- Metals & Minerals

- Flexible Copper Foil Market

Flexible Copper Foil Market Size, Share, and Growth Forecast 2026 - 2033

Flexible Copper Foil Market by Thickness (Below 10µm, 10-20µm, 20-50µm, Above 50µm), Application (Circuit Boards, Batteries, Solar & Renewable Energy, Medical, Other), and Regional Analysis for 2026-2033

Flexible Copper Foil Market Size and Trend Analysis

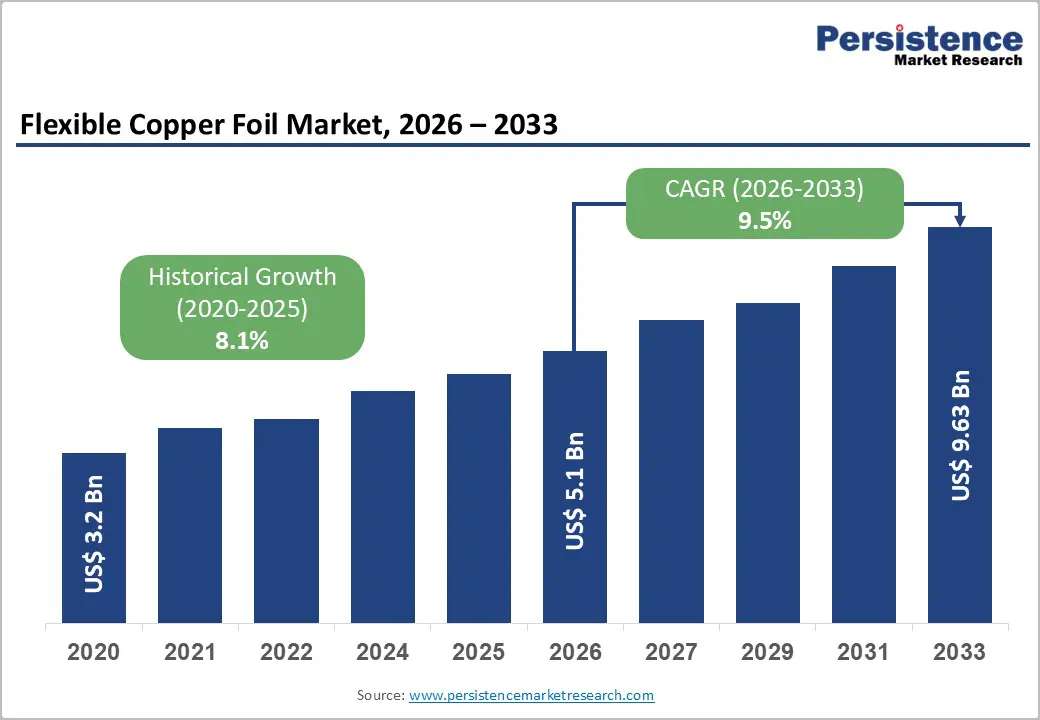

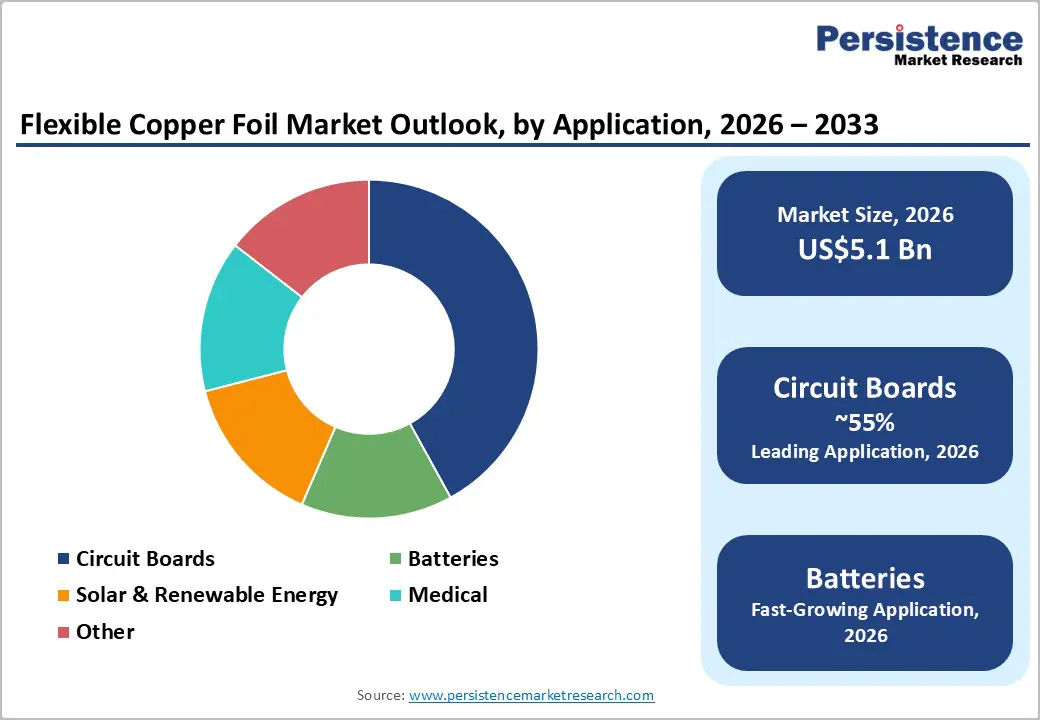

The global Flexible Copper Foil market size is supposed to be valued at US$ 5.1 Bn in 2026 and is projected to reach US$ 9.6 Bn by 2033, growing at a CAGR of 9.5% between 2026 and 2033.

The flexible copper foil market is experiencing substantial growth, primarily driven by the rapid expansion of the electric vehicle industry and the increasing deployment of renewable energy technologies. The global transition toward transportation electrification, with electric vehicle sales projected to exceed 30 million units by 2030, is generating significant demand for high-performance lithium-ion batteries, where copper foil serves as a critical anode current collector.

Key Market Highlights

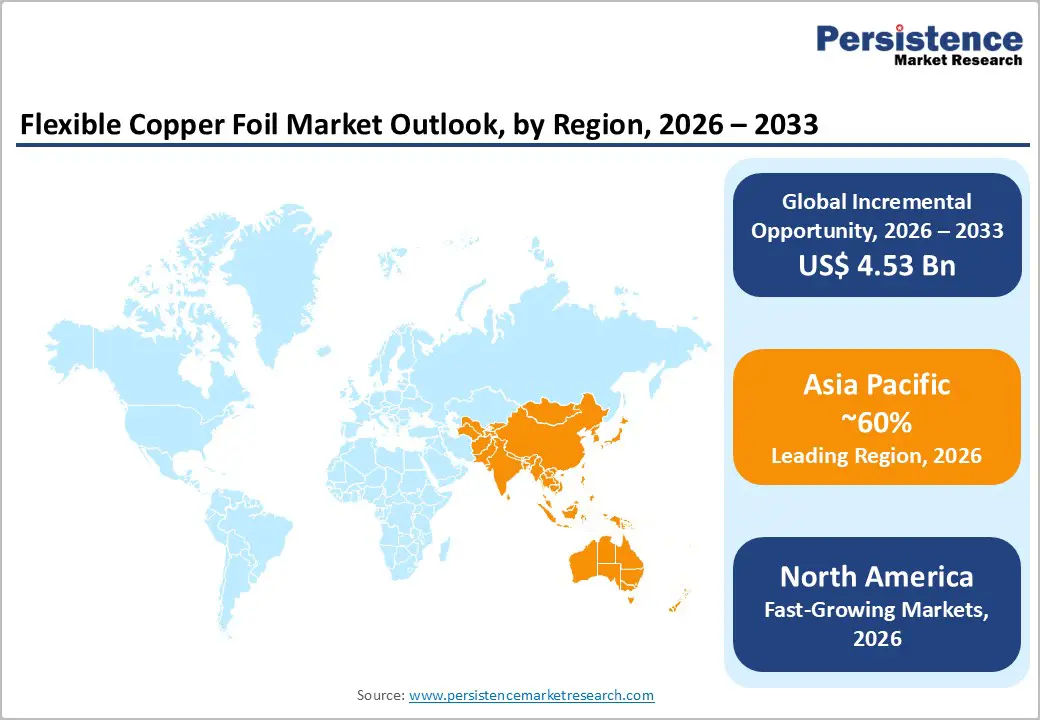

- Leading Region: Asia Pacific dominates flexible copper foil production and consumption with over 60% of global market volume, driven by China's manufacturing scale, Japan's technological leadership, and South Korea's battery production expertise supporting accelerated electric vehicle electrification across the region.

- Fastest Growing Region: North America is experiencing the most rapid regional growth, fueled by electric vehicle battery gigafactory investments, government incentives under the Inflation Reduction Act, and strategic localization of battery material production by international manufacturers establishing North American supply chains

- Dominant Segment: The below 10-micrometer thickness segment dominates flexible copper foil applications, accounting for approximately 45% of market value, reflecting industry-wide miniaturization trends in battery technology and consumer electronics requiring ultra-thin, high-performance foil materials.

- Fastest Growing Segment: Circuit board applications for 5G telecommunications infrastructure and artificial intelligence data centers represent the fastest-growing demand segment, driven by the accelerating deployment of next-generation communication networks requiring high-frequency PCBs with specialized copper foil components.

- Key Market Opportunity: Solid-state battery technology commercialization represents a transformational market opportunity, with major automotive manufacturers planning production launches during 2027-2030, requiring specialized nickel-plated copper foil and creating premium-priced segments for innovative foil manufacturers.

| Key Insights | Details |

|---|---|

| Flexible Copper Foil Market Size (2026E) | US$ 5.1 Bn |

| Market Value Forecast (2033F) | US$ 9.6 Bn |

| Projected Growth CAGR (2026-2033) | 9.5% |

| Historical Market Growth (2020-2025) | 8.1% |

Market Dynamics

Market Growth Drivers

Electric Vehicle Electrification and Battery Demand Expansion

The global electric vehicle market is the primary catalyst for flexible copper foil demand. In 2024, EV battery consumption exceeded 750 GWh, reflecting a 40% increase from 2022, with projections indicating continued growth throughout the decade. Copper foil functions as a critical anode current collector in lithium-ion batteries, comprising approximately 10–13% of battery cell mass and 8–10% of total battery cost. Each electric vehicle requires several kilograms of specialized copper foil to ensure optimal performance.

Advancements in battery energy density are driving manufacturers to develop ultra-thin foils that enhance efficiency without compromising durability. Government incentive programs, including the Inflation Reduction Act in the United States and similar initiatives across Europe and Asia, are accelerating EV production, with leading automakers establishing gigafactories to secure sustained demand for battery-grade copper foil.

5G Infrastructure Deployment and High-Frequency Electronics Demand

The deployment of 5G networks and the rapid expansion of Internet of Things (IoT) applications are significantly increasing demand for high-performance printed circuit boards (PCBs) incorporating flexible copper foil. Telecommunications providers, smartphone manufacturers, and data center operators require advanced PCBs offering superior conductivity and signal integrity to support next-generation communication infrastructure. In response, copper foil manufacturers have introduced specialized solutions such as high-volume low-profile (HVLP) foils and nano-structured variants designed to minimize signal loss and thermal degradation at elevated frequencies.

Additionally, the growing prevalence of smart devices, artificial intelligence servers, and edge computing systems continues to broaden the market for flexible copper foil across consumer electronics and industrial automation sectors worldwide, reinforcing its strategic importance in advanced electronic applications.

Market Restraints

High Production Costs and Manufacturing Complexity

The production of flexible copper foil, particularly ultra-thin variants below 10 micrometers, requires sophisticated electrodeposition technology and precision manufacturing processes that result in elevated production costs. Manufacturing ultra-thin copper foils demands advanced equipment, specialized expertise, and stringent quality control protocols to achieve consistent thickness and surface characteristics required by battery manufacturers and high-frequency circuit board producers.

The cost differential between standard copper foil and specialty grades remains significant, creating barriers to adoption for cost-sensitive applications and limiting market penetration in price-conscious segments. Manufacturers investing in capacity expansion face substantial capital expenditures, and economies of scale remain limited as markets develop, placing upward pressure on production costs that manufacturers must manage through process innovations and supply chain optimization.

Raw Material Price Volatility and Supply Chain Risks

Copper prices exhibit significant volatility in response to macroeconomic factors, geopolitical events, and shifts in global supply dynamics, creating uncertainty for copper foil manufacturers planning long-term production strategies. Mining disruptions, such as those experienced at major operations like Grasberg, can rapidly constrain raw material supplies and elevate input costs across the industry.

Exchange rate fluctuations significantly impact profitability for manufacturers with operations spanning multiple countries, as demonstrated by recent inventory valuation losses reported by Lotte Energy Materials during periods of currency volatility. Supply chain concentration in specific geographic regions, particularly the reliance on Asian production capacity for the majority of global copper foil output, creates systemic risks that can disrupt delivery timelines and increase production costs during periods of market stress.

Market Opportunities

Solid-State Battery Technology and Next-Generation Energy Storage Solutions

Solid-state battery technology represents a transformative opportunity for flexible copper foil manufacturers, as these advanced energy storage systems require specialized copper foil with enhanced adhesion properties and compatibility with new electrolyte systems. Lotte Energy Materials has recently developed nickel-plated copper foil specifically engineered for solid-state battery applications, demonstrating market recognition of this emerging opportunity.

Solid-state batteries promise significantly higher energy density, faster charging capabilities, and improved thermal stability compared to conventional lithium-ion designs, positioning them as the critical enabling technology for next-generation electric vehicles with extended driving ranges. The commercialization timeline for solid-state batteries is accelerating, with major automotive OEMs and battery manufacturers planning production launches in the 2027-2030 timeframe, creating immediate opportunities for foil suppliers to develop and qualify specialized products for this rapidly expanding segment.

Flexible and Wearable Electronics Miniaturization Trend

The consumer electronics industry is experiencing an accelerating trend toward flexible, wearable, and implantable devices that require specialized copper foil components capable of maintaining conductivity and reliability through repeated bending and mechanical stress. Medical device manufacturers are increasingly incorporating flexible copper foil in portable diagnostic equipment such as ultrasound devices and wearable ECG patches, while consumer electronics companies are developing foldable smartphones and augmented reality glasses that depend on flexible circuit technology.

The healthcare sector represents a particularly high-value opportunity, with flexible copper foil enabling miniaturized implantable medical devices, glucose monitoring systems, and continuous health monitoring wearables that generate premium pricing compared to standard applications. Industry projections indicate that flexible electronics applications will represent one of the fastest-growing segments, driven by technological advances that enable ultra-thin foils below 6 micrometers and innovations in surface treatments that enhance adhesion to flexible substrates.

Category-wise Insights

Thickness Analysis

The below 10 µm thickness segment holds a dominant position in the flexible copper foil market, representing approximately 45% of the total market value. This leadership reflects the industry’s strong emphasis on miniaturization and weight reduction in advanced electronic devices. Ultra-thin copper foils within this range are indispensable for high-performance applications in electric vehicle batteries, enabling superior energy density and faster charge and discharge cycles essential for extended driving ranges.

Manufacturing foils below 10 micrometers is highly complex and technologically advanced, with only a limited number of producers capable of consistent large-scale output. This exclusivity provides significant competitive advantages to leading companies such as Mitsui Mining & Smelting, Circuit Foil Luxembourg, and Iljin Materials. Market demand for ultra-thin foils is growing at a CAGR exceeding 10%, outpacing standard thickness categories.

Application Analysis

The circuit boards application segment accounts for the largest share of flexible copper foil consumption, representing approximately 42% of total demand. This dominance is driven by the global requirement for advanced printed circuit boards (PCBs) across consumer electronics, telecommunications, and industrial automation. PCB manufacturers demand copper foil with precise specifications for thickness uniformity, surface roughness, and adhesion to enable multilayer boards with increasingly fine trace geometries.

The transition to 5G infrastructure and the growth of artificial intelligence server deployments have significantly increased demand for high-frequency PCBs utilizing specialized copper foils that minimize signal loss and thermal degradation. Leading manufacturers, including Furukawa Electric, Mitsui Mining & Smelting, and Fukuda Metal Foil & Powder, have expanded capacity, with Mitsui announcing a 45% increase for its VSP™ electro-deposited copper foil designed for high-frequency applications.

Regional Insights

North America Flexible Copper Foil Trends

North America is experiencing rapid growth in flexible copper foil demand, driven by substantial investments in battery gigafactories and the development of integrated electric vehicle supply chains. The Inflation Reduction Act has spurred multi-billion-dollar capital investments in battery manufacturing facilities across the United States and Canada, with major companies such as Tesla, General Motors, and Panasonic establishing large-scale operations requiring reliable supplies of high-quality copper foil.

Lotte Energy Materials has secured exclusive contracts with StarPlus Energy for a 33 GWh battery plant, with annual copper foil requirements estimated between 16,500 and 19,800 tons. Regional production localization reflects strategic efforts to reduce reliance on Asian suppliers and leverage government incentives. Volta Energy Solutions and Redwood Materials are investing heavily in domestic copper foil manufacturing, marking a significant shift in supply chain architecture.

Europe Flexible Copper Foil Trends

Europe is emerging as a key growth market for flexible copper foil, driven by stringent European Union policies promoting renewable energy adoption and electric vehicle deployment to meet climate objectives. Countries such as Germany, France, the United Kingdom, and Spain have implemented aggressive carbon reduction targets, accelerating demand for battery materials and specialty copper foils.

Germany, as the region’s largest manufacturing hub, has positioned itself as a leader in high-performance copper foil production, supported by advanced engineering capabilities and strong OEM partnerships. EU regulatory harmonization and circular economy directives encourage sustainable production and recycling initiatives, exemplified by Circuit Foil Luxembourg’s dedicated battery copper foil facility in Hungary. Additionally, Europe’s expanding battery cell ecosystem and investments in 5G infrastructure are creating diversified demand beyond automotive applications, reinforcing the region’s strategic importance.

Asia Pacific Flexible Copper Foil Trends

Asia Pacific dominates global flexible copper foil production and consumption, accounting for over 60% of total market volume, supported by its robust electronics manufacturing ecosystem and leadership in electric vehicle battery production. China maintains unmatched dominance, with an annual production capacity of approximately 400,000 tons and full integration across the value chain from raw material processing to finished products. Leading battery manufacturers such as CATL and BYD drive sustained demand for high-quality copper foil, reinforcing regional competitiveness.

Japan and South Korea remain critical hubs, with companies like Mitsui Mining & Smelting, Furukawa Electric, and Iljin Materials operating advanced facilities. Iljin has pioneered ultra-thin foils as thin as 1.5 micrometers for semiconductor packaging, while South Korea’s Lotte Energy Materials focuses on next-generation PCB applications. India is emerging, with Hindalco investing ?800 crore in a major copper foil facility in Gujarat.

Competitive Landscape

Market Structure Analysis

The flexible copper foil market demonstrates a moderately consolidated structure characterized by significant entry barriers and technical differentiation between established leaders and emerging competitors. The top three global manufacturers, Mitsui Mining & Smelting, Furukawa Electric, and JX Nippon Mining & Metals, maintain dominant positions through integrated production capabilities, decades of technological expertise, and strong relationships with major OEMs in the automotive and electronics sectors. Market consolidation reflects the capital-intensive nature of advanced facilities, requiring substantial investments in electro-deposition and rolling technologies to meet stringent specifications. Leading players are expanding capacity, with Mitsui increasing VSP™ foil output by 45% to 840 tons monthly, while competitors invest in R&D for ultra-thin foils and specialized surface treatments. Meanwhile, emerging firms in South Korea, Taiwan, and China are intensifying competition through aggressive capacity expansion and innovation in specialty grades.

Key Market Developments

September 2024: Lotte Energy Materials Corp. of South Korea signed a strategic memorandum of understanding with Isu Petasys to supply hyper-very-low-profile copper foil specifically engineered for artificial intelligence and network-focused PCBs, addressing accelerating demand from data center operators and semiconductor manufacturers requiring high-performance materials for next-generation computing infrastructure.

September 2024: Hindalco Industries announced the commencement of copper foil production for lithium-ion batteries at a new manufacturing facility in Vadodara, Gujarat, supported by capital investment of Rs 800 crore and representing India's largest specialized copper foil production capacity, strengthening regional supply chain resilience and supporting EV manufacturing growth.

September 2024: Londian Wason, an electrolytic copper foil producer, signed a strategic memorandum of understanding with Asas Panorama to establish a high-end copper foil production project in the Malaysia-China Kuantan Industrial Park (MCKIP), focusing on electrolytic copper foil for EV batteries and copper-clad laminates, marking the company's expansion into global markets.

Top Companies in the Flexible Copper Foil Market

Mitsui Mining & Smelting Co., Ltd. (Tokyo, Japan) is a leading global manufacturer with over 70 years of copper foil production expertise, commanding significant market share through its VSP™ electro-deposited copper foil product line designed for high-frequency circuit boards and advanced battery applications. The company operates integrated production facilities across multiple geographies, including Taiwan, Malaysia, and Japan, enabling global supply chain flexibility and customer responsiveness for major automotive and electronics manufacturers worldwide

Furukawa Electric Co., Ltd. (Tokyo, Japan) represents a diversified industrial manufacturer with extensive experience in copper products, fiber optics, and automotive components, leveraging technological expertise developed across multiple industry segments to produce specialized copper foils for printed circuit boards and emerging flexible electronics applications. The company maintains strong customer relationships with tier-one automotive suppliers and consumer electronics manufacturers, supporting sustained demand growth across its product portfolio.

JX Nippon Mining & Metals Corporation (Tokyo, Japan) operates as a comprehensive mining, smelting, and refining company with dedicated copper foil production capabilities serving battery manufacturers, circuit board producers, and renewable energy infrastructure projects. The company's vertically integrated operations spanning raw material processing through final product manufacturing enable superior cost management and supply chain security, supporting competitive positioning in both standard and specialty product segments.

Companies Covered in Flexible Copper Foil Market

- Mitsui Mining & Smelting Co., Ltd.

- Furukawa Electric Co., Ltd.

- JX Nippon Mining & Metals Corporation

- Fukuda Metal Foil & Powder Co., Ltd.

- Circuit Foil Luxembourg S.A.

- LS Mtron Ltd.

- Iljin Materials Co., Ltd.

- Chang Chun Group

- Doosan Corporation Electro-Materials

- Lingbao

- Lotte Energy Materials

Frequently Asked Questions

The global flexible copper foil market is projected to reach US$ 9.6 billion by 2033, growing from US$ 5.1 billion in 2026 at a CAGR of 9.5%, driven primarily by expanding electric vehicle battery production and renewable energy infrastructure deployment across developed and emerging markets.

The primary demand for drivers includes accelerated electric vehicle electrification with global EV sales projected to exceed 30 million units by 2030, expansion of 5G telecommunications infrastructure requiring advanced printed circuit boards, and proliferation of Internet of Things and artificial intelligence applications demanding high-performance electronic components.

The below 10-micrometer thickness segment dominates the market, commanding approximately 45% of total value, because ultra-thin copper foils enable superior energy density and faster charge-discharge cycles essential for next-generation electric vehicle batteries while supporting miniaturization requirements in consumer electronics and wearable device applications.

Asia Pacific dominates the global market with over 60% of worldwide production and consumption, driven by China's manufacturing scale with production capacity exceeding 400,000 tons annually, Japan's technological leadership in advanced foil production, and South Korea's battery manufacturing dominance.

Solid-state battery technology commercialization represents a transformational market opportunity, with major automotive manufacturers planning production launches during 2027-2030, requiring specialized nickel-plated copper foil with enhanced adhesion properties and compatibility with new electrolyte systems, creating premium-priced market segments for innovative manufacturers.

Market leaders Mitsui Mining & Smelting, Furukawa Electric, and JX Nippon Mining & Metals maintain dominant positions through integrated production capabilities, decades of technological development, established OEM relationships, and the capacity to produce ultra-thin foils below 10 micrometers, while South Korean competitors like Iljin Materials and Lotte Energy Materials are challenging through innovation in specialty grades and strategic capacity expansion.