- Packaging

- Flexible Intermediate Bulk Container Market

Flexible Intermediate Bulk Container Market Size, Share, and Growth Forecast 2026 - 2033

Flexible Intermediate Bulk Container Market by Product Type (Type A, Type B, Type C, Type D), Design (U-Panel, Baffle/Q-Bag, Circular, 4-Panel), End-use Industry (Food, Chemical, Pharmaceutical), and Regional Analysis, 2026 - 2033

Flexible Intermediate Bulk Container Market Size and Trends Analysis

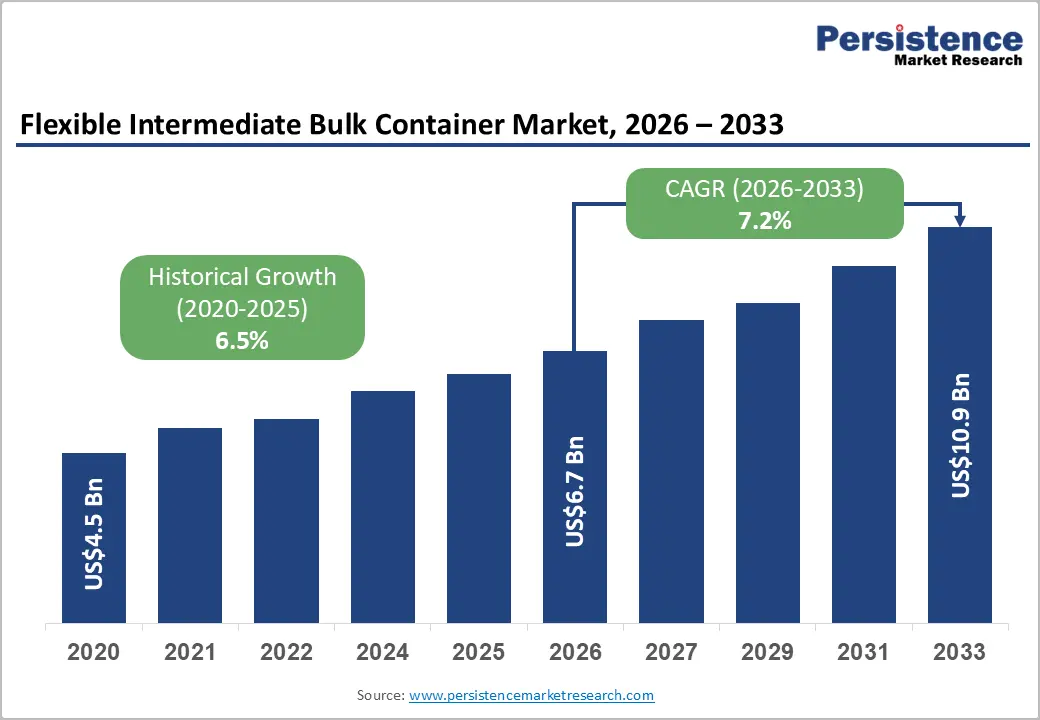

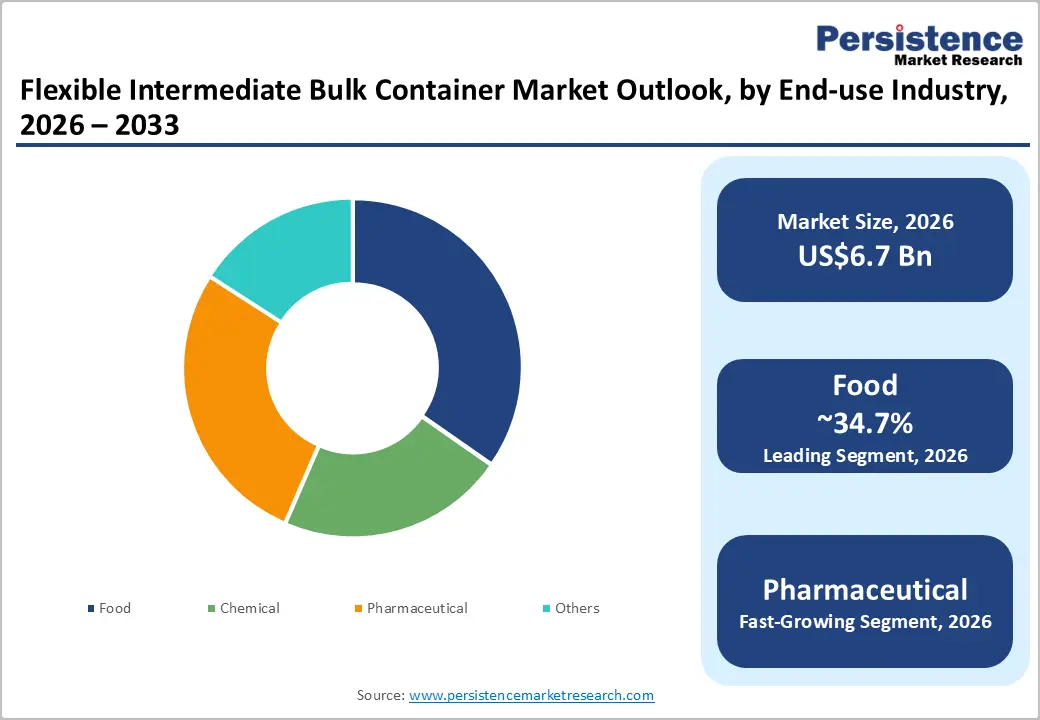

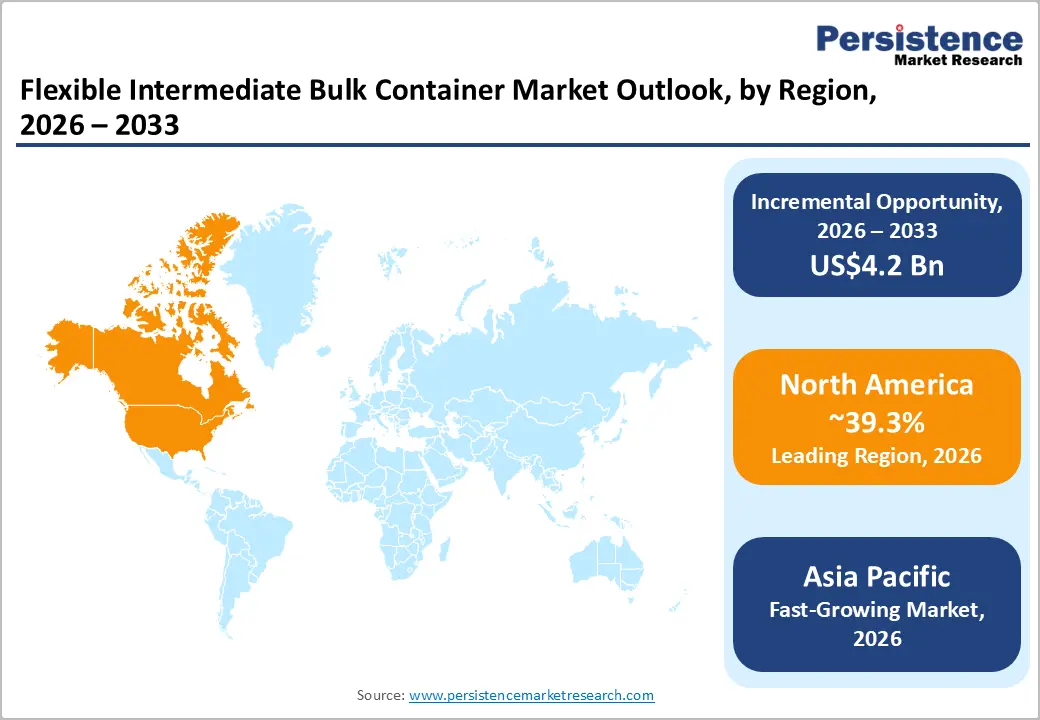

The global flexible intermediate bulk container market size is likely to be valued at US$6.7 billion in 2026 and is expected to reach US$10.9 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by rising bulk trade of agricultural commodities and chemicals and high demand for cost-efficient and lightweight packaging solutions. The market is also benefiting from the shift toward recyclable and reusable packaging materials.

Key Industry Highlights:

- Leading Product Type: Type A, approximately 67.5% share in 2026, as several industries in developing countries operate in low-risk environments where anti-static protection is not required.

- Dominant End-use Industry: Food, nearly 34.7% share in 2026, backed by large-scale global trade of grains, sugar, and processed ingredients.

- Leading Region: North America, with about 39.3% share in 2026, owing to strict safety regulations for bulk material handling and rising demand from the food processing industry.

- Fast-growing Region: Asia Pacific, spurred by rising exports of agricultural commodities and chemicals from India and China.

- Latest Agreement: In September 2025, Time Technoplast signed a Memorandum of Understanding (MoU) to acquire a 74% stake in Ebullient Packaging Pvt. Ltd., marking its entry into the flexible industrial packaging and FIBC segment. The acquisition was aimed at strengthening the company’s industrial packaging portfolio and broadening its presence in bulk packaging applications.

DRO Analysis

Driver - Rising Bulk Exports of Food and Agro Commodities

Export-scale volumes of grains, pulses, sugar, and flour are pushing buyers away from traditional sacks toward food-grade Flexible Intermediate Bulk Containers (FIBCs). The U.S. Department of Agriculture (USDA) reported that U.S. agricultural exports alone reached US$196 billion in 2023, with bulk grains and processed food requiring specialized packaging that meets international food safety standards. Beyond the U.S., produce exporters in South America and Southeast Asia now prefer food-grade FIBCs to cut per-ton freight costs.

Millers in the U.S. are retrofitting silos with bottom-spout feeds for automated flour discharge. Compliance with standards such as BRC, ISO 22000, and FDA 21 CFR 177.1520 is also tightening. The FAO estimates that 14% of global food production is lost between harvest and retail, with inadequate packaging being a significant contributing factor. Hence, making a switch to certified food-grade FIBCs is predicted to be a direct business case for exporters.

Stringent Norms for Hazardous Chemical Handling

Strict enforcement of chemical safety rules is making UN-certified and antistatic FIBCs a compliance necessity rather than an optional upgrade. Increasing regulation from the UN, EPA, and OSHA for hazardous and toxic chemical transportation is pushing demand for UN-certified FIBCs, especially in the chemical sector. For flammable powders and solvents, the requirements go further.

IEC 61340-4-4 specifies requirements for FIBCs used in hazardous explosive atmospheres, covering zones where combustible dusts or flammable gases may be present. In the U.S., NFPA 77, NFPA 652, and NFPA 654 all specify that Type B, C, and D FIBCs must be tested to and meet the requirements of IEC 61340-4-4 before use in hazardous environments. Procurement managers are switching from standard commodity sacks to certified units despite price premiums of 20 to 30%, viewing them as risk-mitigation assets that reduce downtime and insurance exposure.

Restraint - High Compliance Costs for Static-Dissipation Certification

While demand for antistatic FIBCs is rising, the cost of meeting electrostatic safety standards remains a key barrier, especially for small-scale manufacturers and buyers. Anti-static bulk bags used with flammable or explosive materials must be tested and classified per IEC 61340-4-4, which defines four types, i.e., A through D, based on electrostatic properties, each requiring specific tests for surface resistance and charge dissipation. The gap between Type C and Type D adds both cost and operational complexity.

Type C bags are cheaper but require grounding, whereas Type D bags are more expensive but eliminate the risk of human error from forgetting the ground wire. Liner compatibility adds another layer. Using a standard plastic liner inside a Type C bag can insulate the static and cause a spark, so liners must also comply with IEC 61340-4-4, classified as L1, L2, or L3. For companies selling into ATEX-rated environments, third-party test reports from accredited laboratories such as Dekra or Swissi are required to validate compliance. It adds both time and cost before a single bag reaches the customer.

Opportunity - IoT- and RFID-Enabled FIBCs to Improve Supply Chain Visibility

Embedding sensors into FIBCs is moving from pilot phase toward mainstream adoption, mainly in pharmaceutical and food logistics where traceability is now a regulatory expectation. Some manufacturers are already piloting RFID-enabled FIBCs that improve inventory management and reduce loss rates by up to 15%. More advanced versions go further. Smart FIBC solutions featuring real-time tracking, humidity sensors, and temperature-controlled bulk bags have demonstrated better control over storage conditions, lower spoilage rates, and improved supply chain visibility.

The research backing is strong too. A ScienceDirect review published in 2025 confirmed that integrating RFID with IoT sensors can evolve smart packaging into a progressive network capable of sensing environmental factors and enabling high-level interaction across systems. As food safety traceability mandates tighten globally, smart FIBCs are positioned to shift from a premium option to a procurement standard.

Recycled-Material FIBCs to Gain Impetus under Circular Economy Mandates

Sustainability regulations are creating demand for FIBCs made from recycled or low-carbon materials. The EU's Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025, aims to reduce the use of primary raw materials. It also focuses on making recycling of all EU packaging economically viable by 2030 and putting the packaging sector on track for climate neutrality by 2050. The industry is already responding.

In May 2025, Chemco Group and Kandoi Group announced a joint venture to build two greenfield FIBC manufacturing facilities in Gujarat, producing bags entirely from recycled PET. It also declared the launch of a closed-loop system covering PET bottle collection through to final fabrication. The commercial production was expected by end of 2025. Recycled-content polypropylene FIBCs are further seeing high demand as brand owners and regulators push circular-economy compliance. For exporters supplying buyers in Europe, complying with EPR frameworks is fast becoming a baseline expectation.

Category-wise Analysis

Product Type Insights

Type A FIBC bags are predicted to lead with a share of approximately 67.5% in 2026, as they are the most economical and widely used option for transporting non-flammable bulk materials such as grains, fertilizers, sand, cement, and plastic resins. These bags are made from woven polypropylene and do not require expensive anti-static technology, which keeps production costs low. Industries that operate in non-hazardous environments prefer Type A bags as they deliver high load capacity and easy customization without additional safety expenses. The construction and agriculture sectors especially rely on these bags for bulk transport due to their durability and low replacement cost.

Type D FIBC bags are estimated to be the fastest-growing product type in 2026, as industries handling combustible powders and flammable chemicals are facing strict safety regulations. These bags are designed to safely dissipate static electricity without requiring grounding connections. This reduces the risk of sparks during filling and discharge operations. Chemical, mineral, and pesticide manufacturers are mainly adopting Type D bags to lower explosion risks in hazardous environments.

End-use Industry Insights

The food segment is anticipated to dominate with a share of nearly 34.7% in 2026, as food grains, sugar, flour, starch, coffee, spices, seeds, and processed ingredients are transported in massive bulk quantities worldwide. FIBC bags simplify storage, loading, and export logistics while reducing packaging waste compared to rigid containers. Their lightweight structure also lowers freight costs for exporters and food processors. Another important factor is the increasing focus on food safety and traceability. Modern food-grade FIBC bags are manufactured under strict hygiene conditions and often include liners, UV protection, and contamination barriers.

The pharmaceutical segment is expected to remain in the second position in 2026, as drug manufacturers now require highly controlled bulk packaging systems for APIs, excipients, and specialty powders. Pharmaceutical supply chains are expanding rapidly due to rising biologics production, vaccine manufacturing, and global medicine exports. This has increased the demand for contamination-resistant and static-protective FIBCs.

Regional Insights

North America Flexible Intermediate Bulk Container Market Trends

North America is predicted to account for a share of approximately 39.3% in 2026, owing to a mature chemical supply chain, high agricultural export volumes, and strict OSHA compliance that favors high-margin certified bags. The chemical sector is the largest consumer. The U.S. Department of Commerce reported that chemical exports exceeded US$220 billion in 2023, making FIBCs essential for both domestic and international supply chains. Safety regulations have also upgraded buying behavior.

OSHA's 2024 compliance with UN GHS revision 7 raised the technical bar for containers carrying flammable powders and solvents. It has made Type C and Type D bags with conductive yarns the new standard at chemical plants, pharmaceutical mixers, and lithium-ore processors.

U.S. Flexible Intermediate Bulk Container Market Trends

The U.S. is being pulled from multiple directions at once. The pharmaceutical industry is one key driver. The surge in demand from the pharmaceutical and food industry, along with strict government regulation toward sustainable packaging, is pushing growth. Food output adds to this momentum. Regulation is also influencing procurement choices. Procurement managers are switching from commodity sacks to certified FIBCs to reduce downtime. A new growth pocket is emerging in critical minerals. The food and agriculture segment is advancing at a steady pace, catalyzed by strict water-safety and traceability codes that lean toward tamper-evident liners and HACCP-friendly printing.

Asia Pacific Flexible Intermediate Bulk Container Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026, with a share of nearly 28.5%, spurred by heavy investment in battery metal refining and broad-based manufacturing expansion. China's Baotou rare-earth hub, India's production-linked incentives, and Southeast Asia's agribusiness exports converge to lift regional orders for conductive and high-stack designs. Industrial output data confirms this trend. Vietnam's Industrial Production Index rose by 7.6% in Q1 2025, compared to 5.9% in the same period in 2024. India's IIP recorded a 5.0% YoY increase in January 2025, both indicators showcasing manufacturing momentum that supports bulk packaging demand.

China Flexible Intermediate Bulk Container Market Trends

China's FIBC demand is being spurred by its dominant position in rare earth processing and petrochemical capacity additions. The country is projected to rise at a substantial CAGR of approximately 8.3% from 2026 to 2033, making it one of the fastest-growing individual markets globally. The rare earth sector is a key demand driver. Baotou already reports 43.5 million tons of proven rare earth reserves, around 84% of China's total, with a 2024 rare earth industry output of 103.05 billion yuan. Capacity across magnetic, polishing, catalytic, and hydrogen-storage materials is approaching 300,000 tons, pointing to a near-complete local supply chain.

India Flexible Intermediate Bulk Container Market Trends

India is one of the most interesting markets. On the export side, exports of FIBC woven sacks, woven fabrics, and tarpaulin grew by 24.1% in FY2026 over the same period the previous year, with cumulative plastics and related material exports reaching US$5.8 billion in FY25. It was an 11.54% increase from FY24. Policy support is sharpening competitiveness. In 2024, the government adjusted the RoSCTL rate for FIBCs to 2.3%, a move designed to bolster the export competitiveness of domestic textile manufacturers.

Domestic consumption is also expanding swiftly. FIBC demand in India is anticipated to surge at nearly 5.8% CAGR through 2033, supported by Make in India initiatives. Packem Umasree's 2025 commissioning of a plant with 3.5 million bag capacity in Gujarat exemplifies this industrial expansion.

Europe Flexible Intermediate Bulk Container Market Trends

Europe is growing steadily, backed by sustainability mandates and rising pharmaceutical sector demand. The continent is anticipated to account for a share of approximately 17.1% in 2026. Firms such as FlexSack have introduced FIBCs made with 30% recycled polypropylene. Germany and the Netherlands are enacting regulations requiring at least 30% recycled content in industrial packaging by 2025. Nearly 5,000 tons of bio-FIBCs were shipped in Europe in 2024, providing 20% lower CO2 emissions while matching the tensile strength of virgin polypropylene.

Digital tools are also broadening the market. Greif's 2025 launch of an IBC collections app in Europe shows how digital tools facilitate the retrieval and reconditioning of used packaging, propelling customer lock-in.

U.K. Flexible Intermediate Bulk Container Market Trends

The U.K. is the fastest-growing country in Europe, spurred by its superior innovation network and forward-looking policy environment. The Plastic Packaging Tax (PPT) is pushing recycled-content FIBCs into mainstream procurement. PPT, introduced in 2024, imposes a levy of £200 (US$269.05) per ton on plastic packaging containing less than 30% recycled content, which is a direct incentive to upgrade to compliant FIBC variants. On the trade side, post-Brexit opportunities are opening new channels. The U.K. government has been keen on establishing free-trade agreements with countries such as the U.S., China, and other Asian nations, creating new avenues for FIBC players in the region.

Germany Flexible Intermediate Bulk Container Market Trends

Germany is estimated to witness steady growth owing to its pharmaceutical dominance and stringent sustainability legislation. The country is predicted to account for over 25% of share in Europe in 2026, boosted by its advanced industrial hub, novel engineering, and export-oriented economy. On packaging regulation, Germany is ahead of most EU peers. Since January 1, 2024, manufacturers in the country have been obligated to pay fees for the single-use plastics they place on the local market, as mandated by the German Environment Agency (UBA).

Competitive Landscape

The global flexible intermediate bulk container market is moderately fragmented, with a mix of multinational packaging companies, regional manufacturers, and low-cost producers. Large players such as Greif, Berry Global, LC Packaging International BV, and Rishi FIBC Solutions Pvt. Ltd. hold superior positions due to global distribution networks, product certifications, and long-term contracts with bulk exporters. However, regional companies continue gaining share through price competitiveness and speedy customization capabilities.

Competition in the market is now shifting from simple cost-based manufacturing to sustainability-led innovation. Manufacturers are investing in recyclable polypropylene, reusable bulk bags, anti-static materials, UV-resistant coatings, and food-grade contamination control systems to meet strict packaging regulations in Europe and North America. India-based firms have become particularly influential in the export market owing to their expandability and cost advantage.

Key Industry Developments:

- In April 2026, Mitsu Chem Plast announced its entry into the Intermediate Bulk Container (IBC) segment with plans to establish a fully automated manufacturing facility expected to become operational by FY2026-27. The company stated that the plant would use integrated blow molding and assembly systems to improve production efficiency and consistency.

- In February 2026, manufacturers in Madhya Pradesh’s Pithampur industrial belt reported a revival in U.S. orders for polypropylene jumbo bags after reciprocal tariffs were reduced to 18%. The tariff revision improved India’s competitiveness against suppliers from Vietnam and Turkey, encouraging some companies to consider production expansion.

- In October 2025, Jumbo Bag Limited approved the acquisition of Hitech Polymers LLP, an FIBC conversion unit based in Chennai, for nearly INR 6 crore. The company also approved land leasing plans at the Gummidipudi SIPCOT Industrial Area to support future capacity expansion activities.

Companies Covered in Flexible Intermediate Bulk Container Market

- Greif

- Halsted Corporation

- Langston Bag

- IPG

- Palmetto Industries International Inc.

- Commercial Syn Bags Limited

- Codefine

- SafeFlex International Ltd.

- Dewitt

- JohnPac

- Bulk Corp International

- K-PACKING

- FORMOSA SYNTHETICS PVT. LTD.

Frequently Asked Questions

The global flexible intermediate bulk container market is projected to be valued at US$6.7 billion in 2026.

The flexible intermediate bulk container market is expected to reach US$10.9 billion by 2033.

Key market trends include the shift toward recyclable and reusable FIBCs and increasing automation in bulk packaging systems.

Type A is expected to be the leading product type with a share of nearly 67.5% in 2026, as it is cost-effective and widely used for transporting non-flammable bulk goods.

The flexible intermediate bulk container market is expected to grow at a CAGR of 7.2% from 2026 to 2033.

Greif, Halsted Corporation, Langston Bag, and IPG are a few key market players.