- Aerospace & Defense

- U.S. Aircraft Refurbish Market

U.S. Aircraft Refurbish Market Size, Share, and Growth Forecast for 2025 - 2032

U.S. Aircraft Refurbish Market by Aircraft Type (Narrowbody, Widebody, Business & Private Jets, Regional Jets & Misc.), Service Type (Passenger-to-Freighter Conversion, Commercial Refurbishing, VIP Cabin Refurbishing), Refurbishment Type (Interior, Exterior, Systems & Avionics, Conversions & Heavy Modifications), End-use, and Regional Analysis for 2025 - 2032

U.S. Aircraft Refurbish Market Size and Trends Analysis

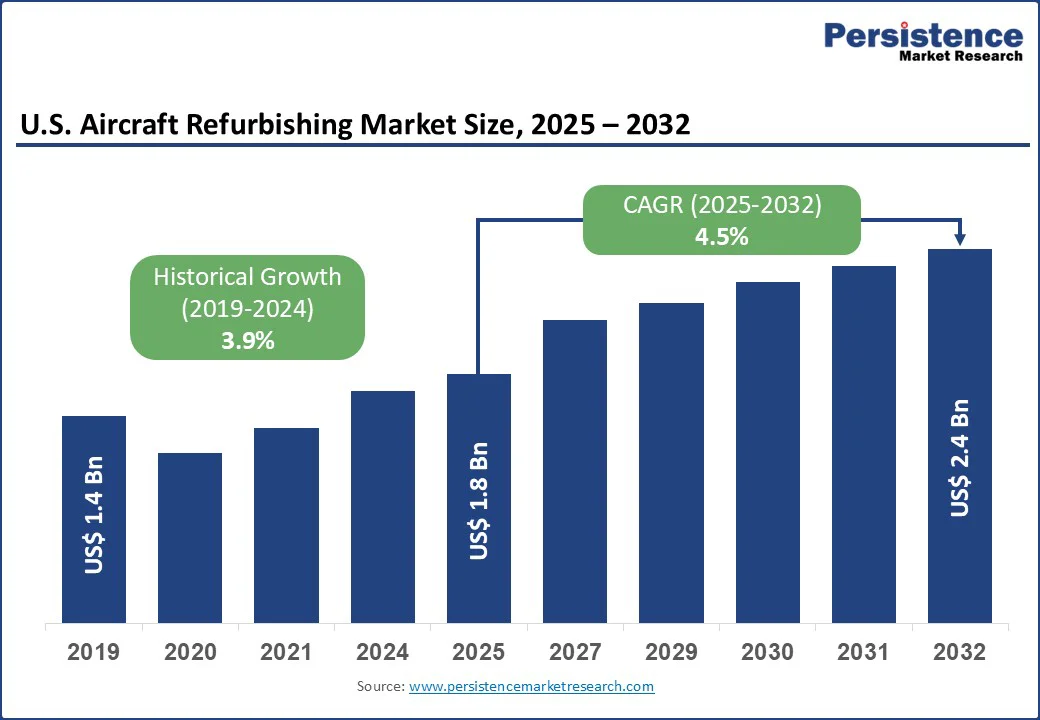

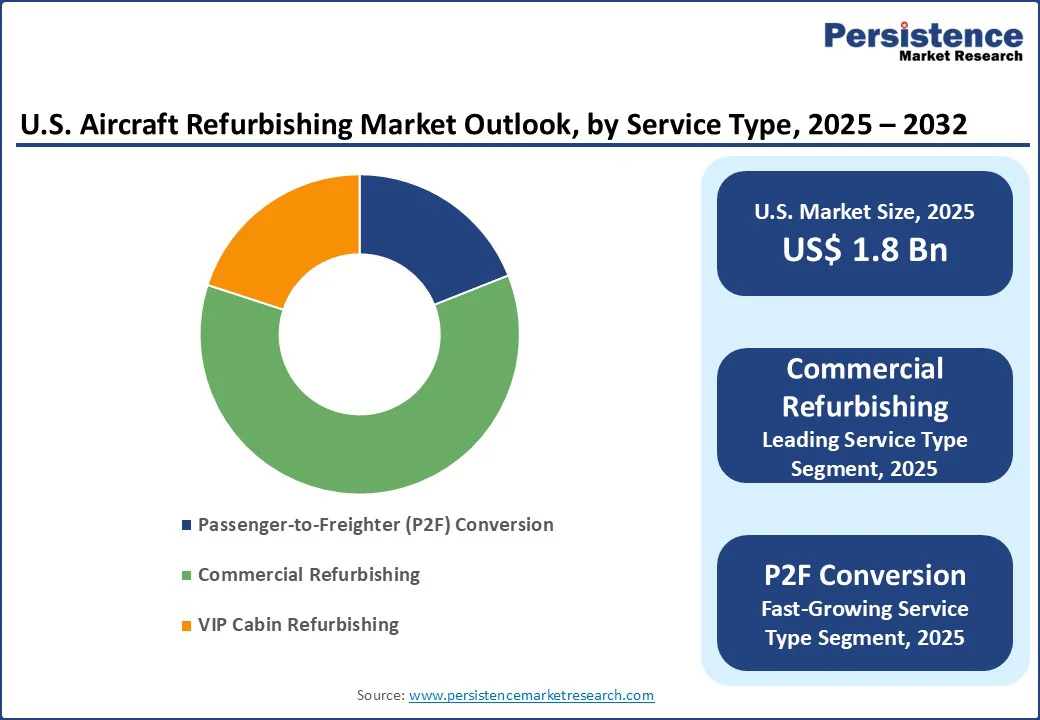

The U.S. Aircraft Refurbish Market size was valued at approximately US$1.8 Bn in 2025, and is expected to reach US$2.4 Bn by 2032, representing a CAGR of 4.5% over the forecast period 2025 - 2032.

Key Industry Highlights:

- Leading Aircraft Type: Narrowbody aircraft command about 42% in 2025, driven by their heavy use on short-haul domestic routes. Frequent cabin refresh cycles and growing passenger demand for comfort and digital connectivity keep refurbishment activity strong in this fleet segment.

- Fast-growing Aircraft Type: Business and private aviation refurbishment is advancing at a 5.2% CAGR, driven by increasing demand for VIP interiors and customized connectivity solutions. Charter operators and fractional ownership firms are consistently investing in upgrades to sustain premium service offerings.

- Leading Refurbishment Type: Interior refurbishment holds roughly 48% share, as airlines prioritize upgrades in seating, cabin lighting, and in-flight entertainment/connectivity systems. Enhancing passenger experience and aligning with evolving comfort standards remain key investment drivers.

- Dominant Service: Passenger-to-Freighter (P2F) conversions are charting the fastest growth at a 5.3% CAGR, supported by the boom in e-commerce logistics and rising cargo demand. Fleet modernization programs from integrators like FedEx and Amazon Air are central to this momentum.

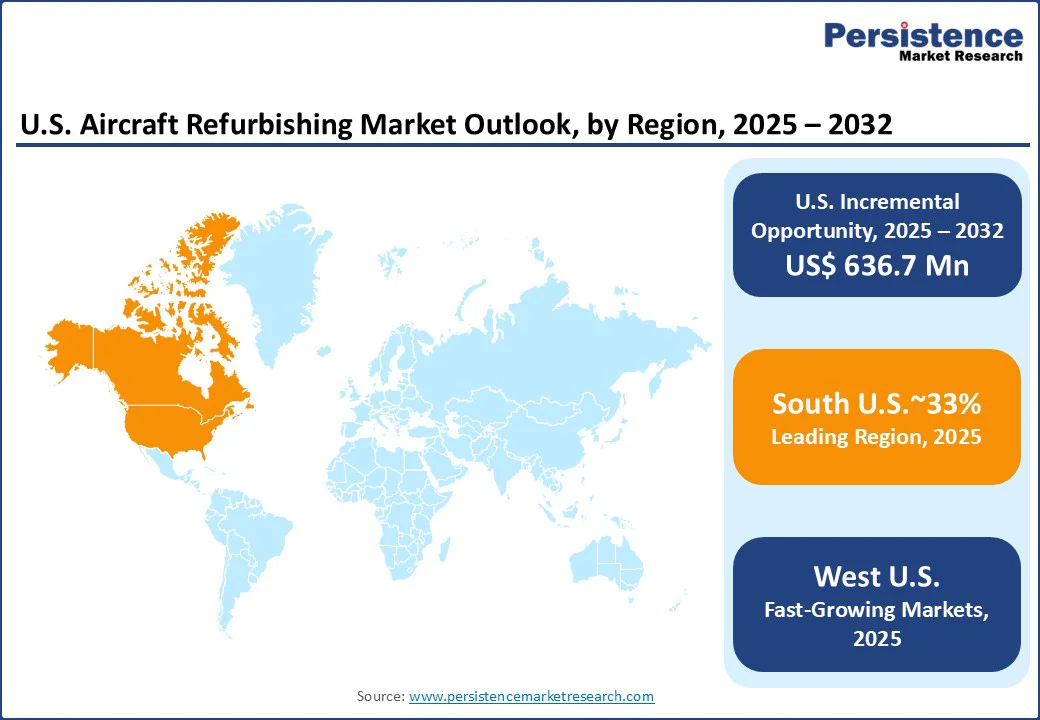

- Leading Zone: U.S. South leads with around 33% share, anchored by major MRO hubs in Texas, Georgia, and Florida. Strong airline presence and active leasing transitions in these states foster dense clusters of refurbishment services.

| Market Attribute | Key Insights |

|---|---|

| U.S. Aircraft Refurbish Market Size (2025E) | US$ 1.8 Bn |

| Market Value Forecast (2032F) | US$2.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.9% |

This expansion is driven by factors such as growing aircraft lifecycles, intensified demand for cabin comfort and fuel-efficient upgrades, evolving regulatory safety and environmental mandates, and rising investment in modular refurbishment technologies.

Market Factors- Growth, Barrier, and Opportunity Analysis

Driver - Expanding Lifecycle and Modernization Trends Propel the U.S. Aircraft Refurbishment Market

Fleet modernization and lifecycle extension initiatives are significantly influencing the U.S. Aircraft refurbishment market. The average age of commercial aircraft in the U.S. reached approximately 14.8 years in 2024, reflecting a gradual increase over the past decades.

Airlines are focusing on interior upgrades, avionics enhancements, and structural modifications to prolong aircraft service life while ensuring adherence to safety and operational standards. Innovations in modular cabin retrofits, lightweight materials, and advanced seating systems enable faster, cost-effective refurbishments that improve passenger experience and operational efficiency.

Regulatory frameworks also drive refurbishment activity. The Federal Aviation Administration (FAA) enforces strict maintenance, inspection, and refurbishment requirements under 14 CFR Part 43, maintaining airworthiness of aging aircraft. Advisory Circulars such as AC 43.13-1B provide detailed guidance for acceptable maintenance, repair, and alteration practices.

Rising passenger expectations for comfort, connectivity, and in-flight entertainment further motivate airlines and business aviation operators to invest in cabin upgrades. These structural, technological, and regulatory factors continue to support sustained demand for refurbishment services across commercial, cargo, and business aviation segments in the U.S. market.

Operational and Regulatory Complexities Limit Refurbishment Expansion in the U.S.

Operational constraints and evolving regulatory requirements are key challenges. Aging aircraft require extensive structural inspections and precise adherence to FAA-mandated standards, such as 14 CFR Part 43, which can extend downtime and disrupt refurbishment scheduling.

Additionally, the integration of advanced avionics and cabin systems often requires specialized engineering approvals and Supplemental Type Certificates (STCs), creating bottlenecks in production and delaying project timelines.

These factors not only increase the complexity of refurbishment projects but also limit the speed at which operators can implement upgrades, particularly for large fleets. As a result, refurbishment providers face logistical and certification hurdles that constrain market adoption and moderate overall growth despite rising demand for interior, exterior, and systems modernization across commercial, cargo, and business aviation sectors.

Digitalization and Sustainable Upgrades Unlock Future Growth in the U.S. Aircraft Refurbish Market

The transition toward digitalization and sustainability represents a major growth opportunity. Airlines and business aviation operators are increasingly adopting modular cabin solutions, advanced materials, and energy-efficient systems to reduce weight, fuel consumption, and carbon emissions.

Incorporating smart avionics, predictive maintenance technologies, and connected cabin systems allows refurbishments to improve operational efficiency while enhancing passenger experience, positioning providers to deliver higher-value, technologically advanced offerings.

Government and industry initiatives reinforce this trend. The Federal Aviation Administration (FAA) promotes the adoption of NextGen avionics and updated maintenance protocols, supporting modernization across aging fleets. Leading manufacturers and MRO providers, including OEM-authorized shops, are investing in digital cabin design tools, lightweight composites, and eco-friendly materials to meet regulatory standards and sustainability goals.

These innovations, combined with increasing regulatory emphasis on emissions reduction and operational efficiency, create a forward-looking market landscape where refurbishment extends beyond maintenance to strategic fleet optimization, ensuring long-term growth opportunities across commercial, cargo, and business aviation segments.

Category-wise Analysis

Service Type Insights

Commercial Refurbishing Leads as P2F Conversions Gain in the U.S. Market

Commercial refurbishing leads the U.S. aircraft refurbish market with an estimated 61% revenue share, reflecting consistent demand from airlines seeking interior, exterior, and systems upgrades to enhance passenger experience and maintain fleet airworthiness.

The segment’s steady growth is supported by airlines’ operational reliance on scheduled maintenance programs and adherence to FAA regulations under 14 CFR Part 43. Passenger-to-Freighter (P2F) conversions are the fastest-growing service at a 6.7% CAGR, driven by expanding e-commerce logistics and cargo fleet modernization initiatives.

VIP cabin refurbishments also play a significant role, particularly in business and private aviation, where operators focus on bespoke interiors and advanced connectivity. Together, these services are reinforced by regulatory frameworks, technological innovations, and rising expectations for efficiency and passenger comfort, creating a balanced market where multiple service types sustain growth while meeting diverse end-user needs.

End-use Insights

Commercial Airlines Dominate While Cargo and Private Aviation Expand Opportunities

Commercial airlines dominate the U.S. aircraft refurbish market, holding an estimated 46% revenue share, driven by the need to maintain passenger comfort, modernize interiors, and comply with FAA safety regulations. Frequent fleet rotations and scheduled maintenance programs reinforce consistent refurbishment demand across narrowbody and widebody fleets.

Cargo and freighter operators represent a fast-growing segment with a 6.3% CAGR, fueled by the surge in e-commerce logistics and P2F conversion initiatives that enhance operational capacity.

Leasing companies and lessors contribute through standardized cabin upgrades and repainting programs to prepare aircraft for new lessees. Business and private aviation, along with government and defense operators, focus on VIP interiors, specialized missions, and advanced connectivity systems.

Regulatory frameworks, technological innovation, and evolving passenger and operational expectations collectively sustain growth across these diverse end-user segments, ensuring that refurbishment remains an essential component of U.S. aviation operations.

Zone Insights

South U.S. Aircraft Refurbish Market Trends

Southern U.S. Leads Aircraft Refurbishments with Major MRO Hubs and Fleet Modernization

Southern U.S. accounts for 33% and remains the leading region, anchored by major MRO hubs in Texas, Georgia, and Florida, where airlines and leasing companies focus on fleet maintenance and modernization. Investments such as Delta TechOps’ 2023 expansion of its Atlanta refurbishment facilities have boosted the region’s capacity for cabin upgrades, avionics modernization, and passenger-to-freighter conversions.

Dense airline operations, combined with proximity to key cargo integrators, sustain strong demand for refurbishment services. Major airports, including Dallas-Fort Worth, Atlanta, and Miami support frequent aircraft rotations, enabling rapid project execution and operational efficiency.

Rising expectations for passenger comfort, technology-enhanced cabins, and efficient turnaround times continue to reinforce the South’s dominant position in the U.S. aircraft refurbishment market.

West U.S. Aircraft Refurbish Market

Western U.S. Emerges as a Hub for Advanced Business and Private Aircraft Refurbishments

Western U.S., growing at a CAGR of around 4.7%, is becoming a key market for aircraft refurbishment, driven by business and private aviation operators in California and Arizona seeking VIP cabin transformations, cutting-edge connectivity, and upgraded avionics.

Expansions at MRO facilities, such as Jet Aviation’s California center in 2023, have accelerated turnaround times for complex cabin and systems upgrades. The concentration of corporate fleets, proximity to major technology hubs, and a skilled workforce experienced in high-end aviation modifications have strengthened the region’s capabilities.

Airports in Los Angeles, San Francisco, and Phoenix support frequent fleet rotations, enabling operators to implement rapid upgrades and maintain operational efficiency. Rising expectations for luxury interiors and advanced digital systems continue to position the Western U.S. as a fast-growing center for sophisticated aircraft refurbishment services.

North U.S. Aircraft Refurbish Market Trends

Northeast U.S. Drives Aircraft Refurbishment Through Legacy Fleets and Hub-Centric Operations

Northeastern U.S., accounts for a 24% share in 2025. It is anchored by legacy commercial airline fleets concentrated in New York, Massachusetts, and Pennsylvania. Airlines in this region prioritize interior refurbishments, avionics modernization, and structural updates to comply with federal safety regulations and extend aircraft lifecycle.

In 2023, partnerships like Lufthansa Technik’s collaboration with New York and Boston carriers enhanced regional refurbishment capacity and reduced project turnaround times.

Major hubs such as JFK, Logan, and Philadelphia airports support frequent fleet rotations, enabling airlines to implement upgrades efficiently. State-level initiatives in Massachusetts and New York promoting workforce training for MRO operations further strengthen refurbishment capabilities. These factors position the Northeast as a critical region for sustaining operational reliability and meeting compliance standards across commercial and business aviation segments.

Competitive Landscape

The U.S. Aircraft Refurbish Market includes refurbishment providers who focus on advanced cabin digitalization, lightweight materials, and avionics modernization while aligning with FAA regulations and certification standards. These strategic initiatives intensify competition, encouraging innovation and service differentiation, and strengthening supplier and distributor networks for specialized components.

By streamlining material sourcing and MRO operations, the market experiences improved turnaround times, enhanced operational efficiency, and expanded capacity, creating a more resilient and growth-oriented ecosystem across commercial, cargo, and business aviation sectors.

Industry Developments:

- In August 2025, Jet Aviation acquired ASTONSKY's ground handling, hangarage, and FBO operations at Paris-Le Bourget Airport. This acquisition expands Jet Aviation’s global footprint in fixed-base operations, allowing it to offer integrated MRO and refurbishment services to high-value business and private aircraft clients across Europe and North America.

- In August 2024, StandardAero acquired Aero Turbine Inc., a provider of MRO services for military engines and accessories. It enhances StandardAero’s defense capabilities by adding specialized engine and accessory maintenance expertise, enabling faster turnaround and expanded service offerings for U.S. military and government aircraft programs.

- In November 2024, FEAM Aero partnered with SkyDrive, a Japanese eVTOL manufacturer, to explore maintenance services for advanced air mobility aircraft in North America. This partnership positions FEAM Aero at the forefront of emerging eVTOL and urban air mobility markets, providing specialized inspection, maintenance, and refurbishment services for next-generation electric aircraft platforms.

Companies Covered in U.S. Aircraft Refurbish Market

- AAR Corp

- StandardAero

- FEAM Aero

- Trimec Aviation

- Lufthansa Technik North America

- Jet Aviation

- Gulfstream Aerospace

- SIA Engineering Company

- Sabreliner Aviation

- Rose Aircraft Services

- Nextant Aerospace

- AFI KLM E&M

- MTU Aero Engines

- Pratt & Whitney

- Rolls-Royce

Frequently Asked Questions

The U.S. Aircraft Refurbish market is set to reach US$ 1.8 Bn in 2025.

Ongoing efforts to extend aircraft service life, paired with investments in cabin, avionics, and structural upgrades, are fueling refurbishment demand across commercial, cargo, and business aviation sectors in the U.S.

The market growth is estimated to rise at a CAGR of 4.5% from 2025 to 2032.

The adoption of advanced digital technologies, coupled with eco-friendly cabin and systems upgrades, is creating new growth opportunities across the U.S., enhancing operational efficiency, passenger experience, and long-term fleet sustainability.

The major players dominating the U.S. Aircraft Refurbish Market are AAR Corp, StandardAero, FEAM Aero, Trimec Aviation, and Lufthansa Technik North America.