- Automotive Components & Materials

- Tire Pressure Monitoring Systems (TPMS) Market

Tire Pressure Monitoring Systems (TPMS) Market Size, Share, Trends, Growth, Forecasts 2025 - 2032

Tire Pressure Monitoring Systems (TPMS) Market By Product Type (Direct TPMS, Indirect TPMS), Vehicle Type (Passenger Vehicles, Lights Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles) Sales Channel (OEM, Aftermarket), Regional Analysis 2025 - 2032

Tire Pressure Monitoring Systems (TPMS) Market Share and Trends Analysis

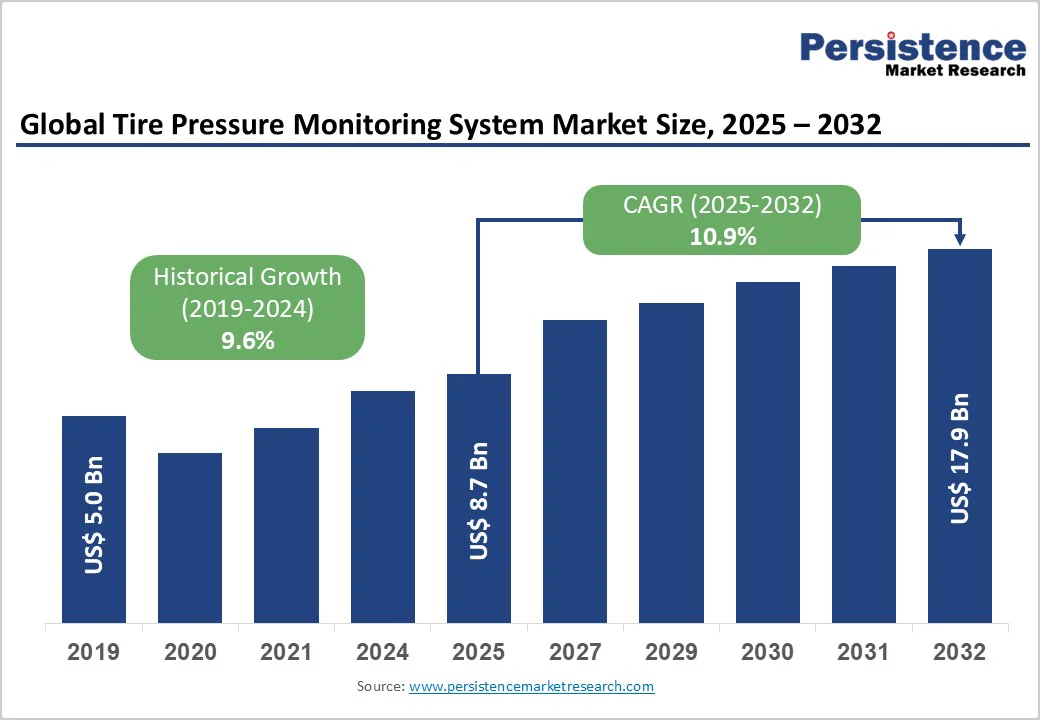

The global tire pressure monitoring systems (TPMS) market size is likely to value at US$ 8.715 Bn in 2025 and is projected to reach US$ 17.926 Bn by 2032, growing at a CAGR of 10.9% between 2025 and 2032.

This robust growth trajectory is driven by stringent government safety regulations mandating TPMS installation across major automotive markets, rising consumer awareness regarding vehicle safety benefits, and accelerating integration with advanced driver-assistance systems (ADAS) technologies.

The market expansion is further supported by the rapid electrification of vehicles, requiring optimized tire pressure management for enhanced battery efficiency and range optimization.

Key Industry Highlights:

- Direct TPMS dominates with 63% market share with fastest growth while Indirect TPMS achieves a prominent CAGR at 10.2%, reflecting technology preferences and cost optimization strategies across market segments.

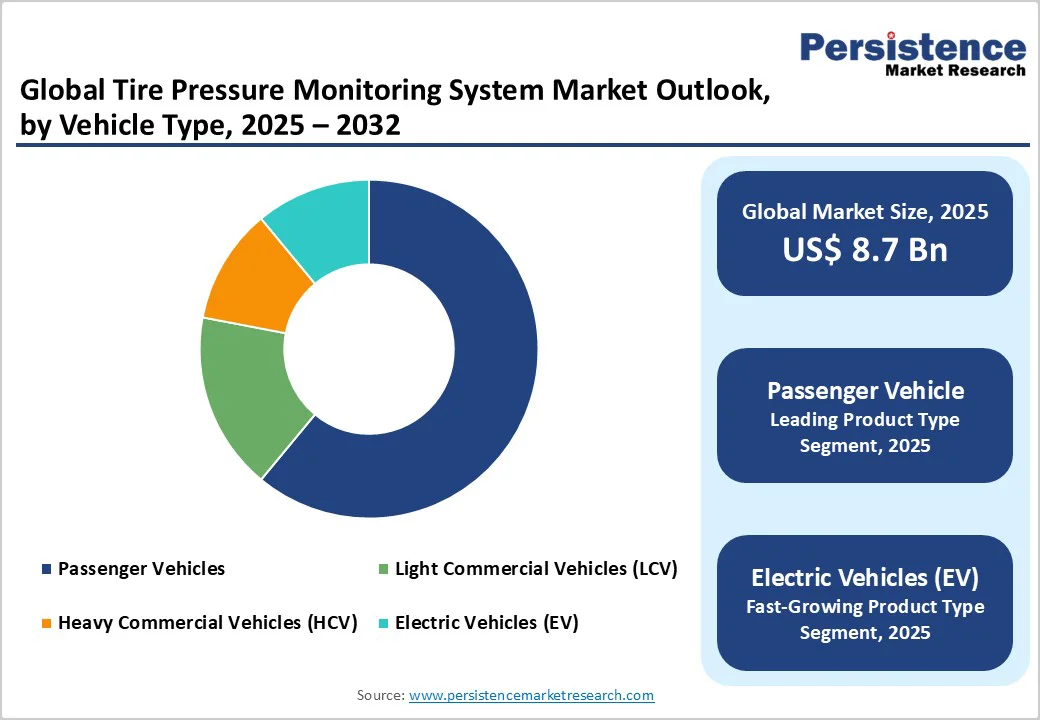

- Electric vehicles represent fastest-growing vehicle segment at 12.5% CAGR, creating substantial opportunities for advanced TPMS integration and range optimization applications.

- OEM channel maintains 78% market dominance while aftermarket grows at 11.8% CAGR, supported by vehicle replacement cycles and expanding service infrastructure.

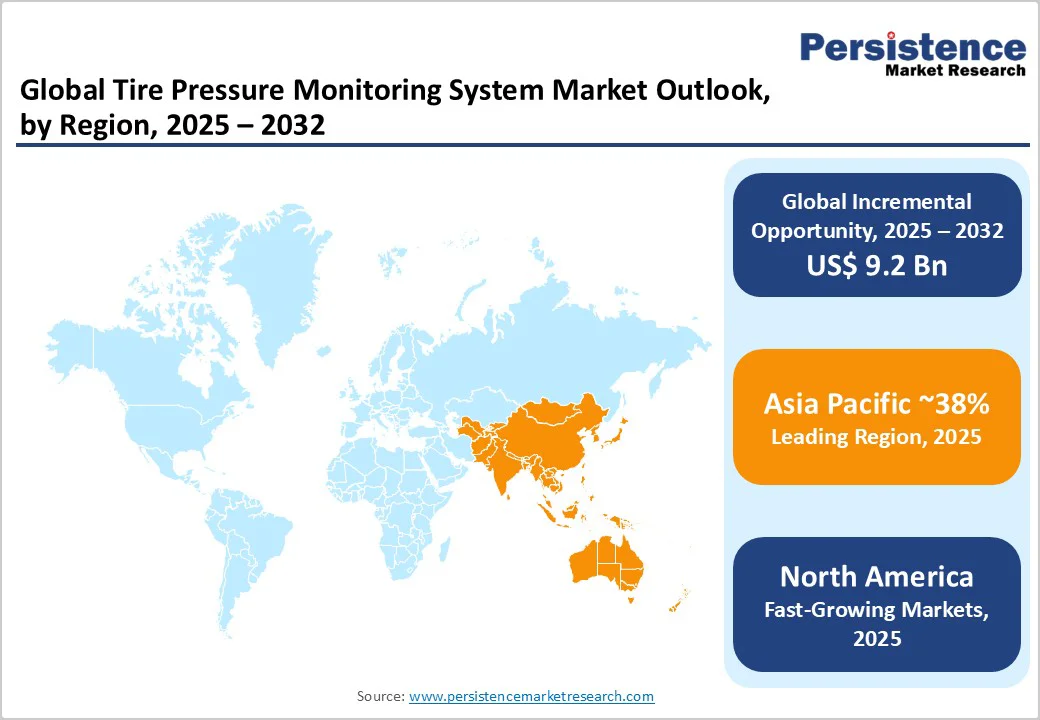

- Asia Pacific leads with 38% global market share, Europe holds 24%, and North America shows 10.7% CAGR, reflecting regional automotive production patterns and regulatory implementation timelines.

- Continental AG and Sensata Technologies lead market consolidation with top 5 suppliers controlling around 55-60% of global shipments, while emerging players target specialized applications and regional markets.

- Strategic developments focus on AI integration, IoT connectivity, and commercial vehicle applications, with major capacity expansions in Asia Pacific supporting continued market growth.

| Key Insights | Details |

|---|---|

| Tire Pressure Monitoring System Market Size (2025E) | US$ 8.7 Billion |

| Market Value Forecast (2032F) | US$ 17.9 Billion |

| Projected Growth CAGR (2025-2032) | 10.9% |

| Historical Market Growth (2019-2024) | 9.6% |

Market Dynamics Analysis

Drivers - Stringent Regulatory Mandates and Safety Compliance

Government regulations worldwide have emerged as the primary catalyst driving TPMS market adoption, with mandatory installation requirements implemented across major automotive markets. The United States pioneered this movement through the Transportation Recall Enhancement, Accountability, and Documentation (TREAD) Act, requiring all light vehicles under 10,000 pounds sold after September 2007 to include TPMS.

The European Union followed with comprehensive regulations mandating TPMS installation in all new passenger cars from November 2014, with commercial vehicles up to 3.5 tonnes included from July 2024.

Asia Pacific markets have rapidly adopted similar mandates, with China implementing TPMS requirements for all vehicles manufactured after January 2020, while South Korea enforced regulations in 2013 for vehicles under 3.5 tonnes.

These regulatory frameworks are projected to prevent approximately 660 fatalities and 33,000 injuries annually according to the National Highway Traffic Safety Administration (NHTSA), while reducing tire-related accidents by up to 56%. The cascading effect of these mandates creates sustained baseline demand exceeding 85 million vehicles annually across regulated markets, establishing TPMS as a non-negotiable safety component rather than optional equipment.

Rapid Electric Vehicle Adoption and Range Optimization Requirements

The accelerating transition toward electric mobility has created unprecedented demand for precise tire pressure monitoring solutions, as underinflated tires significantly impact battery range and energy efficiency. Electric vehicles demonstrate 3-4% greater sensitivity to tire pressure variations compared to internal combustion engines, making accurate TPMS data critical for range optimization. Industry analysis indicates that proper tire inflation can improve electric vehicle range by up to 25 kilometers per charge cycle, while reducing rolling resistance by 15-20%.

The global electric vehicle tire market is projected to grow from USD 11.4 billion in 2025 to USD 27.6 billion by 2032 at a CAGR of 13.5%, creating substantial opportunities for integrated TPMS solutions. Leading automotive manufacturers including Tesla, BYD, and traditional OEMs are increasingly specifying advanced TPMS with real-time data analytics as standard equipment across their electric vehicle portfolios.

This trend is reinforced by government incentives promoting electric vehicle adoption, with over 40 countries implementing zero-emission vehicle mandates by 2030, directly translating to expanded TPMS market potential.

Restraint - High Implementation Costs and Aftermarket Price Sensitivity

The significant cost differential between OEM and aftermarket TPMS solutions presents a substantial barrier to market expansion, particularly in price-sensitive emerging markets. Direct TPMS sensors typically cost USD 50-100 per wheel for OEM applications, while aftermarket alternatives range from USD 20-60 per sensor, creating affordability challenges for vehicle owners seeking replacement solutions.

Additionally, installation and programming expenses can add a moderate to substantial amount per sensor, raising the overall replacement cost per vehicle to a few hundred dollars, depending on the system’s design complexity and calibration requirements.

Battery replacement requirements every 7-10 years for direct TPMS sensors create recurring cost burdens, with replacement sensor costs often exceeding 60% of original system value.

Market analysis indicates that 34% of vehicle owners in emerging markets defer TPMS repairs due to cost considerations, particularly for vehicles over five years old where aftermarket sensor compatibility issues increase complexity and expense. The cost sensitivity is further amplified by insurance coverage limitations, with most policies excluding TPMS-related repairs, forcing consumers to absorb full replacement costs out-of-pocket.

Technological Complexity and Sensor Compatibility Challenges

The increasing diversity of TPMS protocols and sensor technologies across different vehicle manufacturers has created significant compatibility and service complexity issues that constrain market growth. Over 150 different TPMS sensor configurations exist across global automotive brands, requiring specialized programming tools and technical expertise for proper installation and calibration.

Independent service providers face substantial investment requirements for acquiring advanced TPMS diagnostic equipment capable of servicing multiple vehicle brands, creating significant barriers to aftermarket service expansion, especially within smaller or cost-sensitive markets.

Wireless interference and signal degradation issues affect approximately 8-12% of TPMS installations, particularly in urban environments with high electromagnetic interference, leading to false alerts and reduced system reliability.

The proliferation of different communication protocols including 315 MHz, 433 MHz, and emerging Bluetooth Low Energy standards has fragmented the market, preventing standardization benefits and increasing inventory complexity for distributors. Additionally, cybersecurity concerns regarding wireless TPMS communications have emerged, with potential vehicle tracking risks identified by privacy advocates, potentially limiting adoption in security-conscious markets.

Opportunity - Fleet Management and Commercial Vehicle Integration

The rapid digitization of fleet operations presents exceptional growth opportunities for advanced TPMS solutions that integrate with comprehensive telematics platforms. Commercial vehicle fleet operators achieve average cost savings of USD 1,200-1,800 per vehicle annually through predictive TPMS systems that prevent roadside failures and optimize maintenance scheduling.

The global commercial vehicle telematics market, valued at USD 4.8 billion in 2024, is increasingly incorporating TPMS data streams to provide holistic vehicle health monitoring, creating integration opportunities worth an estimated USD 850 million by 2028. Last-mile delivery and e-commerce logistics represent particularly lucrative segments, with companies like Amazon, FedEx, and UPS investing heavily in tire monitoring technologies to minimize delivery delays and reduce operational costs.

Government initiatives promoting smart transportation infrastructure, including connected vehicle corridors and real-time traffic management systems, create opportunities for TPMS data integration worth an estimated USD 1.4 billion globally. The emergence of autonomous commercial vehicles further amplifies TPMS importance, as unmanned vehicles require redundant safety systems including advanced tire monitoring capabilities.

Smart Tire Pressure Monitoring System and Connected Vehicle Integration

The evolution of TPMS from a basic safety feature to a fully connected, intelligent vehicle component is opening transformative opportunities in the global market. Modern TPMS now seamlessly integrate with smart tires, IoT platforms, and ADAS, providing real-time tire data that enhances stability control, adaptive cruise, and autonomous driving capabilities.

Vehicles equipped with these advanced systems show notable safety and efficiency benefits, including lower accident rates and improved fuel economy. AI-driven analytics and predictive maintenance enable operators to anticipate tire failures weeks in advance, reducing downtime and operational costs.

Leading manufacturers and technology firms are investing heavily in next-generation TPMS platforms, combining pressure, temperature, and motion sensors with wireless communication. Blockchain-enabled tire tracking and lifecycle management further add value, improving transparency and warranty efficiency.

Fleet management and OEM applications stand to benefit significantly, creating recurring revenue streams and positioning TPMS as a central element of the intelligent, connected vehicle ecosystem.

Category-wise Analysis

Product Type Insights

Direct TPMS maintains market leadership with a commanding 63% market share, positioning itself as the preferred technology solution across passenger and commercial vehicle segments. This dominance stems from superior accuracy capabilities, providing real-time pressure readings within ±1 psi tolerance compared to indirect systems' ±3-4 psi variance.

Direct TPMS systems utilize dedicated pressure sensors installed within each tire valve, enabling immediate detection of rapid pressure loss, slow leaks, and temperature variations that indirect systems cannot identify. The technology's precision makes it particularly valuable for premium vehicles, electric vehicles, and commercial fleets where tire performance directly impacts operational efficiency and safety outcomes.

Indirect TPMS represents the prominent-growing segment with a projected CAGR of 10.2%, driven primarily by cost advantages and simplified installation requirements. This growth trajectory reflects increasing adoption in European markets where automotive manufacturers leverage existing ABS wheel speed sensors to estimate tire pressure changes through rotational speed variations.

Indirect systems typically cost 30-40% less than direct alternatives while eliminating battery replacement requirements, making them attractive for cost-sensitive market segments. The technology's integration with existing vehicle electronics reduces complexity for aftermarket installations, supporting adoption in emerging markets where service infrastructure limitations favor simpler solutions.

Vehicle Type Analysis

Passenger vehicles dominate the TPMS market with a substantial 61% market share, reflecting the segment's large production volumes and comprehensive regulatory coverage across major automotive markets. This leadership position is reinforced by mandatory TPMS requirements in the United States, European Union, Japan, South Korea, and China covering virtually all passenger vehicle categories.

The segment benefits from consumer safety awareness and insurance incentives that increasingly recognize TPMS as essential safety equipment. Premium passenger vehicles demonstrate particularly high TPMS attachment rates exceeding 95%, with luxury brands often incorporating advanced direct TPMS systems as standard equipment across their model ranges.

Electric vehicles represent the fastest-growing vehicle segment with an exceptional CAGR of 12.5%, significantly outpacing overall market growth and creating substantial opportunities for advanced TPMS applications. This accelerated growth reflects the critical importance of tire pressure optimization for electric vehicle range and efficiency, where underinflated tires can reduce driving range by 15-25 kilometers per charge cycle.

Electric vehicle manufacturers including Tesla, BYD, and traditional OEMs transitioning to electrification specify advanced TPMS systems with enhanced accuracy and integration capabilities as standard equipment. The segment's growth is further supported by government incentives promoting electric vehicle adoption, with over 40 countries implementing zero-emission vehicle targets that directly expand the addressable TPMS market.

Sales Channel Analysis

Original Equipment Manufacturers (OEM) channel maintains market dominance with 78% market share, reflecting the channel's control over new vehicle production and regulatory compliance requirements. OEM dominance is reinforced by mandatory TPMS installation requirements across major markets, ensuring virtually 100% attachment rates for new vehicles in regulated jurisdictions.

The channel benefits from long-term supply agreements with major automotive manufacturers, providing volume pricing advantages and integrated development opportunities that strengthen competitive positioning. OEM relationships also enable early involvement in vehicle design processes, allowing TPMS suppliers to optimize system integration and develop customized solutions for specific vehicle platforms.

Aftermarket channels demonstrate robust growth with an 11.8% CAGR, driven by expanding vehicle parc requiring TPMS replacement and increasing consumer awareness of tire safety benefits. This growth trajectory reflects the aging of vehicles originally equipped with TPMS systems, creating replacement demand as sensor batteries reach end-of-life after 7-10 years of operation.

The aftermarket channel benefits from universal sensor technologies that reduce inventory complexity and enable broader service provider participation. Market expansion is further supported by decreasing sensor costs and simplified programming procedures that make aftermarket TPMS replacement more accessible to independent service providers and consumers seeking cost-effective alternatives to OEM replacement parts.

Regional Market Insights

North America Tire Pressure Monitoring Systems (TPMS) Market Trends

North America stands as a pioneering market for TPMS technology, establishing the regulatory foundation that influenced global adoption patterns while maintaining technological leadership through innovation ecosystems centered in the United States.

The region demonstrates a prominent CAGR of 10.7%, reflecting continued market expansion despite mature regulatory frameworks and high existing penetration rates. This sustained growth stems from vehicle fleet renewal cycles, technological upgrades to advanced TPMS systems, and expanding integration with connected vehicle platforms that enhance value propositions beyond basic safety compliance.

The United States market benefits from early regulatory implementation through the TREAD Act, 2000 creating a well-established supply chain infrastructure and comprehensive service network that supports both OEM and aftermarket channels effectively.

The region's strength lies in its robust regulatory framework and advanced automotive ecosystem that drives continuous innovation in TPMS technologies. Major automotive manufacturers including General Motors, Ford, and Stellantis, maintain substantial North American operations with integrated TPMS development capabilities, while technology leaders such as Sensata Technologies operate global TPMS operations from U.S. headquarters.

The presence of leading semiconductor companies including NXP Semiconductors and Infineon Technologies, supports advanced sensor development, while established tier-one suppliers maintain substantial R&D investments in next-generation TPMS platforms. Consumer awareness regarding tire safety benefits remains exceptionally high, with market research indicating around 80-90% of vehicle owners recognize TPMS value, supporting premium product adoption and aftermarket service demand.

Europe Tire Pressure Monitoring Systems (TPMS) Market Trends

Europe maintains a significant market position with 24% of the global market share, driven by comprehensive regulatory harmonization across European Union member states and strong emphasis on vehicle safety and environmental performance.

The region's market development reflects the successful implementation of EU General Safety Regulation requirements mandating TPMS installation across passenger and commercial vehicle categories, creating consistent demand patterns across diverse national markets.

Germany leads in TPMS adoption with a robust automotive manufacturing infrastructure and consumer preference for advanced safety technologies. The country's dominance reflects the presence of major automotive manufacturers, including Volkswagen Group, BMW, and Mercedes-Benz, alongside leading TPMS suppliers Continental AG, Robert Bosch GmbH, and Huf Hülsbeck & Fürst GmbH & Co. KG.

Regional growth is supported by stringent environmental regulations that emphasize fuel efficiency improvements and CO2 emission reduction, positioning TPMS as an essential component for regulatory compliance. The European Union's commitment to carbon neutrality by 2050 creates additional demand drivers as properly inflated tires contribute measurably to vehicle efficiency and emission reduction targets.

United Kingdom, France, and Spain demonstrate strong TPMS adoption rates exceeding over 85% for new vehicles, with aftermarket demand growing steadily as early TPMS installations reach replacement intervals.

The region benefits from advanced automotive service infrastructure and high consumer awareness regarding tire safety benefits, supporting premium TPMS product adoption and comprehensive aftermarket service availability across urban and rural markets.

Asia Pacific Tire Pressure Monitoring Systems (TPMS) Market Trends

Asia Pacific dominates the global TPMS market with commanding 38% market share, reflecting the region's position as the world's largest automotive production hub and rapidly expanding vehicle ownership base.

The region's leadership stems from China's emergence as the world's largest automotive market, with annual vehicle production exceeding 25 million units and comprehensive TPMS mandates implemented since January 2020. China holds over 38% share in Asia Pacific TPMS market revenue as of 2024, driven by mandatory installation requirements and expanding domestic vehicle production capabilities.

Japan and South Korea contribute substantial market value through advanced automotive technologies and early TPMS adoption, while India represents the fastest-growing segment with expanding middle-class vehicle ownership and emerging regulatory requirements.

Manufacturing advantages and cost competitiveness position Asia Pacific as the global production center for TPMS components and systems. The region benefits from established semiconductor manufacturing infrastructure, particularly in China, Taiwan, and South Korea, supporting cost-effective sensor production and assembly operations.

Leading global TPMS suppliers including Continental AG, DENSO Corporation, and Sensata Technologies maintain substantial manufacturing operations across the region, leveraging labor cost advantages and proximity to major automotive production centers.

The region's growth potential remains substantial, with vehicle ownership rates significantly below developed market levels and ongoing urbanization trends supporting sustained automotive market expansion.

Competitive Landscape

The global tire pressure monitoring system (TPMS) market demonstrates moderate concentration with the top five suppliers controlling approximately 55-60% of global shipments, creating a competitive landscape characterized by established technology leaders and emerging market participants.

Key players such as Continental AG, Sensata Technologies (Schrader), DENSO Corporation, ZF Friedrichshafen AG, and Robert Bosch GmbH collectively shape the global TPMS landscape through advanced sensor innovation, OEM collaborations, and integrated automotive electronics and chassis system capabilities.

The market structure reflects barriers to entry including substantial R&D investments, regulatory approval requirements, and established OEM relationships that favor existing suppliers while creating opportunities for specialized technology providers and regional market participants.

Strategic Developments

- In June 2024, Continental AG doubled its TPMS production capacity for passenger cars in India's Bangalore plant in June 2024, introducing next-generation TPMS technology aimed at enhancing safety and sustainability while reinforcing its Vision Zero initiative. This strategic expansion reflects growing demand in Indian automotive markets and Continental's commitment to localizing production for regional customer requirements.

- In October 2022, Volvo Group, Qamcom Group, and inventor Roman Iustin established Fyrqom AB, a specialized startup focusing on automated tire pressure monitoring system calibration for heavy-duty vehicles, offering advanced solutions that simplify service operations and improve reliability for commercial fleets. The collaboration demonstrates industry recognition of commercial vehicle TPMS opportunities and the value of specialized technology development for specific market segments.

Innovation and technology differentiation drive competition, with leading players advancing AI-based analytics, IoT integration, and holistic tire health monitoring. Strategies emphasize cost efficiency, localized manufacturing, and tailored solutions to meet regulatory and affordability needs across emerging and price-sensitive automotive markets.

Companies Covered in Tire Pressure Monitoring Systems (TPMS) Market

- Continental AG

- Sensata Technologies (Schrader)

- DENSO Corporation

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Huf Hülsbeck & Fürst GmbH & Co. KG

- VALEO

- HELLA GmbH & Co. KGaA

- Pacific Industrial Co., Ltd.

- NXP Semiconductors

- Infineon Technologies

- NIRA Dynamics

- BARTEC

- Alligator Ventilfabrik

- Steelmate

Frequently Asked Questions

The global TPMS market is valued at US$ 8.7 billion in 2025 and projected to reach US$ 17.9 billion by 2032, reflects strong demand driven by regulatory mandates and advancing vehicle safety technologies.

The market is primarily driven by stringent government safety regulations mandating TPMS installation globally, rapid electric vehicle adoption requiring precise tire pressure optimization for range efficiency, and increasing integration with advanced driver assistance systems (ADAS) and connected vehicle technologies.

The TPMS market demonstrates a projected CAGR of 10.9% from 2025 to 2032.

Key opportunities include expanding penetration in emerging markets with rising automotive production, integration with commercial vehicle fleet management systems delivering significant annual cost savings per vehicle, and convergence with smart tire technologies creating high-value IoT-enabled service platforms by the end of the forecast period.

Market leaders in the global Tire Pressure Monitoring System include Continental AG (Germany), Sensata Technologies/Schrader (USA), DENSO Corporation (Japan), ZF Friedrichshafen AG (Germany), and Robert Bosch GmbH (Germany), which collectively hold a prominent market share.