- Home Appliances

- Flexible Display TV Market

Flexible Display TV Market Size, Share, and Growth Forecast 2026 - 2033

Flexible Display TV Market by Product Type (Rollable TVs, Foldable OLED TVs, Bendable / Curvable TVs, Others), by Display Technology (Flexible OLED, AMOLED, Micro-LED on flexible substrate), by Screen Size (50–65 inches, 66–75 inches, Above 75 inches), by Distribution Channel (Online, Offline), by Regional Analysis, 2026-2033

Flexible Display TV Market Size and Trend Analysis

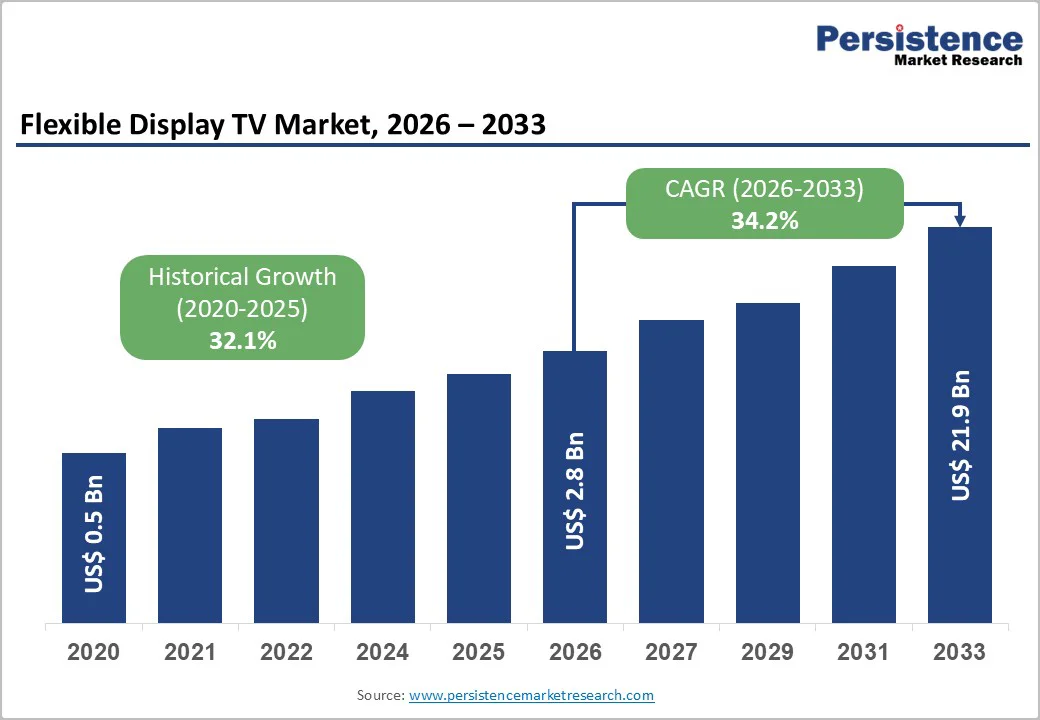

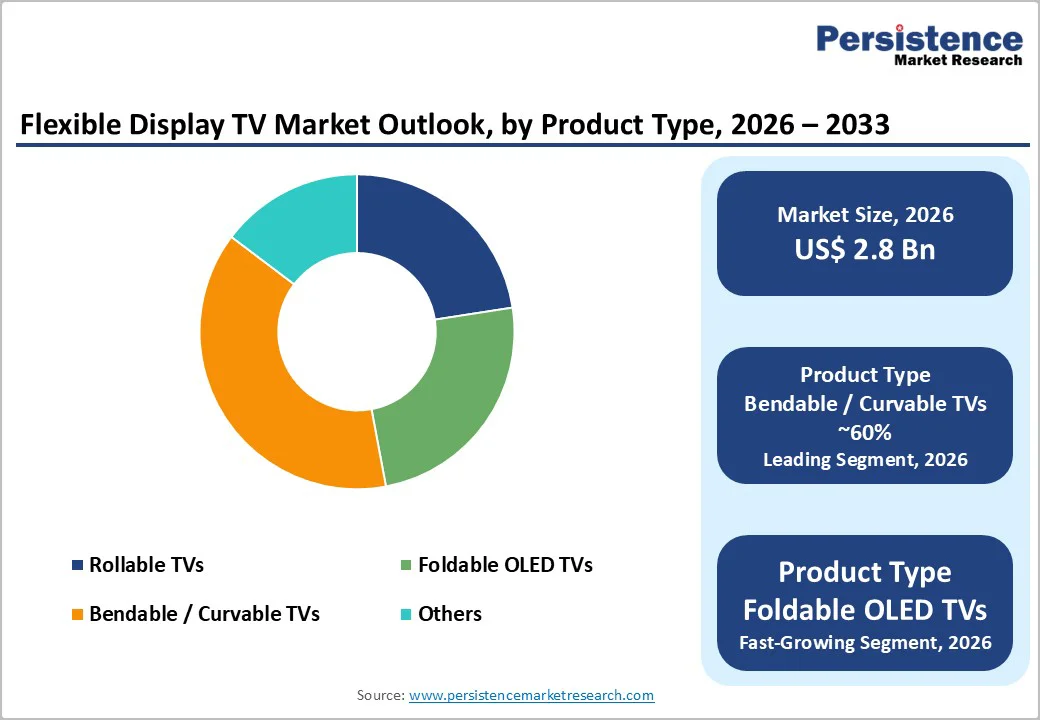

The global Flexible Display TV market size is likely to be valued at US$2.8 billion in 2026 and is expected to reach US$21.9 billion by 2033, growing at a CAGR of 34.2% during the forecast period from 2026 and 2033. The market is poised for exponential growth driven by the maturation of next-generation manufacturing processes, specifically inkjet-printed OLED technologies, which are significantly lowering production barriers.

As consumer preferences shift toward "lifestyle-integrated" electronics that blend seamlessly with modern interiors, the demand for form factors that can hide, retract, or reshape, such as rollable and bendable televisions, is intensifying. This growth is further supported by the spillover of flexible display advancements from the automotive and smartphone sectors, enhancing yield rates and durability for larger panels.

Key Market highlights

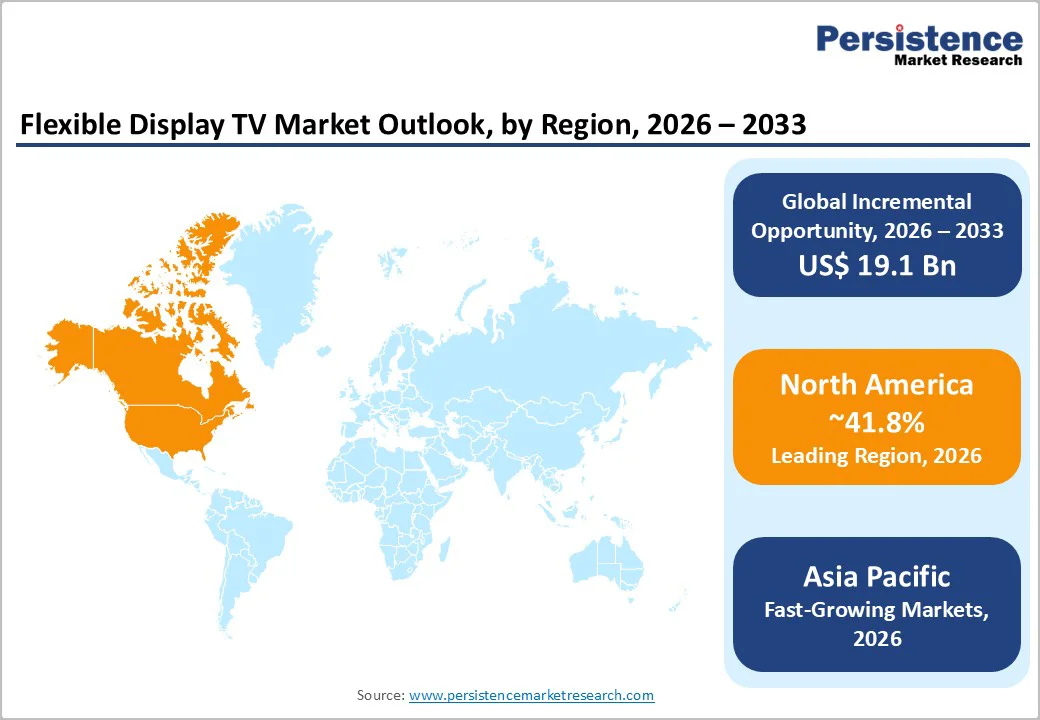

- Leading Region: North America leads the market, accounting for about 41.8% of global revenues, driven by high disposable income and strong luxury smart-home adoption.

- Fastest-Growing Region: Asia Pacific is expanding fastest, already representing roughly 38.2% of global market share, supported by strong manufacturing ecosystems and rapid commercialization.

- Dominant Technology Segment: Flexible OLED remains the technology leader, capturing around 75% market share due to superior image quality and mature supply chains.

- Fastest-Growing Product Segment: Bendable / Curvable TVs dominate adoption with about 60% market share, expanding rapidly on the back of premium gaming and immersive viewing demand.

- Key Market Opportunity: Automotive integration is emerging as a major secondary revenue stream, enabling broader deployment of flexible panels and helping amortize R&D costs across markets.

| Key Insights | Details |

|---|---|

| Flexible Display TV Market Size (2026E) | US$ 2.8 Bn |

| Market Value Forecast (2033F) | US$ 21.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 34.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 32.1% |

Market Dynamics

Market Growth Drivers

Advancements in Inkjet-Printed OLED Manufacturing Enabling Scalable Flexible Panels

The shift from evaporation-based OLED production to inkjet-printed processes is reshaping cost structures for large flexible displays. By digitally depositing emissive materials onto substrates similar to printing on paper, manufacturers dramatically reduce material waste and lower production complexity. Companies such as TCL CSOT are proving that this approach improves manufacturing efficiency while enabling broader format flexibility.

As production yields stabilize and defect rates decline, inkjet printing unlocks economically viable large-format panels. This reduces the premium associated with flexible TVs, opening availability beyond ultra-luxury buyers to affluent mass-market consumers. With new production lines coming online, supply capacity is expected to expand rapidly, accelerating commercialization timelines and directly supporting faster adoption across residential and premium entertainment environments.

Growing Consumer Preference for Convertible, Disappearing Displays in Modern Living Spaces

Urban lifestyles, shrinking home sizes, and minimalist interior trends are fueling interest in electronics that recede when not in active use. Rollable and retractable flexible TVs eliminate the permanent “black mirror” aesthetic of traditional screens, preserving visual openness in high-end living rooms. This aligns closely with the rise of smart homes, which seamlessly blend technology into architectural design.

Luxury real estate developers and interior designers increasingly specify flexible TVs as statement features that add functionality without visual clutter. The ability to reveal or hide entertainment systems on demand creates emotional value, enhances design continuity, and supports premium positioning. As consumers seek adaptable spaces that transform between work, leisure, and socializing, flexible display TVs become an aspirational, space-optimizing upgrade.

Market Restraints

High Upfront Pricing and Complex Manufacturing Economics Limiting Mainstream Adoption

Even with steady advances in production, the cost of building flexible-display TVs remains substantially higher than that of conventional models. Multi-layer encapsulation systems, sophisticated backplane architectures, and moisture-resistant barriers add significant fabrication complexity. Early market launches, such as the LG Signature OLED R, priced near US$100,000, demonstrated how elevated price ceilings immediately confined demand to ultra-premium buyers and design-centric luxury installations.

High-performance polyimide substrates, precision-engineered rolling or hinge assemblies, and stringent quality control further increase production expenses. As a result, average selling prices remain well above mass-market expectations. These economic factors slow category diffusion, extend replacement cycles, and delay flexible TVs from reaching the adoption trajectory previously achieved by flat-panel OLEDs and LCD televisions.

Concerns Over Long-Term Durability, Reliability, and Mechanical Wear

Flexible display TVs must repeatedly roll, bend, or retract without compromising image quality, a requirement that introduces significant reliability uncertainty. Consumers express hesitation over potential crease formation, panel distortion, or failures in motorized mechanisms after years of routine use. These perceptions are amplified because televisions are expected to remain functional far longer than smartphones or tablets.

Unlike mobile devices with replacement cycles of 2 to 3 years, TVs typically remain installed for 7 to 10 years. Ensuring that organic layers, thin-film transistors, and mechanical components endure thousands of deformation cycles without pixel degradation or structural fatigue remains a critical engineering challenge. Until proven longevity becomes widely demonstrated, durability skepticism will continue to constrain broad consumer acceptance.

Market Opportunities

Integration of Flexible TVs With Gaming, Productivity, and Hybrid Work Lifestyles

Bendable and adjustable-curve displays unlock a compelling dual-purpose proposition: they can operate flat for productivity tasks and transform into curved formats for immersive gaming. This adaptability resonates with users who want a single screen to manage entertainment, work, and creative workflows. As remote work becomes normalized, large-format flexible displays evolve from living-room appliances into multi-functional digital workspaces tailored to changing daily needs.

Manufacturers can position bendable TVs as high-performance, professional-grade monitors that also deliver premium gaming experiences. Adjustable curvature settings, including aggressive options like 900R, enable personalized ergonomics and visual immersion unavailable on rigid monitors. This creates a differentiated, high-margin niche within the gaming and workstation ecosystem, expanding revenue beyond traditional TV buyers.

Extending Flexible Display Technology Into Automotive and Semi-Outdoor Environments

Flexible TV innovations are increasingly transferable to new use cases, including luxury vehicles and semi-outdoor entertainment areas. As autonomous features advance, vehicle cabins are evolving into leisure-oriented spaces, with retractable, roll-out displays enhancing entertainment, navigation, and passenger comfort. Rollable screens integrated into dashboards, ceilings, or seatbacks offer space-efficient formats that disappear when not required.

Designing flexible displays to withstand heat fluctuations, vibration, glare, and durability standards creates strong synergy with automotive OEM requirements. At the same time, weather-resistant semi-outdoor installations, such as patios, yachts, and hospitality venues, open additional premium channels. Sharing R&D and component platforms across home entertainment and mobility applications allows manufacturers to spread development costs, accelerate commercialization, and unlock broader profitability opportunities.

Category-wise Insights

Product Type Analysis

Bendable / Curvable TVs currently dominate the market, accounting for about 60% of total sales. Their leadership stems from simpler mechanics compared with fully rollable models, resulting in lower production risk and better pricing. Products such as LG OLED Flex demonstrate how adjustable curvature delivers immersive gaming benefits while staying technically feasible and commercially scalable, unlike complex retractable architectures.

The fastest-growing category is rollable TVs, driven by strong consumer fascination with displays that disappear when not in use. Premium homeowners and luxury interior designers view rollable screens as design-centered technology rather than traditional appliances. As form factors shrink into cabinets and consoles, rollable models are rapidly gaining traction as aspirational upgrades for high-end living environments and prestige smart homes.

Display Technology Analysis

Flexible OLED remains the clear technology leader, representing roughly 75% of total market value. Its self-emissive architecture eliminates the need for backlighting, enabling ultra-thin, lightweight designs that bend without structural stress. With mature supply ecosystems led by Samsung Display and LG Display, OLED delivers superior reliability, deep blacks, and premium cinematic contrast that aligns perfectly with the luxury positioning of flexible televisions.

The fastest-growing technology segment is microLED-based flexible prototypes and hybrid approaches. Although still emerging, they promise exceptional brightness, durability, and energy efficiency compared with conventional panels. Manufacturers and research labs are increasingly investing in micro-scale packaging and flexible substrates, positioning this technology as the next evolution for ultra-premium, long-life flexible displays across both residential and commercial deployment scenarios.

Screen Size Analysis

The 50–65 inch range leads the market with an estimated 45% share. It strikes the optimal balance between immersive viewing, manageable production costs, and acceptable defect rates for flexible substrates. These sizes also integrate seamlessly into standard living rooms and cabinetry systems, allowing manufacturers to address mainstream replacement demand while minimizing structural complexity and installation challenges for homeowners.

The fastest-growing segment is above 65 inches, driven by luxury buyers seeking cinematic experiences at home. As materials, yield rates, and mechanical designs improve, manufacturers are experimenting with larger flexible panels for statement installations. These displays increasingly target high-end villas, media rooms, and designer interiors, where visual impact and architectural integration carry more value than compact footprint or affordability.

Distribution Channel Analysis

Offline retail remains dominant with approximately 65% market share. Because flexible TVs are expensive and unfamiliar, buyers prefer hands-on demonstrations before committing. Experience centers and flagship electronics stores allow customers to see rolling, bending, and retracting mechanisms firsthand, helping address concerns about longevity, reliability, and price justification, making physical retail essential to purchase decision-making.

The fastest-growing channel is online and direct-to-consumer digital sales. As awareness improves and product videos showcase real usage, consumers are increasingly comfortable configuring premium purchases through brand portals. Manufacturers benefit from richer data, controlled storytelling, virtual demos, and bundled installation packages, all of which support gradual migration toward digital-first purchasing without compromising reassurance or service quality.

Regional Insights

North America Flexible Display TV Market Trends

North America remains the leading regional market, accounting for an estimated 41.8% share of global revenues. High-income households, strong luxury home-theater culture, and an established custom-installation ecosystem position flexible TVs as both status symbols and architectural design tools. U.S. integrators and CEDIA-aligned installers play a central role in embedding rollable and hidden displays into premium smart homes.

Growing enthusiasm for bendable gaming displays complements this trend, supported by high discretionary spending on gaming hardware and content. Although regional energy-efficiency standards remain strict, ultra-premium devices face less pricing pressure from compliance requirements. This allows brands to emphasize performance, aesthetics, and exclusivity rather than affordability, reinforcing North America’s leadership during the early commercialization phase of flexible display televisions.

Europe Flexible Display TV Market Trends

Europe follows as a sophisticated demand center driven by design-conscious consumers and a strong appreciation for industrial aesthetics. Trade fairs such as IFA Berlin amplify interest as manufacturers showcase prototypes and concept models aligned with European taste for refined interiors. Flexible TVs appeal particularly in urban homes, where rollable units preserve visual harmony without occupying permanent wall space.

The region’s regulatory environment is shaping product engineering in unique ways. “Right to Repair” policies and sustainability expectations are pushing manufacturers to create modular, serviceable mechanical components. As these repairable architectures mature, Europe is projected to grow at a steady CAGR of about 36.9%, supported by premium adoption, eco-design mandates, and gradual replacement of high-end OLED installations.

Asia Pacific Flexible Display TV Market Trends

Asia Pacific is the fastest-growing region, holding an estimated 38.2% share and serving as the global manufacturing nucleus for flexible displays. South Korea and China anchor the ecosystem, housing leaders such as Samsung Display, LG Display, BOE, and TCL CSOT. Regional control over substrates, panel fabrication, and component logistics significantly lowers production costs and accelerates technology scaling.

China’s domestic brands, including Hisense and Skyworth, are intensifying competition by introducing comparatively affordable flexible models. Government incentives for advanced display manufacturing and rapid progress in inkjet-printed OLED lines are expanding local capacity. As production efficiencies improve, Asia Pacific is positioned to democratize flexible TVs faster than Western markets, spreading availability across emerging ASEAN economies and premium metropolitan households alike.

Competitive Landscape

The market remains highly consolidated, dominated by a few vertically integrated manufacturers that control advanced panel technology and core intellectual property. High capital costs, complex production processes, and tight supply chains create significant entry barriers, keeping competition limited and margins closely guarded.

However, competitive dynamics are gradually evolving as newer participants invest in next-generation fabrication lines and push innovation beyond novelty concepts. Strategies are shifting toward functional versatility, durability, and repairability, with intensified R&D focused on extending material lifetimes, strengthening mechanical components, and minimizing warranty risks, ultimately aiming to make flexible displays more reliable, scalable, and commercially viable.

Key Market Developments

- In May 2025, TCL CSOT showcased its 65-inch Inkjet Printed OLED TV at Display Week, demonstrating a production process that reduces material costs by 20% compared to traditional evaporation methods.

- In May 2024, LG Electronics reportedly halted the production of its Signature OLED R rollable TV to realign resources toward transparent and bendable OLED displays, marking a strategic pivot in its flexible portfolio.

- In August 2025, Samsung Electronics unveiled its "Micro RGB" TV lineup, a transitional technology bridging the gap to full Micro-LED, offering flexible-grade backlighting modules intended for future curved large-format displays.

Companies Covered in Flexible Display TV Market

- LG Display

- Samsung Display

- BOE Technology Group

- Sony Corporation

- TCL Electronics

- Visionox Technology

- Sharp Corporation

- Hisense Group

- Skyworth Group

- Vizio Inc.

- Konka Group

- Philips (TP Vision)

- AU Optronics

- China Star Optoelectronics

Royole Corporation

Frequently Asked Questions

The global market is projected to reach a value of US$ 21.9 Billion by the end of 2033, growing significantly from its 2026 valuation.

Key drivers include the adoption of inkjet-printed OLED manufacturing, which lowers costs, and the rising consumer preference for "hidden" or aesthetic-focused electronics in smart homes.

The Bendable / Curvable TVs segment currently leads the market with 60% market share, as these devices offer practical versatility for both cinematic viewing and high-performance gaming.

North America is the dominant region with 41.8% market share, driven by early adoption of premium electronics and a strong market for luxury custom home installations.

A major opportunity exists in leveraging flexible display technology for automotive interiors, creating cross-industry revenue streams that support the development of consumer TV panels.

Major companies include LG Display, Samsung Display, BOE Technology Group, TCL Electronics, and Skyworth Group, among others.