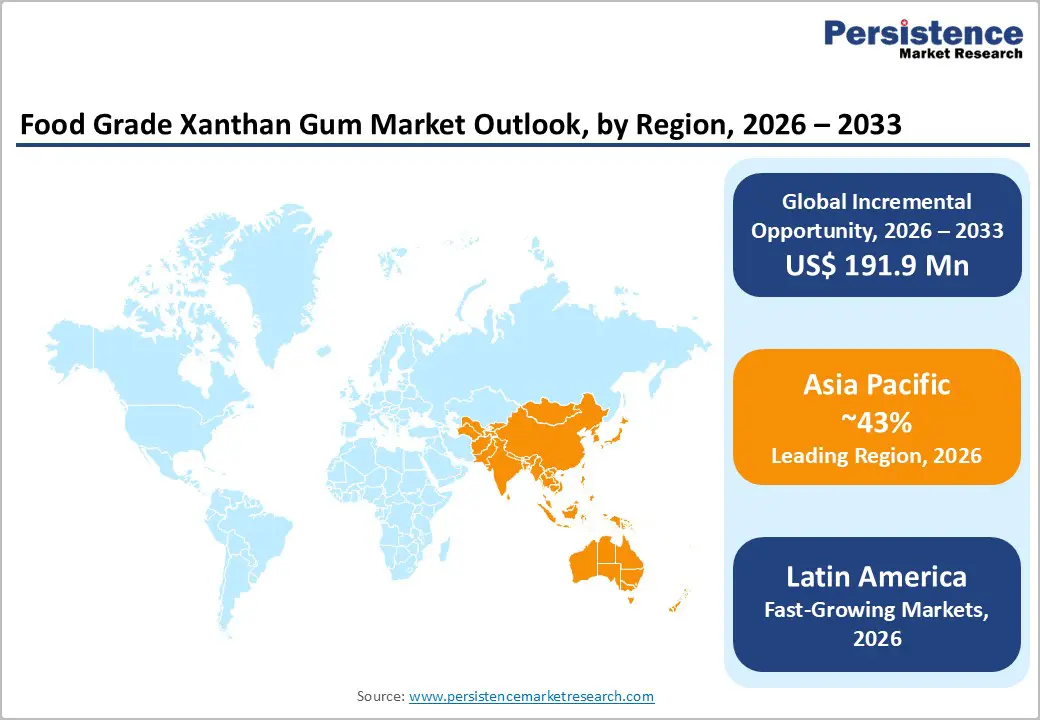

- Leading Region: Asia Pacific, holding approximately 43% market share, driven by large-scale production in China, strong raw material availability, and expanding food processing industries across emerging economies

- Fastest-Growing Region: Latin America, fueled by rising middle-class consumption, rapid expansion of organized retail, and increasing demand for packaged and convenience foods

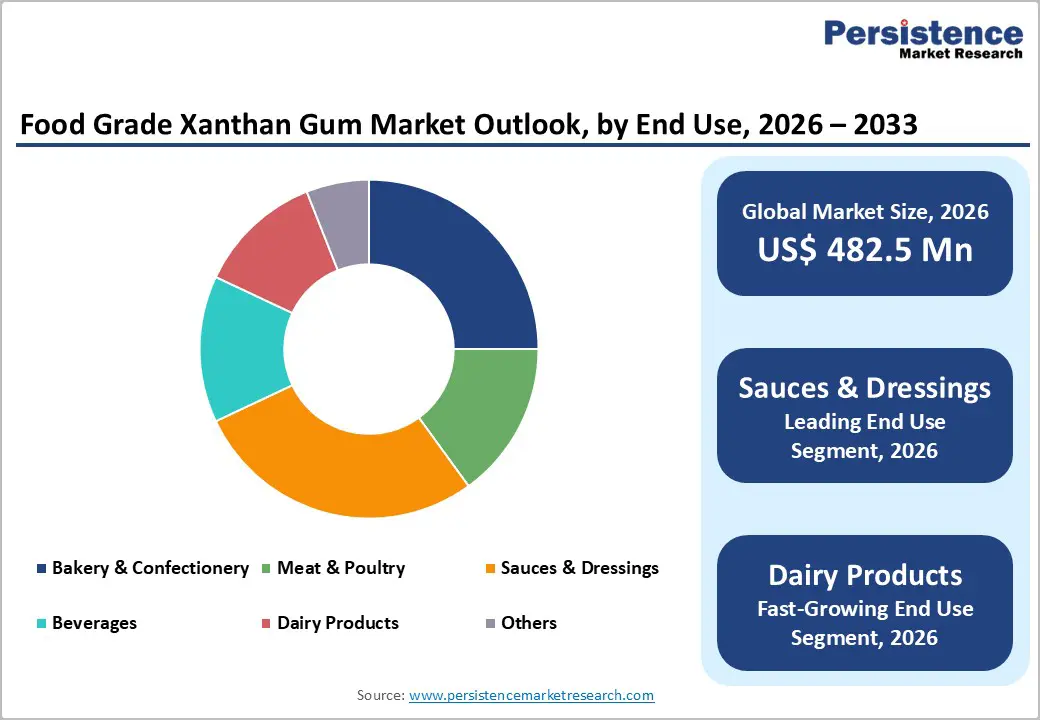

- Fastest-Growing End Use Segment: Dairy Products, driven by rising consumption of plant-based milk, yogurt alternatives, and demand for improved texture and suspension properties

- Growth Indicators: Increasing shift toward gluten-free, clean-label, and health-centric diets, positioning xanthan gum as a key functional ingredient in bakery, beverages, and reduced-fat formulations

- Opportunities: Expanding applications in plant-based dairy and vegan meat alternatives, supported by demand for texture optimization and clean-label stabilization solutions

- Consumer Trends: Growing preference for vegan, allergen-free, and minimally processed foods is accelerating demand for fermentation-derived hydrocolloids with transparent labeling

- Key Developments: In September 2025, the National Health Commission of China and the State Administration for Market Regulation introduced updated food safety standards for xanthan gum, strengthening regulatory frameworks; in September 2024, Jungbunzlauer invested US$200 million in a new biogum facility in Canada to expand sustainable ingredient production.

| Key Insights | Details |

|---|---|

|

Global Food Grade Xanthan Gum Market Size (2026E) |

US$ 482.5 Mn |

|

Market Value Forecast (2033F) |

US$ 674.4 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.5% |

Market Dynamics

Driver - Growing Consumer Shift Toward Gluten-Free and Health-Centric Diets

A key growth driver for the global food grade xanthan gum market is the accelerating shift toward gluten-free and allergen-friendly diets. Increasing prevalence of celiac disease and gluten intolerance, highlighted by organizations such as the World Health Organization, is pushing food manufacturers to adopt effective alternatives to wheat-based ingredients. Xanthan gum plays a critical role by providing viscosity, elasticity, and structure in gluten-free formulations, making it essential in bakery products, pasta, and ready-to-eat meals. Its fermentation-derived origin and compatibility with clean-label formulations further strengthen its appeal among health-conscious consumers.

Beyond gluten-free applications, xanthan gum is increasingly used in low-fat and reduced-sugar products to maintain texture and mouthfeel. Companies such as Ingredion Incorporated and Cargill, Incorporated are expanding hydrocolloid portfolios to meet this demand, particularly across dairy alternatives, sauces, and functional beverages.

Restraints - Technical formulation challenges and regulatory scrutiny

Despite its versatility, food grade xanthan gum faces limitations related to formulation complexity and evolving regulatory oversight. While effective as a standalone thickener, optimal performance in processed foods often requires precise blending with other hydrocolloids such as guar gum or locust bean gum. Inconsistent ratios can lead to undesirable textures like excessive viscosity or phase separation, posing challenges for small and mid-sized manufacturers with limited R&D capabilities. Additionally, regulatory bodies such as the European Commission continue to reassess food additive safety, labeling standards, and acceptable intake levels. These ongoing evaluations, combined with concerns around digestive tolerance in high-consumption products, increase compliance costs and formulation complexity, ultimately restraining broader adoption across price-sensitive and mass-market applications.

Opportunity - Surging Demand for Plant-Based Dairy and Vegan Meat Alternatives

A significant growth opportunity in the global food grade xanthan gum market lies in the rapid expansion of plant-based dairy and meat alternatives. Xanthan gum is widely used to replicate the creaminess, viscosity, and mouthfeel of dairy fats in products such as almond milk, oat-based beverages, and vegan yogurts. Its ability to stabilize emulsions and prevent phase separation makes it essential in delivering consistent texture in plant-based formulations. Growing consumer preference for vegan and flexitarian diets is accelerating demand for such multifunctional, plant-derived stabilizers.

Industry trends highlighted by organizations like the Personal Care Products Council reflect broader demand for botanical ingredients across sectors. Companies such as Tate & Lyle and Archer Daniels Midland Company are investing in advanced variants like rapid-hydration and low-dust xanthan gum, enabling efficient processing and unlocking high-margin opportunities in next-generation food products.

Category-wise Analysis

Function Insights

The stabilizer segment holds the leading position in the global food grade xanthan gum market, driven by its exceptional ability to maintain stable emulsions in complex food systems. Xanthan gum is widely used in sauces and dressings to prevent phase separation, ensuring uniform consistency and extended shelf life. Its high resistance to shear, temperature variations, and pH fluctuations makes it particularly effective in processed and packaged foods that require stability during storage and transport. This functionality is critical for maintaining product quality in large-scale food manufacturing.

In contrast, the texturizing agent segment is witnessing rapid growth, especially in dairy products and bakery applications. Xanthan gum enables the development of desirable mouthfeel, viscosity, and structure, particularly in low-fat and reduced-calorie formulations. Its ability to mimic fat-like sensory properties makes it valuable in premium and health-oriented products, supporting innovation in clean-label and functional food categories.

End-user Insights

The sauces and dressings segment remains the dominant end-use category, accounting for approximately 32% of the global food grade xanthan gum market in 2025. Xanthan gum is widely used to enhance viscosity, improve cling, and prevent phase separation in condiments such as salad dressings, mayonnaise, and dips. Its ability to maintain stability under varying temperatures and shear conditions makes it indispensable in industrial food processing. Additionally, it supports extended shelf life and consistent product quality, which are critical for large-scale packaged food manufacturers.

The dairy products segment is the fastest-growing, driven by increasing consumption of plant-based milk, yogurt, and dessert alternatives. Xanthan gum plays a key role in preventing sedimentation and delivering a smooth, creamy texture. Meanwhile, the meat and poultry segment is expanding steadily, with xanthan gum used in brining and marinades to enhance moisture retention, improve yield, and optimize texture in processed protein products.

Regional Insights

Asia Pacific Food Grade Xanthan Gum Market Trends and Insights

Asia Pacific dominates the global food grade xanthan gum market, accounting for around 43% share in 2025, driven by large-scale production capabilities and expanding food processing industries across China, India, and ASEAN countries. China remains the global manufacturing hub, with companies like Fufeng Group Company Limited leading in scale and cost efficiency. The region benefits from strong raw material availability, favorable conditions for fermentation-based production, and increasing demand for processed and convenience foods, supporting both domestic consumption and exports.

Innovation in the region is focused on improving production efficiency and expanding global market reach. In India, government initiatives supporting food processing modernization are encouraging the use of functional ingredients in traditional and packaged foods. Additionally, the rapid growth of modern retail and e-commerce channels is increasing accessibility to xanthan gum-based products, while the shift toward plant-based additives continues to drive long-term market expansion.

Latin America Food Grade Xanthan Gum Market Trends and Insights

Latin America is emerging as the fastest-growing region in the food grade xanthan gum market through 2033 driven by expanding middle-class populations and the rapid growth of organized food retail in countries such as Brazil and Mexico. Changing dietary habits and increasing preference for convenience foods are accelerating demand for packaged sauces, dressings, and bakery products where xanthan gum plays a critical role in improving stability and texture. This shift is strengthening the adoption of functional food ingredients across urban markets.

Regional growth is further supported by favorable trade frameworks and a rising focus on value-added food processing. In countries like Argentina and Colombia, manufacturers are incorporating xanthan gum to enhance texture while improving the nutritional profile of traditional foods. Additionally, growing interest in dairy alternatives and lactose-free products is creating new application areas. As supply chains and processing capabilities improve, Latin America is evolving into a key demand center for food-grade hydrocolloids.

Competitive Landscape

The food grade xanthan gum market demonstrates a moderately consolidated structure, led by major global players such as Cargill, Incorporated, Archer Daniels Midland Company, and Fufeng Group Company Limited. These companies maintain strong control through vertically integrated operations spanning raw material sourcing to finished product distribution. Strategic priorities include geographic expansion, microbial strain optimization, and acquisitions to secure supply chains. At the same time, specialized firms like Jungbunzlauer Holding AG and Lubrizol Corporation focus on high-purity and application-specific variants, strengthening niche market segments.

Competition is increasingly driven by innovation, clean-label positioning, and global supply chain optimization. Companies are expanding specialty ingredient portfolios and targeting high-growth sectors such as dairy alternatives, beverages, and bakery products in emerging markets. Investments in advanced processing technologies and product customization are enabling manufacturers to meet evolving customer requirements, supporting sustained market expansion.

Key Developments:

- In September 2025, National Health Commission of the People's Republic of China and the State Administration for Market Regulation jointly released the National Food Safety Standards for xanthan gum, strengthening regulatory oversight and quality benchmarks for its production and application in food products.

- In September 2024, Jungbunzlauer announced a US$200 million investment to establish a first-of-its-kind biogum production facility in Canada, aimed at expanding its portfolio of biodegradable and sustainable hydrocolloid ingredients.

Companies Covered in Food Grade Xanthan Gum Market

- Cargill, Incorporated

- DowDuPont, Inc.

- Ingredion Inc

- ADM

- Ashland Global Holdings Inc.

- Tate & Lyle PLC

- Jungbunzlauer Holding AG

- Nestlé Health Science S.A.

- Fuerst Day Lawson Limited

- Lubrizol Corporation

- Fiberstar, Inc

- Fufeng Group Company Ltd

- Others

Frequently Asked Questions

The global Food Grade Xanthan Gum market is projected to be valued at US$ 482.5 Mn in 2026.

Growing Consumer Shift Toward Gluten-Free and Health-Centric Diets is a major driver of the global Food Grade Xanthan Gum market.

The global Food Grade Xanthan Gum market is poised to witness a CAGR of 4.9% between 2026 and 2033.

Surging Demand for Plant-Based Dairy and Vegan Meat Alternatives is a significant opportunity in the Food Grade Xanthan Gum market.

Major players in the global Food Grade Xanthan Gum market include Cargill, Incorporated, DowDuPont, Inc., Ingredion Inc, ADM, Ashland Global Holdings Inc., Tate & Lyle PLC, Jungbunzlauer Holding AG., and others.