- Industrial Goods & Service

- U.S. and Canada Industrial Racking System Market

U.S. and Canada Industrial Racking System Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. and Canada Industrial Racking System Market by Design (Selective Racking, Cantilever Racking, Push Back Racking, Narrow & Wide Aisle Racking, Drive-In Racking, Pallet Flow Racking, Carton Flow Racking, Mobile Racking, Rack Supported Warehouse, Misc.), Carrying Capacity (Light Duty (40 to 200 kg), Medium Duty (0.25 to 1 Ton), Heavy Duty (2-4 Tons).), Ownership (Direct Ownership, Rentals), End-user, and Regional Analysis for 2026 - 2033

U.S. and Canada Industrial Racking System Market Size and Trends Analysis

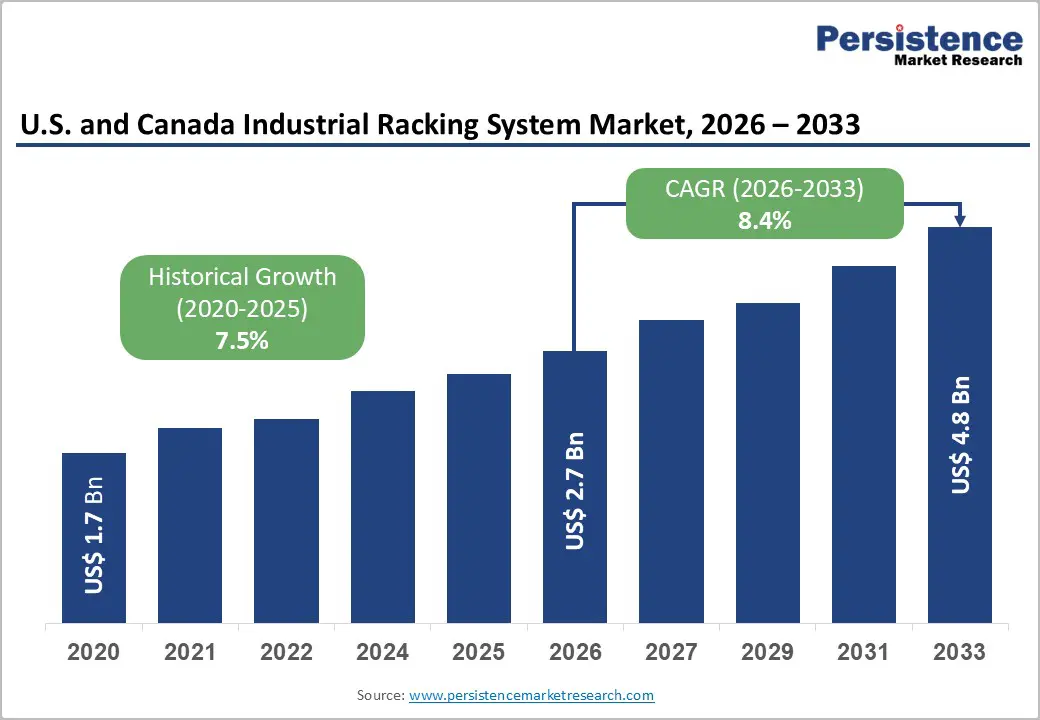

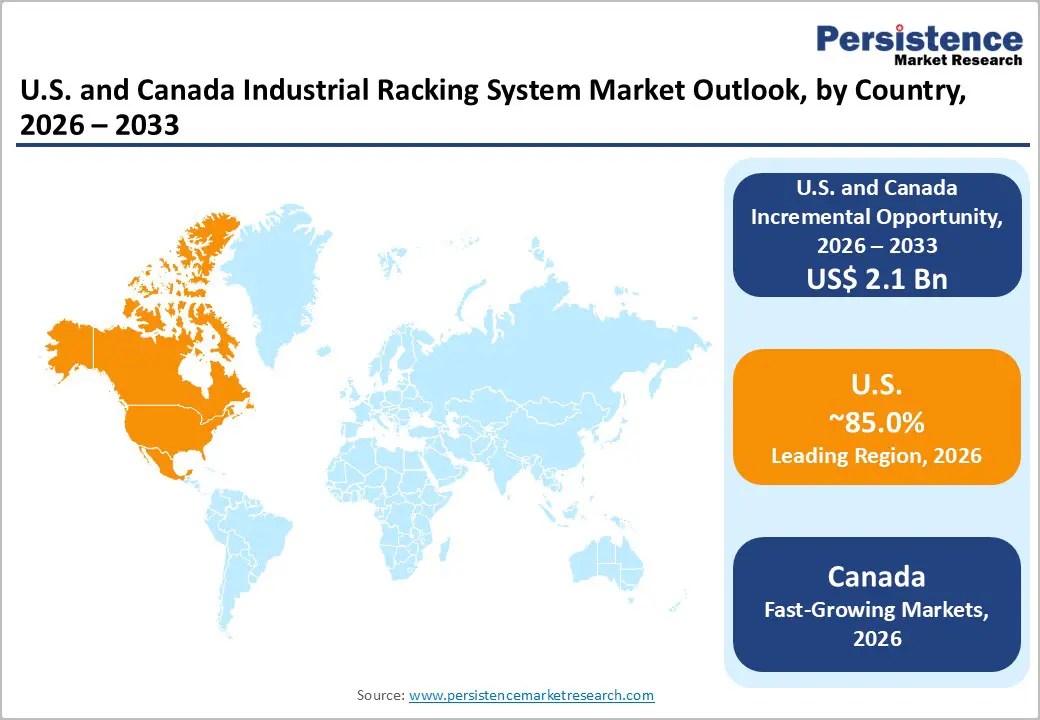

The U.S. and Canada industrial racking system market size is likely to be valued at US$ 2.7 billion in 2026 and is projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

This robust expansion reflects fundamental structural shifts in North American logistics infrastructure, driven by accelerating e-commerce penetration, heightened 3PL automation investments, and regulatory-driven warehouse modernisation.

Key Industry Highlights:

- Key E-commerce Expansion Driving Demand - U.S. retail e-commerce reached US$310.3 billion in Q3 2025, while Canadian e-commerce is projected to hit US$104 billion by 2029, fueling demand for high-throughput, automation-compatible racking systems.

- 3PL Growth Boosts Racking Adoption - Third-party logistics providers, commanding 23.8% market share in 2026, increasingly invest in modular, automated, and multi-client racking solutions to support high-velocity fulfilment operations.

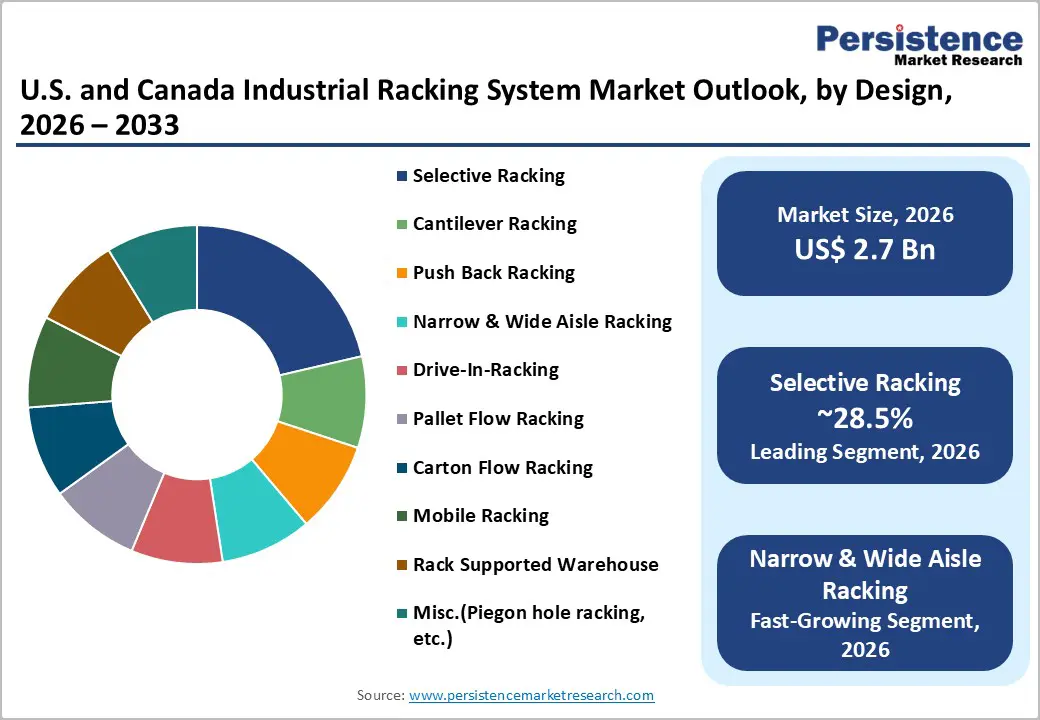

- Selective Racking Leads Design Segment - Selective racking systems dominate with 28.5% market share, valued for versatility, ease of installation, and broad applicability across e-commerce, food & beverage, and automotive warehouses.

- Medium-Duty Racking Commands Capacity Market - Medium-duty systems (0.25 to 1 Ton) capture 52.1% of the market, catering to standard carton-pick, case goods, and general manufacturing needs, while light-duty systems grow fastest for micro-fulfilment and high-velocity SKUs.

- Automation & Robotics Integration as Growth Opportunity - Rising adoption of AS/RS, pallet shuttles, and AMRs drives demand for racking systems engineered for robotic material handling, with manufacturers like Interlake Mecalux and SSI SCHAEFER leading integration capabilities.

| Key Insights | Details |

|---|---|

| U.S. and Canada Industrial Racking System Market Size (2026E) | US$ 2.7 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.5% |

Market Dynamics

Drivers - E-Commerce Acceleration and Last-Mile Fulfilment Demand

E-commerce represents a fundamental structural driver reshaping the industrial racking system market across the U.S. and Canada, requiring specialised storage architectures that accommodate rapid inventory turnover and omnichannel fulfilment. According to the U.S. Census Bureau, retail e-commerce sales in Q3 2025 reached approximately US$ 310.3 billion, representing a 5.1 percent year-over-year increase and accounting for 16.4 percent of total retail sales. In Canada, e-commerce generated approximately US$3.14 billion in December 2024 alone and is projected to reach US$104 billion by 2029.

This substantial expansion directly correlates with demand for flexible racking configurations that enable rapid order consolidation, sortation, and fulfilment functions that become increasingly critical as e-commerce volumes expand. Fulfillment centres operating under peak seasonal demand, such as holiday periods, experience 50Percent order spikes, necessitating scalable racking solutions compatible with automated picking systems.

The Industrial Racking System Market responds by deploying pallet-flow systems, carton-flow configurations, and selective racking designs that maximise throughput while minimising picker travel time, a direct response to e-commerce operators' requirement for <24-hour order processing cycles.

Third-Party Logistics (3PL) Infrastructure Consolidation and Automation Investment

The 3PL sector has emerged as a dominant force in North American warehousing, with 3PLs capturing 34.1 percent of bulk industrial leasing activity leases ≥100,000 sq. ft. through Q3 2025, a substantial increase from 30.6 percent in the prior year. This represents a fundamental shift away from corporate private warehouse networks toward specialised 3PL operations, each requiring proprietary racking configurations optimised for multi-client, high-velocity fulfilment.

The Industrial Racking System Market directly benefits from this consolidation trend, as 3PL providers require integrated warehouse solutions combining traditional storage architectures with automation-ready frameworks. 3PL providers are deploying Autonomous Mobile Robots (AMRs), Automated Storage & Retrieval Systems (AS/RS), and AI-powered Warehouse Management Systems (WMS) to enhance order throughput and reduce operational costs. Approximately 93 percent of warehouse executives surveyed prioritise "improving throughput" as either very important or extremely important.

This automation imperative drives demand for racking systems engineered to interface seamlessly with robotic picking arms, conveyor networks, and sortation equipment capabilities that traditional fixed-design racking systems cannot accommodate. Racking manufacturers are responding by developing automation-compatible configurations, including rack-supported platforms, deep-lane storage systems, and modular designs that integrate with robotic infrastructure.

Regulatory Compliance and Structural Safety Standards

Occupational safety regulations and warehouse industry standards have become increasingly stringent across the U.S. and Canada, establishing minimum structural, load-capacity, and maintenance requirements that directly influence racking procurement decisions. The ANSI MH16.1-2023 standard, published by the Rack Manufacturers Institute (RMI) and referenced by the International Building Code (IBC), establishes mandatory design, testing, and utilisation requirements for industrial steel storage racks. This standard specifies load-application and rack-configuration (LARC) drawing requirements, beam deflection limits (L/180), seismic stability calculations, and annual third-party inspection protocols.

Regulatory frameworks also require clearly posted load-capacity signage, intact footplate/baseplate installations, properly anchored diagonal struts, and documented damage-assessment protocols. These compliance requirements eliminate lower-cost, non-compliant racking designs from the procurement pool, creating a quality floor that favors established manufacturers with engineering and certification capabilities.

Organisations that fail to maintain ANSI-compliant racking systems face operational shutdowns, workers' compensation liabilities, and equipment seizures, creating powerful compliance incentives across North America. The market for compliant racking systems consequently reflects a "quality-first" procurement dynamic in which safety certification, load-rating documentation, and structural integrity are non-negotiable purchasing criteria.

Restraint - High Capital Investment Requirements and SME Affordability Constraints

Steel represents the primary material input for industrial racking systems, creating direct exposure to commodity price fluctuations and supply-chain disruptions. Steel pricing has experienced significant volatility during 2024-2025, driven by cyclical demand patterns, tariff policy shifts, and production capacity constraints in primary steel-producing regions.

Elevated material costs directly compress profit margins for racking manufacturers operating under fixed-price customer contracts or long delivery schedules. Additionally, supply-chain bottlenecks in steel logistics, specialty coating applications (e.g., galvanising, powder coating), and component subassembly create production delays that extend customer lead times, particularly problematic for time-sensitive fulfilment-centre buildouts. Many customers respond to extended lead times and elevated pricing by deferring racking purchases, extending existing system lifecycles, or consolidating racking requirements across multiple distribution facilities to achieve volume discounts. This behaviour creates cyclical demand patterns that amplify industry-wide margin pressure and reduce equipment-purchasing frequency.

Opportunities - Seamless Automation-Racking System Integration and Robotic Material Handling

Warehouse automation and smart logistics infrastructure represent a transformative opportunity in the U.S. and Canada Industrial Racking System Market, driven by labour cost pressures, operational efficiency imperatives, and technological maturation. The regional logistics sector is transitioning from traditional warehousing toward integrated, intelligent systems incorporating automated storage and retrieval systems (AS/RS), robotic picking technologies, machine learning algorithms for demand forecasting, and AI-powered route optimisation. IoT-enabled monitoring systems provide real-time temperature and humidity data and inventory visibility, with predictive maintenance capabilities that prevent equipment failures and reduce unplanned downtime.

The industrial racking system market faces a transformative opportunity through engineered integration of racking systems with advancing robotic material-handling technologies, including Autonomous Mobile Robots (AMRs), Automated Pallet Shuttles, and Robotic Arm picking systems. Advanced racking designs facilitate robotic throughput by optimising clearance specifications, beam configurations, and spatial layouts that enable seamless integration with AMRs and automated picking arms.

Companies including Interlake Mecalux and SSI SCHAEFER have demonstrated market-leading integration capabilities through platforms combining semi-automated pallet shuttles, 3D AS/RS systems, and warehouse management software. At ProMat 2025 in Chicago (February 2025), Interlake Mecalux showcased high-density storage technologies maximising storage capacity while enabling automated pallet handling, directly addressing North American warehousing demand for space optimisation and automation compatibility. The Industrial Racking System Market benefits as customers increasingly specify racking configurations designed explicitly for robotic compatibility, creating differentiated product categories commanding premium pricing and superior margins.

As warehousing automation expands beyond large enterprises (Amazon, Walmart, Home Depot) to mid-market 3PL operators and regional fulfilment centres, demand for affordable, modular automation-compatible racking accelerates. Racking manufacturers that develop cost-effective integration frameworks will capture substantial market share among price-sensitive customers seeking automation benefits without incurring enterprise-scale capital expenditures. Market analysts estimate automation-compatible racking represents the fastest-growing design category, with annual unit growth rates potentially exceeding 12 to 15 per cent through 2030.

Sustainability-Driven Warehouse Modernisation and Net-Zero Supply Chain Initiatives

Environmental regulations and corporate sustainability commitments are driving substantial warehouse modernisation investments across North America, creating demand for energy-efficient, space-optimised storage systems that minimize facility carbon footprints. Advanced racking designs, particularly high-density configurations such as rack-supported warehouses, drive-in systems, and gravity-flow designs, reduce facility square-footage requirements, thereby lowering building energy consumption, HVAC loads, and operational carbon intensity. Companies achieving net-zero supply chain targets require racking systems engineered to maximize vertical space utilisation, minimise forklift travel distances, and support energy-efficient material-handling equipment.

At ProMat 2025, Steel King Industries introduced its SK ADVANTX Structural Bolted Racking System specifically targeting cold storage facilities and automation-compatible warehouses, reflecting market recognition of environmental modernisation drivers. The system's patent-pending bolted upright design enhances flexibility and scalability while supporting reduced-footprint facility designs.

As regulatory frameworks tighten, particularly regarding supply chain environmental accounting and Scope 3 emissions, enterprises are prioritising investments in warehouse infrastructure modernisation. The Industrial Racking System Market benefits through premium pricing for sustainability-optimised designs and accelerated replacement cycles for older, inefficient systems. The estimated market opportunity through 2033 suggests that sustainable racking configurations could account for 15 to 20 percent of total market revenue, with annual growth rates exceeding the standard market CAGR by 2 to 3 percentage points.

Category-wise Analysis

Design Insights

Selective racking systems command the largest design segment share of 28.5% within the U.S. and Canada industrial racking system market, representing the most versatile and cost-effective solution for general-purpose warehousing applications spanning e-commerce, 3PLs, automotive, and food & beverage sectors. Selective racking's market leadership reflects its accessibility to warehouse operators of all sizes, straightforward installation protocols, compatibility with standard forklift equipment, and direct line-of-sight access to every pallet position. The design's simplicity enables rapid operator adoption without extensive training requirements, a critical advantage in labour-constrained markets where operator familiarity directly impacts operational efficiency.

Despite newer, specialised configurations gaining market traction, selective racking's foundational role in warehousing architecture ensures sustained demand driven by replacement cycles, facility expansions, and adoption by emerging markets and smaller distributors.

Narrow and wide Aisle racking systems represent the fastest-growing design category, driven by increasing space-utilisation pressures and warehouse automation integration. These specialised configurations optimise storage density by reducing aisle widths to 2.0 to 2.5 meters, thereby multiplying usable storage capacity within fixed facility footprints, a critical advantage as real estate costs escalate and e-commerce demand requires rapid facility expansion.

The segment's dominance is reinforced by broad applicability across end-use industries and facility types. From pharmaceutical distribution centers supporting temperature-controlled storage to automotive components warehouses accommodating just-in-time delivery requirements, selective racking systems deliver the optimal balance between storage density and accessibility. This broad applicability establishes selective racking as the foundational technology for general-purpose industrial storage, supporting sustained market share across the forecast period. Market adoption is further supported by the segment's cost-effectiveness relative to specialised storage systems, including drive-in, narrow-aisle, and mobile configurations, enabling widespread deployment across large-scale multinational operators and regionally focused SME logistics providers.

Narrow and wide-aisle racking systems achieve rapid expansion within the design segment, driven by intensifying space utilization imperatives in high-value urban real estate, automation integration requirements, and operational density optimization pressures.

Carrying Capacity Insights

Medium-duty racking systems command the largest market share at 52.1% in 2026, reflecting the design's suitability for the broadest customer base across e-commerce, food & beverage, pharmaceutical, and general-purpose manufacturing applications. This capacity range (250-1,000 kg per beam level) accommodates standard carton-pick operations, case goods, and intermediate manufacturing components representing the most common warehouse product categories. Medium-duty designs optimize cost-to-capacity economics, delivering sufficient load capacity for standard warehouse operations without the material and engineering expense of heavy-duty systems.

The segment's dominance reflects adoption breadth across enterprise and mid-market customers, where budget constraints and operational versatility drive specification of medium-duty solutions. Growth projections indicate medium-duty racking will maintain market leadership through 2033, though at slightly moderated growth rates as light-duty and heavy-duty segments capture specialised applications.

Light-duty racking systems represent the fastest-growing capacity category, driven by emerging e-commerce micro-fulfilment centres, specialised pharmaceutical/nutraceutical operations, and retail distribution networks handling small, high-velocity SKUs. Light-duty designs enable compact facility footprints through vertical stacking and space-efficient configurations, directly addressing market pressures toward distributed fulfilment networks serving last-mile delivery requirements.

End-user Insights

Third-party logistics providers represent the largest and most strategically significant end-use segment, commanding a 23.8% market share in 2026 and exhibiting disproportionately high growth relative to other segments. The market consolidation toward 3PL service providers reflects corporate warehouse portfolio optimisation, wherein companies divest private logistics infrastructure in favour of outsourced 3PL partnerships offering specialised expertise, geographic scale, and automation-enabled fulfilment capabilities.

3PLs operate multiple client accounts simultaneously, requiring racking systems engineered for rapid reconfiguration, high-velocity throughput, and compatibility with sophisticated warehouse management systems. This operational complexity drives 3PL procurement toward premium racking designs incorporating advanced features such as rack-supported platforms, automated handling integration, and modular expansion capacity.

E-commerce represents the fastest-growing end-use segment, reflecting fundamental structural shifts toward online retail penetration and the corresponding requirement for specialised fulfilment infrastructure. E-commerce operators require racking systems optimized for omnichannel order fulfilment, emphasizing rapid item picking, carton-flow configurations, and integration with automated sorting equipment. U.S. retail e-commerce achieved US$ 310.3 billion in Q3 2025 with 16.4 percent penetration of total retail sales, while Canadian e-commerce is projected to reach US$ 104 billion by 2029 from approximately US$ 89.4 billion in 2024. This sustained expansion directly correlates with demand for specialised e-commerce racking configurations, with market analysts estimating 14 to 16 percent annual growth rates for e-commerce-specific racking solutions through 2033.

Competitive Landscape

The U.S. and Canada Industrial Racking System market is moderately fragmented, with a diverse mix of large, well-established manufacturers and regional specialists competing across pallet racking, cantilever, and high-density storage solutions. No single company holds overwhelming dominance, but several key players, such as Steel King Industries, Ridg-U-Rak, Inc., Interlake Mecalux, SSI SCHAEFER, Hannibal Industries, and Frazier Industrial Company, are widely recognised for their broad product portfolios and strong North American presence, driving innovation and customisation in warehouse storage systems.

Smaller and mid-tier firms such as Advance Storage Products and Speedrack Products Group further contribute to competitive dynamics by offering specialised and regional solutions tailored to specific end-use industries. The market’s fragmented nature fosters competitive pricing, regional specialisation, and rapid technological adoption, particularly in e-commerce, cold storage, and automation, which needs to accelerate demand for flexible and advanced racking configurations.

Key Developments :

- In January 2026, SSI SCHAEFER and Moffett Automation announced a strategic partnership to integrate free-roaming pallet shuttle systems with warehouse management software and high-density pallet storage technologies. This cooperation enhances deployment of scalable, space-efficient pallet handling systems, a key requirement in modern North American warehouses facing automation, throughput, and layout constraints. The combined solution supports higher storage density and flexible system integration, aligning with ongoing automation adoption in the U.S. and Canadian racking environment.

- In March 2025, Steel King Industries introduced its SK ADVANTX Structural Bolted Racking System at ProMat 2025 in Chicago, targeting the growing needs of automation and cold storage facilities in North America. Featuring a patent-pending bolted upright design that enhances flexibility, scalability, and on-site assembly, the system reflects increasing customer demand for durable, customizable, and automation-friendly racking infrastructure in the U.S. and Canadian warehousing sectors.

Companies Covered in U.S. and Canada Industrial Racking System Market

- North American Steel

- Frazier Industrial Company

- HYMTEX

- Steel King Industries, Inc.

- Ridg-U-Rak, Inc.

- Interlake Mecalux

- SSI SCHAEFER

- Hannibal Industries

- UNARCO Material Handling, Inc.

- Advance Storage Products

- Speedrack Products Group, Ltd.

- CONCOA Storage Solutions

- Plymouth Industries Inc.

- Craftsman Storage System

Frequently Asked Questions

The U.S. and Canada industrial racking system market is projected to be valued at US$ 2.7 Bn in 2026.

The selective racking segment is expected to account for approximately 28.5% of the U.S. and Canada industrial racking system market by design in 2026.

The U.S. and Canada industrial racking system market is expected to witness a CAGR of 8.4% from 2026 to 2033.

The industrial racking system market growth is primarily driven by e-commerce expansion, 3PL consolidation with automation adoption, and stringent regulatory compliance requiring high-quality, flexible, and automation-compatible racking solutions.