- Technology

- U.S. LegalTech Market

U.S. LegalTech Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

U.S. LegalTech Market By Solution (Software & Services), Application (E-discovery, Practice Management, Document Management, Legal Research, Contract Lifecycle Management, Time-Tracking & Billing, Compliance & Risk Management, Legal Analytics & Knowledge Management, and Others), and End-user Analysis for 2025 - 2032

U.S. LegalTech Market Size and Trends

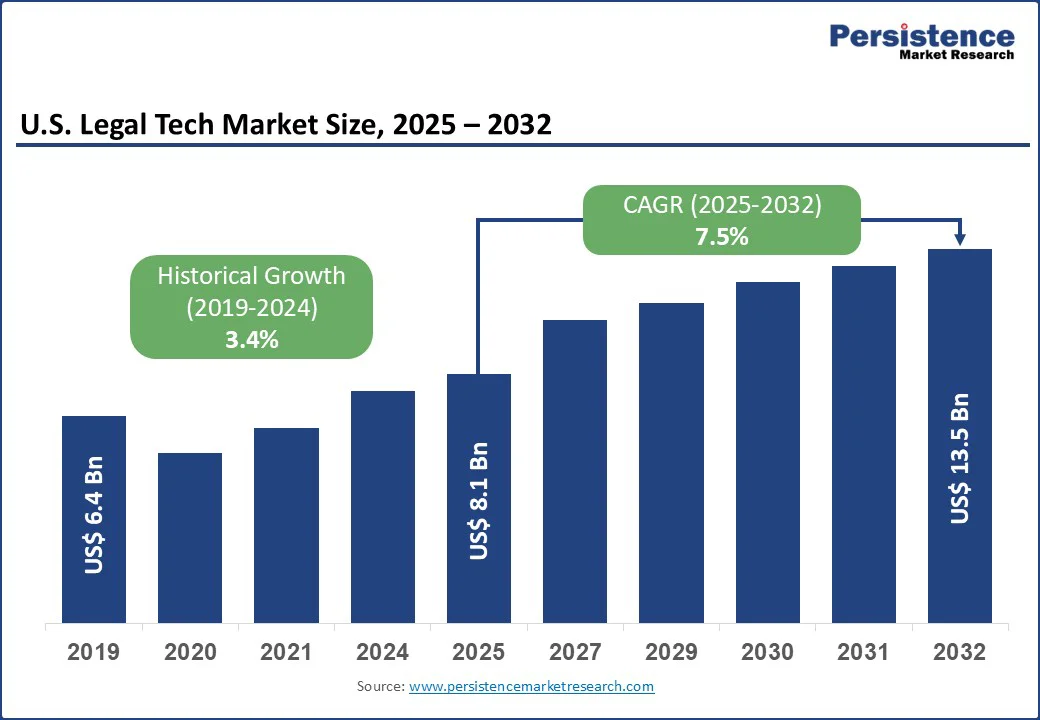

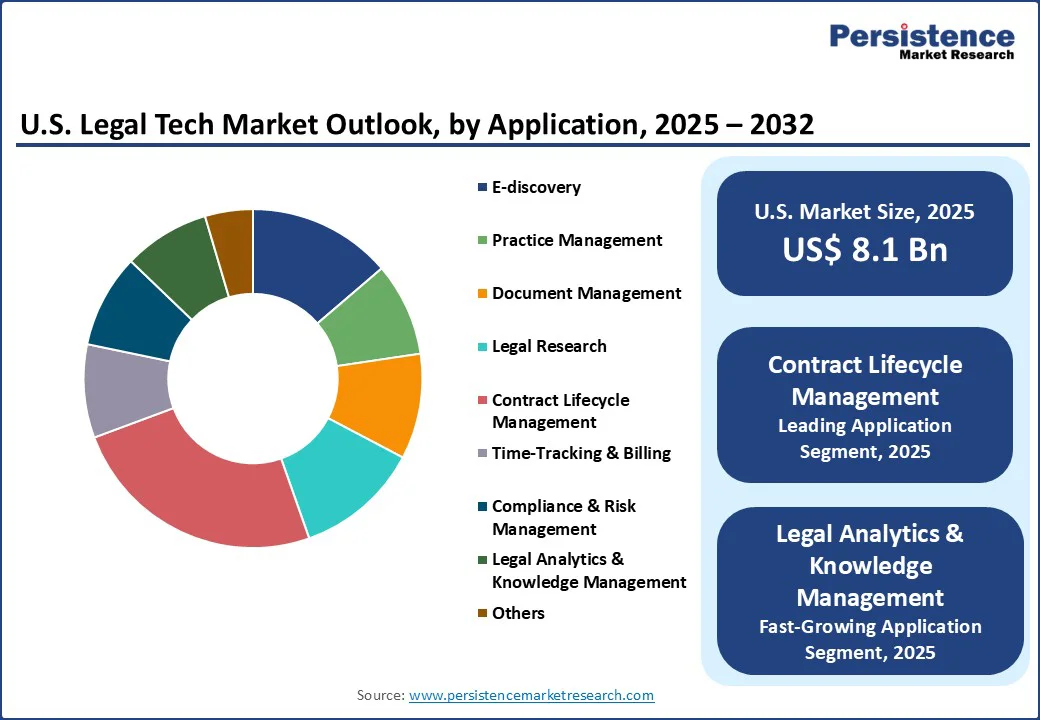

The U.S. LegalTech Market size is likely to value at US$8.1 Bn in 2025 and is expected to reach US$13.5 Bn by 2032 growing at a CAGR of 7.5% during the forecast period from 2025 to 2032.

The rise in volumes of legal data, complex regulatory requirements, and the demand for faster decision-making are fueling the adoption of digital solutions. The pressure to deliver more client-centric, transparent, and affordable services is pushing legal organizations to embrace innovative technologies. There is a growing need for greater efficiency, cost reduction, and improved access to legal services. Firms are rapidly adopting digital tools to streamline workflows, enhance compliance, and reduce reliance on manual processes.

Key Industry Highlights:

- Dominant Solution: Software, with over 71% share, driven by the growing need for efficient legal operations, automation of repetitive tasks, and faster case management, which enables reduced costs, improved accuracy, and more client-centric services.

- Leading Application: Contract lifecycle management software, holding more than 27% market share in 2025, driven by the need for organizations to streamline contract creation, review, and approval processes, reduce errors, ensure compliance, and accelerate contract execution while improving visibility across the contract portfolio.

- Dominant End-user: Law firms, over 48% share, driven by the need to manage increasing volumes of legal data efficiently. They are adopting advanced technologies such as AI, document automation, and legal analytics to streamline workflows, ensure compliance, and deliver faster, cost-effective services.

- Investment Plans: Matey raised $7.5M in seed funding led by Timespan Ventures, with participation from Neo and Streamlined Ventures. Its CrimD platform is being used by public defenders, law firms, and government agencies to streamline discovery, analyze digital evidence, and support trial preparation.

|

Market Attribute |

Key Insights |

|

U.S. LegalTech Market Size (2025E) |

US$8.1 Bn |

|

Market Value Forecast (2032F) |

US$13.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.4% |

Market Dynamics

Driver - Rising Legal Complexity & Case Volume

Modern products face increasingly intricate supply chains, sophisticated IP management, and stricter contractual obligations, especially in pharmaceuticals, technology, and consumer electronics. Compliance with regulations such as the Food, Drug, and Cosmetic Act, Sarbanes-Oxley Act, and state-level consumer protection laws has become critical, as non-compliance can result in hefty fines, litigation, and reputational loss.

Rising volumes of disclosures, patent filings, and internal controls are fueling demand for workflow-centric LegalTech tools like matter management, e-discovery, contract automation, claims handling, and IP operations. The U.S. is experiencing an increase in RegTech solutions as financial and legal sectors adapt to complex regulatory environments.

Growing regulatory oversight further reinforces this shift, as the USPTO’s 2025 Patents Dashboard reports sustained high application inventories and double-digit-month pendency, signaling the scale of legal work that must be digitally tracked and docketed. OSHA conducted 34,625 inspections (programmed + unprogrammed) in FY2024, underscoring the intensity of enforcement that often generates documentation demands, corrective-action plans, and litigation risks. These pressures are accelerating LegalTech adoption for incident tracking, evidence collection, and faster compliance responses, reducing manual errors while ensuring efficiency and accuracy.

Restraint - Resource Gaps, Cost Pressures, and Training Limitations

LegalTech encompasses diverse applications, but firms often struggle to consolidate specialized tools into a cohesive workflow. The rapid evolution of AI-driven contract analysis and document automation has outpaced the development of structured training programs, leaving many professionals without the technical expertise required to leverage these tools. This results in resistance to adoption, stemming from concerns over reliability, accuracy, and fear of obsolescence.

Disparities in access to advanced tools further constrain adoption, particularly among smaller firms. The American Bar Association’s 2025 survey reveals that only 35% of solo practitioners engage in e-discovery cases compared to 66% of large firms, while predictive coding and AI-assisted search remain largely underutilized among solos (11% and 29%, respectively) and small firms (7%). Cost barriers amplify this gap, with 74% solos spending under US$3,000 annually on legal software and 61% under $2,999 on hardware, whereas large firms routinely invest over US$20,000. Platform preferences also highlight fragmentation, with Fastcase leading among solos, government sites among small firms, and Lexis/Lexis+ versus Westlaw/Westlaw Precision dominating, underscoring uneven adoption and reinforcing market restraints.

Opportunity - Generative AI, Risk Management, and Data Integration

AI-driven legal research and drafting are creating major opportunities for law firms, corporate legal departments, and federal agencies to improve efficiency, reduce costs, and enhance service delivery. A July 2025 GAO (Government Accountability Office) report showed that federal AI use cases nearly doubled from 2023 to 2024, underlining the pace of adoption. At the same time, the New York State Unified Court System highlighted that 92% of civil legal needs of low-income Americans went unmet in 2021, positioning AI-powered legal tools as scalable solutions to expand access to justice.

Growing reliance on data analytics further unlocks market potential by supporting predictive case outcomes, proactive risk management, and improved compliance. The U.S. Courts’ Long Range Plan for IT and the 2024 Legal Aid Interagency Roundtable advocate for people-centered, data-driven approaches in judicial services. Platforms like DISCO, a cloud-native AI-powered legal solution, showcase how integration with enterprise systems streamlines workflows, reduces manual intervention, and accelerates legal processes, driving innovation, investment, and large-scale adoption across the U.S. market.

LegalTech Market Key Trend

Market Expansion through M&A and Client-Centric LegalTech

Firms in the U.S. are increasingly pursuing mergers and consolidations to create holistic, end-to-end platforms that address a wide array of legal processes. Such strategies enable companies to expand product offerings, strengthen management teams, achieve economies of scale, and integrate emerging technologies. For instance, the merger of Onit and Legal Files reflects this shift, combining workflow automation with case management to deliver comprehensive services. Legal process outsourcing (LPO) providers further amplify this by operating across time zones, relying on advanced tools such as AI-powered e-discovery, NLP for legal research, and blockchain for secure records, while ensuring compliance with U.S. laws and regulations.

The rise of remote and hybrid working models has boosted reliance on secure cloud-based platforms that enable real-time collaboration between in-house legal teams, law firms, and LPO partners. Client-facing LegalTech platforms with mobile-friendly interfaces, digital consultation scheduling, and real-time case tracking are aligning with the broader digital transformation in the U.S. legal sector.

Affordable subscription models, pay-per-use pricing, and automated workflows are democratizing access to legal services for small businesses and individuals, lowering the costs of tasks such as NDAs, lease reviews, and incorporations. This feature helps expand the client base and enables sustainable growth.

Category-wise Analysis

By Solution, Software Enables Scalable, Secure, and Efficient Legal Operations

Based on the solution, the market is divided into software and services. Software is expected to account for more than 71% share in 2025, as law firms and corporate legal departments face increasing pressure to manage large volumes of documents, contracts, and case data efficiently. The growing need for automation, accuracy, and compliance drives adoption, helping reduce manual workload, minimize errors, and accelerate decision-making. This addresses the demand for faster and more cost-effective legal services. Firms prefer cloud-based solutions for their ability to provide scalable operations, secure handling of sensitive legal data, and seamless access for remote teams.

Services are expected to grow at a significant rate due to the increasing complexity of legal operations and the lack of in-house expertise to implement and manage advanced technologies. The adoption of AI, analytics, and automation in legal processes requires continuous technical guidance, seamless system integration, and ongoing maintenance. As businesses prioritize efficiency, accuracy, and cost-effectiveness, reliance on external service providers becomes critical, making LegalTech services essential enablers of digital transformation.

By Application, Contract Lifecycle Management Boosts Accuracy, Visibility, and Legal Risk Mitigation

By application, the segmentation comprises e-discovery, practice management, document management, legal research, contract lifecycle management, time-tracking & billing, compliance & risk management, legal analytics & knowledge management, and others. Out of these, contract lifecycle management (CLM) is expected to account for more than 27% share in 2025 due to companies facing increasing pressure to ensure compliance, reduce risks, and streamline contract approvals and renewals.

Manual contract management is time-consuming and error-prone, making automation critical for efficiency and accuracy. CLM enables organizations to track obligations, deadlines, and approvals, reducing the likelihood of costly legal disputes, while centralized repositories and improved cross-departmental visibility further drive its adoption.

Legal analytics & knowledge management is expected to grow at the highest rate due to the increasing need for data-driven decision-making. As legal cases become increasingly complex, organizations rely on advanced analytics to predict outcomes, assess risks, and optimize strategies. Knowledge management solutions centralize legal documents, precedents, and best practices, improving efficiency and reducing research time. AI-powered automation further enhances accuracy and speed, making these tools crucial for modern legal teams.

By End-user, Law Firms Are Leading Due to the Need for Better Efficiency and Compliance

Based on the end user, the segmentation comprises law firms, corporate legal departments, and others. Law firms are expected to account for more than 48% share in 2025, as they face increasing pressure to deliver faster, more cost-effective, and client-centric services while managing rising volumes of legal data. To remain competitive, firms are adopting advanced technologies such as AI, document automation, and legal analytics to streamline workflows and enhance compliance. The need to improve efficiency, reduce manual processes, and increase accuracy in case management drives a heavy reliance on digital solutions.

Corporate legal departments are expected to grow at the highest rate due to mounting pressure to manage increasing legal complexity, regulatory compliance, and rising litigation risks while keeping costs under control. They face strict budget constraints and are shifting towards technology-driven solutions to reduce outside counsel spending and enhance in-house efficiency. Digital tools enable corporate legal teams to streamline workflows, improve transparency, and strengthen collaboration with other business units. As enterprises expand, demand for scalable, secure, and integrated legal-tech solutions will continue to surge.

Competitive Landscape

The U.S. LegalTech market is fragmented, with numerous specialized software and service providers catering to different legal functions. Companies compete through innovation in AI-driven solutions, automation, and analytics, aiming to enhance efficiency and compliance. They are also focusing on strategic partnerships and acquisitions to expand their product portfolios and market reach, while emphasizing cloud-based, scalable platforms and customer-centric pricing to attract diverse legal organizations.

Industry Developments:

- In August 2025, SurePoint Technologies launched SurePoint Legal Suite, unifying its legal software solutions into a single ecosystem. The move marks a shift from traditional practice management to firm performance solutions, helping mid-sized law firms drive efficiency, align departments, and leverage data-driven insights amid rising client and resource pressures.

- In August 2025, Everlaw launched the open beta of EverlawAI Deep Dive (formerly Project Query), a GenAI-powered tool that lets legal teams search terabytes of eDiscovery data in seconds using conversational queries. Already adopted in large-scale matters exceeding 10 million documents, it delivers instant, fact-supported insights tied to specific issues, parties, or events.

- In August 2025, Francisco Partners announced its acquisition of Elite, a provider of mission-critical software and integrated payment solutions for the legal industry, from TPG Capital and Thomson Reuters. The deal brings Elite a new financial partner to support its growth, innovation, and market momentum.

- In July 2025, ChronoTracer launched the first litigation and investigation software that automates case chronologies, consolidating communications and time-based records from diverse digital evidence into a single, time-ordered view. Designed for litigators and investigative teams, it streamlines evidence reviews from days to seconds, enabling faster and more accurate fact analysis.

Companies Covered in U.S. LegalTech Market

- DocuSign, Inc.

- Thomson Reuters

- LexisNexis

- Mitratech

- Onit, Inc.

- Themis Solutions Inc.

- Ironclad, Inc.

- Litera

- NetDocuments Software, Inc.

- Consilio

- Epiq

- Exterro

- Others

Frequently Asked Questions

The U.S. LegalTech market is projected to be valued at US$8.1 Bn in 2025.

Rising volumes of legal data, the need to ensure compliance with complex regulations, and the demand to deliver faster, cost-effective services are the key drivers of the LegalTech market.

The U.S. LegalTech market is poised to witness a CAGR of 7.5% from 2025 to 2032.

Rising adoption of AI, automation, and cloud-based solutions to improve efficiency, compliance, and client-centric service delivery is creating strong growth opportunities.

DocuSign, Inc., Thomson Reuters, LexisNexis, Mitratech, Onit, Inc., Themis Solutions Inc. are among the leading key players.