- Biotechnology

- Porcine Vaccines Market

Porcine Vaccines Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Porcine Vaccines Market by Vaccine Type (Live Attenuated, Inactivated), Disease Indication (Porcine Circovirus Type 2 (PCV2), Others), Route of Administration, End-user (Commercial Pig Farms, Veterinary Hospitals & Clinics), and Regional Analysis for 2025 - 2032

Porcine Vaccines Market Size and Trends Analysis

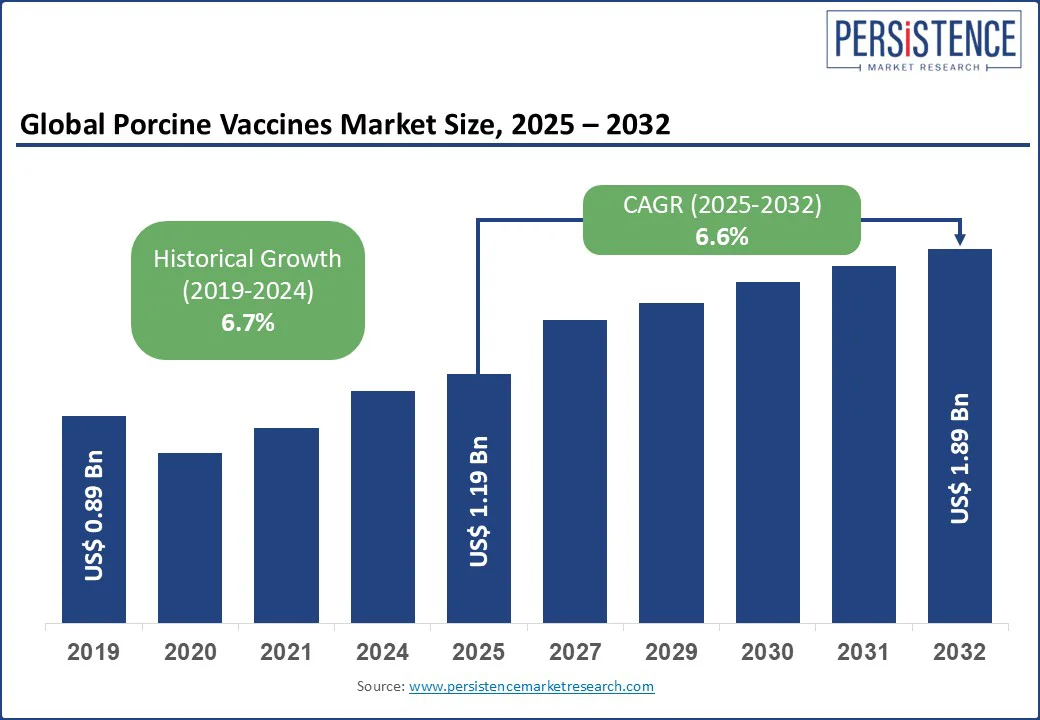

The global porcine vaccines market size is likely to be valued at US$ 1.19 Bn in 2025 and is expected to reach US$ 1.89 Bn 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032. The porcine vaccines market growth is driven by rising concerns over swine health and the increasing prevalence of viral and bacterial diseases in pigs. With the growing demand for safe and high-quality pork products, veterinary healthcare providers are focusing on preventive measures through vaccination programs.

The surge in global pork consumption, coupled with intensified commercial pig farming, is driving the adoption of swine disease prevention solutions across both developed and emerging markets. Advancements in vaccine technology, such as recombinant, DNA-based, and intradermal delivery systems, are reshaping disease control strategies in the livestock industry. Government initiatives, improved animal husbandry practices, and rising awareness about zoonotic disease transmission risks further contribute to the expanding market landscape.

Key Industry Highlights

- Porcine reproductive and respiratory syndrome (PRRS) is the leading segment, holding over 34% market share, driven by persistent outbreaks and demand for intradermal and mucosal vaccines with broader protection.

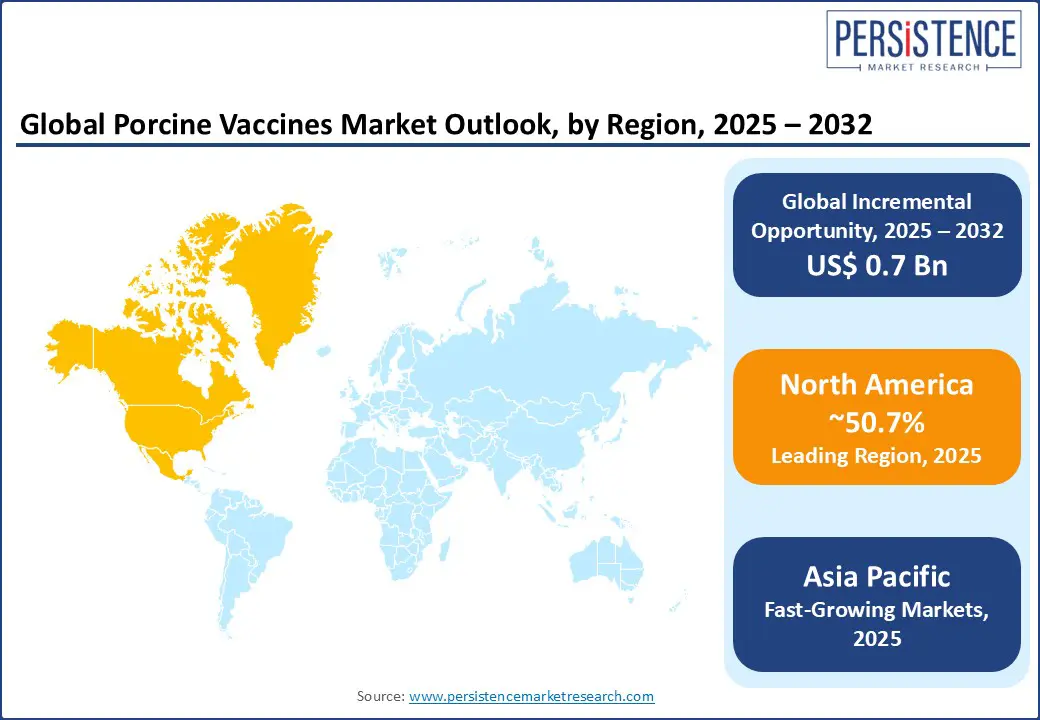

- North America is the largest regional market, accounting for over 50.7% of global revenue, backed by high vaccination rates and widespread use of needle-free delivery systems.

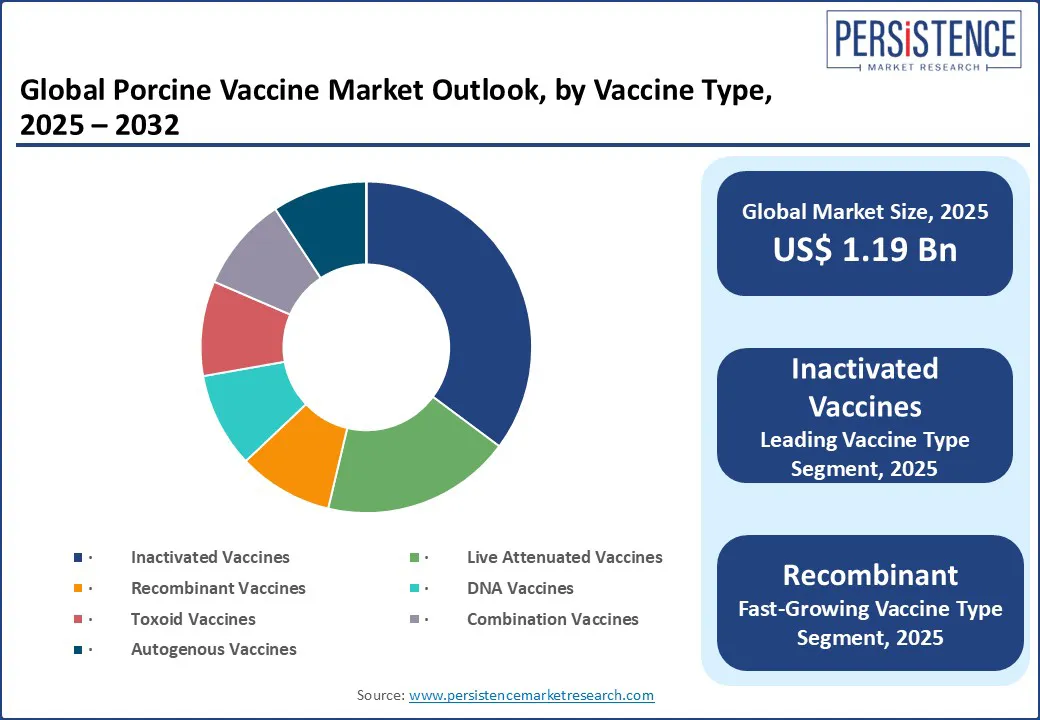

- Inactivated vaccines lead by type with 38% market share, though recombinant vaccines are gaining traction in high-biosecurity commercial farms for their precision and safety.

- Needle-free and oral delivery methods are seeing increased adoption, especially in large-scale farms prioritizing animal welfare and operational efficiency.

- Top players such as Boehringer, Zoetis, and MSD are investing in combo vaccines and digital tracking tools, improving real-time monitoring and farm-level immunity management.

|

Market Attribute |

Key Insights |

|

Porcine Vaccines Market Size (2025E) |

US$ 1.19 Bn |

|

Market Value Forecast (2032F) |

US$ 1.89 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.7% |

Market Dynamics

Driver - Technological Advancements in Swine Vaccination Boost Disease Control Efficiency

Vaccination against porcine reproductive and respiratory syndrome (PRRS) via needle-free intradermal delivery systems is increasingly adopted in commercial swine herds. This active immunization strategy sharply reduces viremia, reproductive losses, and piglet mortality. Farms invest in jet injector needle-free vaccine devices to improve animal welfare, eliminate broken needles risk, and ensure uniform antigen dosing. This uptake is particularly strong in PRRS-endemic regions where productivity gains directly boost profitability.

Rapid adoption of oral mass vaccination through drinking-water applicators is reshaping disease control in large pig farms. Producers facing labor shortages leverage water-based swine influenza vaccines to vaccinate thousands of pigs efficiently. This method lowers stress, improves biosecurity, and expands coverage in high-density operations. Injectable vaccine costs and logistics drive this shift, especially for enteric pathogen prevention in piglets.

Restraints - Uneven Antigen Stability in Delivery Systems and Vaccine Residue Formation at Injection Sites

Mass adoption of oral swine influenza vaccination through water-based applicators is being hindered by uneven antigen stability in delivery systems. In large farm settings, inconsistent water temperature and pH can degrade the live vaccine, reducing efficacy. Oral vaccine degradation by gastric enzymes often results in sub-protective dosage per piglet, making producers revert to injectables despite higher labor costs.

While needle-free jet injector intradermal vaccination of PRRS and PCV2 improves welfare, its success is limited by vaccine residue formation at injection sites. Around 20-30% of pigs show visible skin residue, requiring increased operator training to ensure correct depth and dosage, and increasing labor intensity per animal. High-pressure delivery may risk antigen degradation if device calibration slips, undermining immunogenicity and requiring re-dosing.

Opportunity - Innovative mRNA Vaccines and Needle-free Delivery Drive Swine Health Advances

Biotech leaders are now developing the mRNA-based PRRS mosaic vaccines combined with ASF epitope constructs, enabling broader protection across virus strains. These platforms can be rapidly updated using in silico design, responding to emerging variants. The room-temperature-stable DNA/mRNA swine vaccine formulations promise easier logistics in rural and tropical settings. These innovations can reduce vaccine rollout time from years to months, opening new commercial pathways.

Custom-tailored autogenous farm-specific porcine vaccines target local PRRS and PCV2 strains, enhancing herd immunity where commercial options fall short. Combining that with intranasal mucosal vaccination for PRRS can elicit both systemic and local defenses against respiratory pathogens. Deploying needle-free nasal spray swine vaccine devices accelerates on-farm administration and minimizes stress. These niche delivery methods improve coverage and support precision livestock health management.

Category-wise Analysis

Vaccine Type Insights

By vaccine type, the inactivated vaccines segment is projected to dominate, accounting for a market share of approximately 38%. These vaccines are widely used due to their favorable safety profile, especially for classical swine fever and porcine parvovirus control. Their stability in diverse farm conditions makes them suitable for mass vaccination programs in both developed and developing markets. Inactivated vaccines are often preferred in settings where cold chain maintenance is a challenge, offering better shelf life and handling flexibility. Many government-led animal health campaigns in regions such as Latin America and parts of Asia continue rely on these formulations due to their cost-effectiveness and proven efficacy.

Recombinant vaccines are emerging as the fastest-growing, particularly in regions battling emerging strains of PRRS and PCV2, due to their enhanced immunogenicity, antigen-specific responses, and adaptability. These vaccines are increasingly adopted in high-biosecurity commercial farms that require precision disease management. As genomic surveillance improves, recombinant platforms are also being used to develop next-gen multivalent vaccines, offering broader protection with fewer doses.

Disease Indication Insights

The porcine reproductive and respiratory syndrome (PRRS) vaccine segment is projected to lead, capturing around 34% of the total market share in 2025. PRRS remains one of the most economically devastating swine diseases globally, prompting widespread vaccination efforts across both commercial and smallholder farms. A rise in PRRS outbreaks globally, especially in North America and Asia, underlines the critical need for effective immunization. Innovations in needle-free and intradermal PRRS vaccines are helping reduce stress and tissue damage during administration, improving animal welfare and vaccine uptake.

Key players in the PRRS vaccine market include Boehringer Ingelheim, recognized for its widely used Ingelvac PRRS MLV and ongoing innovation in adjuvant systems to enhance vaccine efficacy. Zoetis Inc. offers both live and inactivated PRRS vaccines, along with combination platforms that integrate protection against multiple respiratory pathogens.

PCV2 (porcine circovirus type 2) vaccines are anticipated to be the fastest growing, given their role in controlling post-weaning multisystemic wasting syndrome (PMWS) and other associated conditions. These vaccines are especially critical in nursery and grower pigs, where mortality and production losses can be substantial. Cross-protection against new PCV strains is also becoming a focus area, especially in regions with high genetic diversity of the virus.

Leading producers such as Boehringer Ingelheim, Zoetis, and MSD Animal Health offer PCV2 vaccines as standalone or combination products (often with Mycoplasma hyopneumoniae or PRRS), providing broad-spectrum respiratory and systemic protection. Early-life vaccination, typically between three to five weeks of age, is common to ensure immunity before viral exposure peaks.

Regional Insights

North America Porcine Vaccines Trends

North America is projected to lead, contributing around 50.7% of the global revenue in 2025, with the U.S. being the largest contributor. High pork consumption, industrialized farming practices, and stringent animal health protocols drive this dominance. Routine immunization against PRRS, PCV2, and Mycoplasma is standard in over 80% of commercial pig farms. The adoption of needle-free intradermal devices and combination vaccines has increased due to growing animal welfare awareness.

In recent years, the U.S. has expanded use of intradermal and recombinant vaccine platforms such as Porcilis PRRS ID and Fostera Gold PCV MH, both FDA-approved and now widely deployed in commercial herds. Ongoing research collaborations between USDA and private firms are also exploring thermostable DNA vaccines for remote regions. Canada is also witnessing strong adoption of autogenous vaccines and DNA platforms, especially in disease-prone regions such as Quebec and Ontario, growing at a CAGR of nearly 7% from 2025 to 2032. Federal R&D funding has supported pilot trials of farm-customized PRRS vaccine strains, and provincial subsidies have accelerated uptake in smaller farms lacking herd immunity.

Asia Pacific Porcine Vaccines Trends

Asia Pacific is likely to be the fastest-growing region, with China representing over 50% of the region's porcine vaccine consumption, driven by its massive pork production and aggressive vaccination campaigns following ASF outbreaks. Over 88% of swine herds in China are vaccinated against PCV2 and PRRS. Vietnam, Thailand, and the Philippines have also rapidly adopted oral and intranasal vaccine delivery platforms in high-density farms, with India also ramping up demand through its national piggery development programs. Asia Pacific’s growth is further fueled by rising consumer demand for high-quality pork, increased awareness about zoonotic diseases, and government-backed disease eradication schemes.

Following ASF, China’s government has prioritized development and rollout of recombinant, intranasal, and mRNA-based PRRS and PCV2 vaccines. Provincial agriculture departments now enforce herd-level immunization tracking, and several biotech startups, including Boehringer Ingelheim China, are scaling up AI-supported vaccination compliance systems. Vietnam’s Ministry of Agriculture has led successful pilots of oral swine vaccination through feed or water, improving coverage and cost-efficiency. As part of its swine repopulation plan post-ASF, Vietnam has partnered with global firms to introduce thermostable PRRS vaccines, especially in its northern provinces where smallholder farming dominates.

Europe Porcine Vaccines Trends

The Europe porcine vaccines market is supported by expanding veterinary infrastructure and high biosecurity compliance across the EU. Spain, one of the largest pork producers in Europe, achieved 92% vaccination coverage for PCV2, resulting in a 19% decline in productivity losses related to porcine circovirus. Germany, accounting for about 20% of Europe’s porcine vaccine revenues, invests heavily in research, driving innovation in mRNA-based PRRS vaccines.

France and the Netherlands are expanding their use of combination and mucosal vaccines to reduce antimicrobial reliance. Overall, the region is projected to grow at a high CAGR during the forecast period, with demand increasing in both export-focused producers and smaller, organic farms using welfare-centric vaccination strategies.

Germany has intensified investments in mRNA and genotype-specific vaccines, following BioNTech’s 2025 acquisition of CureVac. Germany’s Fraunhofer Institute is also leading a consortium developing mucosal PRRS vaccines to tackle localized outbreaks. Spain’s swine sector is one of the EU's largest and has been transitioning to combination vaccines such as Circo/MycoReady and CEVA’s PCV2d formulations. These moves align with EU goals for reducing antibiotic use and increasing resilience against co-infections in intensive farms.

Latin America Porcine Vaccines Trends

Latin America is also emerging as a growth hotspot, with Brazil and Argentina leading the region, supported by their expanding commercial pork industries and export activities. Argentina recorded a 3.9% increase in pork production in 2022, largely due to disease control programs and improved vaccination coverage for swine flu and Mycoplasma. Brazil has also adopted autogenous and recombinant vaccines for region-specific strains of PRRS and PCV2. The use of combination vaccines in weaners and growing pigs is rising, especially in integrated production systems.

In addition to recombinant platforms, Brazil is focusing on autogenous vaccines tailored to regional strains, especially in the south. Key players have partnered with state agricultural boards to implement on-site disease surveillance and vaccine production clusters, which drastically reduce vaccine response lag. Argentina continues to improve productivity through genotype-specific Mycoplasma vaccines in commercial farms. It is also trialing thermostable liquid vaccines in rural areas to overcome infrastructure and cold-chain limitations, backed by public–private research grants.

Competitive Landscape

The global porcine vaccines market is moderately consolidated, with a few global players dominating and several regional manufacturers competing on price, disease specificity, and delivery innovation. The future competitive edge will hinge on next-gen platforms (mRNA), customized immunization programs, and non-invasive vaccine delivery technologies.

Leading players include Boehringer Ingelheim Animal Health, Merck Animal Health (MSD), Zoetis Inc., Ceva Santé Animale, and Elanco Animal Health, collectively accounting for more than 75% of the global revenue. These firms maintain competitive advantages through extensive product portfolios, strong distribution networks, and continuous investments in research and development, particularly in the areas of recombinant and combination vaccines.

Key Industry Developments

- In 2024, IIL launched a line of thermostable PCV2 and CSF vaccines optimized for tropical and rural environments, with minimal cold-chain dependency. This move is crucial for improving vaccine reach in remote pig-farming belts in South Asia and Africa.

- In 2023, Boehringer released an upgraded version of its PRRS vaccine in Europe, offering improved immune response and longer protection duration against evolving PRRSV strains. The vaccine is compatible with needle-free IDAL delivery systems, reinforcing welfare-oriented immunization protocols.

Companies Covered in Porcine Vaccines Market

- Boehringer Ingelheim Animal Health

- Merck Animal Health (MSD)

- Zoetis Inc.

- Ceva Santé Animale

- Elanco Animal Health

- Huvepharma

- HIPRA S.A.

- Indian Immunologicals Ltd.

- Phibro Animal Health Corporation

- Vetoquinol

- Biovet S.A. (part of Huvepharma Group)

- Biogenesis Bagó

- Ringpu

- Medion Farma Jaya

- Shanghai Veterinary Research Institute

- AVIVAC

- Agrovet Market Animal Health

Frequently Asked Questions

The porcine vaccines market is projected to reach US$ 1.19 Bn in 2025, driven by rising disease outbreaks and increased commercial pig farming.

The porcine vaccines market is expected to reach a valuation of US$ 1.89 Bn, growing at a steady pace, by 2032.

Key trends include the adoption of needle-free intradermal delivery systems, growth in farm-specific autogenous vaccines, and the emergence of mRNA-based swine vaccines for PRRS and ASF prevention.

By disease indication, PRRS (porcine reproductive and respiratory syndrome) dominates the market with the largest share due to its global prevalence and high economic impact.

The market is projected to grow at a CAGR of 6.6% from 2025 to 2032, supported by rising commercial pig populations and advancements in vaccine technology.

The major player include Boehringer Ingelheim Animal Health, Merck Animal Health (MSD), Zoetis Inc., Ceva Santé Animale, and Elanco Animal Health.