- Non-food Packaging

- Flexible Plastic Packaging Market

Flexible Plastic Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Flexible Plastic Packaging Market By Material Type (Polyethylene, Polypropylene), Product Type (Pouches, Bags & Sacks), Packaging Type, Application, and Regional Analysis for 2025 - 2032

Flexible Plastic Packaging Size and Trends Analysis

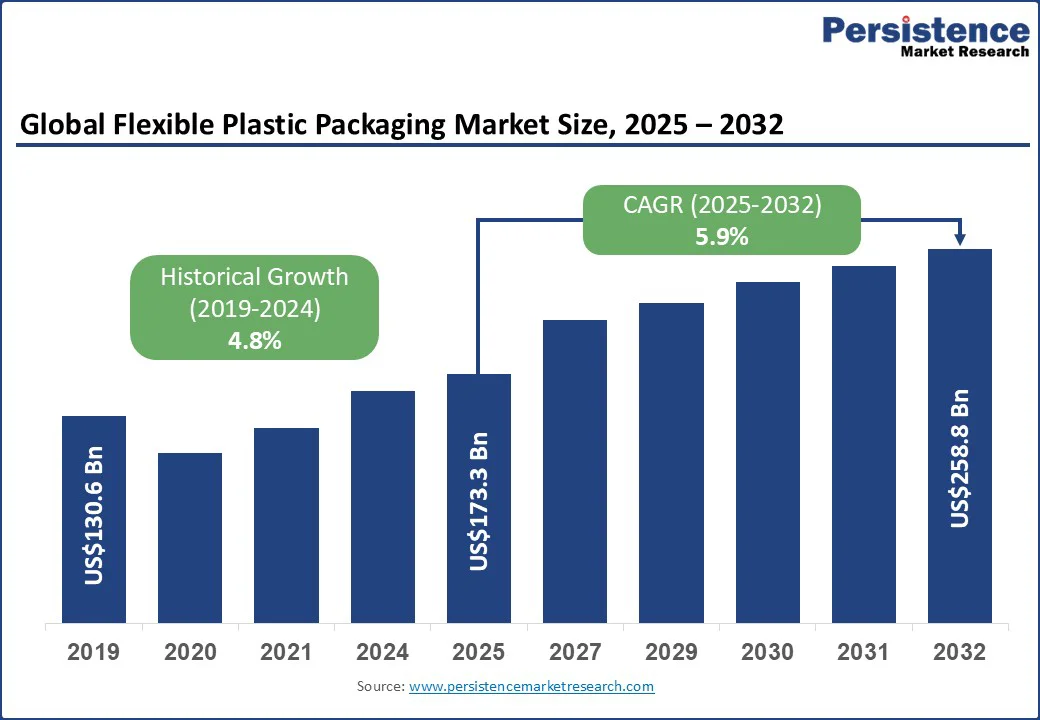

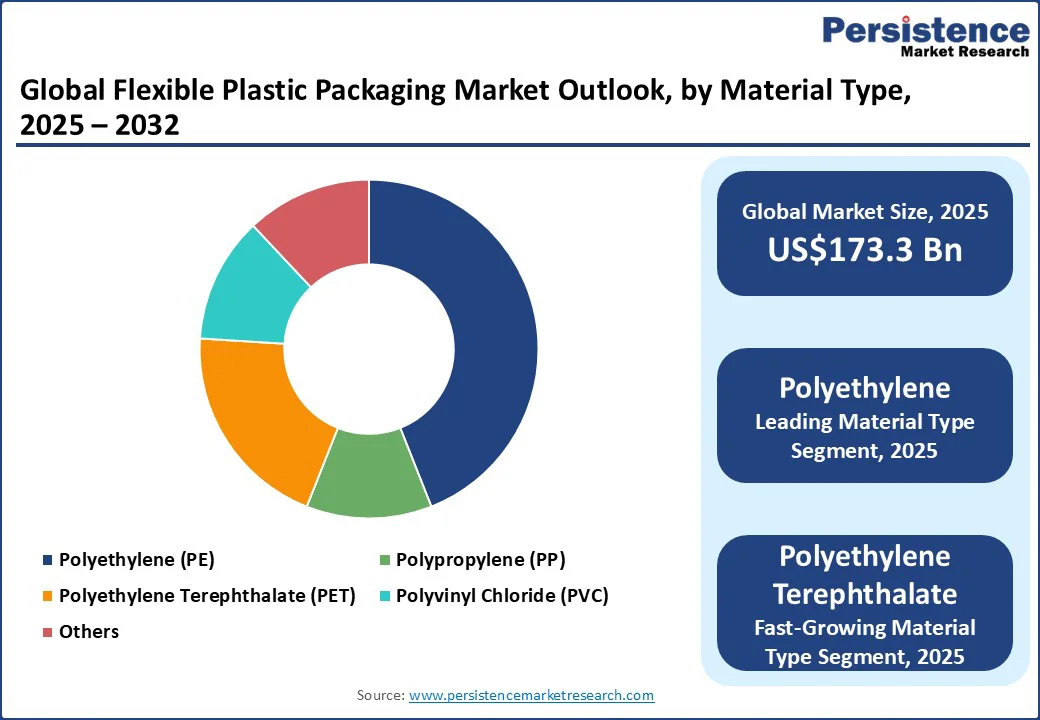

The global flexible plastic packaging market size is likely to be valued at US$173.3 Bn in 2025 and is expected to reach US$258.8 Bn by 2032, growing at a CAGR of 5.9% during the forecast period from 2025 to 2032, driven by increasing consumer demand for convenience, including single-serve packaging and on-the-go consumption. Additionally, the continued expansion of e-commerce is broadening the need for protective yet cost-effective packaging formats, further fueling market demand.

Key Industry Highlights:

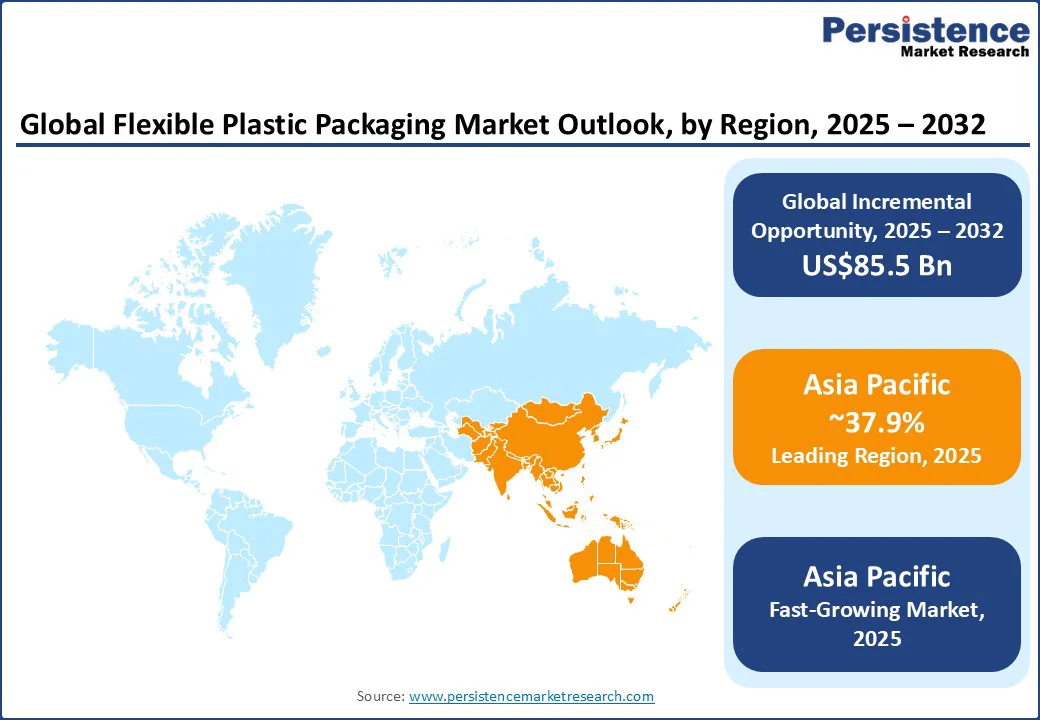

- Leading Region: Asia Pacific, with a market share of approximately 37.9%, driven by high demand in China and rapid industrialization across the region.

- Fastest-growing Region: Asia Pacific is showing rapid growth, due to urbanization, the expanding food processing sector, and increasing adoption of sustainable packaging solutions.

- Investment Plans: Jindal Poly Films announced an investment of US$7.93 Mn to expand its Nashik facility for the production of BOPP, PET, and CPP films, enhancing capacity for flexible packaging in the food, beverage, and pharmaceutical sectors.

- Dominant Material Type: Polyethylene, holding around 42.8% share, favored for its versatility, moisture resistance, and compatibility with recyclable packaging initiatives.

- Leading Product Type: Pouches, capturing approximately 43% of the market, valued for convenience, portability, and adaptability across food and beverage, personal care, and pharmaceutical applications.

| Key Insights | Details |

|---|---|

|

Flexible Plastic Packaging Market Size (2025E) |

US$173.3 Bn |

|

Market Value Forecast (2032F) |

US$258.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

High-Barrier Multilayer Films and Sustainability Drive Flexible Packaging Demand

Advancements in high-barrier multilayer co-extruded films are playing a critical role in shaping demand for flexible plastic packaging. These films provide strong protection against oxygen, moisture, and UV exposure, while innovations such as antimicrobial coatings are enhancing food safety and extending shelf life. Industries including ready-to-eat meals and pharmaceuticals are increasingly adopting modified atmosphere packaging (MAP) and vacuum-sealed flexible pouches to meet stringent shelf-life requirements without relying heavily on preservatives.

The expansion of cold chain networks and e-grocery channels, especially in the Asia Pacific, is further accelerating adoption. For instance, demand for multilayer flexible packaging with more than seven layers has grown significantly, reflecting the need for high-performance and sustainable solutions in sectors with strict quality standards.

Growing emphasis on sustainability is also reshaping the market through the adoption of compostable multilayer films and monomaterial recyclable flexible plastics. Regulatory pressures, such as extended producer responsibility (EPR) laws, plastic taxes, and bans on single-use plastics, are driving packaging converters to redesign solutions that align with recyclability and end-of-life management goals.

Supply Chain Volatility and Recycling Challenges Hinder Market Stability

Volatility in the supply of high-barrier resins and specialty additives is creating uncertainty for manufacturers of flexible plastic packaging. Materials such as ethylene-vinyl alcohol (EVOH) and vinyl acetate monomer (VAM), which are essential for multilayer barrier films, remain exposed to fluctuations in petrochemical feedstocks. Disruptions in the availability of silica, antioxidants, and functional coatings further complicate consistent production schedules. These supply constraints lead to irregular performance of barrier films, which is a significant concern for food and pharmaceutical brands that depend on precise shelf-life guarantees.

The recycling inefficiency of multi-layer flexible packaging structures is another barrier to market growth. Laminates that combine PET, aluminium foil, EVOH, and adhesives deliver strong performance but create technical challenges in post-consumer recycling streams. Contamination from inks, food residues, and odorous components further reduces the quality of recycled output, making it unsuitable for high-value or food-grade applications.

Monomaterial Recyclable Films and Biodegradable Innovations Unlock New Market Potential

The shift toward monomaterial recyclable films with enhanced oxygen-barrier performance is opening new avenues for innovation in flexible plastic packaging. Industries such as food, pharmaceuticals, and personal care are increasingly prioritizing packaging solutions that fit seamlessly into existing recycling systems while maintaining the same protective properties as complex multilayer laminates.

Developments in all-PE, mono-PP, and mono-PET structures are gaining traction, as they combine recyclability with printability, moisture resistance, and seal strength. This trend is particularly attractive to brand owners who are under pressure to meet sustainability commitments without compromising product safety or shelf life. A recent example is ITP’s RecySealflex mono-PE film, which effectively replaces traditional PET/PE laminates in stand-up pouches while ensuring recyclability and high barrier functionality.

Opportunities are also expanding through the adoption of biodegradable multilayer films designed for dry goods and fresh produce packaging. Compostable and bio-based structures using PLA and PBAT are being developed to protect products while aligning with circular economy goals. These solutions are especially relevant for categories such as snacks, bakery, and fresh fruits and vegetables, where packaging performance directly impacts shelf stability and product freshness.

Retailers and consumers have shown a willingness to pay a premium for packaging that combines environmental responsibility with functional benefits, creating a profitable niche for manufacturers. Coveris’ MonoFlex Thermoform film for tortilla wraps illustrates this shift, as it replaced a PA/PE structure with a recyclable alternative that delivers the same six-month shelf life, proving the commercial viability of sustainable innovations in this market.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) is anticipated to dominate the flexible plastic packaging market, accounting for more than 42.8% share in 2025. Its leadership comes from its versatility, cost-effectiveness, and widespread use in films, laminates, and pouches. PE offers excellent moisture resistance, flexibility, and processing efficiency, making it the preferred choice across food, beverage, and household product applications. Its compatibility with mono-material packaging solutions, which support recyclability efforts, further strengthens its market position. With a well-established global supply chain, PE remains the material of choice for high-volume packaging production.

Polyethylene Terephthalate (PET) is projected to be the fastest-growing material segment through 2032. Its demand is rising due to superior clarity, strength, and barrier properties, which are essential in beverage, personal care, and premium food packaging. PET’s lightweight nature also reduces transportation costs and carbon footprint, supporting both performance and sustainability demands. Recycled PET (rPET) solutions are further accelerating adoption, as brands integrate higher percentages of recycled content into packaging.

Product Type Insights

Pouches represent the largest product category in flexible plastic packaging, holding nearly 43% of the market share in 2025. Their growth stems from their convenience, portability, and adaptability across industries such as food and beverages, pharmaceuticals, and personal care. Stand-up and spouted pouches, in particular, have gained popularity as they combine functional advantages such as resealability and extended shelf life, with strong branding potential. Their ability to reduce material usage compared to rigid packaging formats also makes them more cost-efficient and sustainable, giving them a strong edge in mass-market adoption.

Films and wraps are currently the fastest-growing product segment. The segment is benefiting from the expansion of e-commerce and logistics, where protective, lightweight, and customizable packaging is in high demand. Shrink and stretch films, for example, are increasingly used for bundling and protecting goods during transport, while specialty barrier films are expanding into food preservation and healthcare applications. With advances in printing technologies, films now also serve as effective branding surfaces, which adds marketing value. The combination of protective performance, adaptability to diverse uses, and compatibility with sustainability-driven innovations is accelerating the growth of films and wraps in the coming years.

Regional Insights

Asia Pacific Flexible Plastic Packaging Market Trends - Rapid Expansion and Eco-Friendly Adoption

Asia Pacific is projected to be the dominant and fastest-growing market for flexible plastic packaging globally, holding the largest market share at approximately 37.9%. The region is experiencing rapid growth, driven by industrialization, urbanization, a rising middle class, and the expansion of e-commerce and modern retail. China leads the region, supported by its large food and beverage industry, growing pharmaceutical sector, and increasing adoption of advanced packaging technologies.

Sustainability is a growing priority in Asia Pacific. Dow’s collaboration with Chinese detergent brand Liby to use the INNATE TF 220 Precision Packaging Resin in fully recyclable laundry detergent packages highlights the region’s push toward sustainable and circular packaging solutions. Such initiatives indicate a strong trend toward environmentally responsible packaging and demonstrate how companies are aligning material innovation with consumer expectations.

China leads the Asia Pacific market, driven by its large-scale manufacturing and rising demand for high-performance flexible packaging. Investments in sustainable production technologies and recycling initiatives are further strengthening the market.

India is emerging as the fastest-growing market in the Asia Pacific. The country’s rapid urbanization, expanding food processing sector, and evolving consumer lifestyles are driving strong demand for flexible packaging. Indian companies are increasingly focusing on recyclable and biodegradable materials, reflecting both regulatory pressures and growing consumer awareness about environmental sustainability.

North America Flexible Plastic Packaging Market - Innovation and Sustainability Driving Growth

North America remains a key player in the flexible plastic packaging market, with the U.S. driving the region’s growth. The market benefits from advanced manufacturing capabilities, strong adoption of innovative packaging technologies, and growing demand for sustainable solutions. The U.S. dominates the regional market, largely due to the mature food and beverage, pharmaceutical, and personal care sectors, which continue to rely heavily on flexible packaging for convenience, product protection, and branding.

Sustainability initiatives have become a central focus for companies in North America. Amazon, for instance, has replaced plastic air pillows with recycled paper filler in its packaging operations across the region. This move, initiated in 2024, is expected to eliminate billions of plastic air pillows annually, demonstrating a strong commitment to reducing packaging waste while promoting recyclable materials. The U.S continues to see high demand for flexible packaging solutions, particularly in food and beverage applications.

Companies are increasingly adopting recyclable materials and reducing packaging volumes to align with evolving consumer preferences and environmental regulations. Mexico is witnessing strong growth, driven by the food processing sector and increased demand for packaged goods. The country is gradually shifting toward bioplastics and recyclable materials, reflecting a broader regional trend toward sustainability.

Europe Flexible Plastic Packaging Market Trends - Regulation-Led Circular Economy Advances

Europe’s market is heavily influenced by environmental regulations and strong sustainability initiatives. The region has experienced steady growth as companies adapt to stringent EU regulations, invest in recycling technologies, and explore eco-friendly packaging alternatives. The European market is led by Germany, where flexible packaging adoption is highest in the food and beverage sector, supported by investment in energy-efficient manufacturing and recyclable materials.

Sustainability-driven developments are shaping market dynamics across the region. Amazon ceased using plastic air pillows and single-use delivery bags in its European operations, reflecting the push toward reducing plastic waste and promoting recyclable packaging solutions. Nestlé has invested in U.K.-based Impact Recycling to process hard-to-recycle flexible plastics into pellets for reuse, demonstrating the commitment of major companies to circular economy practices.

Germany remains the largest and most mature market, characterized by established infrastructure for high-quality packaging production and recycling. Spain is emerging as one of the fastest-growing markets in Europe, fueled by the increasing demand in the food and beverage sector and the adoption of sustainable packaging practices. Companies in Spain are investing in recyclable materials and innovative packaging designs to comply with the EU regulations while meeting consumer expectations.

Competitive Landscape

The global flexible plastic packaging market is highly competitive, dominated by several multinational and regional players investing heavily in innovation, sustainability, and capacity expansion. Key players such as Amcor, Sealed Air, Mondi Group, Berry Global, and Huhtamaki are focusing on developing recyclable and bio-based packaging solutions, improving barrier performance, and adopting advanced printing technologies to differentiate their offerings.

Collaborations and partnerships are common. For example, Dow worked with Liby to launch recyclable detergent packaging, highlighting the industry's shift toward circular economy initiatives. Companies are also expanding geographically, particularly in high-growth regions such as Asia Pacific, to capture the rising demand from the food, beverage, pharmaceutical, and e-commerce sectors.

Key Industry Developments:

- In June 2025, Dow introduced the INNATE TF 220 Precision Packaging Resin, a high-density polyethylene innovation designed to support the recyclability and performance of flexible plastic packaging. This resin enables the design of recyclable, high-performance biaxially oriented polyethylene (BOPE) films for flexible packaging.

- In July 2025, Jindal Poly Films Limited announced a US$7.93 Mn investment to expand its Nashik facility. The expansion will include new production lines for biaxially oriented polypropylene (BOPP), polyethylene terephthalate (PET), and cast polypropylene (CPP) films.

Companies Covered in Flexible Plastic Packaging Market

- Amcor

- Sealed Air Corporation

- Dow Inc.

- Mondi Group

- Huhtamaki Oyj

- Berry Global Inc.

- Coveris Holdings S.A.

- Constantia Flexibles

- Winpak Ltd.

- ProAmpac

- Sonoco Products Company

- Klöckner Pentaplast Group

- Mitsubishi Chemical Holdings Corporation

- RPC Group (part of Berry Global)

- Uflex Ltd.

- Jindal Poly Films Limited

- Smurfit Kappa Group

- Toray Industries, Inc.

- Plastipak Packaging, Inc.

- Evergreen Packaging

Frequently Asked Questions

The flexible plastic packaging market is estimated at US$173.3 Bn in 2025.

The flexible plastic packaging market is projected to reach US$258.8 Bn by 2032.

Sustainability and recyclable materials are key trends, alongside growth in stand-up pouches, films, and smart packaging solutions. E-commerce and food & beverage sectors continue to drive demand, while innovations such as biodegradable and circular packaging gain traction.

Polyethylene is the leading material type, holding approximately 42.8% of the market, while pouches are the leading product type with around 43% market share due to their convenience, flexibility, and compatibility with sustainable initiatives.

The flexible plastic packaging market is expected to grow at a CAGR of 5.9% from 2025 to 2032.

The top players in the flexible plastic packaging market include Amcor, Sealed Air, Dow, Mondi Group, and Huhtamaki.