- Food Ingredients & Additives

- Dehydrated Vegetables Market

Dehydrated Vegetables Market Size, Share, and Growth Forecast, 2025 - 2032

Dehydrated Vegetables Market By Product Type (Onions, Carrots, Others), Form (Powder & Granules, Flakes, Others), Technology, End-use, and Regional Analysis for 2025 - 2032

Dehydrated Vegetables Market Size and Trends Analysis

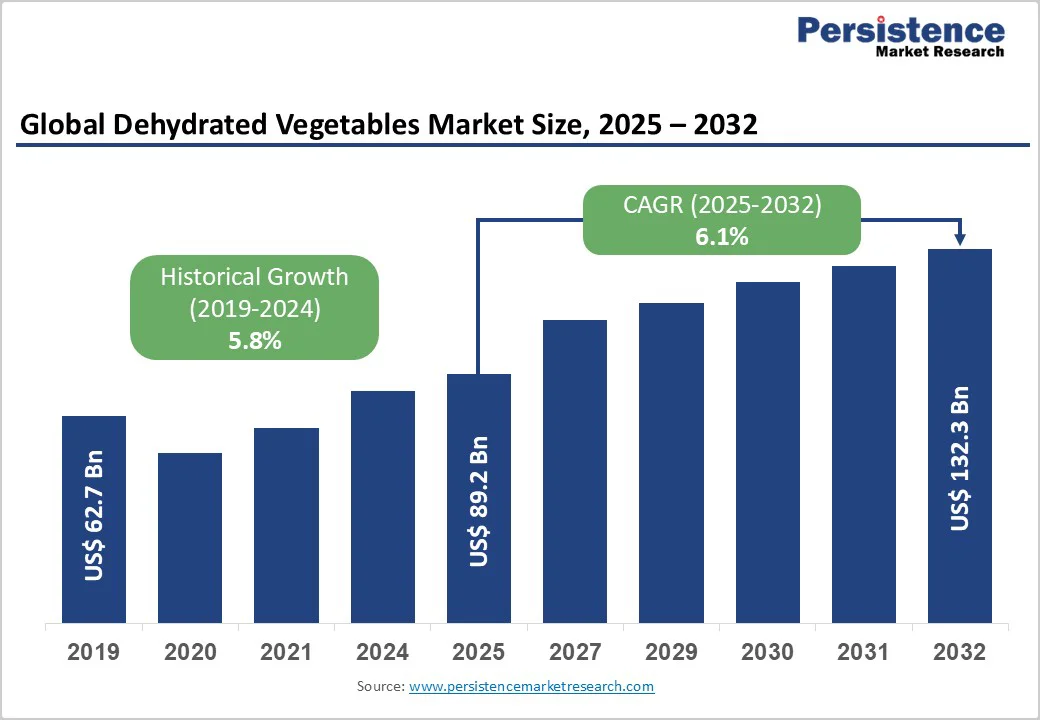

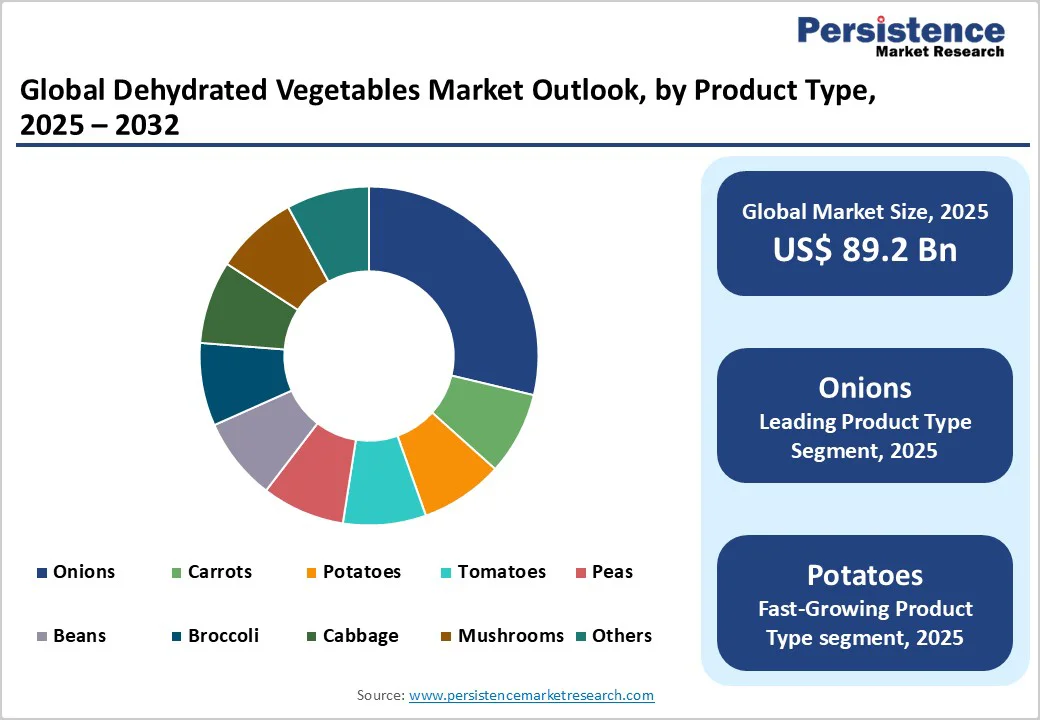

The global dehydrated vegetables market size is likely to be valued at US$89.2 Billion in 2025 and is expected to reach US$132.3 Billion by 2032, growing at a CAGR of approximately 5.8% during the forecast period from 2025 to 2032, driven by rising demand for convenient, shelf-stable and natural food ingredients; increasing application in soups, snacks, meal kits and ready-to-eat formats; and continuous improvements in food dehydration technologies that help retain flavor and nutrients.

Growth in quick-service restaurants, clean-label foods, and waste-reduction initiatives in fresh produce supply chains further accelerates market adoption. Differences in market estimates across providers stem mainly from varied scope definitions and category inclusions.

Key Industry Highlights

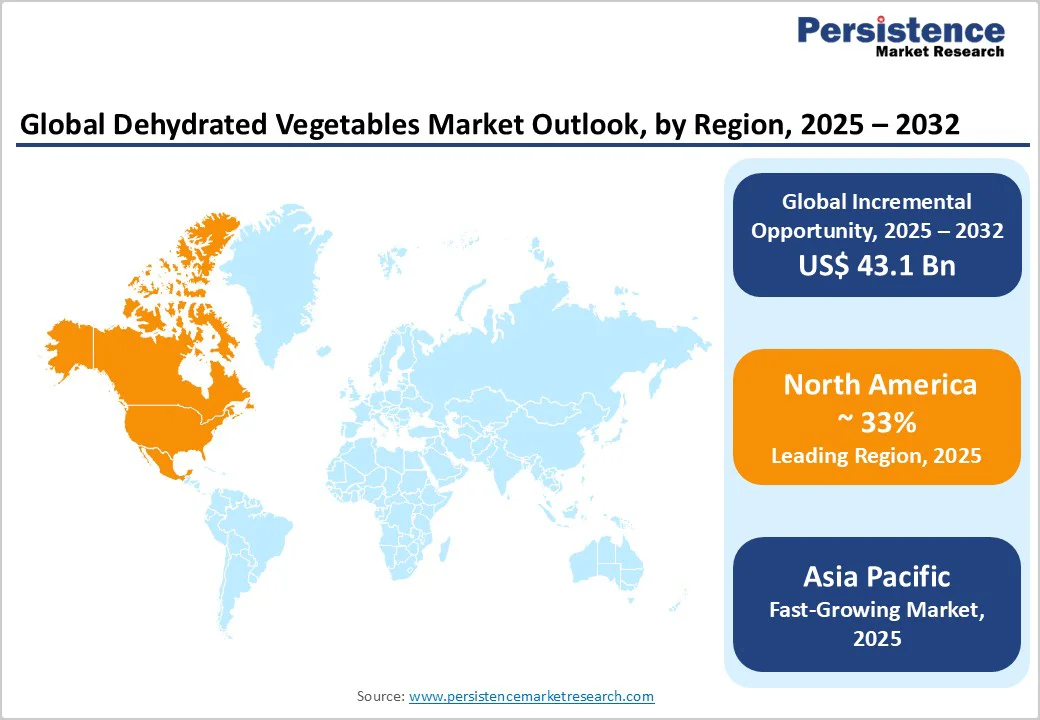

- Leading Region: North America remains the dominant regional market, accounting for approximately 33% of the market share, supported by high consumption of packaged soups, snack mixes, and ready-to-cook meals.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rising demand for convenience foods, expanding food processing capacity, and rapid urbanization.

- Investment Plans: Manufacturers are allocating 20-25% of new capital expenditure to advanced dehydration technologies, such as freeze-drying, vacuum drying, and micronization, to support premium powder formats, improve nutrient retention, and expand product portfolios.

- Dominant Product Type: Onions lead the product type category with more than 29.8% share, supported by their extensive use in seasonings, instant foods, and large-scale food processing operations globally.

- Leading Form: Powder and flake formats dominate the form segment with approximately 48% share, driven by their high compatibility with industrial formulations, longer shelf life, and efficiency in automated production lines.

| Key Insights | Details |

|---|---|

|

Dehydrated Vegetables Market Size (2025E) |

US$89.2 Bn |

|

Market Value Forecast (2032F) |

US$132.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Industrial Use of Shelf-Stable Ingredients

Food processing industries account for roughly half of global dehydrated vegetable consumption, reflecting the extensive integration of dehydrated onion, garlic, potato, and tomato products into soups, seasonings, sauces, snack mixes, and ready meals. Manufacturers favor dehydrated formats to standardize flavor profiles, reduce wastage, improve shelf life, and ensure availability despite seasonal fluctuations. This industrial reliance forms a steady demand base and supports continuous investments in advanced dehydration lines, including low-temperature and energy-efficient systems.

Urban Lifestyle Shifts and Clean-Label Preferences

Urbanization, time-poor consumer lifestyles, and the growth of ready-to-eat formats have increased the adoption of dehydrated vegetables in both retail and foodservice. Clean-label and natural-ingredient positioning boosts demand for organic, additive-free dehydrated products. Advances in drying technologies, such as vacuum drying, freeze-drying, and spray-drying, enhance nutritional retention and sensory quality, strengthening the appeal of premium dehydrated formats in meal kits, fortified blends, baby food, and health-oriented snacks.

Waste Reduction and Supply-Chain Efficiency

Dehydrated vegetables mitigate supply-chain risks by enabling long-term storage without cold-chain dependence, reducing post-harvest losses, and stabilizing costs driven by seasonal price volatility. For producers and exporters, dehydration reduces bulk weight and freight costs. Regions with variable harvest cycles rely increasingly on dehydrated ingredients to maintain a year-round supply, making dehydration an important strategy for both value retention and operational resilience.

Barrier Analysis - High Energy and Capital Costs

Dehydration processes, especially freeze-drying, are capital-intensive and require significant energy input. Volatile energy prices and tightening environmental standards directly influence production costs. Smaller companies face barriers to adopting modern drying technologies due to high upfront costs, while larger processors may face margin pressure as energy costs rise sharply.

Inconsistent Standards and Quality Control Variability

Global discrepancies in product definitions (dried, dehydrated, freeze-dried), moisture thresholds, and labelling requirements create inconsistencies in market data and complicated procurement decisions. Quality control is critical, as microbial safety, flavor profile management, and consistent particle size require stringent oversight. Variability in standards across jurisdictions increases compliance costs for exporters and slows cross-border expansion for emerging players.

Opportunity Analysis - Premium Instant Meals, Powders, and Snacking Formats

Premium instant meals, fortified powders, freeze-dried snacks, and single-serve kit formats represent a high-growth opportunity. Powdered and flaked dehydrated vegetables offer high margins, broad application versatility, and strong demand from formulators seeking convenient, nutrient-dense ingredients. As consumers increasingly adopt healthier instant meal solutions, this segment is positioned to capture a meaningful share of incremental global market value over the next decade.

Production & Export Expansion in Emerging Economies

Asia Pacific, particularly China, India, and Southeast Asia, has become an attractive manufacturing base due to abundant raw materials, competitive labor, expanding processing capabilities, and supportive food-processing incentives. Rising domestic demand and strong export prospects offer investors opportunities to build vertically integrated operations, including contract farming, dehydration, and B2B export supply. Long-term prospects are bolstered by rapid urbanization and the expansion of packaged food categories.

Category-wise Analysis

Product Type Insights

Onions remain the largest product segment, with a 29.8% share, due to their universal culinary relevance, high consumption frequency, and compatibility with multiple dehydration methods, including hot-air, spray, and freeze drying. Formats such as flakes, kibbles, granules, and powders are widely used in instant soups, seasoning blends, snack flavorings, bakery fillings, gravies, and frozen meal bases. Their stable aroma, long shelf life, and consistent flavor make them indispensable for bulk food processors. Large dehydration clusters in India, China, and the U.S. ensure a steady supply of raw materials and strong export capacity. Global QSRs, ready-meal producers, and seasoning brands rely heavily on dehydrated onion formats for uniform flavor and processing efficiency.

Potato-based dehydrated ingredients form the fastest-growing category as they gain traction in instant pasta mixes, noodle seasoning sachets, baby food, savory bakery fillings, plant-based kits, and snack coatings. Their neutral taste and high starch content offer versatility across applications. Dehydrated potato flakes and granules serve as effective binders, bulking agents, and texture enhancers in extruded snacks, frozen patties, thickened soups, and gluten-free baked goods that require clean-label stability. Potato powders and pre-gelatinized starch feature prominently in ready-to-cook mashed blends, instant soup cups, and gravies that demand fast dispersion and smooth texture. Snack manufacturers also use fine granules to boost expansion and create lighter puffed snacks.

Form Insights

Powder and flake forms dominate the market as they provide superior formulation flexibility, longer shelf life, and compatibility with automated manufacturing processes. Powders are widely used by seasoning manufacturers, instant food producers, and snack companies because they disperse evenly, deliver strong flavor concentration, and simplify mass production.

Flake formats, especially onion and potato flakes, are preferred in soups, ready meals, dehydrated mixes, frozen applications, and culinary pastes due to their ability to rehydrate quickly and maintain texture. Industrial processors adopt these formats due to their low moisture content, reduced transportation weight, and ability to support high-volume contract manufacturing. They are essential in applications requiring precise dosing, such as instant noodles, bouillon cubes, bakery mixes, and functional dietary products.

Premium powder formats, especially freeze-dried onion, tomato, spinach, beetroot, and mushroom powders, are growing rapidly as demand for nutrient-dense, clean-label ingredients rises. Freeze-dried options retain superior vitamins, color, and aroma, making them ideal for fortified beverages, nutraceutical blends, clinical nutrition, and premium soups. Micro-milled powders offer ultra-smooth textures for ready-to-drink mixes, gourmet sauces, baby foods, and health-focused meal kits. Innovations in micronization, encapsulation, and low-temperature drying boost flavor and solubility. Plant-based food makers and energy-mix brands increasingly adopt these powders for convenience and nutrition, with beetroot powder used in natural sports drinks and spinach or carrot powders featured in functional pasta and immunity snacks.

Regional Insights

North America Dehydrated Vegetables Market Trends - Advanced Processing, Clean-Label Innovation & Supply-Chain Integration

North America is a major and mature market for dehydrated vegetables, holding about 33% of the global share, with the U.S. as the dominant contributor. The region’s strong food processing infrastructure, efficient cold-chain systems, and high reliance on packaged and convenience foods support sustained demand. The U.S. hosts established clusters producing dehydrated onion, potato, garlic, and mixed vegetable powders, while Canada adds strength through large potato-processing capacities. Mexico enhances the supply chain with chili and specialty vegetable dehydration for U.S. export. Growth is fueled by clean-label innovation, rising use of natural seasonings, and strong demand from snack, meal-kit, and QSR foodservice operators.

Regulatory frameworks, including FDA safety and labeling standards, impose strict microbial, moisture, and traceability controls, increasing entry barriers but favoring established producers with certified facilities. The competitive landscape spans major ingredient processors, agribusinesses, and specialized dehydrated-vegetable firms.

Companies invest in automation, energy-efficient drying, product innovation, and long-term supply contracts. Vertical integration and sustainability upgrades, such as renewable-energy drying and waste-heat recovery, are expanding. Recent trends include facility expansions, diversification into premium powders and plant-based ingredients, and multi-year agreements with major food brands, underscoring North America’s continued leadership in demand and innovation.

Europe Dehydrated Vegetables Market Trends - Sustainability-Driven Premium Processing & Retail-Oriented Innovation

Europe is a key market with deep-rooted expertise in vegetable processing, supported by advanced food manufacturing hubs across the Netherlands, Belgium, Germany, and the U.K. Strong potato-processing clusters and cooperative structures support large-scale dehydration for both domestic and export markets. Europe’s retail landscape, which prioritizes sustainability, traceability, and clean labels, drives demand for high-quality powders, flakes, and value-added dehydrated ingredient blends. Key markets include the Netherlands and Belgium, which have long-standing capabilities in potato and vegetable processing; Germany, with a large packaged-food sector; and the U.K. and France, where retail private-label demand for healthy, convenient ingredients is strong.

Sustainability policies and waste-reduction mandates in the European Union encourage food manufacturers to adopt dehydrated ingredients to reduce spoilage and improve resource efficiency. Packaging directives and organic certification systems shape product development, enabling manufacturers to innovate around recyclable packaging and organic dehydrated variants.

Investments in advanced drying lines, application laboratories, and new product innovation, such as vegetable-based natural colorants and seasoning blends, are increasing across the region. Recent developments include product diversification efforts, restructuring activities, and expansion of value-added dehydrated offerings. Europe is poised for steady growth, driven by sustainability goals, retail innovation, and continued investments in premium dehydrated formats.

Asia Pacific Dehydrated Vegetables Market Trends - High-Growth Production Hub with Export-Led Capacity Expansion

Asia Pacific is the fastest-growing regional market and a major global production hub. China and India dominate regional supply due to abundant raw materials, competitive labor costs, and rapid expansion of food-processing infrastructure. Governments across the region have implemented incentives to support food processing and export-oriented manufacturing, boosting private investment in dehydration facilities. China leads in capacity expansion, supplying both domestic convenience food manufacturers and global clients. India is a key supplier of dehydrated onions, potatoes, and mixed vegetables; favorable climate, extensive agricultural base, and export-friendly policies contribute to its rising importance.

Japan and several ASEAN countries represent demand centers for high-quality freeze-dried and specialty dehydrated ingredients, particularly for premium instant meals and retail applications. Urbanization and higher disposable incomes are reshaping consumption patterns, increasing demand for instant foods, meal kits, and clean-label products. Global buyers rely on Asia Pacific for cost-competitive procurement of vegetable powders, flakes, and granules. Regulatory systems are evolving, with greater emphasis on hygiene, traceability, and export compliance. Facilities seeking to serve the EU and U.S. markets must invest heavily in certifications, microbial control, and supply-chain transparency.

The key investment trend includes upgrading to freeze-drying lines, integrating contract farming for quality control, and strengthening backward linkages to secure agricultural supply. Recent announcements reflect expansions in dehydration capacity, new export-oriented plants, and the scaling of premium powdered ingredients for both domestic and international buyers.

Competitive Landscape

The global dehydrated vegetables market is moderately fragmented. Large global processors and integrated agribusinesses coexist with numerous regional specialists. The competitive advantage of major players stems from scale, raw-material integration, advanced drying technologies, and strong compliance capabilities. Smaller firms primarily focus on niche products, specialty powders, or regional supply contracts.

Vertical integration, energy-efficient operations, and clean-label innovation are becoming key differentiators. Leading players focus on vertical integration, premium product development (clean-label powders, freeze-dried ingredients), cost efficiency through manufacturing optimization, and B2B co-development with major food manufacturers. Traceability, sustainable production, and energy-efficient drying technologies serve as emerging themes across competitive strategies.

Key Industry Developments

- In April 2025, McCormick & Company announced the acquisition of The Dehydrated Vegetable Company to accelerate its dehydrated vegetable powders portfolio for soups, sauces, and ready-to-eat meals.

- In January 2025, the Emsland Group announced a distribution partnership in India to expand the reach of its dehydrated potato products through a local food-ingredient company.

Companies Covered in Dehydrated Vegetables Market

- Olam Food Ingredients

- Sensient Natural Ingredients

- Van Drunen Farms

- Silva International

- Berrifine

- Jain Farm Fresh Foods

- Garlico Industries

- Gebrüder Bagusat

- Freeze-Dry Foods

- Mercer Foods

- Harmony House Foods

- Eurocebollas

- Fine Organics

- Tongxiang Fengming

- Xinjiang Longping High-Tech

- Natural Dehydrated Vegetables Pvt. Ltd.

- Daksha Foods

- Chaucer Foods

- Garden Fresh Foods

- Radiance Global

Frequently Asked Questions

The dehydrated vegetables market size in 2025 is valued at US$89.2 Billion.

The market is expected to reach US$132.3 Billion by 2032.

Key trends include the rising demand for clean-label ingredients, growth in premium freeze-dried and micro-milled powders, greater use of dehydrated vegetables in instant foods and foodservice, and increasing adoption of advanced drying technologies for better nutrient retention and quality.

Onions are the leading product segment, driven by extensive use in seasonings, soups, snacks, meal kits, and industrial food processing.

The dehydrated vegetables market is projected to grow at a CAGR of 5.8% from 2025 to 2032.