- Processed Food

- Brined Vegetables Market

Brined Vegetables Market Size, Share and Growth Forecast, 2026 - 2033

Brined Vegetables Market by Product Type (Pickles, Brined Olives, Fermented Brassicas, Brined Root Vegetables, Brined Peppers, Brined Beans and Legumes), Brining Process (Traditional, Vinegar Based, Vacuum, Cold and Hot, HPP and Advanced Preservation), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Wholesale and Food Service), and Regional Analysis for 2026 - 2033

Brined Vegetables Market Share and Trends Analysis

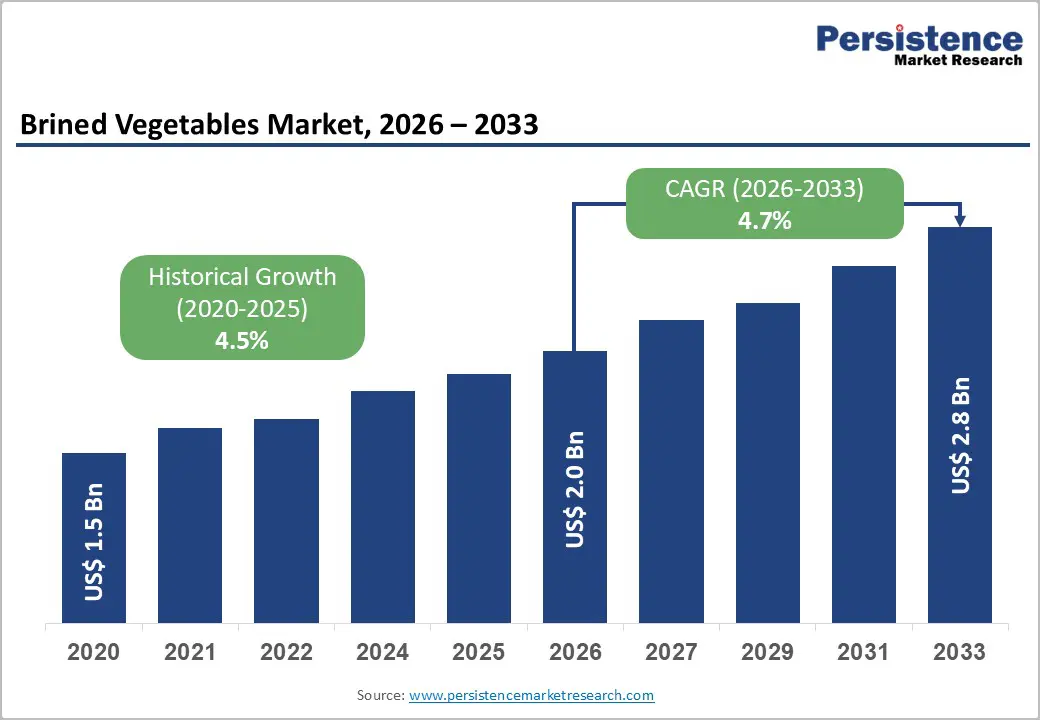

The global brined vegetables market size is likely to be valued at US$ 2.0 billion in 2026 and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 4.7% during the forecast period 2026 - 2033.

The market is expanding as consumers increasingly prefer convenient, ready-to-eat, and health-conscious food options. Products offer clear functional advantages, including enhanced flavor, natural preservation, and probiotic benefits, which appeal to both households and foodservice providers.

Growth in retail and distribution channels, such as supermarkets, specialty stores, and online platforms, is improving product accessibility. Simultaneously, urbanization, rising incomes, and expanding middle-class populations in emerging regions are driving greater adoption of packaged and brined vegetables. These combined factors create a favorable environment for sustained market expansion across diverse geographies and consumer segments.

Key Industry Highlights

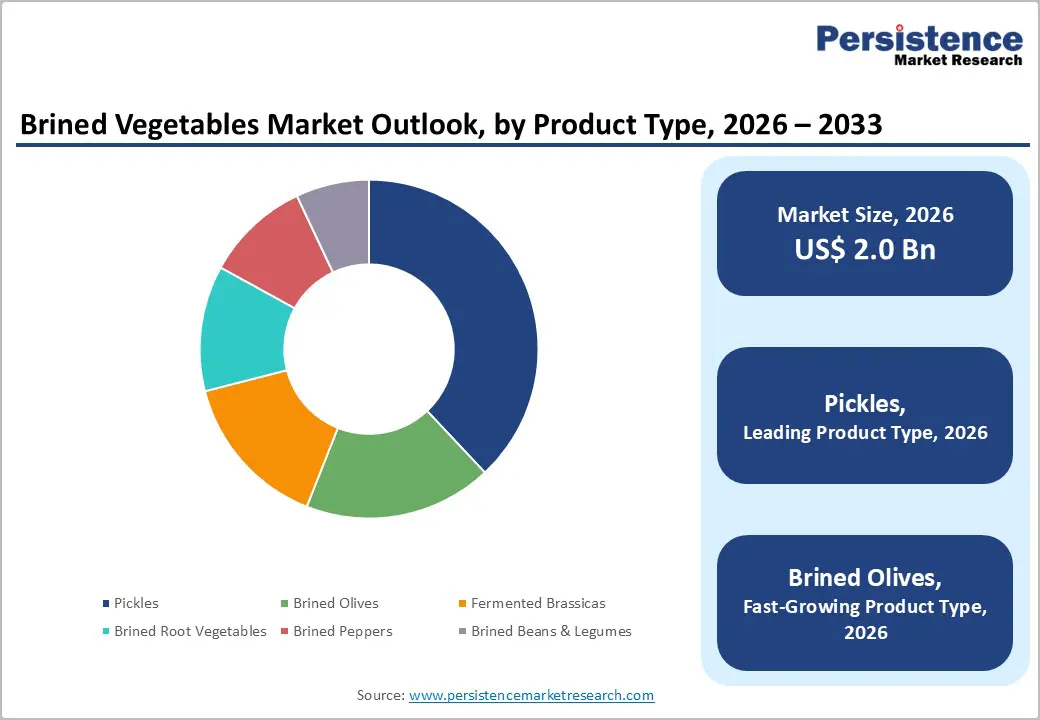

- Dominant Product Types: Pickles are projected to command approximately 38% of the revenue share in 2026, while brined olives are expected to grow the fastest at around 6.5% CAGR through 2033, driven by rising demand for Mediterranean diets and premium snacking trends.

- Leading Brining Processes: Traditional brining methods are anticipated to lead with an estimated 42% share in 2026, whereas HPP (High-Pressure Processing) and advanced preservation techniques are likely to grow fastest at about a 7% CAGR, supported by consumer preference for extended shelf life and clean-label products.

- Dominant Distribution Channels: Supermarkets and hypermarkets are expected to hold roughly 45% share in 2026, while online retail is forecasted to grow fastest at 12% CAGR, fueled by e-commerce expansion and increased consumer convenience.

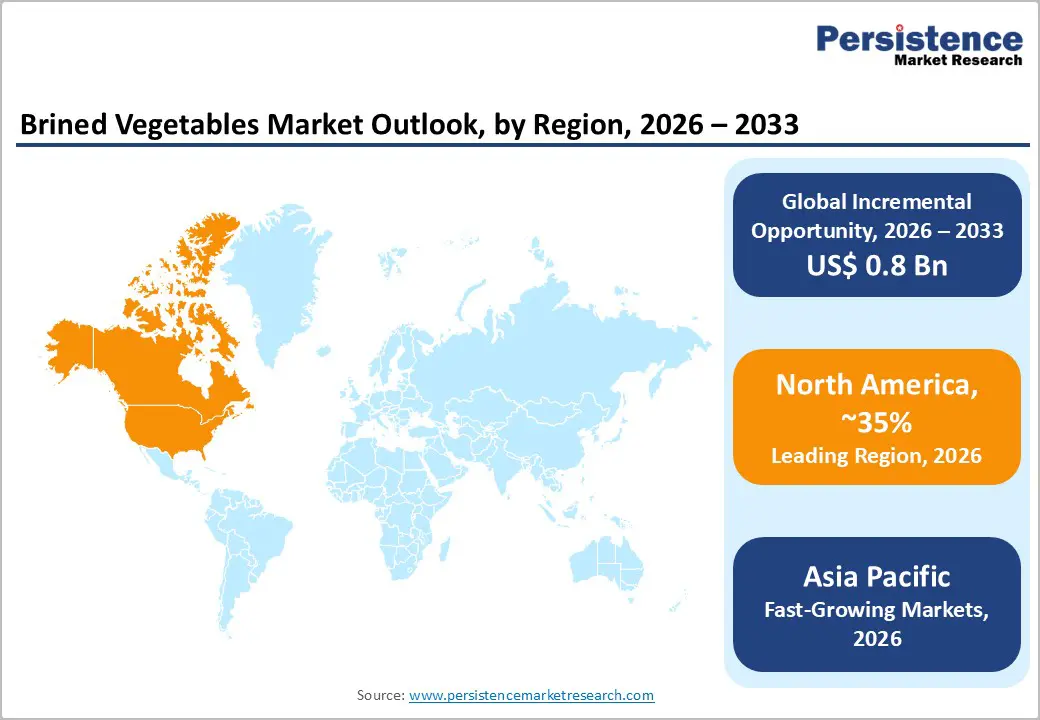

- Regional Leadership: North America is projected to retain the largest market value with 35% share in 2026, whereas the Asia Pacific is poised to be the fastest-growing region at 9% CAGR, driven by urbanization, rising incomes, and evolving dietary trends.

- Competitive Environment: Strategic developments include technology partnerships, mergers and acquisitions, and geographic capacity expansions, enabling companies to strengthen their presence and capture growth in emerging and mature markets.

| Key Insights | Details |

|---|---|

| Brined Vegetables Market Size (2026E) | US$ 2.0 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

DRO Analysis

Driver - Rising Consumer Demand for Convenience and Health-Oriented Foods

Consumers increasingly favour convenience combined with wellness, reshaping food purchase decisions and elevating demand for portable, long-lasting products. Functional food trends in 2026 highlight a strong emphasis on items that support digestion, immunity, and overall well-being, such as fibre-rich and fermented foods, driven by evolving lifestyle preferences and health awareness worldwide. This shift is reinforced by mainstream media coverage linking fermented and gut-friendly foods to broader nutrition trends, elevating their cultural relevance. The appeal of brined vegetables stems from their ready-to-eat convenience, natural preservation, and enduring flavour profiles, making them attractive across both traditional retail and modern foodservice channels. This broad consumer shift is expanding category acceptance beyond niche markets into everyday grocery baskets, supporting sustained consumption.

The growing appreciation for gut health and functional nutrition is not just anecdotal. Media and industry reporting in 2025 confirmed that fermented foods had become a recognized lifestyle trend in markets like India, where urban populations are actively embracing them for their wellness benefits. This has helped reposition traditional pickles and fermented brassicas as value-added foods rather than simple condiments. In parallel, broader processed-food trends documented at the beginning of 2026 indicate that clean-label offerings, minimal processing, and natural ingredient profiles are reshaping product innovation and consumer perceptions.

Expansion of Retail Networks and Digital Sales Channels

The expansion of organized retail infrastructure and digital grocery platforms continues to amplify the distribution of brined vegetables, improving access and stimulating sales. News in 2025-2026 highlights aggressive growth in physical grocery footprints, such as large grocery chains planning nationwide expansion and extended retail hours, increasing consumer touchpoints and product visibility. These developments reflect broader retail strategies aimed at meeting growing demand for diverse, convenient food options. As retail footprints expand, brined vegetables benefit from greater shelf presence in supermarkets, hypermarkets, and specialty outlets, where shoppers increasingly prefer modern, health-oriented food assortments. The broader retail ecosystem’s push for omnichannel engagement deepens penetration across urban and suburban markets.

Simultaneously, the adoption of digital and quick commerce is transforming how consumers purchase groceries, with online platforms making fresh and preserved foods accessible at speed and scale. In India, for example, major grocers are investing in rapid delivery models that can fulfill orders within minutes, exemplifying how digital infrastructure is reshaping food accessibility and consumer convenience. This trend supports broader e-grocery adoption and aligns with global patterns of retail transformation, where integration between offline and online channels is becoming a core growth driver. By increasing product touchpoints and enabling seamless access through technology-enabled distribution, modern retail expansion and digital penetration are strengthening the market’s structural foundation and fueling long-term growth.

Restraint - High Production and Supply Chain Costs

Producing high-quality brined vegetables, particularly those using advanced preservation methods such as High Pressure Processing (HPP), requires substantial capital investment in specialized equipment, trained personnel, and extended processing time. These fixed costs raise per-unit costs relative to conventional products, narrowing producers' profit margins. Supply chain challenges are intensifying globally as shipping and energy costs surge due to geopolitical tensions, including conflict-related disruptions that have driven freight and fuel inflation and pushed food prices higher, according to the United Nations’ food price index. These cost pressures cascade through cold chain logistics, increasing refrigeration and transport expenses and squeezing margins further for producers dependent on temperature-controlled supply routes.

The cold chain infrastructure itself is under stress, with industry reports indicating ongoing challenges in temperature-controlled logistics that increase operational expenditure and downtime risks, especially for smaller operators. Maintaining precise temperature control to prevent spoilage remains costly due to aging facilities and high energy consumption needs. The combined impact of rising energy, logistics, and raw material expenses makes it more difficult for SMEs and regional producers to scale production or compete on price with larger manufacturers. This dynamic limits competitive parity, particularly in markets where cost structures are already tight, and affects decisions on new process adoption or capacity expansion, as producers seek to balance investment risk with volatile supply chain economics.

Regulatory Compliance and Labeling Complexity

Brined and fermented vegetable products must comply with detailed food safety and labeling regulations across major markets, presenting a compliance burden that stretches operational resources. In 2026, India’s food safety regulator FSSAI implemented stricter rules requiring scientific evidence to support product safety claims, marking a shift toward more rigorous oversight for new food offerings. Such rules require manufacturers to invest in documentation, testing, and risk assessment capabilities, thereby increasing upfront compliance costs and extending time-to-market for new or reformulated products. This regulatory complexity is mirrored globally, where producers must adapt to divergent labeling standards for nutritional content, allergens, and allowable claims in regions such as North America, Europe, and the Asia Pacific.

Ongoing amendments to food standards, such as updated compositional definitions and purity benchmarks, add another layer of compliance needs that require dedicated quality and legal resources. For companies selling across borders, tailoring labels and documentation to meet each jurisdiction’s criteria significantly increases administrative workload and expense, reducing pricing flexibility. This regulatory pressure disproportionately impacts smaller companies that lack the scale of compliance teams, slowing product launches and complicating global distribution strategies, ultimately dampening broader market responsiveness.

Opportunities - Growth in Emerging Markets and Expanding Retail Access

Emerging economies continue to offer strong growth opportunities as consumer demand for packaged and convenient foods expands across regions such as Latin America, Africa, and Asia. Retail infrastructure is evolving rapidly as major grocery chains and digital platforms strengthen distribution networks worldwide. For example, discount grocer Aldi announced plans to open over 180 new stores in the U.S. in 2026 amid shifting consumer habits toward value-oriented grocery spending, signaling broad demand for a diverse range of food products. Expansion in physical retail formats increases retail accessibility, especially in urban and suburban markets where consumers seek convenience and variety.

Parallel to store expansion, online grocery and rapid delivery services are reshaping food purchasing behavior, creating new pathways for brined vegetables to reach diverse consumer segments. In the UK, Tesco’s rapid-delivery service ‘Whoosh’ is expanding rapidly, integrating online and physical retail to capture evolving grocery demand, reflecting broader global momentum toward digitally enabled convenience shopping. In South Africa, online grocery sales are expected to account for an increasing share of total retail turnover, highlighting the growing role of digital channels in driving food category growth. These trends suggest that manufacturers who align their distribution strategies with expanding physical and digital retail access can unlock significant market potential across both emerging and developed regions.

Consumer Behavior Shifts and Digital Retail Innovation

Shifts in consumer behavior toward convenience, digital shopping, and value-driven choices continue to create fertile ground for brined vegetable categories that offer ready-to-eat, flavorful, and nutrient-oriented options. Grocery trends in 2026 reflect evolving shopping patterns, with lower- and middle-income households driving growth in grocery visits and frequent purchases, indicating demand for affordable, accessible food products. At the same time, rapid innovation in e-grocery and hybrid retail models is reshaping fulfillment norms, with major retailers investing in omnichannel delivery and inventory integration, as evidenced by online grocery profitability improvements reported by large chains.

Digital transformation in retail is also enhancing how consumers discover, order, and receive food products, strengthening engagement with brands that leverage these capabilities. Global quick commerce and instant fulfillment models are accelerating expectations for convenience, while broader online grocery adoption is supported by major players integrating rapid delivery services with traditional retail footprints. This evolution in digital retail infrastructure enables brined vegetable manufacturers to expand reach via omnichannel strategies, subscription offerings, and personalized e-commerce experiences. By tapping into evolving consumer priorities centered on convenience, value, and digital-first access, businesses can accelerate category penetration and build enduring customer loyalty in dynamic grocery ecosystems.

Category-wise Analysis

Product Type Insights

Pickles are expected to be the leading product type, estimated to account for approximately 38% of global brined vegetable revenue in 2026, serving as versatile condiments and ready-to-eat snacks with strong shelf stability and flavour retention. Their mass-market appeal is reinforced as pickled cucumbers and other brined products feature prominently in mainstream 2026 food trends, including snacks, beverages, and flavor-centric dishes. Supermarkets, convenience stores, and online platforms maintain broad distribution, while inclusion in meal kits strengthens repeat purchases.

Flavour innovation, including sweet-meets-spicy profiles and bold “swicy” trends, attracts new consumer segments. Pickles blend traditional familiarity with culinary novelty, evolving into a core ingredient in modern dishes. These dynamics sustain leadership, drive revenue growth across geographies, and enhance brand visibility in both emerging and mature markets.

Brined olives are anticipated to be the fastest-growing product type, with a CAGR of 6.5% through 2033, driven by rising global interest in Mediterranean diets, premium snacking, and restaurant menu incorporation. Higher per-unit pricing and health benefits, including antioxidants and dietary fats, appeal to conscious consumers.

Expanded online and specialty retail distribution enhances visibility, while marinated, stuffed, and infused varieties encourage trial. Culinary adoption in global dishes and premium positioning support growth across mature and emerging markets. Innovation in flavour, packaging, and portion formats accelerates adoption, making brined olives a key driver of market expansion. The segment also benefits from increased consumer education on heart-healthy diets and functional snacking trends, supporting sustained premium demand.

Brining Process Insights

Traditional brining is likely to remain the dominant process, capturing roughly 42% of brining process revenue in 2026, valued for cost efficiency, authentic flavour, and alignment with heritage perceptions. Widely applied across pickles, fermented brassicas, and root vegetables, it supports large-scale production without advanced equipment. Retailers and foodservice rely on traditionally brined products for predictable shelf life and consistent flavour profiles. Heritage and nostalgia appeal, combined with rising interest in fermentation, reinforce consumer adoption.

Traditional methods maintain strong positioning as everyday staples while supporting predictable revenue streams globally. This enduring relevance is further strengthened by the integration of traditional brined products into modern meal solutions and fusion cuisines.

High-Pressure Processing (HPP) and advanced preservation methods are projected to be the fastest-growing brining techniques, with a 7% CAGR through 2033, offering extended shelf life, nutrient retention, and clean-label appeal. Adoption is rising among premium brands and in regions prioritizing food safety and minimally processed foods. Modern HPP equipment integrates with automated production lines, improving efficiency and regulatory compliance. Functional food trends and health-conscious consumer demand drive trial, while enhanced freshness and texture differentiate offerings.

Innovation in HPP-enabled products supports premium positioning and global market expansion, accelerating adoption relative to traditional brining. Increasing interest in sustainable packaging and energy-efficient processing further reinforces the growth potential of HPP methods in 2025 - 2026.

Regional Insights

North America Brined Vegetables Market Trends

North America is the largest regional market for brined vegetables, holding an estimated 35% of global revenue share in 2026, largely driven by the United States and Canada. Traditional condiments such as pickles have become cultural staples, deeply integrated into fast-food, casual dining, and everyday meals, a trend highlighted by the “pickle era” surge in U.S. restaurants and grocery aisles in 2025, when major chains expanded pickle-centric menu items. This cultural traction underscores widespread consumer engagement beyond basic consumption into mainstream culinary relevance. Consumer preferences are shifting toward convenience, clean-label products, and flavor-forward innovations, driving both retail and foodservice adoption.

Supermarkets, convenience stores, and online retail platforms anchor distribution, supported by mature infrastructure and advanced cold-chain logistics. Regional retail dynamics are bolstered by rising demand for artisanal and craft pickles with unique flavor profiles, while meal kit and ready-to-eat integrations reinforce repeat purchase patterns. Regulatory frameworks from federal food safety authorities shape product formulations, especially regarding sodium and labeling standards.

Competitive dynamics combine established players with a growing niche of small-batch producers, enhancing both variety and innovation. Strategic investments in in-store promotions and e-commerce integration support sustained market expansion and brand visibility.

Europe Brined Vegetables Market Trends

Europe represents one of the most established brined vegetable markets, with Germany, the U.K., France, and Spain driving consumption through both traditional and contemporary culinary practices. Germany is a major market for sauerkraut and other fermented brassicas, while Mediterranean regions exhibit high demand for olives, peppers, and regional specialties. European consumption patterns are influenced by deeply embedded food traditions that favor fermented and preserved vegetables as essential components of regional diets. Regional culinary tourism also encourages exploration of authentic local flavors, expanding interest in premium and artisanal products.

The regulatory environment shaped by EU food safety standards promotes quality assurance, traceability, and strict additive guidelines, prompting producers to innovate with reduced-sodium and clean-label products. European consumers are increasingly drawn to organic and locally sourced brined products, reflecting broader food sustainability trends supported by EU agricultural policies. Retail distribution balances supermarkets and specialty outlets, with gourmet and premium segments expanding through curated offerings.

Product diversification into ready-to-eat and artisanal formats enhances growth prospects. Premiumization, policy support, and evolving consumer expectations underpin steady regional expansion and investment in innovative packaging and preservation technologies.

Asia Pacific Brined Vegetables Market Trends

Asia Pacific is poised to be the fastest-growing region with 9% CAGR. The growth is supported by large population bases, rising disposable incomes, and evolving consumption patterns that blend traditional preservation with modern convenience. China and Japan maintain high baseline demand for pickled and fermented products, while social and economic shifts encourage packaged and branded offerings. Urbanization, rise in middle-income groups, and lifestyle changes are the primary growth factors. Expanding awareness of the health benefits of fermented foods further fuels adoption across multiple demographic groups.

Retail expansion, including modern supermarkets and e-commerce grocery platforms, has improved access in urban and semi-urban markets. India’s growing urban food demand and ASEAN’s dynamic consumer segment further accelerate market growth. Companies are investing in localized product development and distribution infrastructure to cater to diverse tastes and compliance requirements. Regulatory frameworks vary, but localized manufacturing advantages, cost competitiveness, and cultural alignment with fermented foods support long-term expansion. Integration of convenience formats, ready-to-eat offerings, and premium product lines strengthens market penetration and revenue growth across the region.

Competitive Landscape

The global brined vegetables market is moderately consolidated, with top players such as McCormick & Company, Kraft Heinz, Bonduelle, Del Monte, and FrieslandCampina controlling over half of revenue. These companies leverage broad distribution across supermarkets, convenience stores, specialty outlets, and online platforms. They invest in product innovation, advanced preservation technologies, and flavor diversification to maintain leadership. Strong brand equity and regulatory compliance capabilities support premium positioning. Strategic R&D ensures alignment with health trends and evolving consumer preferences.

Regional and niche players, including artisanal producers and local fermentation specialists, focus on innovative recipes and culturally aligned products. Regulatory complexity, supply chain challenges, and labeling compliance create barriers for new entrants. Digitalization and e-commerce growth enable smaller brands to expand reach efficiently. Market consolidation is expected to rise via M&A and strategic partnerships, while niche players capture share with unique flavors and health-oriented offerings.

Key Developments:

- In March 2026, McCormick and Unilever announced a US$ 44.8 billion merger of Unilever’s Foods business with McCormick, creating a global flavor and condiments leader with brands like Knorr, Hellmann's, and Frank's RedHot. The deal allows Unilever to focus on Personal Care while McCormick dominates the spices, sauces, and condiments segment.

- In March 2026, Olive My Pickle opened a new "pickle superstore" featuring over 40 fermented products and grab-and-go offerings, reflecting growing consumer demand for probiotic-rich and experiential retail experiences. This expansion reinforces local community roots and builds on prior success in Jacksonville.

Companies Covered in Brined Vegetables Market

- The Kraft Heinz Company

- Conagra Brands, Inc.

- Mt. Olive Pickle Company, Inc.

- Del Monte Foods, Inc.

- B&G Foods, Inc.

- ADF Foods Ltd.

- Pinnacle Foods

- Grillo’s Pickles

- Bubbies

- Claussen

- McClure’s Pickles

- Ripon Pickle Co. Inc.

Frequently Asked Questions

The brined vegetables market is projected to reach US$ 2.0 billion in 2026.

Rising demand for convenient, shelf-stable, and health-oriented vegetable products drives growth.

The market is expected to grow at a CAGR of 4.7% from 2026 to 2033.

Expansion in emerging markets and adoption of advanced brining technologies offer significant growth potential.

The leading players include Kraft Heinz, Conagra Brands, Mt. Olive Pickle Company, Del Monte Foods, and B&G Foods.