- Pharmaceuticals

- Bovine Vaccines Market

Bovine Vaccines Market Size, Share, and Growth Forecast 2026 - 2033

Bovine Vaccines Market by Vaccine Type (Live Attenuated, Inactivated, Toxoid, Subunit, DNA Vaccines), Disease Type (Foot-And-Mouth Disease, Brucellosis, Bovine Respiratory Disease, Others), End-User (Cattle Farms, Veterinary Clinics, Government Agencies), and Regional Analysis, 2026 - 2033

Bovine Vaccines Market Size and Trend Analysis

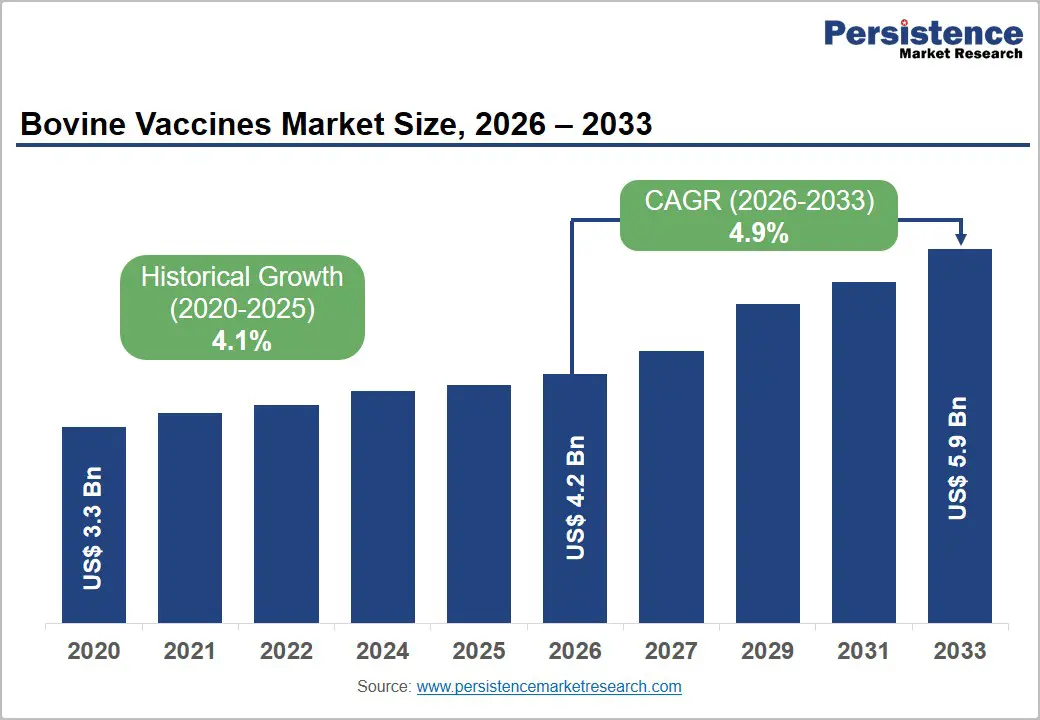

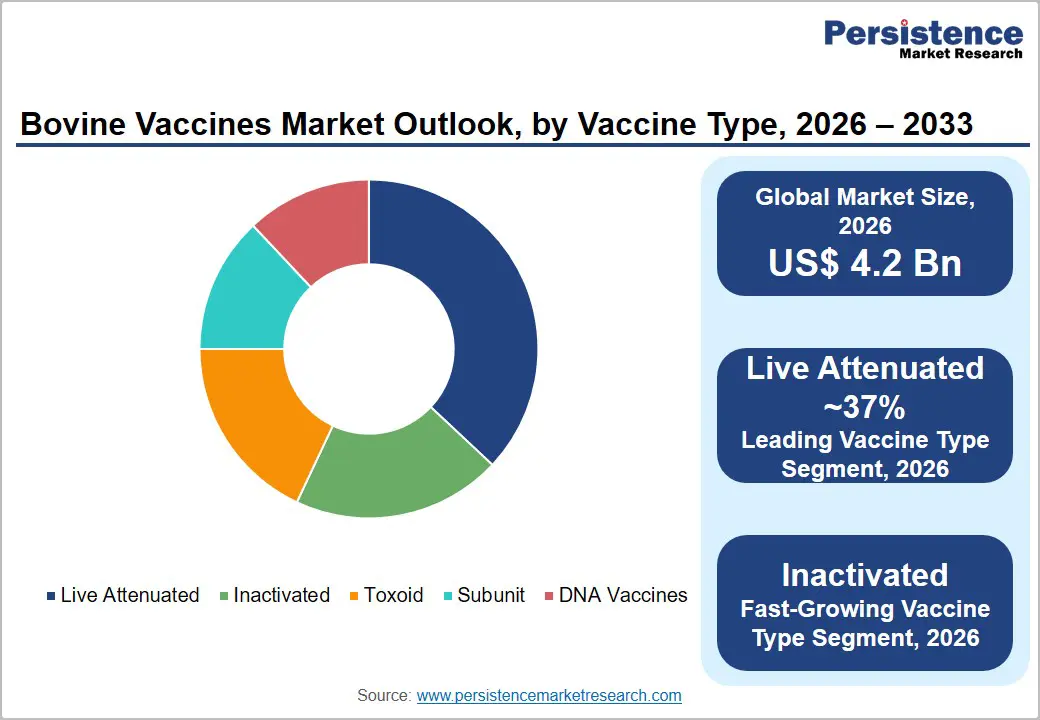

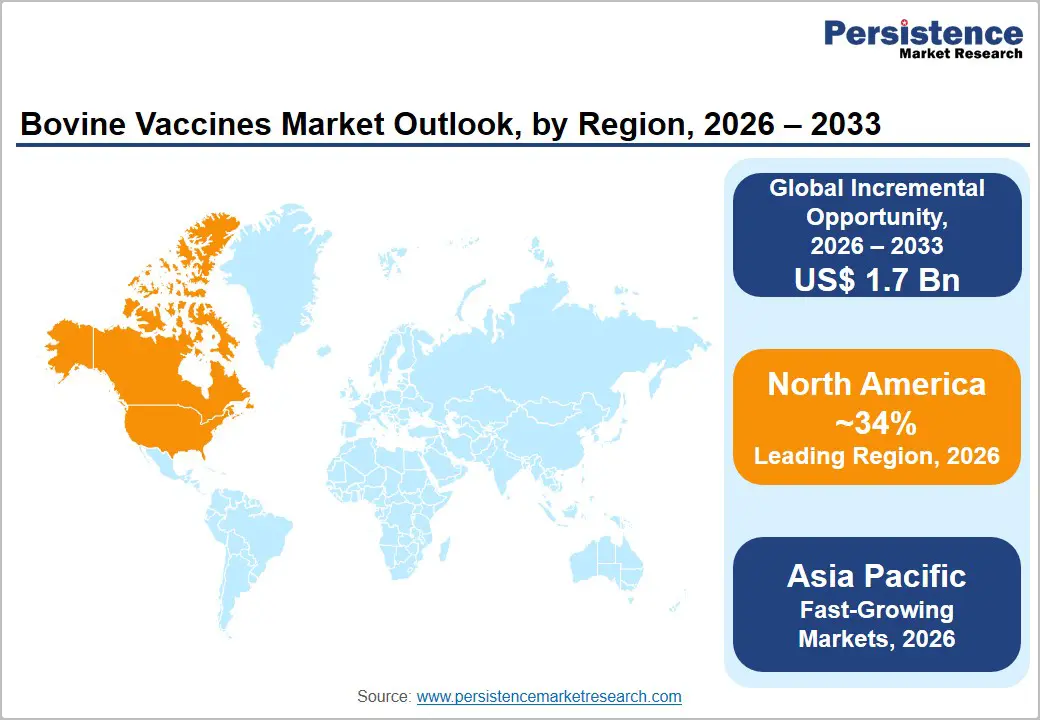

The global bovine vaccines market size is expected to be valued at US$ 4.2 billion in 2026 and projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The growing global beef and dairy consumption driving cattle herd expansion, intensifying government-mandated livestock vaccination programs targeting diseases with significant economic and zoonotic impact particularly Foot-and-Mouth Disease (FMD) and Brucellosis and the accelerating adoption of advanced inactivated and subunit vaccine platforms that offer improved safety and efficacy profiles. The Food and Agriculture Organization (FAO) estimates global cattle population at ~1 billion head, representing an immense and expanding base of animals requiring preventive immunization against economically devastating bovine diseases.

Key Industry Highlights:

- Leading Region - North America leads with 34% share, supported by large cattle population, high veterinary spending, and strong BRD vaccination programs in feedlots.

- Fast-Growing Market - Asia Pacific is likely to achieve a fast-growth due to India’s NADCP, China’s compulsory FMD vaccination programs, and massive cattle population requiring systematic immunization.

- Dominant Segment - Live attenuated vaccines dominate with 37% share due to strong immunity performance in BRD, IBR, and BVD prevention across cattle populations.

- Fast-Growing Segment - Inactivated vaccines grow fastest driven by export compliance needs, better safety, thermostability, and WOAH-supported FMD control strategies globally.

- Key Opportunity - India’s NADCP and China’s large-scale FMD vaccination programs create massive volume opportunities for domestic and global bovine vaccine manufacturers.

Market Dynamics

Drivers - Rising Global Protein Demand Expanding Cattle Herd Size and Vaccine Utilization

The increasing global demand for animal protein is significantly driving expansion in cattle herd sizes and boosting the need for comprehensive bovine vaccination programs worldwide. Rising incomes, urbanization, and growing middle-class populations across Asia Pacific, Latin America, and Africa are fueling higher consumption of beef and dairy products. According to the Food and Agriculture Organization, global meat demand is projected to rise by approximately 14% by 2030 compared to 2012 levels, with beef contributing a major share of this growth. This shift is encouraging the expansion of large-scale commercial cattle farming operations, particularly feedlots in the United States, Brazil, and Australia, where intensive production systems require routine and preventive vaccination programs.

In addition, high-density livestock farming increases disease transmission risk, making preventive immunization critical for maintaining herd productivity and economic efficiency. The United States Department of Agriculture estimates that bovine respiratory disease alone costs the U.S. cattle industry around US$ 900 million annually, highlighting the financial burden of untreated infections. This has led to widespread adoption of vaccines targeting respiratory, reproductive, and clostridial diseases. As cattle populations continue to grow and intensify globally, demand for bovine vaccines is expected to remain structurally strong across both developed and emerging livestock markets.

Restraints - Cold-Chain Logistics Challenges Limiting Vaccine Delivery in Emerging Markets

Cold-chain logistics limitations remain a major restraint in the bovine vaccines market, particularly across emerging and rural regions. Most live attenuated and inactivated vaccines require strict temperature control between 2°C and 8°C throughout storage and transportation to maintain efficacy. However, weak refrigeration infrastructure, unreliable electricity supply, and underdeveloped last-mile distribution networks across Sub-Saharan Africa, South Asia, and parts of Latin America significantly hinder vaccine accessibility. These regions also carry a high burden of diseases such as foot-and-mouth disease and brucellosis, further increasing unmet immunization needs. The World Organisation for Animal Health highlights cold-chain inadequacies as a key barrier to achieving global disease control and eradication targets, limiting effective vaccine deployment where it is most urgently required.

Opportunities - Inactivated Vaccines Driving Fastest Growth Through Safety and Trade Compliance

Inactivated bovine vaccines are emerging as the fastest-growing segment within the global bovine vaccines market, driven by their improved safety profile, regulatory acceptance, and suitability for international trade. Unlike live attenuated vaccines, inactivated formulations eliminate the risk of residual virulence, making them safer for use in large commercial herds. They also offer greater stability and are more compatible with stringent disease-free certification requirements imposed by global trade bodies. As a result, they are increasingly preferred in export-oriented cattle-producing countries seeking access to premium beef and dairy markets.

Furthermore, international organizations such as the World Organisation for Animal Health and the Food and Agriculture Organization recommend inactivated vaccines for use in foot-and-mouth disease control programs in disease-free zones. Leading animal health companies, including Zoetis and Boehringer Ingelheim, are investing in next-generation inactivated platforms with enhanced antigen potency and longer immunity duration. Growing demand from Latin America and Asia Pacific exporters aiming to meet global certification standards is expected to sustain strong long-term growth in this segment.

Category-wise Analysis

Vaccine Type Insights

Live attenuated vaccines hold the leading position in the bovine vaccines market by vaccine type, commanding ~37% revenue share in 2026. Live attenuated vaccines deliver robust, long-lasting immunity with typically a single or two-dose immunization schedule reducing labor costs and administration complexity in extensive cattle farming systems. They are the standard of care for a range of important bovine diseases including infectious bovine rhinotracheitis (IBR), bovine viral diarrhea (BVD), and several clostridial conditions.

The USDA reports that modified-live virus (MLV) vaccines a sub-category of live attenuated vaccines dominate U.S. bovine respiratory disease prevention programs due to their rapid immune response characteristics. Leading MLV products from Zoetis (Bovi-Shield Gold) and Merck Animal Health (Pyramid) sustain this segment's market leadership.

End-user Insights

Cattle farms represent the leading end-user segment in the bovine vaccines market, accounting for ~55% of revenues in 2026. Commercial cattle farms ranging from intensive feedlots to extensive range operations are the primary consumers of bovine vaccines, implementing comprehensive vaccination schedules that address respiratory, reproductive, and clostridial diseases endemic to their production systems.

The USDA National Agricultural Statistics Service (NASS) reports over 3.5 million cattle operations in the United States alone, with large commercial operations (500+ head) consuming the highest vaccine volumes per unit. The shift toward larger, more intensively managed commercial beef and dairy operations in Latin America, Australia, and Asia is concentrating purchasing power and driving volume-based vaccine procurement agreements with leading animal health companies.

Regional Insights

North America Bovine Vaccines Market Trends and Insights

North America leads the global bovine vaccines market with ~34% revenue share in 2026, driven by the largest commercially managed cattle sector in the world, comprehensive USDA CVB-regulated vaccine quality frameworks, and the highest per-head vaccination expenditure globally. BRD prevention and reproductive vaccine programs supported by extension services and veterinary prescription requirements sustain high and recurring vaccine utilization across the region's commercial feedlot and cow-calf operations.

U.S. Bovine Vaccines Market Size

The United States accounts for ~82% of North American bovine vaccine revenues in 2026, supported by a cattle population exceeding 93 million head according to the United States Department of Agriculture. High adoption of preventive animal healthcare practices, mandatory BRD vaccination protocols in commercial feedlots, and government-supported brucellosis vaccination programs continue driving strong vaccine demand. Major companies including Zoetis, Merck Animal Health, and Boehringer Ingelheim dominate the market with advanced bovine respiratory, reproductive, and infectious disease vaccines.

Europe Bovine Vaccines Market Trends and Insights

Europe is the second-largest bovine vaccines market, characterized by stringent EMA-regulated veterinary biologics standards, active brucellosis and tuberculosis eradication programs across member states, and high compliance with preventive veterinary health plans on commercial dairy and beef operations. EU regulations mandate periodic FMD contingency vaccination preparedness, sustaining institutional readiness vaccine stockpiles in member states.

Germany Bovine Vaccines Market Size

Germany is the largest bovine vaccines market in Europe, accounting for ~20% of regional revenues in 2026. The country’s highly productive dairy and beef sectors support extensive utilization of bovine respiratory disease (BRD), bovine viral diarrhea (BVD), and infectious bovine rhinotracheitis (IBR) vaccines. According to Destatis, Germany maintains ~3.8 million dairy cattle. Strict animal health regulations, strong veterinary healthcare infrastructure, and preventive livestock management practices continue supporting vaccine adoption. Major domestic and international manufacturers actively supply advanced bovine vaccines across Germany’s commercial cattle farming operations.

UK Bovine Vaccines Market Size

The United Kingdom accounts for ~12% of European bovine vaccine revenues in 2026, supported by strong veterinary disease management programs and advanced livestock healthcare infrastructure. The Veterinary Medicines Directorate regulates veterinary biologics and supports strict animal health compliance standards nationwide. Increasing concerns regarding bovine tuberculosis (bTB) outbreaks affecting thousands of cattle herds annually are driving demand for preventive vaccination programs and ongoing field trials.

Rising focus on cattle health, disease prevention, and productivity improvement continues supporting consistent bovine vaccine procurement across commercial dairy and beef farming operations throughout the UK.

France Bovine Vaccines Market Size

France represents ~16% of European bovine vaccine revenues in 2026, supported by one of Europe’s largest cattle farming industries. According to the French Ministry of Agriculture, the country maintains around 3.5 million beef cattle and 1.7 million dairy cattle. Government-supported disease surveillance programs, including brucellosis and tuberculosis control initiatives, continue driving strong bovine vaccine demand. Increasing adoption of preventive veterinary healthcare practices and EU-backed animal disease eradication programs further support consistent vaccine procurement across France’s commercial dairy and beef cattle farming sectors.

Asia Pacific Bovine Vaccines Market Trends and Insights

Asia Pacific is the fast-growing bovine vaccines market, anchored by India's 305 million cattle head (DAHD) and the government's massive NADCP vaccination initiative, and China's compulsory FMD vaccination programs covering hundreds of millions of cattle annually under provincial government mandates. Both markets offer enormous scale for domestic vaccine producers Indian Immunologicals, Hester Biosciences, and Chinese state-owned animal biologics companies alongside multinationals.

India Bovine Vaccines Market Size

India’s bovine vaccines market is valued at ~US$ 220 million in 2025, driven by the country’s massive livestock population and government-led vaccination initiatives. According to the Department of Animal Husbandry and Dairying, India maintains over 305 million cattle. The National Animal Disease Control Programme (NADCP) targeting foot-and-mouth disease and brucellosis vaccination across 500 million livestock animals is significantly boosting vaccine demand. Domestic manufacturers including Indian Immunologicals Ltd. and Hester Biosciences Ltd. dominate government vaccine supply contracts nationwide.

Japan Bovine Vaccines Market Size

Japan’s bovine vaccines market is valued at ~US$ 75 million in 2026, supported by advanced livestock healthcare management and strict disease prevention policies. According to the Ministry of Agriculture, Forestry and Fisheries of Japan, the country maintains ~2.5 million beef and dairy cattle. Japan’s strong focus on maintaining foot-and-mouth disease (FMD)-free status and ensuring livestock productivity continues driving demand for preventive bovine vaccination programs. Domestic manufacturers such as Kyoto Biken Laboratories play a key role in supplying bovine vaccines across the national livestock sector.

China Bovine Vaccines Market Size

China is one of the largest bovine vaccines markets in Asia Pacific, driven by extensive cattle farming operations and government-mandated livestock vaccination programs. The Ministry of Agriculture and Rural Affairs of the People's Republic of China oversees compulsory foot-and-mouth disease (FMD) vaccination programs covering millions of cattle annually. Rising demand for animal protein, expanding dairy and beef production, and increasing focus on livestock disease prevention continue supporting strong vaccine demand nationwide.

Domestic animal biologics manufacturers and multinational animal health companies are actively expanding bovine vaccine production and distribution across China’s rapidly modernizing livestock industry.

Competitive Landscape

The global bovine vaccines market is highly competitive, led by established pharmaceutical giants and supported by emerging regional players. Companies such as Zoetis Inc., Merck Animal Health, and Boehringer Ingelheim Animal Health dominate due to their extensive product portfolios, global distribution networks, and investments in next-generation vaccine technologies. These companies also focus on value-added services such as vaccine scheduling, traceability, and diagnostics to maintain long-term relationships with large cattle farms and veterinary networks.

Reflecting a widespread transformation, the market is moving toward thermostable formulations, autogenous vaccines, and digital integration, reflecting the industry’s response to region-specific challenges and demand for precise, scalable, and affordable cattle immunization solutions.

Key Developments:

- In February 2026, Zoetis Inc. announced the launch of bovine respiratory disease (BRD) genetic prediction capabilities in INHERIT® Select for commercial cow-calf operations, along with an upgraded INHERIT Connect test for seedstock producers.

- In January 2024, Kyoto Biken Laboratories, Inc. expanded its presence in the Middle East after receiving regulatory approval from UAE authorities for a suite of bovine vaccines, including Cattlewin-5k, Calfwin 6 Combo Live, and Ovine Ephemeral Fever Vaccine.

- In August 2024, Merck also secured authorization from the U.K. Veterinary Medicines Directorate (VMD) for the first-ever vaccine protecting cattle against cryptosporidiosis, a gastrointestinal disease with high morbidity in young calves, filling a major unmet need in calf health.

Companies Covered in Bovine Vaccines Market

- Zoetis Inc.

- Merck Animal Health (MSD)

- Boehringer Ingelheim Animal Health

- Ceva Santé Animale

- Elanco Animal Health

- Indian Immunologicals Ltd.

- Hester Biosciences Ltd.

- Bayer Animal Health

- Kyoto Biken Laboratories, Inc.

- Virbac

- Phibro Animal Health Corporation

- Biogenesis Bagó

- Brilliant Bio Pharma Pvt. Ltd.

- Hipra

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 4.2 billion in 2026.

Growth is driven by rising global meat demand, expanding cattle populations, and government-led FMD and brucellosis vaccination and eradication programs worldwide.

North America leads the market with strong cattle population, high veterinary spending, mandatory BRD vaccination programs, and advanced livestock healthcare infrastructure.

Key opportunities include large-scale vaccination programs in Asia Pacific and rising demand for inactivated vaccines driven by export compliance and disease control regulations.

Major players with strong product portfolios and global reach include Zoetis Inc., Merck Animal Health, Boehringer Ingelheim Animal Health, Ceva Santé Animale, Indian Immunologicals Ltd.