- Smart Packaging

- Vegetable Parchment Paper Market

Vegetable Parchment Paper Market Size, Share, and Growth Forecast, 2026 - 2033

Vegetable Parchment Paper Market by Product Type (Bleached, Resin Treated, Others), Type (GSM) (40-50 gsm, 30-40 gsm, Others), Classification, Distribution Channel, and Regional Analysis for 2026 - 2033

Vegetable Parchment Paper Market Size and Trends Analysis

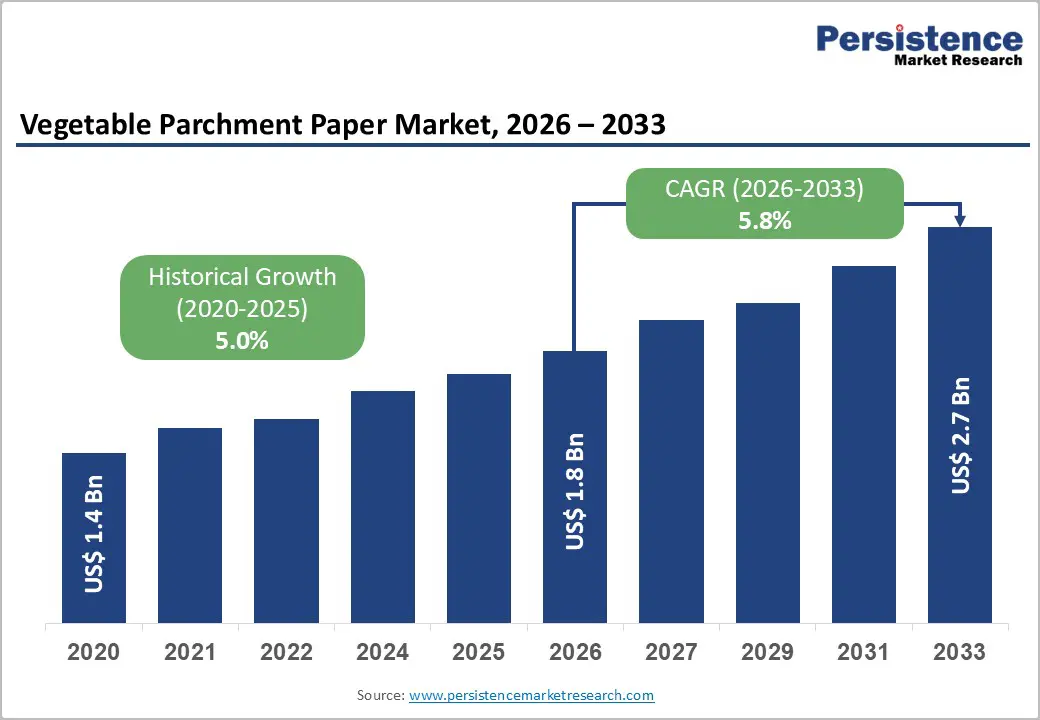

The global vegetable parchment paper market is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033, driven by the rising demand from commercial bakeries and foodservice operators, regulatory pressure to eliminate PFAS-based grease-proofing materials, and increasing adoption of e-commerce channels for bulk procurement.

Vegetable parchment paper continues to gain preference due to its heat resistance, grease barrier performance, and food-contact safety. Product innovation is shifting demand toward bleached parchment for hygiene-sensitive applications and siliconized genuine vegetable parchment for premium and reusable baking needs.

Key Industry Highlights

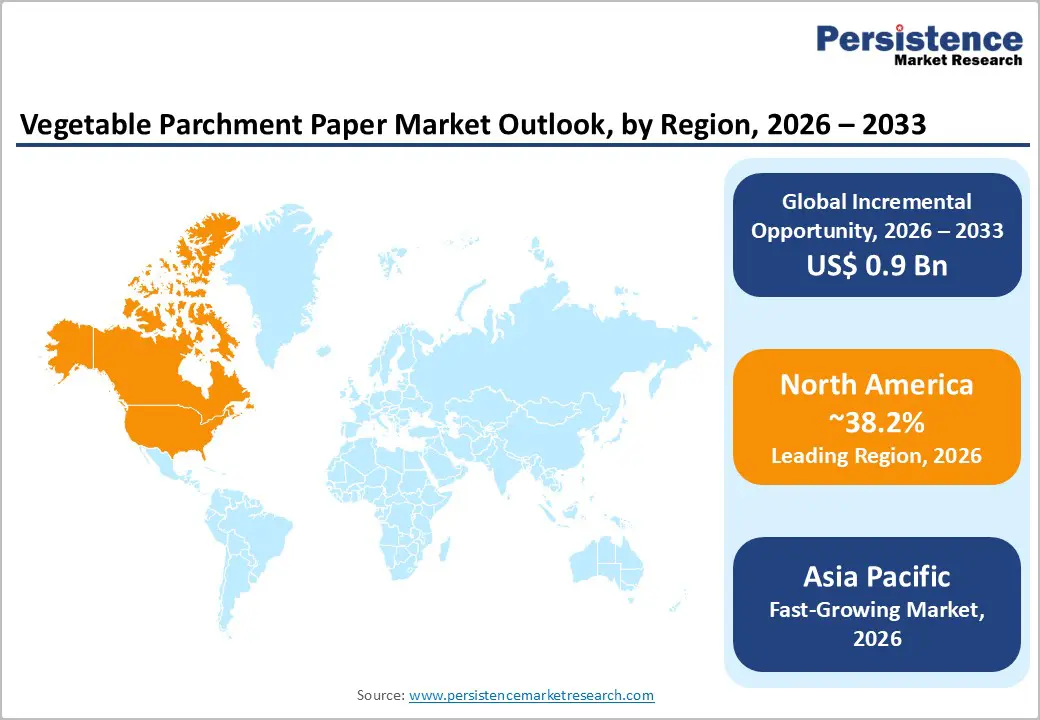

- Leading Region: North America is projected to account for approximately 38.2% of the market share, supported by a mature foodservice sector, high industrial bakery penetration, and accelerated adoption of PFAS-free food-contact materials driven by regulatory oversight in the U.S.

- Fastest-growing Region: Asia Pacific, registering the highest growth rate globally, fueled by the rapid expansion of QSR networks, industrial bakery capacity, and packaged food consumption across China, India, Japan, and ASEAN markets.

- Investment Plans: Ongoing investments are focused on local converting capacity, silicone-treatment technologies, and PFAS-compliant product lines, particularly in North America and Europe, while Asia Pacific is attracting capital toward lower-GSM production lines and regional finishing facilities to support high-volume, cost-sensitive demand.

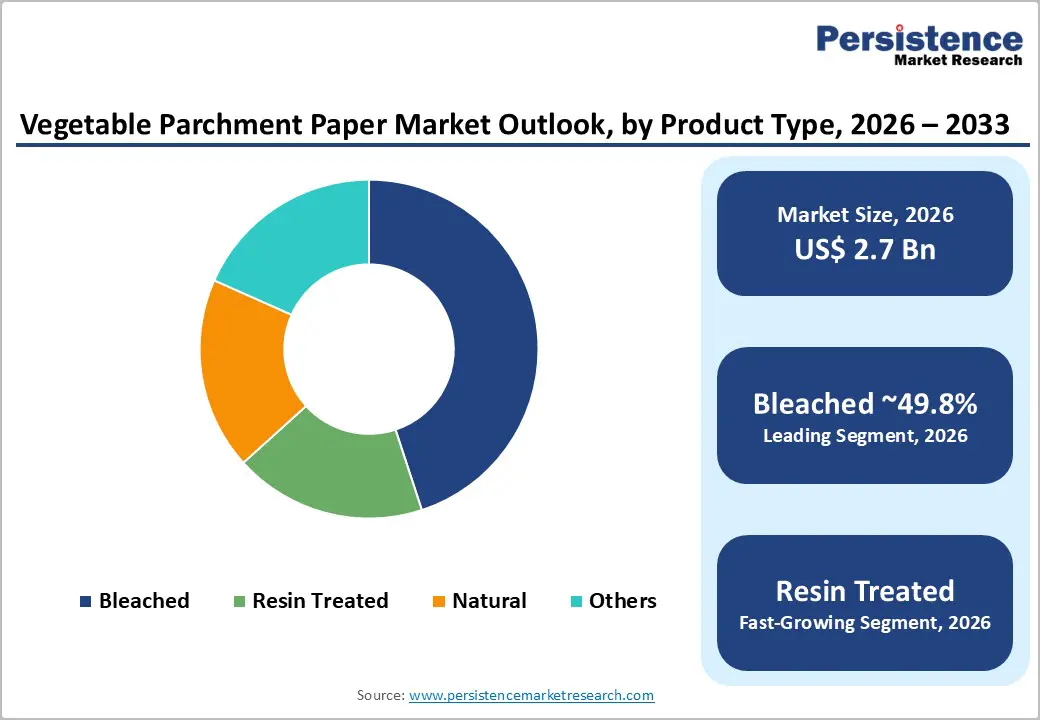

- Dominant Product Type: Bleached vegetable parchment is anticipated to hold approximately 49.8% market share, driven by strong demand for retail bakery trays, frozen food packaging, and branded food wraps that require hygiene assurance and visual consistency.

- Leading Classification: Plain vegetable parchment is estimated to represent roughly 61.2% of the market share, favored for its cost-effectiveness and compostable profile in butter, cheese, and general baked-goods packaging applications.

| Key Insights | Details |

|---|---|

| Vegetable Parchment Paper Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$2.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Barrier -Expansion of Foodservice and Commercial Bakery Operations

Global demand for convenience foods, frozen bakery products, and ready-to-eat meals is driving sustained growth in commercial baking and quick-service restaurant operations. Vegetable parchment paper is widely used in high-throughput baking environments for tray liners, molded baking cups, interleaving, and wrapping due to its thermal stability, grease resistance, and compliance with food safety standards. Commercial bakeries in developed economies are expanding capacity at mid-single-digit rates, while emerging markets in Asia-Pacific are growing faster due to urbanization and changing consumption habits. As production volumes rise, parchment consumption increases proportionally per installed oven line. Food manufacturers are also shifting toward higher-performance parchment grades to reduce product sticking, minimize waste, and improve operational efficiency.

Regulatory Pressure on PFAS and Shift toward PFAS-Free Greaseproofing

Regulatory actions targeting per- and polyfluoroalkyl substances (PFAS) in food-contact materials have reshaped procurement strategies across the food packaging value chain. The phase-out of PFAS-based grease-proofing has accelerated the adoption of genuine vegetable parchment, which achieves grease resistance through cellulose transformation rather than chemical coatings. Silicone-treated parchment has also gained traction as a compliant alternative offering superior release properties. Food brands and foodservice operators are increasingly prioritizing verified PFAS-free materials to mitigate compliance risks and reputational exposure. This regulatory environment has created a structural shift in demand toward parchment solutions that combine food safety assurance with performance reliability.

Sustainability Commitments and Consumer Preference for Compostable Packaging

Retailers and foodservice chains are responding to consumer demand for environmentally responsible packaging by replacing plastic-based and fluorochemical-treated materials with cellulose-based alternatives. Vegetable parchment paper aligns with sustainability objectives due to its compostability and reduced chemical footprint. Large retailers and QSR chains have publicly committed to increasing the content of recyclable and compostable packaging, creating strong downstream demand for certified parchment products. This trend supports higher adoption of natural and unbleached parchment in selected applications and encourages manufacturers to invest in energy-efficient production processes and responsibly sourced pulp. Sustainability disclosure requirements further increase supplier qualification thresholds, reinforcing long-term supplier relationships.

Barrier Analysis - Raw Material and Energy Price Volatility

Vegetable parchment paper production is pulp-intensive and highly energy-intensive, due to chemical parchmentization and thermal processing requirements. Volatility in pulp pricing, transportation costs, and energy inputs can significantly compress margins. During cost-inflation cycles, manufacturers may be forced to absorb cost increases or pass them on to buyers, thereby reducing demand among price-sensitive food processors. Smaller customers often delay purchases or downgrade specifications during such periods, increasing demand volatility. Persistent cost fluctuations also pressure working capital requirements, particularly for specialized mills with limited pricing flexibility.

Capacity Constraints and Food-Safety Qualification Cycles

Food packaging buyers typically require extensive supplier qualification, including migration testing, traceability documentation, and regulatory approvals. Adding new capacity or entering new geographic markets involves substantial capital investment and long validation timelines. Smaller producers face prolonged sales cycles when attempting to supply large retailers or multinational foodservice operators. In periods of sudden demand growth, such as following regulatory bans, existing capacity limitations can lead to temporary shortages and price volatility. Companies without flexible manufacturing capacity or in-house testing capabilities face elevated execution risk.

Opportunity Analysis - Premium Siliconized Genuine Vegetable Parchment for Commercial Reuse

Siliconized genuine vegetable parchment offers enhanced release performance, high-temperature stability, and reusability, making it particularly attractive to commercial bakeries and artisanal baking operations. These products command premium pricing and are increasingly adopted to reduce oil usage, minimize product waste, and improve baking consistency. Demand growth is strongest in North America and Western Europe, where professional baking standards and cost-of-waste considerations are highest. Manufacturers that expand silicone-treatment capabilities can capture higher margins and establish long-term supply agreements with high-volume commercial customers.

Lightweight (30-40 GSM) Eco-Grade Products for Emerging Markets

Demand for lower-basis-weight parchment paper in the 30-40 GSM range is increasing in price-sensitive and logistics-driven markets. Quick-service restaurants and emerging-market retailers favor lightweight, cost-efficient, and eco-labeled packaging materials. Lower GSM products reduce shipping costs and packaging waste while enabling bulk e-commerce distribution. Adoption is accelerating in Asia-Pacific and Latin America, where growth in street food, packaged bakery, and food delivery services is strongest. Suppliers that maintain consistent grease resistance and strength at lower weights can gain a competitive advantage in high-volume segments.

Category-wise Analysis

Product Type Insights

Bleached vegetable parchment paper is expected to account for 49.8% of the market share, supported by its strong hygiene perception, clean visual appeal, and superior printability. These attributes make it the preferred choice for retail bakery trays, frozen food packaging, and branded food wraps, where product presentation and regulatory compliance are critical. Demand is particularly strong in developed markets, where food safety standards and branding requirements are stringent. Bleached grades typically command premium pricing due to additional chemical processing and quality control steps, reinforcing their dominant position in high-value food-contact applications.

Resin-treated and surface-enhanced vegetable parchment is emerging as the fastest-growing product segment, driven by its enhanced grease resistance and improved heat tolerance without reliance on PFAS-based chemistries. These performance benefits support increased adoption in frozen bakery, ready-to-eat meals, and quick-service restaurant (QSR) operations, where consistent release performance and low migration are essential. Regulatory pressure to eliminate fluorochemicals from food packaging has accelerated the shift toward resin-treated alternatives, positioning this segment for sustained growth across both developed and emerging markets.

Classification Insights

Plain vegetable parchment is expected to remain the most widely used classification, accounting for 61.2% of the market share due to its cost-efficiency, compostability, and broad functional suitability. It is extensively applied in butter wrapping, cheese interleaving, and general baked-goods packaging, where moderate grease resistance and thermal stability meet performance requirements. High-volume food processors and regional bakeries favor plain parchment for its balance of functionality and affordability, particularly in price-sensitive markets.

Siliconized genuine vegetable parchment is witnessing rapid adoption, supported by its superior non-stick performance, high-temperature stability, and reusability. Commercial and industrial bakeries increasingly favor siliconized grades to reduce oil usage, minimize product waste, and improve baking consistency across production cycles. Growing emphasis on operational efficiency and premium baking outcomes continues to drive demand for siliconized parchment, especially in professional bakery and foodservice environments.

Regional Insights

North America Vegetable Parchment Paper Market Trends - PFAS-Free Compliance Driving Foodservice and Industrial Bakery Demand

North America is projected to remain the leading regional market, accounting for approximately 38.2% of the market share, supported by a highly developed foodservice ecosystem and strong penetration of industrial baking operations. The U.S. dominates regional demand due to its large-scale consumption of frozen bakery products, ready-to-eat meals, and convenience foods, all of which rely heavily on parchment paper for baking, wrapping, and food separation applications. High commercial bakery density, particularly among large players supplying retail and QSR chains, sustains consistent volume demand for both bleached and siliconized vegetable parchment grades. A defining factor shaping the North American market is regulatory scrutiny of food-contact materials, especially restrictions on PFAS-based greaseproofing agents. Regulatory guidance from U.S. agencies and state-level actions, such as California and New York tightening limits on fluorochemicals in food packaging, have accelerated the shift toward PFAS-free vegetable parchment solutions. This has directly benefited resin-treated and siliconized parchment products, which offer comparable release performance without regulatory exposure. As a result, foodservice brands and bakery chains increasingly specify compliant parchment materials in procurement contracts.

Manufacturers have responded by investing in local converting capacity and surface-treatment technologies to ensure supply reliability and compliance. For example, major North American paper converters supplying baking and foodservice segments have expanded silicone-coating and precision calendering capabilities to support reusable parchment formats demanded by industrial bakeries. At the brand level, premium retail baking-paper labels sold through specialty kitchenware chains and large-format grocery stores have emphasized “chemical-free” and “food-safe” positioning, reinforcing consumer trust and sustaining higher price points. Collectively, these dynamics support North America’s continued leadership despite moderate volume growth relative to emerging regions.

Europe Vegetable Parchment Paper Market Trends - Regulation-Led Demand for Certified, Compostable Baking Papers

Europe represents a structurally strong and regulation-driven market for vegetable parchment paper, underpinned by deep-rooted baking traditions and stringent food safety standards. Key demand centers include Germany, France, the U.K., and Spain, where both artisanal and industrial bakeries maintain high parchment paper usage intensity in bread, pastry, and confectionery production. The region’s emphasis on premium food presentation and material traceability supports steady demand for genuine vegetable parchment that is bleached and siliconized, particularly in branded and export-oriented food packaging.

A critical growth enabler in Europe is regulatory harmonization under the EU food-contact material frameworks, which has increased scrutiny of additives, coatings, and migration limits. The European Food Safety Authority’s ongoing evaluation of chemical substances used in packaging has reinforced demand for cellulose-based, compostable parchment solutions with transparent compliance documentation. This regulatory environment has encouraged food manufacturers and retailers to transition away from alternative greaseproof papers containing synthetic additives, benefiting vegetable parchment suppliers with certified, compliant product lines.

Recent years have seen European producers focus on technology upgrades and compliance-led innovation, rather than pure capacity expansion. Paper mills and converters in Germany and Scandinavia have invested in energy-efficient parchmentizing processes and advanced silicone application systems to meet sustainability targets while maintaining performance. Private-label baking paper brands sold through European supermarket chains have also increasingly highlighted recyclability, compostability, and chemical transparency, aligning with consumer expectations and retailer sustainability commitments. These developments reinforce Europe’s role as a quality-driven, regulation-led market, where innovation is shaped more by compliance and environmental performance than by volume growth alone.

Asia Pacific Vegetable Parchment Paper Market Trends - QSR Expansion and Localized Converting Fueling High-Volume Growth

Asia Pacific is likely to be the fastest-growing regional market for vegetable parchment paper, driven by rapid urbanization, rising disposable incomes, and the continued expansion of quick-service restaurant (QSR) and industrial bakery networks. China and India are emerging as high-volume growth engines as packaged baked goods, frozen snacks, and ready-to-cook foods gain traction among urban consumers. In parallel, Japan maintains a strong demand for specialty parchment products due to its stringent food safety norms and preference for high-quality food packaging materials.

Growth dynamics in the region are closely tied to capacity expansion and localization strategies. Suppliers are increasingly establishing local converting and finishing operations across China, Southeast Asia, and India to reduce import dependence and improve cost competitiveness. This has supported wider adoption of lower-GSM vegetable parchment grades, which are well-suited for high-volume foodservice use and price-sensitive markets. QSR chains operating across the Asia Pacific have played a pivotal role by standardizing baking and wrapping materials across outlets, creating consistent baseline demand for grease-resistant, heat-stable parchment solutions.

Japan and South Korea continue to influence the region’s quality benchmarks, particularly in siliconized parchment used for precision baking and specialty food preparation. ASEAN countries are witnessing increased use of vegetable parchment in processed food exports, where compliance with international food-contact regulations is essential. Asia Pacific is also evolving into both a consumption-driven and manufacturing-oriented market, with suppliers balancing cost efficiency, performance consistency, and regulatory alignment to capture long-term growth opportunities.

Competitive Landscape

The global vegetable parchment paper market is moderately concentrated. Large specialty paper manufacturers dominate premium and technology-intensive segments, while regional producers serve commodity and unbleached grades. Competitive differentiation centers on product performance, food-safety compliance, converting capabilities, and geographic reach.

Recent industry developments include expansion of PFAS-free product lines, capacity upgrades for silicone-treated parchment, and consolidation among regional converters to strengthen food-contact credentials and distribution coverage.

Leading players focus on product premiumization, regional expansion through local converting, and compliance-led differentiation. Emerging strategies include long-term supply contracts with QSR chains and collaborative product development with commercial bakeries.

Key Industry Developments

- In July 2025, Nordic Paper introduced a new natural greaseproof paper for the food industry with barrier properties achieved without fluorochemicals, expanding its sustainable product portfolio.

Companies Covered in Vegetable Parchment Paper Market

- Ahlstrom

- Nordic Paper

- Hoffmaster Group

- Reynolds Consumer Products

- Seaman Corporation

- Papertec

- Pudumjee Pulp & Paper

- Morvel Poly Films

- Amol Group

- JK Paper

- Twin Rivers Paper Company

- Georgia-Pacific LLC

- McNairn Packaging

- METSA Tissue

- Sappi Limited

- Nippon Paper Industries

- Stora Enso

- International Paper

Frequently Asked Questions

The vegetable parchment paper market is valued at US$1.8 billion in 2026.

By 2033, the vegetable parchment paper market is expected to reach US$2.7 billion.

Key trends include rising adoption of PFAS-free grease-proofing, growing demand from commercial bakeries and foodservice operators, increased use of siliconized parchment for superior release and reusability, and expansion of lightweight (30-40 gsm) eco-grade products for cost-sensitive and high-volume applications.

Bleached vegetable parchment is the leading product type, accounting for approximately 45-55% of global market share, driven by hygiene perception, printability, and strong demand from retail bakery and frozen food packaging.

The vegetable parchment paper market is projected to grow at a CAGR of 5.8% between 2026 and 2033, supported by foodservice expansion, regulatory pressure to eliminate PFAS, and rising packaged and frozen food consumption.

Major players include Ahlstrom, Nordic Paper, Reynolds Consumer Products, Hoffmaster Group, and Pudumjee Pulp & Paper Mills.