- Healthcare IT

- U.S. Triage System Market

U.S. Triage System Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

U.S. Triage System Market by System Type (Electronic Triage Systems, Paper-based Triage Systems, and Hybrid Systems), by Application (Emergency Services, Hospitals, and Military Healthcare), by End User (Hospitals & Clinics, Government Agencies, NGOs, and Others) Analysis from 2026 to 2033.

U.S. Triage System Market Share and Trend Analysis

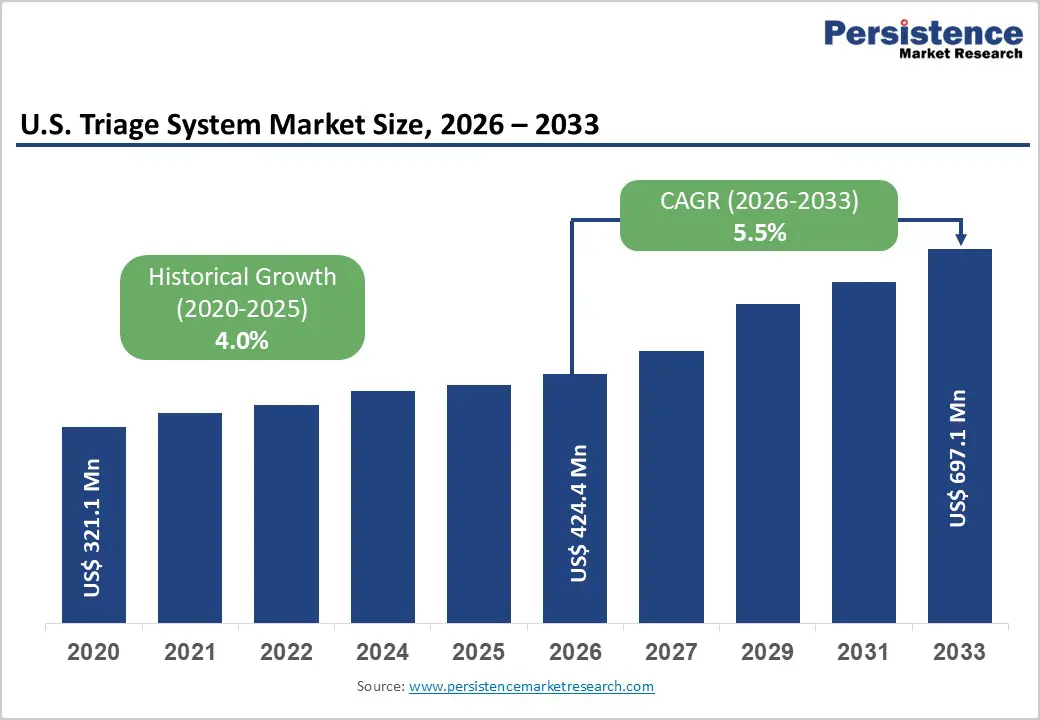

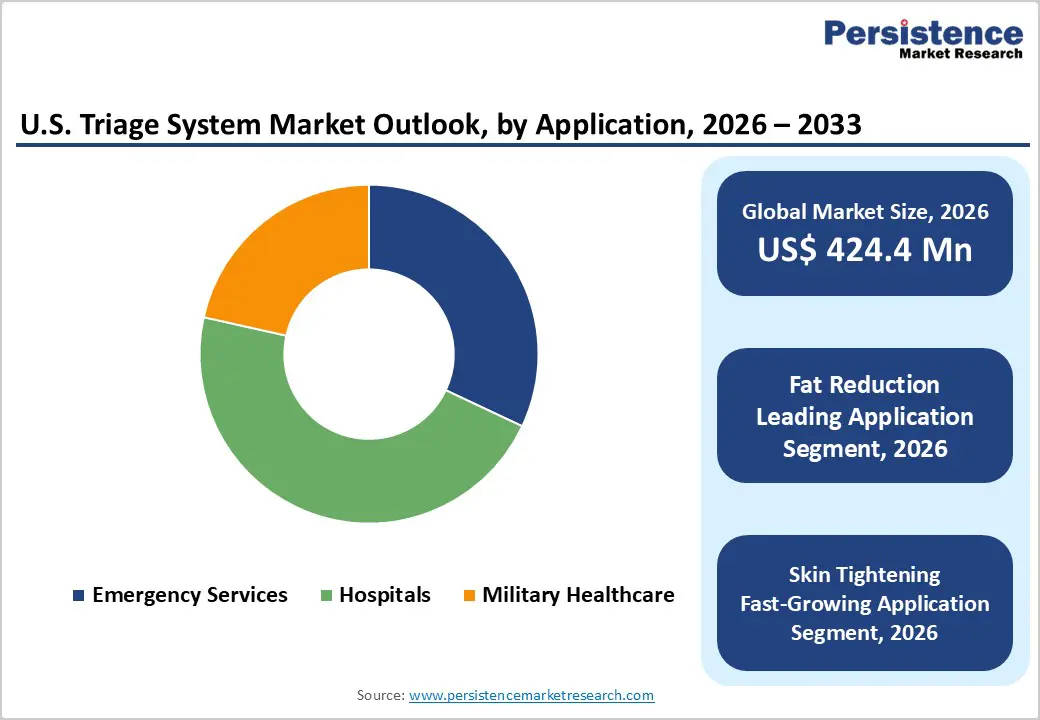

The U.S. triage system market size is estimated to grow from US$ 424.4 Mn in 2026 to US$ 697.1 Mn by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

Demand for triage systems in the U.S. is rising steadily, driven by growing emergency department congestion, increasing patient volumes, and heightened emphasis on timely clinical decision-making and patient safety. Hospitals, urgent care centers, and emergency medical services face continuous pressure to prioritize patients accurately, reduce wait times, and optimize resource allocation in high-acuity environments. An aging population, higher prevalence of chronic conditions, and frequent use of emergency care for non-emergent cases are significantly increasing the burden on frontline care settings.

Triage systems are increasingly deployed across hospitals, emergency rooms, telehealth platforms, and pre-hospital settings to standardize patient assessment, improve documentation accuracy, and support consistent acuity scoring. Providers are showing strong preference for digital, automated, and protocol-driven solutions that minimize human error and enhance throughput. Regulatory focus on quality metrics, patient safety reporting, and audit readiness further supports adoption. Advances in cloud-based deployment, AI-driven decision support, real-time alerts, and interoperability with EHRs are improving scalability and usability. Additionally, continued investment in U.S. healthcare IT infrastructure and expansion of virtual care models are reinforcing long-term demand for triage systems nationwide.

Key Industry Highlights

- Leading System Type Segment: Electronic triage systems dominates the market due to its central role in real-time clinical decision support, digital documentation, workflow standardization, and interoperability with hospital IT systems

- Fastest-Growing System Type Segment: Hybrid systems solutions are expanding rapidly as providers combine digital platforms with selective manual workflows to balance cost, flexibility, and clinical adoption.

- Leading Application Segment: Hospitals remains the top segment, driven by high emergency patient inflow, institutionalized triage protocols, and broad integration with emergency and inpatient care pathways.

- Fastest-Growing Application Segment: Emergency services is scaling quickly as EMS providers and emergency departments adopt real-time triage, analytics, and automation to improve response times and patient outcomes.

- Leading End User Segment: Hospitals & Clinics holds the largest share at 55.0%, supported by advanced healthcare infrastructure, high patient volumes, strict regulatory oversight, and widespread digital health adoption.

- Fastest-Growing End User Segment: Government Agencies is expanding fastest due to public health preparedness initiatives, emergency response modernization, and increasing use of standardized triage systems in disaster and community care settings.

| U.S. Market Attributes | Key Insights |

|---|---|

| U.S. Triage System Market Size (2026E) | US$ 424.4 Mn |

| Market Value Forecast (2033F) | US$ 697.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Dynamics

Driver – Rising Emergency Department Burden, Digital Health Adoption, and Focus on Timely Patient Prioritization

Growth is strongly supported by the increasing strain on U.S. emergency departments caused by rising patient inflow, aging populations, and higher prevalence of chronic and acute conditions. Emergency rooms and urgent care centers face persistent overcrowding, longer wait times, and clinician burnout, creating a critical need for structured and technology-enabled triage solutions. Triage systems help standardize patient prioritization, reduce subjective decision-making, and ensure that high-acuity cases receive immediate attention. The shift toward digital health infrastructure across U.S. hospitals further accelerates adoption, as triage platforms integrate seamlessly with electronic health records, clinical decision support tools, and hospital information systems.

Regulatory emphasis on patient safety, documentation accuracy, and quality-of-care metrics also reinforces demand, as digital triage supports auditability and protocol adherence. Additionally, the expansion of telehealth and nurse-led tele-triage services is driving demand beyond physical emergency rooms. Healthcare providers increasingly rely on triage systems to optimize staff utilization, reduce left-without-being-seen rates, and improve throughput. As hospitals focus on value-based care and operational efficiency, triage systems are becoming essential tools for managing patient flow and clinical risk in high-pressure care environments.

Restraints – Budget Constraints, Change Management Challenges, and Interoperability Limitations

Adoption remains constrained by financial and operational barriers, particularly among small hospitals, rural facilities, and community-based care providers. Implementing advanced triage platforms involves costs related to software licensing, system configuration, cybersecurity compliance, and staff training, which can be difficult to justify in cost-sensitive settings. Beyond capital investment, workflow disruption poses a significant challenge. Introducing new triage systems often requires changes in clinical protocols, staff roles, and documentation practices, leading to temporary productivity losses and resistance from clinicians accustomed to traditional methods. Human factors, such as trust in automated scoring and alert systems, can further slow acceptance.

Technical interoperability issues also limit penetration. Not all triage solutions integrate smoothly with legacy EHRs, emergency department dashboards, or regional health information exchanges, creating data silos and duplication of effort. Concerns around data privacy, HIPAA compliance, and cybersecurity risks associated with cloud-based triage platforms add another layer of complexity. Additionally, inconsistent reimbursement frameworks for digital and tele-triage services reduce return-on-investment clarity. These combined financial, cultural, and technical barriers continue to slow adoption across certain segments of the U.S. healthcare system.

Opportunity – Expansion of Tele-Triage, AI-Driven Decision Support, and Community Care Integration

Strong growth opportunities are emerging from the rapid expansion of telehealth and virtual care models across the U.S. Tele-triage solutions enable nurses and clinicians to assess patient urgency remotely, reducing unnecessary emergency department visits and improving access to care in underserved regions. This trend is particularly relevant for payer-driven care models focused on cost containment and preventive intervention. Technological advancements present another major opportunity. Artificial intelligence and machine learning are increasingly being integrated into triage platforms to enhance acuity prediction, symptom assessment, and risk stratification, supporting more consistent and data-driven decisions. These capabilities are valuable in high-volume emergency settings as well as call centers and remote monitoring programs.

Growing emphasis on community-based care and urgent care networks also creates demand for interoperable triage systems that operate across multiple entry points into the healthcare system. Cloud-native, subscription-based platforms allow scalable deployment across hospital systems, outpatient clinics, and emergency medical services. Additionally, government preparedness initiatives for disaster response and public health emergencies highlight the importance of standardized triage tools. Strategic partnerships between health systems, technology vendors, and telehealth providers are expected to further unlock long-term growth potential.

Category-wise Analysis

By System Type, Electronic Triage Systems Lead Due to Real-Time Decision Support and Digital Workflow Integration

Electronic triage systems are projected to dominate the U.S. triage system market in 2026, accounting for a revenue share of 52.3%. Their leadership is driven by the growing need for centralized clinical data access, rapid patient prioritization, and standardized triage protocols in high-acuity settings such as emergency departments, urgent care centers, and trauma units. These systems enable real-time patient assessment, automated acuity scoring, clinical alerts, and decision-support algorithms that significantly reduce waiting times and variability in care delivery. Seamless integration with electronic health records (EHRs), hospital information systems, and tele-triage platforms improves documentation accuracy and care continuity across departments. The shift toward contact-minimized workflows and digital-first emergency care models has further accelerated adoption, particularly after the COVID-19 pandemic. Cloud-based architectures, scalability across multiple facilities, and interoperability with existing IT infrastructure make electronic triage systems attractive to both large hospital networks and outpatient providers. As U.S. healthcare systems prioritize speed, accuracy, and data-driven patient flow optimization, electronic triage systems continue to command the largest share within the system type segment.

By Application, Hospitals Lead Due to High Patient Inflow and Institutionalized Emergency Care Protocols

The hospitals segment is expected to dominate the U.S. triage system market in 2026, capturing a revenue share of 46.5%. This dominance is primarily attributed to consistently high patient volumes, especially in emergency departments, and the widespread institutional adoption of structured triage protocols. Hospitals rely heavily on triage systems to manage overcrowding, prioritize critical cases, and allocate clinical resources efficiently in time-sensitive environments. Advanced triage solutions support rapid clinical assessments, standardized scoring frameworks, and integration with downstream care pathways, helping hospitals reduce delays and improve outcomes. In addition, hospitals benefit from economies of scale, enabling faster implementation of digital triage platforms across multiple departments, including emergency rooms, inpatient units, and observation wards. Regulatory expectations around patient safety, documentation accuracy, and quality metrics further reinforce adoption. Compared to other care settings, hospitals also demonstrate higher readiness for integrating triage systems with EHRs, analytics tools, and population health platforms. As emergency department utilization continues to rise nationwide, hospitals remain the leading application segment for triage systems.

By End User, Hospitals Lead Due to Clinical Complexity, Compliance Needs, and Care Coordination Requirements

Hospitals are projected to dominate the U.S. triage system market in 2026, accounting for a revenue share of 55.0%. This leadership is driven by the complexity of hospital care delivery, where diverse patient populations, high-acuity cases, and multidisciplinary coordination demand robust triage infrastructure. Hospitals manage large-scale emergency operations that require accurate patient prioritization, rapid decision-making, and continuous communication across clinical teams. Triage systems help hospitals streamline patient flow, reduce overcrowding, and ensure timely intervention for critical cases, directly supporting patient safety and operational efficiency. Moreover, hospitals face stringent regulatory, accreditation, and reporting requirements, making standardized and auditable triage processes essential. Large hospital systems are also more likely to invest in enterprise-wide triage platforms that integrate emergency services, inpatient units, and digital health tools. While government agencies and NGOs increasingly deploy triage solutions for public health and disaster response, hospitals remain the primary revenue contributors due to their scale, complexity, and ongoing need for advanced clinical triage capabilities.

Market Competitive Landscape

The U.S. triage system market is highly competitive, with strong participation from companies such as Philips Healthcare, Siemens Healthineers, TriageLogic, eClinicalWorks, and HGS Healthcare. These players leverage extensive U.S. and global distribution networks, strong brand recognition, and diversified digital health and clinical workflow portfolios to address the growing demand for rapid patient assessment, care prioritization, and operational efficiency across emergency departments, hospitals, and pre-hospital care settings.

Their offerings emphasize system reliability, data accuracy, real-time decision support, ease of integration with hospital IT systems (EHRs, HIS), and adaptability across multiple care environments including emergency rooms, urgent care centers, tele-triage platforms, and ambulatory settings. Continuous technological innovation, regulatory compliance (HIPAA and interoperability standards), cybersecurity, validation of clinical decision accuracy, and adherence to national healthcare quality and safety guidelines remain critical for maintaining competitive positioning in the U.S. triage system market.

Key Industry Developments:

- In January 2026, the U.S. Food and Drug Administration (FDA) cleared Aidoc’s expanded AI-based triage system, BriefCase, adding 11 new indications. Powered by the CARE Foundation Model, the solution consolidates 14 abdomen CT triage indications into a single workflow, enabling earlier identification of time-critical cases and helping reduce emergency department imaging backlogs and overcrowding.

- In November 2023, GE HealthCare announced U.S. FDA 510(k) clearance for Critical Care Suite 2.1, an industry-first solution featuring an enhanced pneumothorax (PTX) algorithm. The update strengthens on-device triage by enabling immediate detection and notification of PTX, along with visual overlay support on both the device and PACS to aid accurate localization and faster clinical decision-making.

Companies Covered in U.S. Triage System Market

- Philips Healthcare

- Siemens Healthineers

- TriageLogic

- eClinicalWorks

- HGS Healthcare

- Cerner Corporation

- Epic Systems Corporation

- Allscripts Healthcare Solutions

- McKesson Corporation

- GE Healthcare

- TeleTracking Technologies

- Meditech

Frequently Asked Questions

The U.S. triage system market is projected to be valued at US$ 424.4 Mn in 2026.

Rising demand for efficient emergency and patient management systems, rapid adoption of digital health/AI-enabled triage solutions, government initiatives promoting healthcare digitization, and increasing emergency department patient volumes due to aging populations and chronic disease prevalence.

The U.S. triage system market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Integration of AI, cloud-based and IoT-enabled tracking solutions to improve inventory management, predictive analytics, interoperability, and operational efficiency in healthcare facilities.

Philips Healthcare, Siemens Healthineers, TriageLogic, eClinicalWorks, and HGS Healthcare are some of the key players in the body U.S. triage system market.