- Automotive

- Vehicle Analytics Market

Vehicle Analytics Market Size, Share, and Growth Forecast, 2025 - 2032

Vehicle Analytics Market By Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), Application (Predictive Maintenance, Driver & Behavior Analysis), End-user and Regional Analysis for 2025 - 2032

Vehicle Analytics Market Size and Trends Analysis

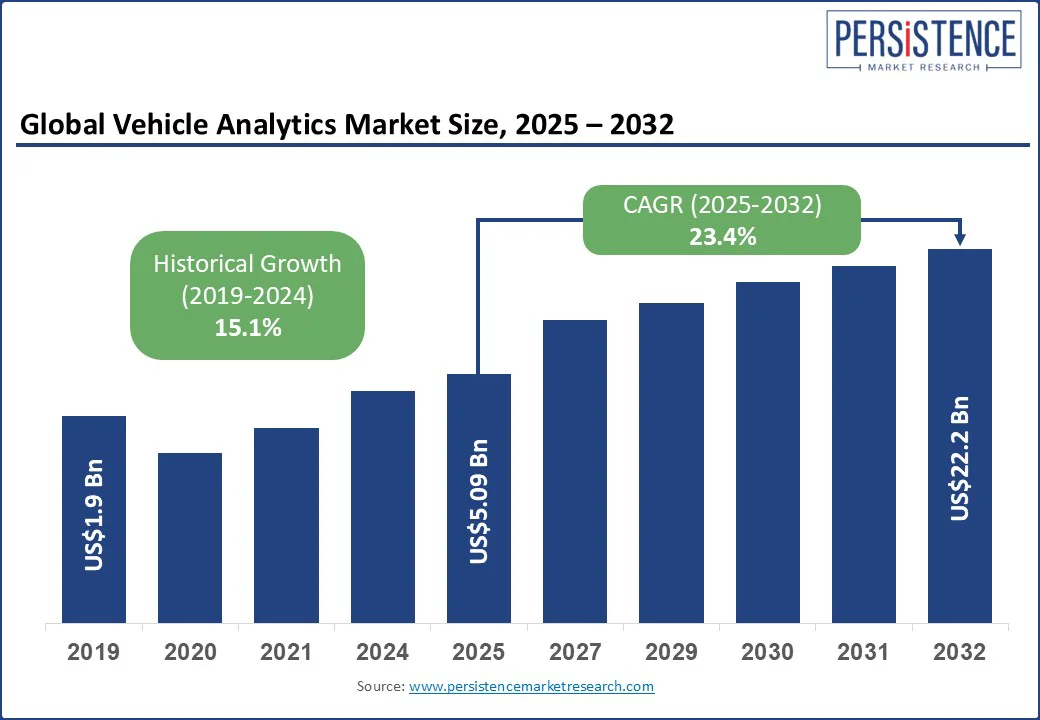

The global vehicle analytics market size is projected to rise from US$5.09 Bn in 2025 to US$22.2 Bn by 2032. It is anticipated to witness a CAGR of 23.4% during the forecast period from 2025 to 2032.

The vehicle analytics industry is witnessing rapid evolution, driven by the surge in connected vehicle technologies and the increasing integration of artificial intelligence (AI) in the automotive sector.

As modern vehicles generate vast amounts of telematics and sensor data, automotive OEMs, fleet operators, and insurers are increasingly turning to advanced vehicle analytics to extract actionable insights. These analytics enable real-time decision-making in predictive maintenance, driver behavior monitoring, traffic management, and usage-based insurance.

The demand for cloud-based deployment and AI-driven analytics platforms is accelerating, especially amid growing smart city initiatives and the rise of electric vehicles (EVs). With digital transformation reshaping the mobility landscape, vehicle analytics is becoming the core pillar in enhancing operational efficiency, road safety, and customer experience.

Key Industry Highlights:

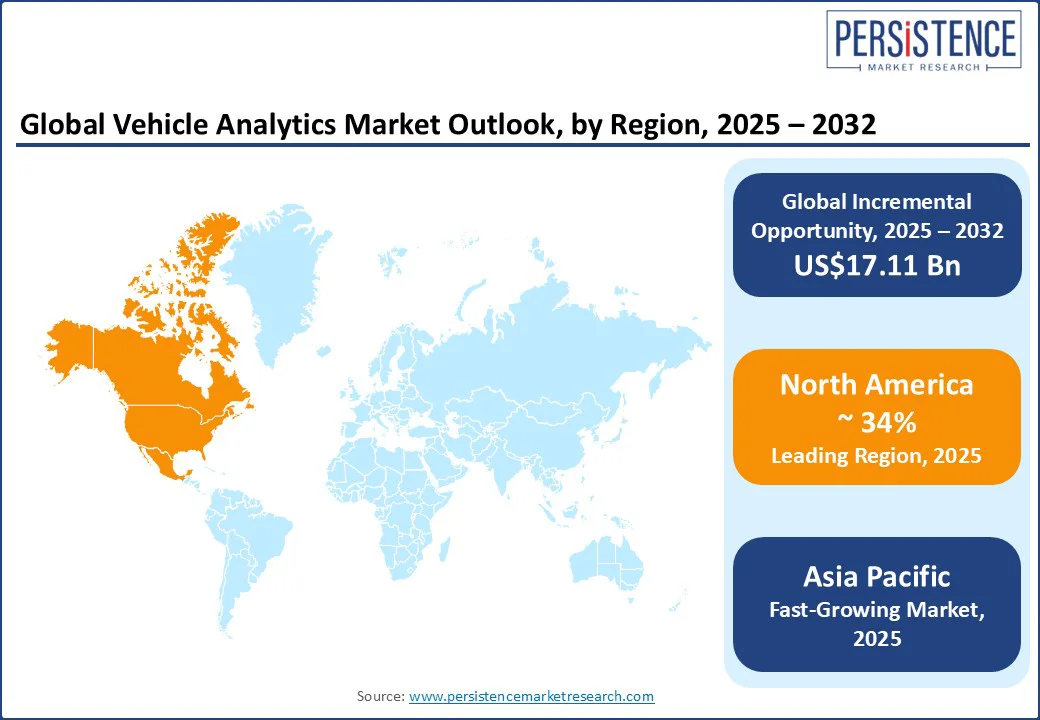

- Leading Region: North America is anticipated to be the leading region with a market share of 34% in 2025, supported by strong adoption of connected car infrastructure and growing investment in autonomous mobility ecosystems.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional segment, set to expand at the highest CAGR through 2032, fueled by major investments in EV production, telematics integration, and smart urban infrastructure in China and India.

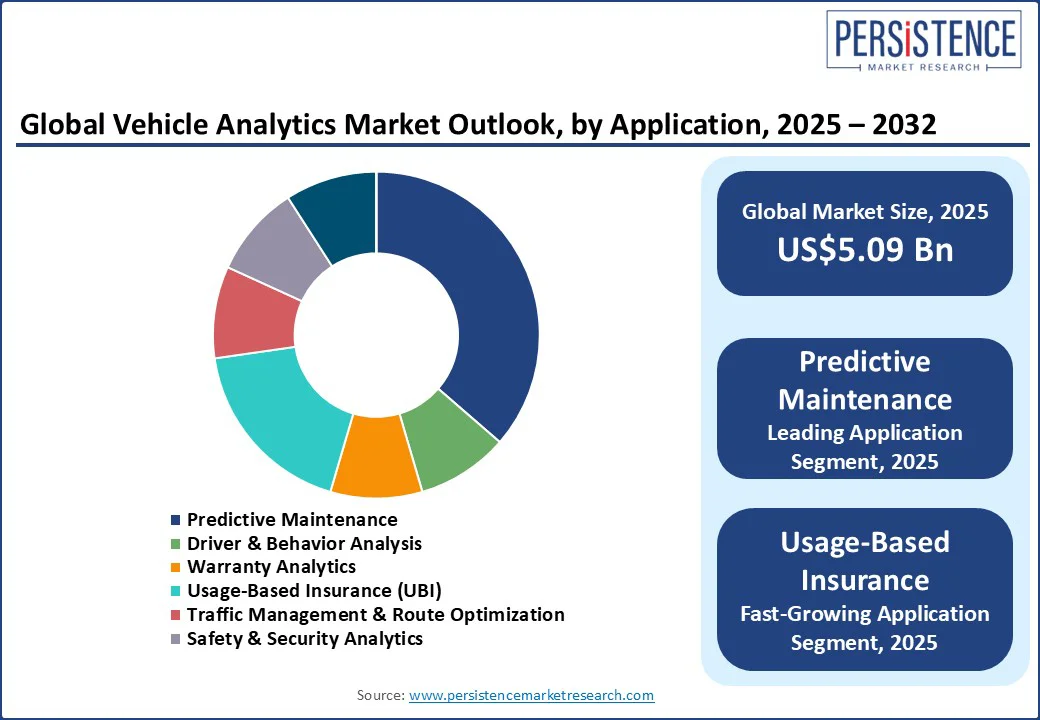

- Dominant Application: Predictive maintenance, projected to hold 40% of the total market share in 2025, leads the application segment by minimizing vehicle downtime and optimizing service cycles through real-time telematics, engine diagnostics, and AI-driven failure prediction models.

- Leading End-user: OEMs and Tier-1 suppliers dominate vehicle analytics adoption with a 39.8% market share, leveraging real-time data for design, testing, warranty management, and personalized features.

|

Global Market Attribute |

Key Insights |

|

Vehicle Analytics Market Size (2025E) |

US$ 5.09 Bn |

|

Market Value Forecast (2032F) |

US$22.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

23.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

15.1% |

Market Dynamics

Driver - Telematics & Predictive Insights Power Smarter Fleet Operations

Vehicle analytics growth is driven by connected vehicle telematics, as modern vehicles are equipped with numerous sensors that monitor engine health, braking behavior, GPS location, and environmental factors. Fleet managers and original equipment manufacturers (OEMs) deploy analytics platforms to transform raw telematics into predictive dashboards, enabling proactive maintenance scheduling and operational efficiency. This real-time data pipeline supports condition-based maintenance, reducing unplanned downtime and maximizing asset utilization in logistics and transportation networks.

Advances in predictive maintenance analytics are transforming vehicle upkeep, with machine learning analyzing historical and real-time sensor data to forecast failures, extend vehicle lifespan, and streamline repair cycles. At the same time, the growth of usage-based insurance is accelerating adoption, as insurers leverage behavioral analytics, such as speed, braking habits, idle time, and fatigue patterns, to customize premiums and encourage safer driving.

Restraint - Legacy Barriers and Data Gaps Hinder Fleet Analytics Integration

Vendors struggle with complex integration when retrofitting legacy fleets lacking built-in telematics and precise sensors. Many fleets struggle to adopt onboard predictive maintenance platforms due to disparate data protocols and missing hardware, leading to costly middleware and phased rollouts. Poor sensor data quality and inconsistent formats result in unreliable predictions under condition-based predictive analytics failure risk, diminishing trust in algorithmic outputs.

Rising adoption is tempered by the complexity of protecting fleet-scale vehicle data, as firms struggle to ensure compliance with GDPR, CCPA-style laws, and new oversight in the U.S. and EU. Transparent privacy disclosure remains poor, studies expose undisclosed driver behavior tracking in infotainment systems, raising concerns about the in-vehicle data transparency deficiency. A shortage of skilled professionals in the AI-driven telematics analytics workforce gap further delays rollout, especially for smaller operators.

Opportunity - EV Battery Diagnostics and Mobility as a Service (MaaS)-Driven Urban Mobility Analytics Unlock New High-Value Opportunities

Vehicle analytics firms can capitalize on EV-battery health monitoring platforms to deliver real-time insights into state of health (SoH), state of charge (SoC), thermal behavior, and degradation patterns. These platforms support predictive EV-battery diagnostics frameworks, enabling fleet operators to forecast battery replacements and proactively manage warranty claims. OEMs and battery-as-a-service providers can adopt real-time battery analytics feedback loops to inform design improvements and reduce recalls, especially as EV penetration surges in emerging markets such as India.

Another niche opportunity lies in connected mobility data integration for MaaS analytics, where shared mobility platforms, transit agencies, and Autonomous Mobility on Demand (AMoD) fleet operators integrate vehicle analytics to optimize operations.

These systems use Vehicle-to-Everything (V2X)-enabled traffic optimization insights to smooth congestion, reduce idle time, and dynamically rebalance fleets in real time. Municipal smart city deployments, such as India's AI-powered road safety pilot, create demand for telematics-based urban mobility analytics engines that feed municipal dashboards and planning tools.

Category-wise Analysis

Application Insights

Predictive maintenance is the largest application segment, accounting for an estimated 40% of the total market share in 2025. It minimizes vehicle downtime and optimizes service cycles by leveraging real-time telematics, engine diagnostics, and AI-driven failure prediction models.

OEMs and large fleet operators embed these solutions to streamline operations and extend asset lifecycles. This segment benefits from strong demand in commercial fleets, where unplanned repairs translate into revenue losses and operational inefficiencies. For example, DHL leverages predictive maintenance powered by real-time telematics to reduce vehicle downtime and optimize fleet operations across its logistics network.

Usage-based insurance (UBI) has emerged as the fastest-growing segment. Insurers are increasingly integrating vehicle analytics to assess driving behavior, factoring in speed consistency, hard braking, acceleration patterns, and trip duration.

This data enables dynamic premium pricing models that reward safe driving and reduce underwriting risks. The proliferation of connected vehicle ecosystems and embedded telematics across new vehicle models has made real-time data accessible for insurers globally.

End-user Insights

OEMs and Tier-1 suppliers lead the market, holding an estimated 39.8% of the market share of total vehicle analytics adoption. These companies lead in embedding analytics platforms directly into vehicle design, testing, and after-sales services. They utilize real-time data for warranty management, R&D improvement cycles, and feature personalization. Predictive diagnostics and component health analytics help reduce warranty claim costs and improve vehicle reliability.

As automotive manufacturers transition toward EVs and autonomous vehicles, the integration of analytics becomes more critical in managing software-defined vehicle architectures and complex sensor arrays. For example, Bosch provides advanced telematics and predictive maintenance solutions integrated into vehicle systems, helping OEMs reduce warranty costs and enhance component performance.

Insurance providers represent the fastest-growing end-user segment. The shift toward UBI and behavior-based underwriting is a key catalyst, as insurers strive for better risk segmentation and more accurate premium calculation. Vehicle analytics enables these insurers to monitor driver patterns at scale, assess claims more efficiently, and reduce fraud. The expansion of smartphone-based telematics, usage-based policy models, and consumer demand for fairness in pricing have fueled rapid adoption.

Regional Insights

North America Leads Vehicle Analytics Market Trends - AI-Focused Infrastructure and OEM-Driven Innovation

North America continues to lead, accounting for an estimated 34% of total revenue share, primarily due to its mature telematics infrastructure, aggressive smart mobility investments, and connected vehicle mandates. The U.S. leads globally for vehicle analytics.

Federal and state-level transportation departments have launched over 38 V2X infrastructure pilots, backed by over US$800 Mn in funding to deploy edge-to-cloud analytics platforms, particularly across highway corridors and smart city zones. Major automakers and fleet operators, such as GM, Ford, UPS, and FedEx, are embedding predictive diagnostics and usage-based analytics across their fleets to reduce downtime and improve operational control.

Canada is also witnessing strong adoption of vehicle analytics through nationwide smart mobility programs and insurance innovation. The expansion of 5G and cloud infrastructure has enabled real-time vehicle tracking and safety analytics for public and private fleets.

Canadian cities such as Toronto and Vancouver are investing in urban analytics platforms to optimize bus routes, reduce carbon emissions, and enhance public transport reliability. Canadian insurers Intact and Desjardins are advancing usage-based insurance (UBI) by leveraging driver behavior analytics to develop personalized policy models.

Asia Pacific Vehicle Analytics Market Trends - EV Penetration and Smart Mobility Expansion Fuel Demand

Asia Pacific is the fastest-growing regional segment, expected to expand at the highest CAGR through 2032. Massive investments in EV production, telematics integration, and smart urban infrastructure make countries such as China and India pivotal to future growth.

Urban digital transformation projects, expanded logistics fleets, and mass transit systems require deep vehicle and urban analytics, making APAC a strategic growth engine for solutions such as V2X route optimization, battery diagnostics, and traffic analytics dashboards.

China is the epicenter of global EV and smart vehicle production, contributing 58% of global EV output in 2023 and hosting several large-scale analytics deployments. Leading Chinese OEMs, BYD, NIO, and Geely, are embedding real-time battery analytics, predictive fault detection, and in-vehicle behavior scoring systems to differentiate in a competitive market.

The Chinese Ministry of Industry and Information Technology (MIIT) has mandated integration of remote diagnostics and driving analytics platforms in new NEVs (New Energy Vehicles).

India is emerging as a strong growth engine for vehicle analytics, driven by surging logistics digitization and EV adoption. The country’s fleet telematics market is projected to grow at a high CAGR, with real-time vehicle health dashboards, route optimization, and usage-based insurance becoming mainstream in cities including Mumbai, Bengaluru, and Delhi.

In 2024, India launched its first AI-powered road safety initiative in Uttar Pradesh, integrating crash prediction and driver monitoring analytics in public buses. Government incentives under FAME II and the National Logistics Policy further support deep telematics integration across EV fleets and long-haul trucks.

Europe Vehicle Analytics Market Trends - Regulatory Push and Safety Analytics Mandates Drive Growth

Europe ranks as the second-largest market, supported by stringent vehicle safety regulations, electrification targets, and increasing adoption of autonomous mobility systems. Germany hosts major OEMs such as Volkswagen, Daimler, and BMW, all heavily investing in analytics-driven innovation.

These automakers are integrating predictive maintenance tools and real-time in-vehicle data platforms to enhance reliability and reduce warranty costs. The national focus on connected EVs and software-defined vehicles has driven the adoption of embedded analytics platforms that sync with R&D pipelines. Germany is among the first countries to pilot ADAS-integrated predictive analytics for autobahn traffic management, supporting wider V2X deployment initiatives.

The U.K. is rapidly transitioning toward AI-powered smart mobility, with Transport for London (TfL) and private operators integrating analytics into fleet logistics, public transport, and rideshare optimization.

The U.K. government’s Connected Places Catapult program has invested in accelerating trials of vehicle analytics platforms, particularly for real-time congestion forecasting and emissions reduction. UBI adoption is accelerating, with insurers such as Admiral and By Miles using live driver feedback to reward safer driving behavior.

Competitive Landscape

The global vehicle analytics market is moderately fragmented, with a mix of legacy automotive software providers, telematics vendors, cloud infrastructure players, and niche AI startups. Companies are investing in AI-driven analytics platforms, real-time telematics, and connected fleet intelligence to capture market share across OEMs, insurers, and mobility providers.

Geotab and IBM are developing dedicated battery analytics modules, offering predictive diagnostics and SoH tracking, and firms are increasingly shifting toward onboard analytics to reduce cloud dependency and improve data latency for real-time decision-making. As vehicle analytics spans highly regulated and technologically demanding verticals, new market entrants face high barriers in terms of data privacy, automotive-grade AI, and integration complexity.

Key Industry Developments

- In March 2025, SAP introduced Vehicle Insights 2.0, adding blockchain-based security and enhanced real-time fleet telematics capabilities to improve predictive maintenance, driver behavior analysis, and asset tracking across OEMs and operators.

- In January 2025, IBM released an AI-powered Fleet Intelligence Suite designed specifically for EV fleets. It offers battery life monitoring, energy consumption forecasting, and maintenance optimization to boost vehicle uptime and cost efficiency.

Companies Covered in Vehicle Analytics Market

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Verizon Connect

- Geotab Inc.

- Teletrac Navman

- Nauto Inc.

- Otonomo Technologies Ltd.

- The Floow (a subsidiary of Otonomo)

- Intellias

- CloudMade

- Smart Eye AB

- NVIDIA Corporation

- Harman International (Samsung)

- Bosch Mobility Solutions

- Applied Intuition

- Wejo Group Ltd.

- Inseego Corp.

- Moovit (an Intel company)

- Continental AG

Frequently Asked Questions

The vehicle analytics market is expected to be valued at approximately US$ 5.09 Bn in 2025.

By 2032, the vehicle analytics market is projected to reach nearly US$ 22.2 Bn, expanding at a strong pace due to the integration of predictive analytics, AI-driven diagnostics, and smart mobility platforms.

Rise of usage-based insurance (UBI) and behavior-based risk models, and shift toward software-defined vehicles (SDVs) with embedded analytics.

Predictive maintenance is the largest segment, due to its proven impact on reducing downtime and enhancing vehicle reliability.

The vehicle analytics market is expected to grow at a CAGR of approximately 23.4% from 2025 to 2032.

Key players include IBM Corporation, Microsoft Corporation, SAP SE, Verizon Connect, and Geotab Inc.