- Industrial Goods & Service

- U.S. Mining Hoses Market

U.S. Mining Hoses Market Size, Share, and Growth Forecast for 2025 - 2032

U.S. Mining Hoses Market by Transporting Media (Slurry, Industrial Water & Alkali, Bulk Powder), Material Composition (Natural Rubber, Synthetic Rubber, PU & Other Polymers), End-Use (Coal Mining, Metal Mining, Other Mining), and Regional Analysis (Northeast, Midwest, South, West) for 2025 - 2032

U.S. Mining Hoses Market Size and Trends

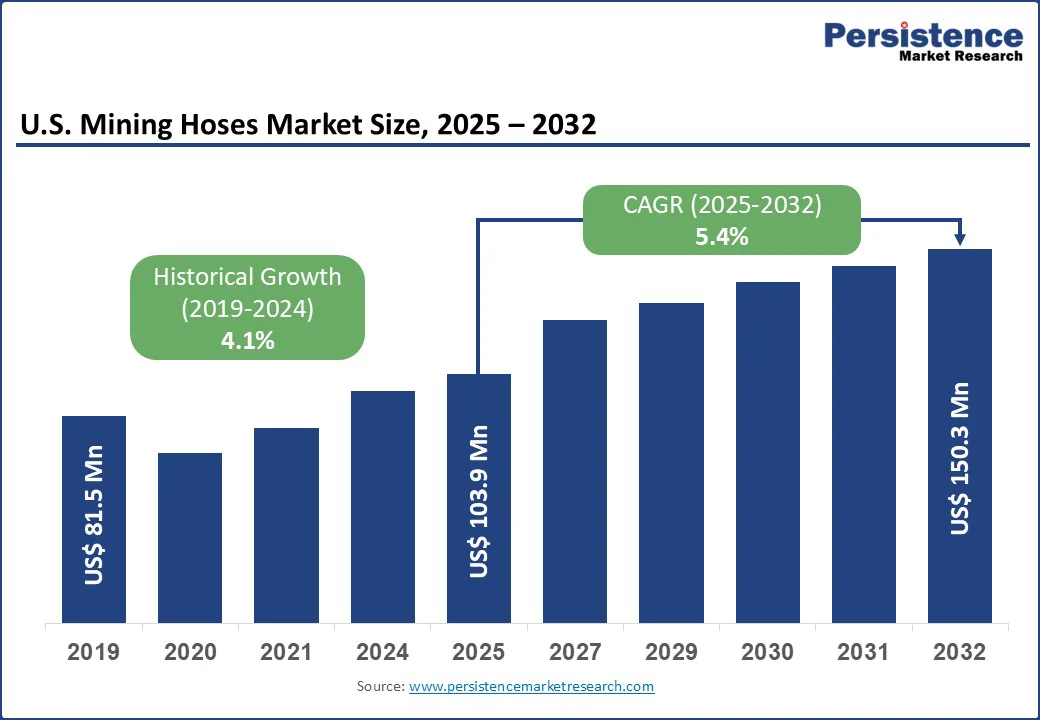

The U.S. mining hoses market size is likely to be valued at USD 103.9 Mn in 2025 and is expected to reach around USD 150.3 Mn by 2032, expanding at a CAGR of 5.4% during the forecast period 2025 - 2032, owing to increased mining investments, stricter safety and environmental regulations, and demand highly durable hoses.

Key Industry Highlights:

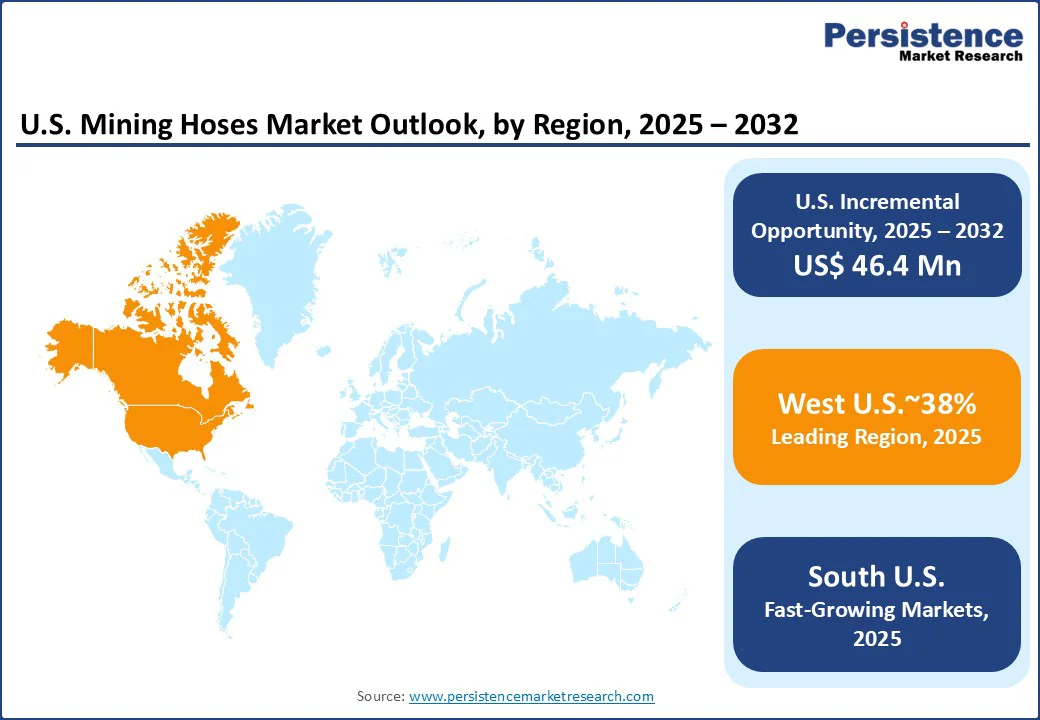

- Demand Trend: Holding the largest market share at 38% in 2025, the Western U.S. leads due to extensive mining operations and abundant resource availability. The South captures 31% of the market with a projected CAGR of 5.3% by 2032. It is driven by coal mining growth and regulatory compliance that supports the adoption of durable, high-performance hoses.

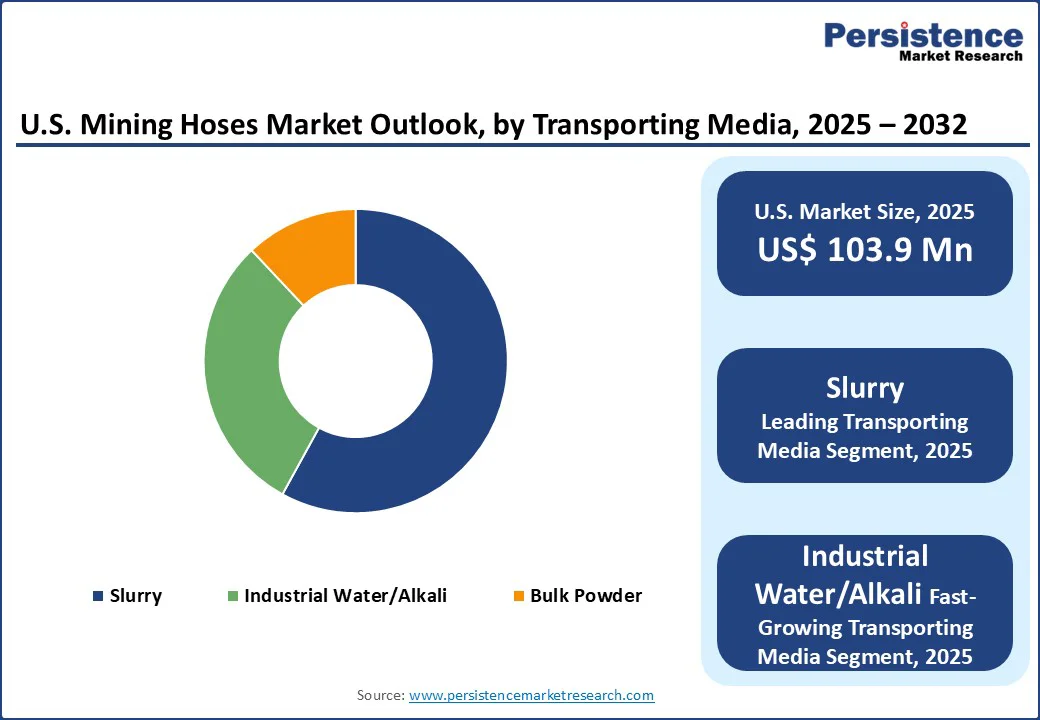

- Leading Transportation Media: Slurry remains the dominant transporting media segment, representing 58% of the market, fueled by the need for efficiency in coal and metal mining operations where abrasion resistance and reliability are critical.

- Prominent Material Composition: Synthetic rubber holds a 40% share and leads the material composition segment. Subtypes such as NBR and SBR are gaining traction due to superior resistance to chemicals, pressure, and abrasion in demanding mining environments.

- Leading End-use: Coal mining continues as the leading end-use segment, accounting for 55% demand. Federal safety regulations and efficiency-focused operations remain key drivers sustaining hose consumption in this sector.

| U.S. Market Attribute | Key Insights |

|---|---|

| U.S. Mining Hoses Market Size (2025E) | US$ 103.9 Mn |

| Market Value Forecast (2032F) | US$ 150.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Dynamics

Growth Driver - Strategic Policy Shifts and Infrastructure Investments Boost U.S. Mining Hoses Market

The U.S. mining hoses market is growing as strategic policy changes and infrastructure investments strengthen domestic mineral production. In response to rising global demand for critical minerals, the government has reallocated funds from the CHIPS Act to support domestic mining projects, reducing reliance on foreign sources. The Department of Energy has also committed nearly $1 billion to advance mining, processing, and manufacturing technologies, enhancing capabilities across critical mineral supply chains.

According to the U.S. Geological Survey 2024 report, total mineral production exceeded $105 billion in 2023, reflecting a surge in mining activities requiring advanced equipment such as mining hoses. The Department of the Interior’s initiatives to recover critical minerals from mine waste further support infrastructure development, sustaining demand for specialized mining hoses and modernized transport systems.

Restraint - Environmental Regulations and Operational Challenges Influence U.S. Mining Hoses Market

The U.S. mining hoses market is experiencing strong demand; however, it faces constraints from strict environmental regulations and operational challenges. Mining activities require federal and state-level permits under laws such as the Clean Water Act of 1972 and the National Environmental Policy Act of 1970, which can lead to delays in project timelines and increased compliance costs. Moreover, fluctuating raw material prices, especially for rubber and synthetic polymers, affect manufacturing costs and can limit profitability for hose producers.

Operational complexities in mining sites, including abrasive material handling and extreme weather conditions, also pose challenges for equipment durability and maintenance. The U.S. Bureau of Labor Statistics reports that mining and extraction sectors face higher-than-average workplace incident rates, necessitating frequent replacement and specialized maintenance of hoses. These regulatory and operational pressures require manufacturers and operators to adopt robust planning and advanced materials, influencing procurement decisions and potentially slowing market expansion in the short term.

Opportunity - Technological Advancements and Infrastructure Modernization Open New Paths in the U.S. Mining Hose Market

The U.S. mining hoses market is poised for expansion as advancements in materials and design improve efficiency and durability. Innovative hose constructions using abrasion-resistant polymers and enhanced reinforcement technologies allow longer operational life and safer material transport in challenging mining environments. Modernization of mining infrastructure, including automated slurry handling and water management systems, further drives the need for specialized hoses capable of handling higher pressures and diverse media.

Government initiatives promoting domestic mineral production also create new opportunities. For instance, the Department of Energy’s funding for critical mineral processing projects and the Department of the Interior’s programs to recover resources from abandoned mines support the adoption of advanced mining equipment. These factors encourage investment in modern hose technologies, enabling manufacturers to offer solutions tailored to evolving operational and environmental demands, expanding their market reach and adoption across mining sectors.

U.S. Mining Hoses Market Insights

Transporting Media Insights - Slurry Transport Dominates the U.S. Mining Hoses Market Amid Expanding Mining Operations

Slurry transport leads the U.S. mining hoses market with an estimated 44% revenue share, reflecting consistent demand from mining operators handling abrasive ores and tailings in large-scale operations.

The segment’s growth is supported by the adoption of wear-resistant hoses capable of withstanding high pressures and continuous material flow, alongside regulatory encouragement for domestic mineral production and infrastructure modernization. Industrial water and alkali transport is the fastest-growing segment at a 6.3% CAGR, driven by government-led water management programs and initiatives promoting sustainable mining practices.

Bulk powder transport also plays a key role, particularly in operations requiring efficient handling of fine materials, where technological improvements enhance throughput and reduce spillage. These segments collectively benefit from ongoing investments in mining infrastructure, automation, and material handling efficiency, enabling the market to meet evolving operational, environmental, and regulatory demands across diverse mining applications.

End-use Insights - Coal Mining Remains the Leading End-Use Segment in the U.S. Mining Hoses Market

Coal mining dominates the U.S. mining hoses market with an estimated 52% revenue share, driven by the ongoing need for reliable slurry and water transport systems in both surface and underground operations. The segment’s sustained demand is reinforced by regulatory requirements for safe material handling and adherence to Mine Safety and Health Administration (MSHA) standards (1977), ensuring operational efficiency and worker safety.

Metal mining represents the fastest-growing end-use segment at a 5.8% CAGR, supported by increased exploration of critical minerals and government initiatives to bolster domestic production of rare-earth and strategic metals.

Other mining activities, including industrial mineral extraction, also contribute to market growth, relying on advanced hose solutions for bulk material handling and process water transport. Across these segments, the combined effect of technological enhancements, infrastructure investments, and regulatory compliance continues to shape adoption patterns and operational strategies.

Zone Insights

West U.S. Mining Hoses Market Trends - Western U.S. Leads Mining Hoses Market Driven by Major Mining Hubs and Infrastructure

The Western U.S., holding a significant market share of around 38% in 2025, remains the dominant region for mining hoses, anchored by major mining operations and industrial clusters in Nevada, Arizona, and California, where both surface and underground mineral extraction are concentrated. Expansions of critical mineral mines and investments in processing facilities have driven strong demand for durable, high-performance hoses capable of transporting slurry, water, and bulk materials efficiently.

Proximity to key mineral reserves and well-developed logistics networks ensures reliable operations and timely material handling. Growing adoption of hoses designed for chemical and water transport reflects increasing focus on sustainable water management and adherence to strict environmental standards. These factors position the Western U.S. as a core hub for high-performance mining hoses, supporting the region’s continued leadership in the U.S. market.

South U.S. Mining Hoses Market Trends- Southern U.S. Emerges as a Growth Hub for Mining Hoses Through Surface Mining and Industrial Expansion

The Southern U.S., growing at a CAGR of around 4.8% is becoming a key region for mining hoses, anchored by expanding surface mining operations and industrial hubs in Texas, Louisiana, and Alabama. Investments in processing facilities and material handling infrastructure have driven demand for hoses capable of transporting slurry, water, and bulk powders under challenging operational conditions.

A well-connected logistics network and proximity to major ports enable efficient supply chain management for mining outputs. Expanding mining projects, infrastructure modernization, and adoption of advanced hose technologies continue to strengthen operational efficiency while ensuring compliance with evolving environmental and regulatory standards. These factors position the Southern U.S. as a fast-growing market for durable, high-performance mining hoses.

North U.S. Mining Hoses Market - Northeast U.S. Maintains Steady Demand in Mining Hoses Through Legacy Operations and Industrial Hubs

The Northeastern U.S., holding around 14% of the mining hoses market, plays a strategic role anchored by established mining operations and industrial mineral centers in Pennsylvania, New York, and West Virginia. Facilities handling coal, limestone, and other industrial minerals depend on durable hoses for slurry, water, and bulk material transport, ensuring uninterrupted operations.

Federal standards such as the Clean Water Act, combined with state-level environmental compliance, have accelerated the adoption of hoses designed for chemical and water handling. Modernization efforts and infrastructure upgrades across regional mines support steady growth, enabling operators to maintain productivity while meeting evolving regulatory and environmental requirements. These factors sustain demand for high-performance mining hoses across diverse applications in the Northeast.

Competitive Landscape

Leading U.S. mining hose manufacturers focus on abrasion-resistant materials, reinforced designs, and high-pressure capabilities while complying with MSHA and environmental regulations. Innovation and process optimization enhance supplier networks and operational efficiency, ensuring reliable material transport across surface, underground, and industrial mining operations. Investments in research and development introduce advanced hoses that meet evolving extraction needs, strengthening competitiveness, expanding capacity, and supporting long-term market growth.

Key Industry Developments:

- In December 2024, Continental AG launched the X-Life™ XCP5 hose, a flexible braided hose designed for high-pressure hydraulic applications requiring extra abrasion resistance. This product enhances their premium braided hose portfolio and is ISO 18752 compliant.

- In August 2024, Metso Corporation acquired Jindex Pty Ltd, an Australian OEM specializing in slurry handling equipment, including hoses, pumps, and valves. This acquisition strengthens Metso's slurry handling offerings and expands its presence in the Asia Pacific region.

- In March 2025, Eaton Corporation expanded its hydraulic filtration portfolio with the launch of three high-performance filter series: DUA, LWF, and DNR. These filters are engineered for demanding applications, enhancing Eaton's product offerings in hydraulic systems.

Companies Covered in U.S. Mining Hoses Market

- Trelleborg Group

- Metso Corporation

- Continental AG

- Weir Group PLC

- Eaton Corporation plc

- Gates Industrial Corporation plc

- Parker Hannifin Corporation

- ALFAGOMMA Group

- Novaflex Group

- Goodall Hoses

- Kanaflex Corporation Co., Ltd.

- Abdex Hose & Couplings Pty Ltd

- NORRES Schlauchtechnik GmbH

- Pacific Hoseflex Pty Ltd

- Salem-Republic Rubber Company

Frequently Asked Questions

The U.S. Mining Hoses market is set to reach US$ 103.9 Mn in 2025.

Significant investments in mining infrastructure, coupled with evolving federal and state regulations, are driving demand for durable, high-performance hoses across the U.S.

The U.S. mining hoses industry is estimated to rise at a CAGR of 5.4% from 2025 to 2032.

Advances in hose technology, combined with the modernization of mining and processing facilities, are creating new opportunities across the U.S., enhancing efficiency, durability, and safety in material handling operations while supporting industry growth.

The major players dominating the U.S. Mining Hoses Market are Trelleborg Group, Metso Corporation, Continental AG, Weir Group PLC, Eaton Corporation plc.