- Medical Devices

- U.S. Ophthalmic Diagnostic Equipment Market

U.S. Ophthalmic Diagnostic Equipment Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

U.S. Ophthalmic Diagnostic Equipment Market by Product (Optical Coherence Tomography (OCT), Tonometer, Slit Lamp, Fundus Cameras, Perimeters, Corneal Topography, and Others), End-user (Hospitals, Ophthalmic Clinics, and Ambulatory Surgical Centers (ASCs), and Regional Analysis from 2025 - 2032

U.S. Ophthalmic Diagnostic Equipment Market Share and Trends Analysis

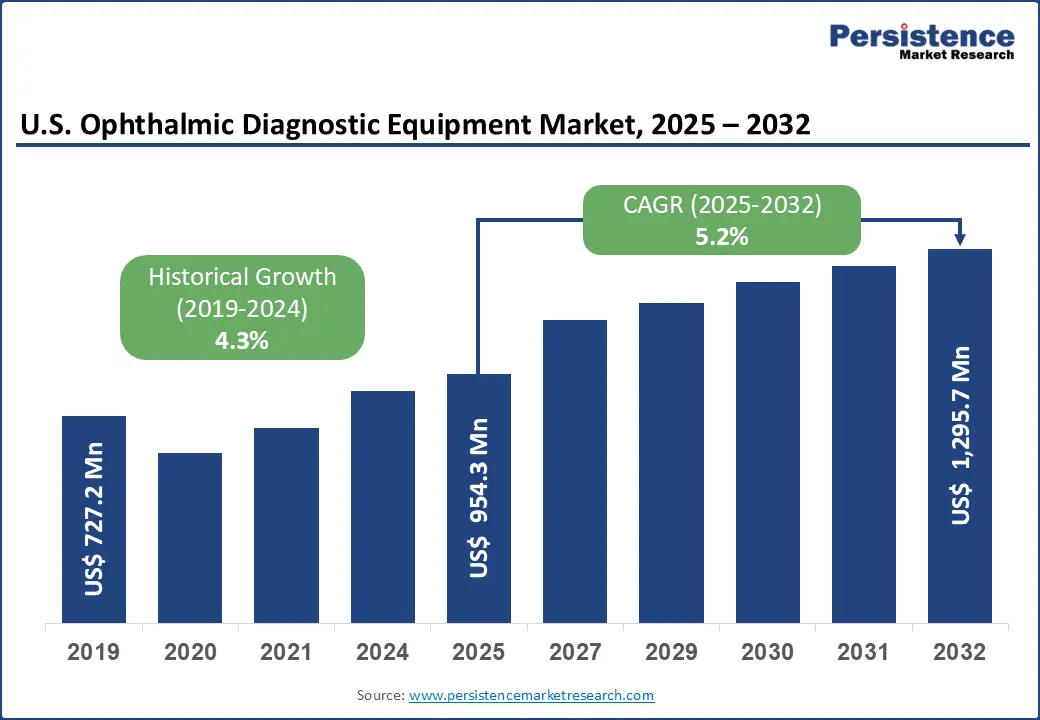

The U.S. ophthalmic diagnostic equipment market size is likely to be valued at US$954.3 Mn in 2025 and is expected to reach US$1,295.7 Mn by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032.

The U.S. ophthalmic diagnostic equipment market is witnessing steady growth, driven by the rising prevalence of eye disorders such as cataracts, glaucoma, and retinal diseases, alongside an increasing volume of ophthalmic surgeries.

The aging population, particularly those above 60 years, is a key factor contributing to higher incidences of vision-related conditions, which in turn fuels demand for advanced diagnostic tools. Technological advancements, including Optical Coherence Tomography (OCT), AI-enabled imaging, and digital fundus cameras, are improving diagnostic accuracy, efficiency, and early detection of ocular diseases.

Hospitals, ophthalmic clinics, and ambulatory surgical centers are increasingly adopting these innovations to streamline workflows and enhance patient outcomes. In addition, rising awareness about eye health, preventive care, and accessibility of ophthalmic services across urban and semi-urban regions further supports market growth.

Key Industry Highlights:

- Leading Zone: West U.S., 27% market share in 2025, underpinned by a high prevalence of age-related eye diseases, strong healthcare infrastructure, and the presence of leading research and academic institutions driving adoption of advanced ophthalmic diagnostic equipment.

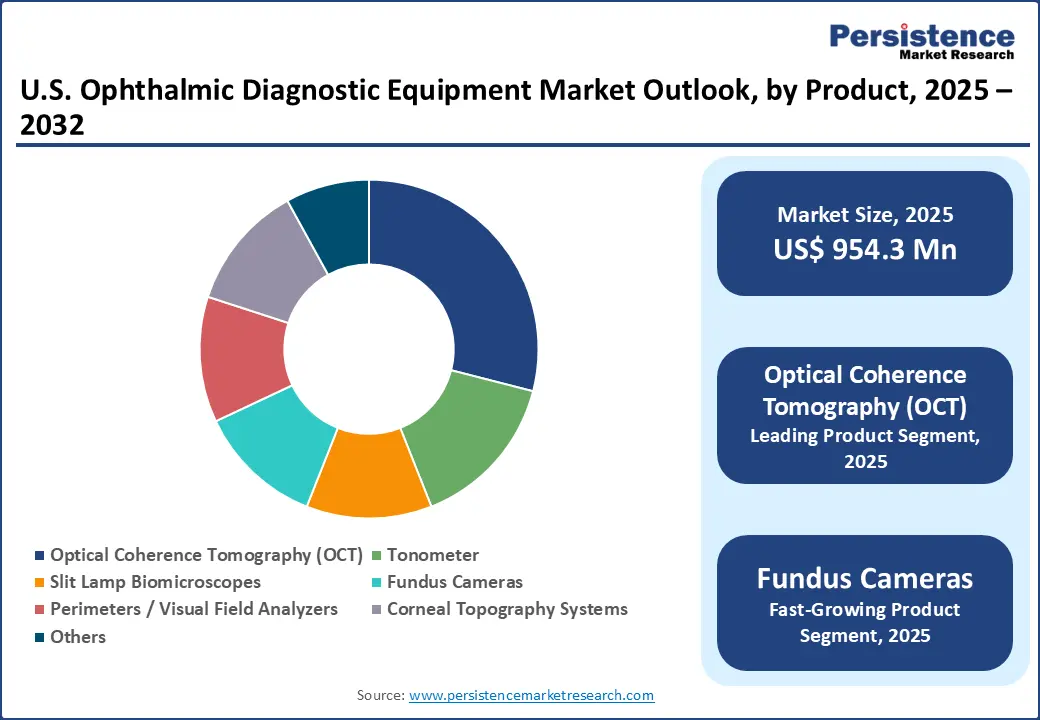

- Fastest-growing Product Segment: Optical Coherence Tomography (OCT) leads the market with over 30% share, driven by its pivotal role in diagnosing retinal and optic nerve diseases, particularly glaucoma and diabetic retinopathy.

- Investment Plans: Companies are increasing investments in research and development to innovate and expand their product portfolios, aiming to meet the evolving needs of the ophthalmic diagnostic market.

- Dominant End-user: Hospitals account for more than 50% of the market share, attributed to their comprehensive diagnostic capabilities and the increasing prevalence of age-related eye conditions.

|

U.S. Market Attribute |

Key Insights |

|

U.S. Ophthalmic Diagnostic Equipment Market Size (2025E) |

US$954.3 Mn |

|

Market Value Forecast (2032F) |

US$ 1,295.7 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Rising Eye Disorder Prevalence Driving Demand for Ophthalmic Diagnostic Equipment

The increasing prevalence of eye disorders in the United States is a significant driver for the ophthalmic diagnostic equipment market. As the population ages, the incidence of conditions such as cataracts, glaucoma, and age-related macular degeneration (AMD) is rising, leading to a higher demand for diagnostic services and equipment. According to the Centers for Disease Control and Prevention (CDC), approximately 20.5 million Americans aged 40 and older have cataracts in one or both eyes, and 6.1 million have undergone cataract surgery in the past five years.

Additionally, about 3 million Americans have glaucoma, with projections indicating this number will increase to 6.3 million by 2050 due to the aging population. Furthermore, an estimated 19.8 million Americans aged 40 and older were living with age-related macular degeneration.

These statistics underscore the growing burden of eye disorders, highlighting the need for advanced diagnostic equipment to manage and treat these conditions effectively. The demand for such equipment is expected to continue rising, presenting significant opportunities for growth in the ophthalmic diagnostic equipment market.

Restraints - High Equipment Costs Limiting Adoption among Smaller Clinics

The substantial cost of ophthalmic diagnostic equipment poses a significant barrier to adoption, particularly for smaller clinics. New diagnostic systems can range from $5,000 to $75,000, depending on their complexity and features. For instance, high-end models with advanced imaging capabilities or specialized functions are typically at the higher end of this price range. Even refurbished equipment, while more affordable, still represents a considerable investment for smaller practices.

This financial challenge is compounded by the limited reimbursement rates from insurance providers for diagnostic procedures, which may not fully offset the initial equipment costs. Consequently, smaller clinics may delay or forgo purchasing advanced diagnostic tools, potentially impacting the quality of care they can provide.

Opportunity - Innovation and Government Support Driving Growth in the U.S. Ophthalmic Diagnostic Equipment Market

The U.S. ophthalmic diagnostic equipment market is experiencing significant growth, driven by advancements in technology and innovation. Government agencies are actively supporting the development of novel ophthalmic devices to enhance diagnostic capabilities and improve patient outcomes.

In February 2024, the Advanced Research Projects Agency for Health (ARPA-H) announced funding for the development of a compact, affordable eye imaging device aimed at improving eye disease diagnostics. This initiative underscores the commitment to making advanced diagnostic tools more accessible and cost-effective. Additionally, the National Institutes of Health (NIH) is leveraging artificial intelligence to enhance existing clinical devices, providing a better understanding of eye health and enabling earlier detection of potential issues.

The FDA's Breakthrough Devices Program further accelerates the development and approval of innovative ophthalmic devices that offer significant advantages over existing alternatives. These concerted efforts by government agencies highlight the emphasis on innovation in the ophthalmic diagnostic equipment market, presenting substantial opportunities for growth and advancement in eye care technologies.

Category-wise Analysis

By Product, Optical Coherence Tomography (OCT) Ophthalmic Diagnostic Equipment is Dominant

In the U.S., the Optical Coherence Tomography (OCT) segment is leading in 2025. Its growth is driven by the increasing number of people affected by eye conditions such as glaucoma, cataracts, and age-related macular degeneration, along with the wider use of digital imaging technologies in eye care. According to the CDC, around 4.2 million Americans have glaucoma, including 1.5 million with vision loss, while 20.5 million people aged 40 and above have cataracts in one or both eyes. About 6.1 million of these individuals have undergone cataract surgery.

New OCT devices, including handheld and portable models, make it easier for doctors to perform eye imaging in hospitals, clinics, and even bedside settings, improving access and convenience. For example, in May 2024, the FDA granted de novo authorization for Notal Vision’s Scanly Home OCT, a patient-operated device. It works with the company’s AI-powered Notal OCT Analyzer (NOA) to automatically assess self-captured images. This clearance represents the first FDA approval of an AI algorithm specifically for OCT imaging. The fundus camera segment is also growing, supported by higher healthcare spending, favorable insurance coverage, and programs encouraging regular eye check-ups.

By End-user, Hospitals Lead While Ambulatory Surgical Centres and Clinics are Likely to Grow Fast

End-users segment the U.S. ophthalmic diagnostic equipment market into hospitals, ophthalmic clinics, and ambulatory surgical centres. Among these, hospitals account for the largest share of the U.S. market. This is due to the higher volume of diagnostic procedures conducted in hospitals, the widespread availability of advanced instruments, and the growing adoption of state-of-the-art diagnostic technologies within hospital settings.

Ambulatory surgical centers (ASCs) are expected to register the fastest growth, driven by a shift toward same-day procedures and outpatient eye care. ASCs play a key role in cataract surgeries, glaucoma laser treatments, and minor retinal procedures, offering faster recovery times and reducing hospital congestion. The affordability, convenience, and efficient use of resources at ASCs are encouraging the installation of diagnostic equipment, including compact and automated devices such as portable OCT systems and slit lamps, which support high patient volumes.

Ophthalmic clinics are also contributing to market growth, particularly in urban and semi-urban areas. Clinics are focusing on early detection and preventive eye care, increasingly investing in mid-range imaging tools and tonometers to enhance service quality and patient outcomes.

Competitive Landscape

The U.S. ophthalmic diagnostic equipment market is growing as companies bring in new technologies, add more product options, and expand through partnerships and regional reach. Established players are focusing on advanced digital solutions to improve accuracy and efficiency in eye care, while newer companies are adding supportive tools and accessories to their product range. This approach helps manufacturers meet the changing needs of doctors and patients, attract more customers, and remain competitive in the fast-developing eye care market.

Key Industry Developments:

- In March 2024, Visionix USA appointed Insight Medical Technologies as its exclusive sales and service partner in Canada for Visionix refraction and screening platforms, Optovue OCT and OCT-A systems, and Briot and Weco finishing equipment. This improved the company’s position in North America.

- In June 2024, NIDEK CO., LTD., a global leader in ophthalmic, optometric, and lens edging equipment, launched the RS-1 Glauvas Optical Coherence Tomography system.

- In October 2023, Bausch + Lomb Corporation, a leading global eye Health Company committed to improving vision and quality of life, unveiled the U.S. launch of SeeNa. This ophthalmic diagnostic system is designed for refractive cataract patients and is fully integrated with Bausch + Lomb’s Eyetelligence™ surgical planning software, helping to streamline surgical planning and enhance information flow.

Companies Covered in U.S. Ophthalmic Diagnostic Equipment Market

- Topcon Corporation

- Haag-Streit

- iCare

- Optos

- Carl Zeiss Meditec AG

- Oculus Optikgeräte GmbH

- Sonomed Escalon

- Nidek

- Essilor

- Optovue

- Ellex

- Coburn Technologies Inc.

- Quantel Medical

- Others

Frequently Asked Questions

The U.S. Ophthalmic Diagnostic Equipment Market is projected to be valued at US$ 954.3 Mn in 2025.

High prevalence of eye disorders, technological advancements in OCT and AI-enabled devices, increasing outpatient procedures, and well-established healthcare infrastructure drive market growth.

The U.S. ophthalmic diagnostic equipment market is poised to witness a CAGR of 5.2% between 2025 and 2032.

Rising demand for early disease detection, expansion of ambulatory surgical centers, AI integration, personalized vision care, and strategic partnerships offer significant growth opportunities in the U.S. market.

Major players in the U.S. Topcon Corporation, Haag-Streit, iCare, Optos, Carl Zeiss Meditec AG, Oculus Optikgeräte GmbH., and others.