- Beverages

- Wine Market

Wine Market Size, Share, and Growth Forecast, 2025 - 2032

Wine Market By Product Type (Red, White, Rosé, Dessert, Sparkling), Price Range (Below US$5, US$5 to US$10, US$10 to US$15, Above US$15), Distribution Channel (On-trade, Off-trade), and Regional Analysis for 2025 - 2032

Wine Market Size and Trends Analysis

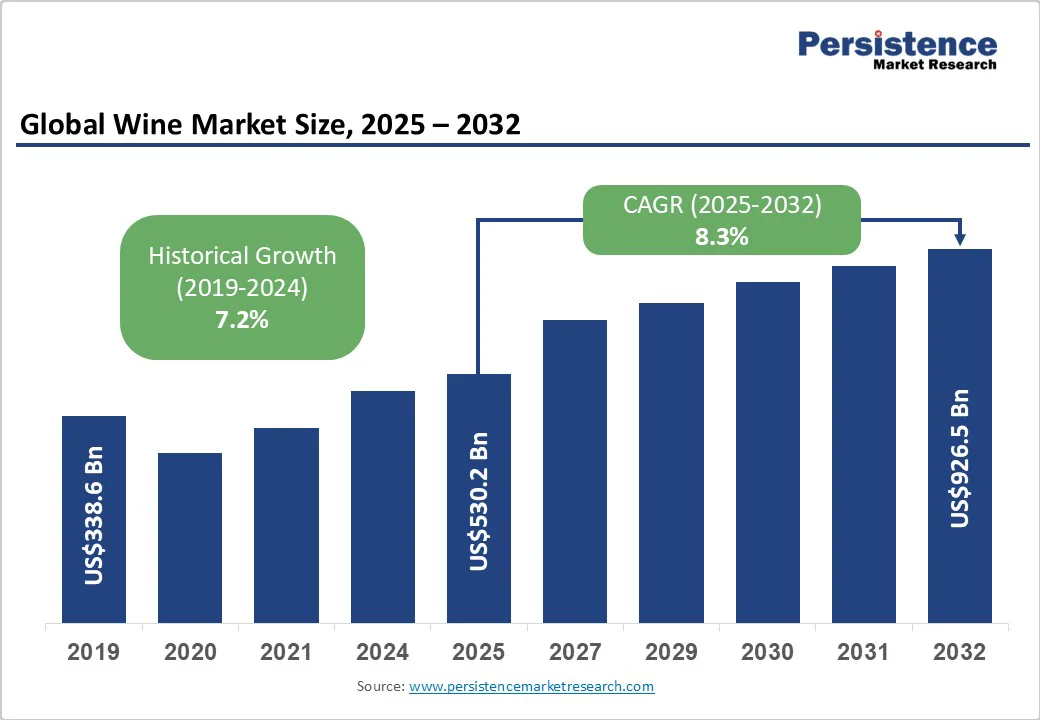

The global wine market is expected to be valued at US$530.2 billion by 2025. It is estimated to reach US$926.5 billion in 2032, growing at a CAGR of 8.3% during the forecast period of 2025 - 2032, driven by the increasing willingness of modern consumers to invest in premium products with authentic stories.

In response, leading wine producers are focusing on innovations such as single-vineyard labels and the revival of heritage grape varieties.

Key Industry Highlights

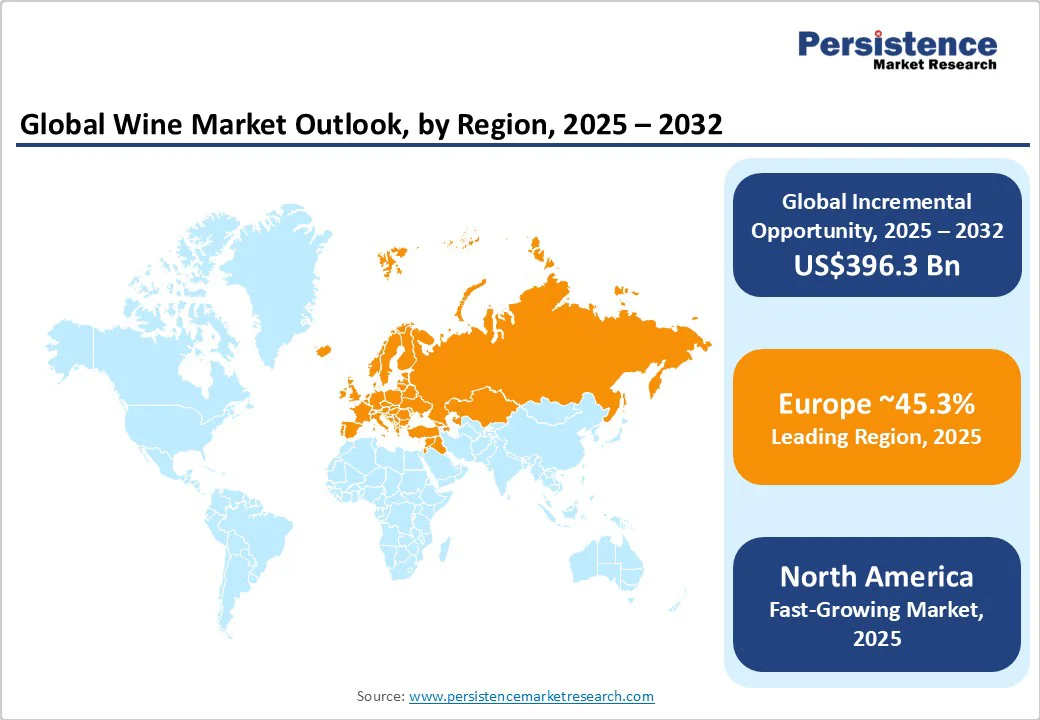

- Leading Region: Europe, with about 45.3% share in 2025, owing to its heritage wine regions and global reputation for premium varietals.

- Fastest-growing Region: North America, backed by rising interest in premium and low-alcohol wines.

- New Product Launch: Cleveland is one of 11 cities where Hall Wines will launch the latest vintage of its 2022 Kathryn Hall Cabernet Sauvignon.

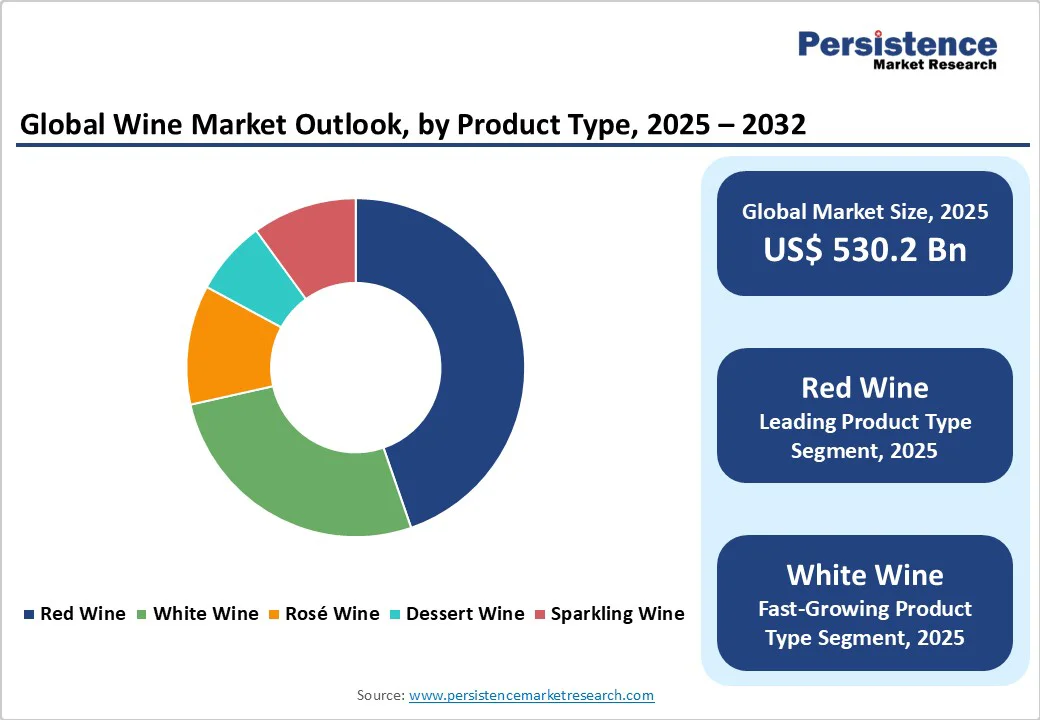

- Leading Product Type: Red wine holds nearly 44.7% share in 2025, spurred by its perceived sophistication and rich flavor profile.

- Dominant Price Range: US$5 to US$10, approximately 33.6% of the wine market share in 2025, as it attracts value-conscious and experimental consumers.

- Key Distribution Channel: The off-trade channel recorded a 76.4% share in 2025, due to its ability to provide convenience, affordability, and wide availability.

| Key Insights | Details |

|---|---|

| Wine Market Size (2025E) | US$530.2 Bn |

| Market Value Forecast (2032F) | US$926.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sophisticated and Health-linked Choice

Wine continues to enjoy a cultural positioning as a sophisticated beverage associated with social occasions and perceived wellness benefits. Unlike spirits or beer, it carries associations with elegance, moderation, and even longevity. The French Paradox continues to shape attitudes, with red wine often associated with heart health when consumed in moderation.

In recent years, brands have leveraged this image by highlighting antioxidants like resveratrol and promoting balanced drinking messages. For example, wellness-oriented campaigns in Europe emphasize wine as part of a mindful lifestyle, rather than as a symbol of excess. This combination of prestige and health perception ensures wine remains aspirational across both established and emerging consumer groups.

Low-alcohol, Organic, and Natural Alternatives

A rising base of health-conscious and environmentally aware drinkers is fueling demand for wines that are light and less industrial. Low- and zero-alcohol wines are no longer viewed as compromise products. E. & J. Gallo and Treasury Wine Estates have recently expanded their alcohol-free lines, signaling the scale of opportunity.

Organic and biodynamic wines further appeal to consumers who want minimal additives and greater transparency in production. The surge of natural wine bars across London, Melbourne, and Tokyo reflects the growing mainstream acceptance of this once-niche movement. Together, these shifts redefine wine as part of a conscious lifestyle rather than just a celebratory indulgence.

Premium Wines with Authentic Stories

Today’s wine drinkers are looking beyond the bottle. They want a narrative that adds depth to their purchase. Wines tied to heritage estates, single-vineyard expressions, or unique terroirs resonate because they connect consumers to authenticity. Storytelling around family-owned wineries, centuries-old traditions, or unique practices is proving just as important as taste.

For instance, 19 Crimes has built its success in the U.S. by combining approachable wines with bold narratives printed on labels, turning bottles into conversation pieces. This trend is prompting consumers to spend more on premium labels that convey a sense of meaning, making storytelling a direct driver of value creation.

Barrier Analysis - Health Risks from Long-term Alcohol Intake

Despite wine’s sophisticated image, increasing awareness of the health risks associated with chronic alcohol consumption is restraining market growth. Scientific studies consistently link long-term drinking to certain cancers, including breast, liver, and colorectal cancers.

Public health campaigns in Europe, North America, and Australia are highlighting these risks, influencing cautious consumer behavior. For instance, the U.K.’s 2024 updated guidelines recommend strict limits on alcohol consumption, directly affecting wine consumption patterns.

Calorie Content and Weight Management Concerns

Wine’s calorie content is increasingly viewed as a barrier, especially among health-conscious and young consumers. A standard glass of wine contains empty calories, which provide energy without essential nutrients and can contribute to weight gain if not balanced with a healthy diet and regular exercise.

Brands such as Skinnygirl and Barefoot have capitalized on this trend by delivering reduced-calorie options, while traditional producers face pressure to reformulate or market more responsibly. For several consumers, the perception that wine may hinder weight management can limit regular consumption.

Opportunity Analysis - Rediscovering Local and Indigenous Grapes

There is a surging interest in wines produced from native grape varieties as consumers seek unique flavors and authentic regional experiences. This trend allows small producers to differentiate themselves from mass-market international varietals.

For example, Spain’s revival of indigenous grapes such as Mencía and Bobal has attracted attention in export markets, while Italy’s lesser-known Nero d’Avola and Aglianico are gaining international recognition for their distinct profiles. In the U.S., some California wineries are experimenting with heritage grapes from early immigrant plantings to appeal to wine enthusiasts looking for novelty.

Unique Packaging with Cans and Boxes

Convenience-driven formats, such as cans and boxes, are changing wine consumption, particularly among urban consumers. These formats allow on-the-go consumption, reduce packaging costs, and appeal to casual or outdoor occasions.

For instance, Australia’s McGuigan Wines and the U.S. brand Underwood have popularized canned wines for festivals and picnics. Premium boxed wines in Europe are also being marketed as eco-friendly alternatives with extended shelf life. Such packaging developments open new distribution channels, including convenience stores, online subscriptions, and sporting events.

Premiumization Pushing Willingness to Pay More

Consumers are willing to trade volume for quality, creating opportunities for wineries to raise pricing and provide premium ranges. The rise of single-vineyard labels, limited-edition blends, and wines with superior storytelling allows brands to tap into the aspirations of buyers.

For example, Napa Valley’s 2025 release of ultra-premium Cabernet Sauvignon and Italy’s boutique Super-Tuscan labels are embracing heritage, terroir, and limited production to justify their high price points. Premiumization not only boosts margins but also improves brand perception.

Category-wise Analysis

Product Type Insights

Red wine is predicted to hold nearly 44.7% of the market share in 2025, due to its superior cultural association with tradition, health, and aging potential. Several consumers view red wine as a ‘serious’ choice tied to heritage and sophistication, especially in Europe, where Bordeaux, Rioja, and Chianti have historic prestige. Studies linking moderate red wine consumption with heart benefits continue to influence buying, specifically among middle-aged drinkers.

White wine is gaining impetus as consumer habits shift toward light, fresh, and versatile beverages. Its crisp profile makes it easier to pair with diverse cuisines, which is mainly appealing in cosmopolitan markets such as Singapore and Tokyo, where fusion dining is popular. Young drinkers are gravitating toward approachable styles, including Sauvignon Blanc and Pinot Grigio. The growth of sparkling white wines such as Prosecco and English sparkling has added further momentum.

Price Range Insights

Wines in the US$5 to US$10 range are poised to account for approximately 33.6% of the market share in 2025, as they strike a balance between affordability and casual drinking occasions. Young consumers and value-driven buyers utilize this tier for experimentation, often selecting easy-drinking reds, whites, or canned formats at supermarkets and convenience stores. Brands such as Barefoot and Yellow Tail continue to dominate this segment by providing consistent quality at entry-level prices.

Wines priced between US$10 and US$15 are seeing notable growth as an accessible premium option. Consumers seeking better varietal expression or sustainably produced bottles often find them here. For instance, Josh Cellars and 19 Crimes have built powerful loyalty in this segment by combining storytelling, packaging appeal, and slightly better quality.

Distribution Channel Insights

The off-trade is expected to hold a share of around 76.4% in 2025, owing to its ability to provide convenience, affordability, and widespread access. Supermarkets, liquor stores, and e-commerce platforms allow consumers to stock up for home drinking occasions, which have surged since the pandemic normalized at-home socializing. In the U.S., chains such as Costco and Trader Joe’s have turned private-label wines into cult favorites, while platforms like Drizly and Vivino make discovery and doorstep delivery effortless.

The on-trade is experiencing decent growth as restaurants, bars, and hotels rebound, making wine a central part of the dining experience. Young consumers, who may not buy premium bottles for home, are willing to explore high-quality wines by the glass in social settings. Sommeliers and curated wine lists are helping niche varietals gain traction, while wine-based cocktails and sparkling options are broadening appeal.

Regional Insights

Europe Wine Market Trends

In 2025, Europe is predicted to account for approximately 45.3% of the market share. The region’s wine scenario is in a phase of balancing heritage with modern shifts. Traditional powerhouses such as France, Italy, and Spain still dominate premium exports, but they are being challenged by consumer shifts toward organic and biodynamic labels. For example, France saw record growth in organic vineyard acreage in 2024, signaling how sustainability is changing competitive positioning.

Climate change is altering production zones. Warm regions in Spain and southern Italy are struggling with droughts, pushing wineries to test heat-resistant grape varieties. Cool regions such as England and Belgium are emerging as surprising producers of sparkling wine. English sparkling wine has gained international recognition, with producers such as Nyetimber and Chapel Down expanding exports across Europe.

North America Wine Market Trends

North America’s market for wines is undergoing a transformation propelled by shifting consumer behavior and regional dynamics. California, historically the anchor of U.S. wine production, is now grappling with climate-related pressures, prompting winemakers to experiment with drought-resistant grapes and relocate sourcing to cool northern regions, including Oregon and Washington. In Canada, British Columbia’s Okanagan Valley has gained visibility, with producers broadening exports after international awards in 2024.

Consumer preferences are leaning toward Premiumization, but in small volumes. Young demographics are drinking less but opting for high-quality or more distinctive wines, often organic or natural. The no- and low-alcohol wine category is gaining traction, highlighted by E. & J. Gallo’s expansion of its NOLO portfolio in 2025 to tap into health-conscious buyers.

Asia Pacific Wine Market Trends

Asia Pacific is expanding steadily but unevenly, influenced by cultural shifts and rising local production. China remains at the forefront, yet consumer tastes are changing. Premium imports such as French Bordeaux and Australian Shiraz still matter, but there is a visible shift toward light styles and sparkling wines. In 2024, Penfolds launched a Made in China wine using Ningxia grapes, signaling how global brands are localizing to stay relevant.

Japan and South Korea are seeing considerable growth in natural, low-intervention, and low-alcohol wines, often tied to urban millennials who associate these with health and lifestyle. Portable formats such as small bottles and canned wines are popular in Tokyo’s retail chains and convenience stores, reflecting a shift toward on-the-go consumption. India is emerging as a production hub with wineries such as Sula and Fratelli broadening their portfolios and pushing exports.

Competitive Landscape

The global wine market is characterized by big-brand consolidation and portfolio reshuffles. Large producers are offloading or buying brands to focus on high-margin lines while regional and new-world players push faster into premium niches.

The June 2025 sale of several Constellation brands to The Wine Group is a good example of incumbents refocusing and mid-sized players scaling up via merger and acquisition. Wineries that master DTC e-commerce, subscription/club models, and data-driven CRM outperform peers who rely on distributor/retailer channels.

Business Strategies

Wine producers are focusing on premium products, cost-efficient vineyard management, and expansion into emerging markets. Market leaders differentiate through superior DTC channels, sustainability credentials, and diversified portfolios, including low- and no-alcohol wines. Emerging trends include subscription-based models, experiential tourism, and cross-category collaborations that appeal to young, health-conscious consumers.

Key Industry Developments

- In September 2025, Avril Lavigne launched Complicated, a limited-edition Pinot Noir created in partnership with California’s Banshee Wines, part of Foley Family Wines & Spirits. It is a light, velvety Pinot Noir layered with bright cherry and raspberry, retailing at US$30.

- In August 2025, Sula Vineyards introduced Sula Muscat Blanc, India’s first aromatic, low-alcohol still white wine. Made from 100% Muscat grapes, this light-bodied wine provides delicate notes of citrus, lychee, and rose petals.

Companies Covered in Wine Market

- E. & J. Gallo Winery

- Treasury Wine Estates

- Constellation Brands, Inc.

- The Wine Group

- Pernod Ricard SA

- Bronco Company

- Accolade Wines

- Banfi Vintners

- Jackson Family Wines

- Henkell Freixenet

- Vina Concha y Toro S.A.

- Beijing Yanjing Beer Group Co.

- Castel Freres

- Concha Y Toro

Frequently Asked Questions

The wine market is projected to reach US$530.2 Billion in 2025.

Key drivers include rising consumer interest in premium wines and the growth of no- and low-alcohol offerings.

The wine market is poised to witness a CAGR of 8.3% from 2025 to 2032.

Revival of native grape varieties and the emergence of canned wines are the key market opportunities.

E. & J. Gallo Winery, Treasury Wine Estates, and Constellation Brands, Inc. are a few key market players.