- Pharmaceuticals

- U.S. Intrathecal Drugs Market

U.S. Intrathecal Drugs Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

U.S. Intrathecal Drugs Market by Drug (Morphine, Baclofen, Ziconotide, Bupivacaine, Hydromorphone, Clonidine), by Application (Pain Management, Spasticity), by Distribution Channel (Hospital Pharmacies, Online Pharmacies), and Analysis for 2025 - 2032

U.S. Intrathecal Drugs Market Size and Trends

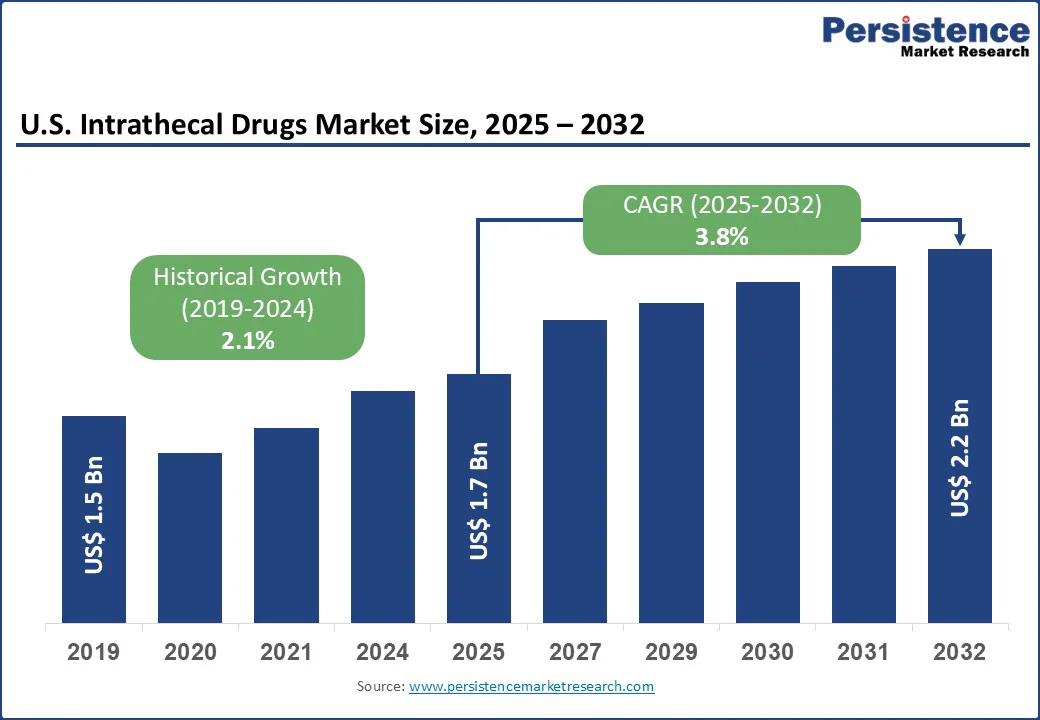

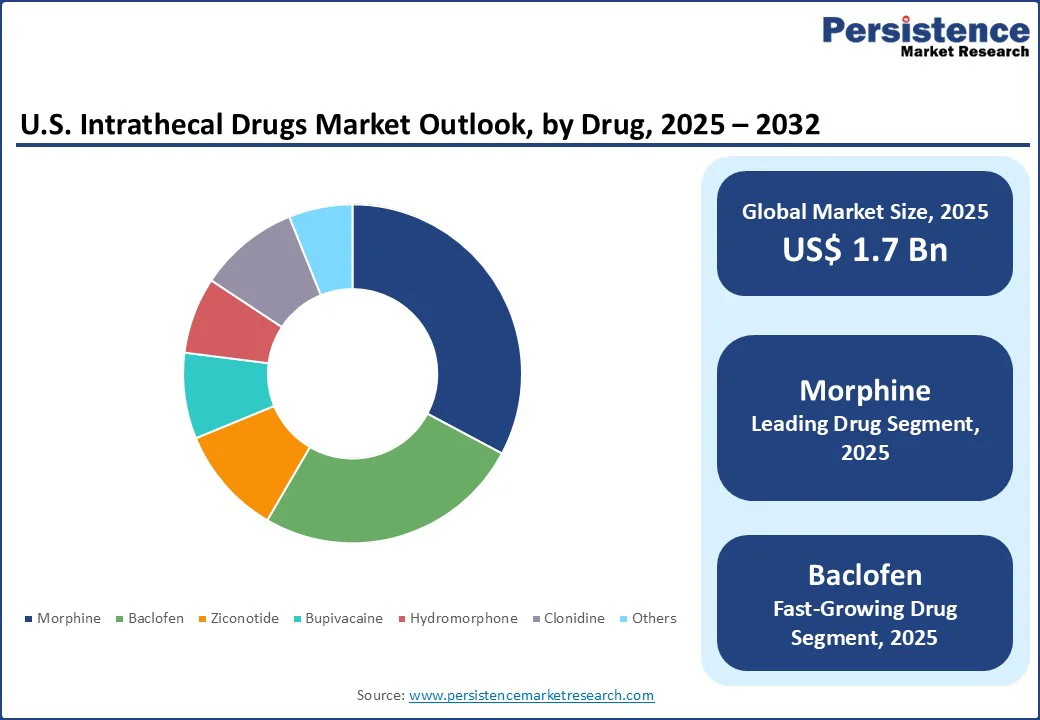

The U.S. intrathecal drugs market size is likely to be valued at US$1.7 Bn in 2025. It is estimated to reach US$2.2 Bn in 2032, growing at a CAGR of 3.8% during the forecast period 2025-2032, driven by increasing prevalence of chronic pain conditions and spasticity as well as rising demand for effective and targeted pain management solutions. Recent studies have emphasized the importance of refining dosing strategies, refining catheter designs, and optimizing patient selection protocols to improve both efficacy and safety.

Key Industry Highlights:

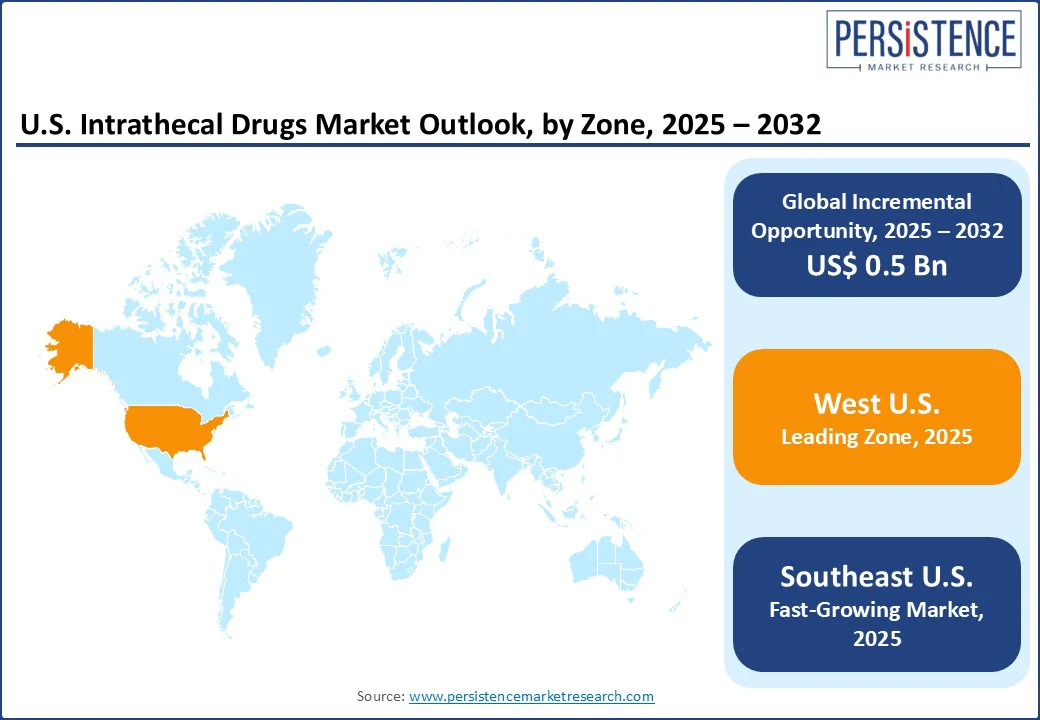

- Leading Zone: West U.S., backed by a high prevalence of chronic pain conditions, increased access to specialized healthcare facilities, and adoption of new pain management technologies.

- Fastest-growing Zone: Southeast U.S., owing to an increasing incidence of conditions requiring surgical interventions, including hip and knee replacements.

- Dominant Drug: Morphine holds approximately 32.8% share in 2025, as it is the gold standard for intrathecal drug delivery due to its potent analgesic effects and well-established clinical efficacy.

- Leading Application: Pain management, with a nearly 60.5% share in 2025, due to the direct and targeted delivery to the spinal cord, which improves the efficacy of analgesics while minimizing side effects.

- Emerging Modality: A 2025 study published in Anesthesia & Analgesia discussed the use of high cervical intrathecal drug delivery for managing intractable craniofacial cancer pain. The study reported pain relief in patients, with over 50% pain reduction achieved in 93% of cases within one week.

| Key Insights | Details |

|---|---|

|

U.S. Intrathecal Drugs Market Size (2025E) |

US$1.7 Bn |

|

Market Value Forecast (2032F) |

US$2.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.1% |

Market Dynamics

Driver - Developments in Surgical Techniques and Recovery Protocols Boost Growth

The increasing prevalence of complex surgical procedures in the U.S. has influenced demand for Intrathecal drug delivery systems (IDDS). It is evident in managing postoperative pain and spasticity. Surgeries such as hip and knee arthroplasties, Coronary Artery Bypass Grafting (CABG), Transurethral Resection of the Prostate (TURP), and organ transplants often result in persistent pain and muscle spasticity. These conditions are challenging to control with oral or intravenous medications alone. IDDS provides a targeted approach, delivering analgesics directly to the spinal cord, thereby improving efficacy and reducing systemic side effects.

Developments in surgical techniques and postoperative care protocols support the adoption of IDDS. As surgical procedures become complex and recovery times lengthen, there is an increasing emphasis on effective pain management strategies. IDDS has emerged as an ideal option. It helps by providing sustained analgesia with lower doses of medication, further minimizing the risk of side effects and refining patient outcomes.

Restraint - CSF Leaks and Hematomas Lead to Withdrawal Syndromes

The adoption of intrathecal drugs in the U.S. faces challenges due to complications, including Cerebrospinal Fluid (CSF) leaks and hematomas. These issues result in clinical concerns such as withdrawal syndromes, neurological deficits, and the requirement for additional surgical interventions. Additionally, complications such as epidural hematomas have been reported, sometimes resulting in severe outcomes, including death or residual neurological deficits.

Such adverse events highlight the importance of meticulous surgical techniques and post-operative monitoring to mitigate risks associated with IDDS implantation and maintenance. Preventive measures and treatment strategies are hence being explored. The application of fibrin glue during IDDS implantation, for example, has been shown to reduce the incidence of post-dural puncture headaches drastically.

Opportunity - Intrathecal MSC Delivery Shows Promise in Treating Progressive Multiple Sclerosis

Researchers are currently exploring intrathecal delivery of Mesenchymal Stem Cells (MSCs) to influence neurological conditions via cerebrospinal fluid delivery directly. In a Phase II randomized, placebo-controlled trial published in mid-2024, patients with progressive multiple sclerosis received intrathecal MSC-neural progenitor (MSC-NP) therapy. Results demonstrated not just safety, but notable efficacy in slowing disease progression. This trial marks a key demonstration of intrathecal cell therapy’s promise in treating chronic neurodegenerative disorders.

An interim analysis presented at the 2024 ACTRIMS Forum revealed that repeated intrathecal injections of the novel MSC therapy NG-01 led to sustained neurological benefits. These included improved walking speed, better cognitive scores, and favorable biomarker trends. Experimental work in spinal cord injury patients further explores the use of intrathecally delivered exosomes derived from mesenchymal stem cells.

Category-wise Analysis

Drug Insights

By drug, the market is divided into morphine, baclofen, ziconotide, bupivacaine, hydromorphone, clonidine, and others. Among these, morphine is poised to account for nearly 32.8% share in 2025 owing to its potent analgesic properties, established clinical efficacy, and regulatory approval. As the only opioid specifically authorized by the U.S. Food and Drug Administration (FDA) for long-term intrathecal infusion, morphine has a well-documented safety and efficacy profile in managing chronic pain. It is evident in both cancer-related and non-cancer-related conditions.

Baclofen is anticipated to witness considerable growth due to its use in managing severe spasticity, especially when oral treatments fail or cause intolerable side effects. Its efficacy is well-documented in conditions such as multiple sclerosis, cerebral palsy, spinal cord injuries, and post-stroke spasticity. Intrathecal baclofen therapy (ITB) helps deliver the drug directly into the cerebrospinal fluid via an implanted pump. This further leads to targeted muscle relaxation with lower doses compared to oral administration, reducing systemic side effects.

Application Insights

Based on the application, the market is bifurcated into pain management and spasticity. Out of these, pain management is speculated to account for approximately 60.5% of the share in 2025 as the IT route allows direct delivery of medication into the cerebrospinal fluid. It enables precise targeting of the spinal cord’s pain-processing pathways. Recent studies have strengthened the clinical utility of intrathecal drugs in pain management. For instance, in 2024, a multicenter study evaluated intrathecal morphine for patients with advanced cancer pain. It found over 60% improvement in pain scores in the first week of therapy.

Spasticity is a key application of intrathecal drugs as it allows direct modulation of the spinal cord circuits responsible for muscle overactivity. This provides precise control over muscle tone. Conditions, including multiple sclerosis and spinal cord injury, often involve severe and disabling muscle stiffness that is poorly managed with oral medications. Intrathecal delivery enables lower doses of drugs such as baclofen to act locally. It helps minimize side effects such as sedation, dizziness, or liver toxicity that are common with oral therapies.

Zone Insights

West U.S. Intrathecal Drugs Market Trends - Cervical Intrathecal Drug Delivery Eases Cancer Pain Management

In the West, the market has evolved due to expanded clinical applications, technological developments, and increased accessibility. California, Washington, and Oregon have become focal points for the adoption of IT therapies. It is attributed to increased academic research, well-established healthcare infrastructure, and high patient demand. A key development in the West is the implementation of high cervical intrathecal drug delivery for managing craniofacial cancer pain.

A 2025 study revealed that placing the catheter tip of an intrathecal morphine pump into the prepontine cistern effectively lowered refractory craniofacial cancer pain with minimal adverse events. This approach delivers a promising alternative for patients with severe and localized pain unresponsive to conventional treatments. In addition, the integration of telemedicine and remote monitoring has improved the management of IT therapies in this zone.

Southeast U.S. Intrathecal Drugs Market Trends - Double-catheter IDDS Gain Impetus with Improvement of Complex Pain

In the Southeast, the application of IDDS has witnessed notable developments, specifically in managing chronic pain and spasticity. Institutions across Florida, Georgia, and North Carolina have integrated IDDS into their pain management protocols. It shows a broad trend toward targeted and effective treatments. The implementation of double-catheter IDDS for patients experiencing concurrent neck and abdominal cancer pain is another important development.

A 2024 multicenter study demonstrated that this approach effectively managed cancer pain without increasing adverse events. While the initial costs were higher, the double-catheter system provided superior long-term pain control and reduced analgesic costs. This highlighted its potential for broad application in complex pain scenarios. The use of IDDS has also been extended to manage refractory abdominal pain associated with systemic amyloidosis.

Northeast U.S. Intrathecal Drugs Market Trends - Telemedicine and Remote Monitoring Support IDDS Management

In the Northeast, the market growth is propelled by established clinical practices and emerging technologies. Institutions in New York, Massachusetts, and Pennsylvania have adopted IDDS for managing chronic pain and spasticity, showing an ongoing trend toward specialized therapies. The integration of telemedicine and remote monitoring has improved the management of IDDS in the Northeast.

The adoption of these technologies allows continuous assessment and adjustment of treatment plans. It has improved patient outcomes and lowered the requirement for frequent in-person visits. The trend caters to the broad movement toward outpatient care, thereby facilitating highly efficient chronic pain and spasticity management.

Competitive Landscape

Established medical device companies, pharmaceutical firms, and emerging players characterize the U.S. intrathecal drugs market. They are striving to address the rising demand for targeted therapies in chronic pain and spasticity management. Key players dominate by providing a wide range of intrathecal drug delivery systems and formulations.

They use their extensive experience in medical devices and pharmaceuticals to maintain a competitive advantage. Emerging players are introducing new solutions and specialized products to capture significant market shares. They are exploring opportunities in pediatric spasticity management and the development of extended-release formulations to improve patient compliance.

Key Industry Developments

- In January 2025, Novartis achieved a milestone in the development of its gene therapy, Zolgensma (onasemnogene abeparvovec). The firm demonstrated its efficacy in patients aged 2 to less than 18 years with Spinal Muscular Atrophy (SMA) through intrathecal (IT) administration.

- In May 2024, the Polyanalgesic Consensus Conference (PACC) released updated guidelines for IDDS in cancer pain management. The guidelines emphasized patient selection, individualized dosing of morphine and ziconotide, device monitoring, comorbidity management, and safety protocols to improve outcomes and reduce complications.

Companies Covered in U.S. Intrathecal Drugs Market

- Hikma Pharmaceuticals PLC

- Piramal Critical Care Limited

- Baxter International Inc.

- Mylan N.V.

- TerSera Therapeutics LLC

- Pfizer Inc.

- Novartis AG

- Fresenius SE & Co. KGaA

- Amneal Pharmaceuticals LLC

- Viatris Inc.

- Others

Frequently Asked Questions

The U.S. intrathecal drugs market is projected to reach US$ 1.7 Bn in 2025.

Rising prevalence of chronic pain and increasing number of complex surgical procedures are the key market drivers.

The U.S. intrathecal drugs market is poised to witness a CAGR of 3.8% from 2025 to 2032.

Incorporation of regenerative medicine and development of extended-release formulations are the key market opportunities.

Hikma Pharmaceuticals PLC, Piramal Critical Care Limited, and Baxter International Inc. are a few key market players.