- Healthcare Services

- Dyslexia Treatments Market

Dyslexia Treatments Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Dyslexia Treatments Market by Drug Type (Central Nervous Stimulants, Selective Norepinephrine Reuptake Inhibitors (SNRIs), Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis from 2026 - 2033

Dyslexia Treatments Market Share and Trends Analysis

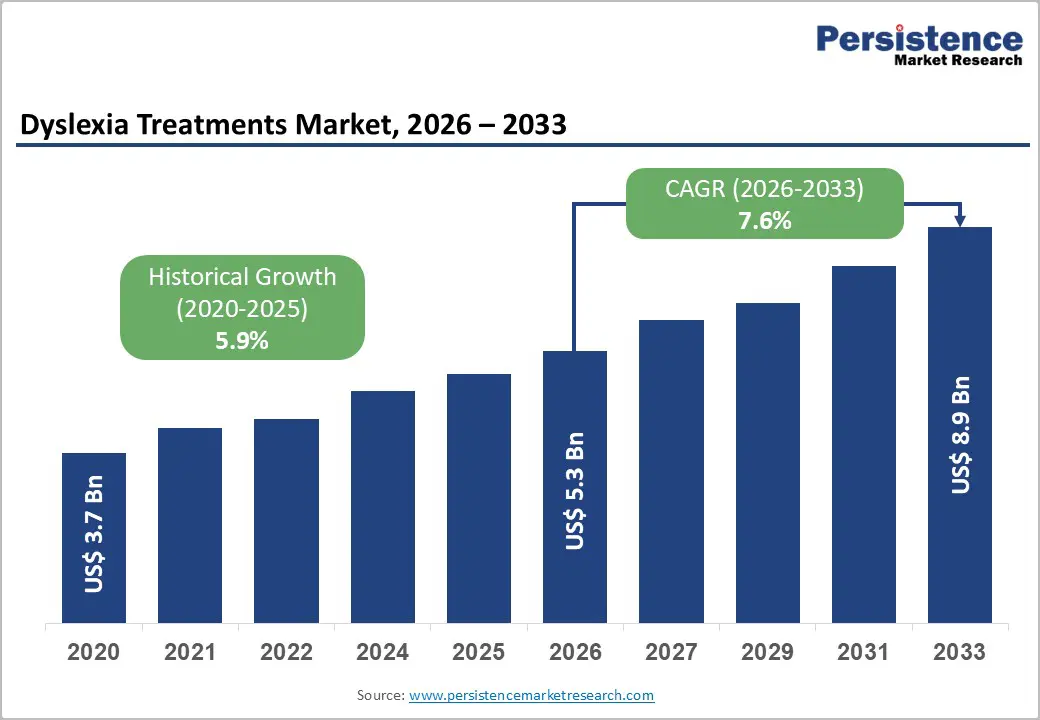

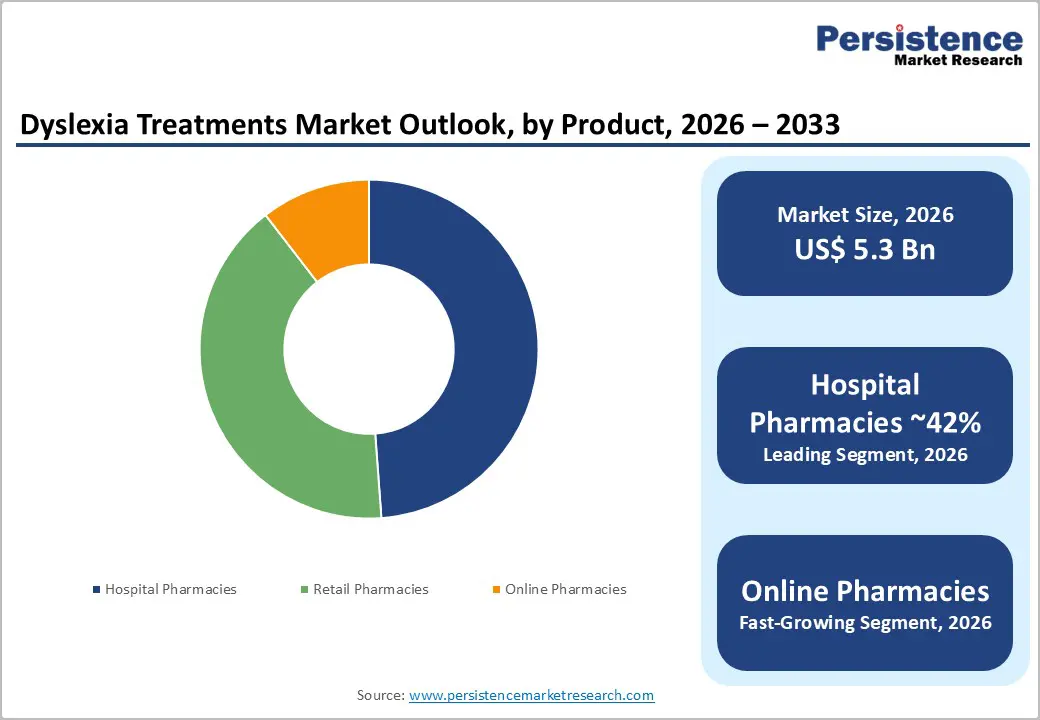

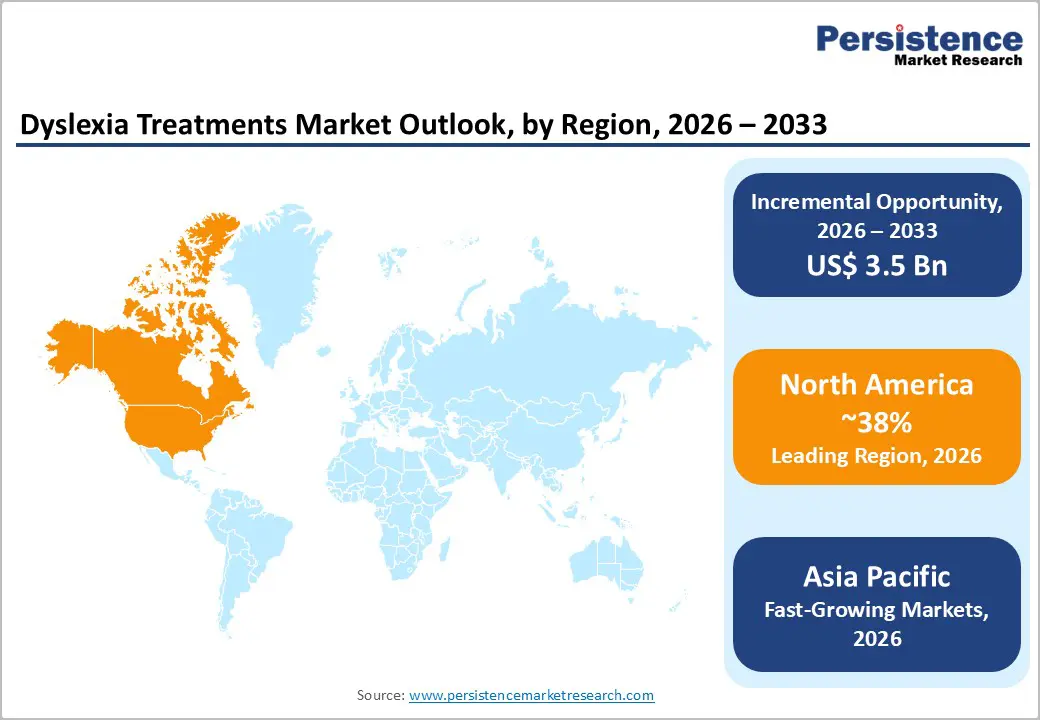

The global dyslexia treatments market size is likely to be valued at US$5.3 billion in 2026 and grow to US$8.9 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033.

The dyslexia treatments market (drug-based) focuses on pharmacological interventions that address cognitive, attention, and related neurological challenges in individuals with dyslexia, often targeting comorbid conditions such as ADHD. It comprises central nervous system stimulants, antihistamines, and other supportive drugs to improve attention, memory, and learning. Growth is driven by rising diagnoses of dyslexia and associated cognitive disorders, increasing awareness of pharmacological support, and expanding research in neurotherapeutics. North America leads due to its established healthcare infrastructure and high adoption of CNS drugs, while the Asia Pacific is the fastest-growing region, fueled by rising awareness and expanding healthcare access.

Key Industry Highlights

- The global drug-based dyslexia treatments market is witnessing steady growth due to increasing diagnoses of dyslexia and comorbid conditions.

- Central nervous system (CNS) dominates the market, helping improve attention and cognitive processing. Antihistamines and other adjunctive drugs are also used to manage vestibular and sensory issues.

- North America holds the largest market share due to high awareness, healthcare infrastructure, and adoption of CNS drugs.

- Leading Drug Type: Methylphenidate improves focus, working memory, and attention, which can indirectly support learning in dyslexic patients.

| Key Insights | Details |

|---|---|

|

Dyslexia Treatments Market Size (2026E) |

US$5.3 Bn |

|

Market Value Forecast (2033F) |

US$8.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Dynamics

Driver - Advancements in CNS-targeted Drugs

Advancements in CNS-targeted Drugs have become a significant driver in the drug-based dyslexia treatment market. Over the past decade, research in neuropharmacology and cognitive neuroscience has led to the development of novel neurostimulants and cognitive enhancers specifically aimed at improving attention, working memory, and learning capabilities in individuals with dyslexia. These drugs primarily target the central nervous system (CNS), modulating neurotransmitter activity such as dopamine and norepinephrine, which are often implicated in attention deficits and learning difficulties associated with dyslexia. Pharmaceutical companies are increasingly focusing on creating formulations with improved efficacy, faster onset of action, and reduced side effects, making them more acceptable for long-term pediatric and adolescent use.

Clinical trials and real-world studies have demonstrated that these CNS-targeted therapies can significantly enhance cognitive processing speed, reading fluency, and overall academic performance in patients with dyslexia, thereby increasing physician confidence in prescribing these medications. Additionally, innovations in drug delivery systems, such as extended-release tablets and pediatric-friendly formulations, are helping to improve adherence and therapeutic outcomes. With growing awareness among parents, educators, and clinicians regarding the neurological basis of dyslexia, the adoption of these advanced pharmacological interventions is expanding rapidly. Overall, continuous advancements in CNS-targeted drugs are not only providing better symptom management for dyslexic patients but also creating a robust growth trajectory for the global drug-based dyslexia treatments market.

Restraints - Preference for Non-Pharmacological Interventions

One of the significant restraints in the drug-based dyslexia treatments market is the strong preference for non-pharmacological interventions among parents, educators, and caregivers. Many stakeholders view dyslexia primarily as a learning or cognitive challenge rather than a medical condition requiring medication. As a result, therapies such as structured literacy programs, cognitive training, one-on-one tutoring, and digital learning tools are often favored over pharmacological solutions. These interventions focus on improving reading, writing, and comprehension skills through personalized instruction, adaptive learning software, and evidence-based educational techniques. The emphasis on non-drug strategies is particularly strong in early education, where parents and teachers are cautious about introducing medications that may carry side effects or long-term health risks.

Additionally, the growing availability of technology-driven solutions, such as educational apps and gamified learning platforms, provides engaging alternatives that can be customized to a child’s pace and learning style. This trend reduces reliance on pharmacological treatments, limiting prescription rates and slowing market growth for drugs targeting dyslexia. Moreover, social and cultural factors, including concerns about medicating children and the desire for natural developmental approaches, reinforce the preference for non-pharmacological interventions. Overall, while drug therapies like Methylphenidate address attention deficits associated with dyslexia, the widespread adoption of alternative learning methods continues to act as a key market restraint.

Opportunity - Rising Personalized Medicine and Therapies

The development of customized treatment regimens based on the distinct cognitive, genetic, and behavioral profiles of dyslexic individuals is made possible by personalized medicine, which raises the general efficacy of therapies. With sophisticated diagnostic instruments, it is possible to pinpoint the unique cognitive and neurological traits linked to dyslexia in every person, allowing for the development of individualized treatment plans. The development of therapies that target the particular genetic components of dyslexia can be guided by the insights gained from genetic testing and biomarker analysis into the underlying genetic variables that contribute to the condition. Functional magnetic resonance imaging (fMRI) and other neuroimaging techniques can be used to discover neural patterns linked to dyslexia, leading to individualized interventions targeting certain brain regions.

Moreover, personalized educational interventions can be created to meet the unique needs, skills, and learning styles of each dyslexic person, maximizing their learning potential. Based on a person's cognitive profile, cognitive training programs can be tailored to address particular areas of weakness and offer exercises that specifically target those skills. Pharmacogenomics is a science that aims to find genetic variants that impact pharmaceutical reactions, hence facilitating the creation of individualized pharmacological therapies for dyslexia. Personalized techniques guarantee that therapies are modified over time by the individual's changing needs and reactions, enabling ongoing monitoring and follow-up.

Category-wise Analysis

By Drug Type Insights

Methylphenidate-based drugs account for the highest share due to their direct therapeutic relevance and established clinical efficacy. Dyslexia, a neurodevelopmental disorder characterized by difficulties in reading, writing, and language processing, is often associated with attention deficits and cognitive challenges. Methylphenidate, a central nervous system stimulant, helps improve focus, working memory, and executive functioning, thereby indirectly enhancing learning outcomes for dyslexic patients.

Its widespread adoption is supported by extensive clinical studies demonstrating efficacy in children and adolescents with attention-related learning difficulties. Also, Methylphenidate is approved in several countries for treating attention-deficit disorders.

In contrast, Cyclizine, Meclizine, and Dimenhydrinate are primarily antiemetic drugs used to treat nausea, vertigo, and motion sickness. These medications do not target the core cognitive or attention deficits associated with dyslexia, which limits their clinical use in this patient population. As a result, their prescription rates and market penetration in the dyslexia segment are minimal. The clear therapeutic advantage, strong clinical adoption, and regulatory approvals for Methylphenidate make it the dominant drug type in this market, while the other three drugs remain peripheral and largely irrelevant for dyslexia treatment.

By End-user Insights

Hospital pharmacies account for the highest share among end-use channels, primarily due to the prescription nature of the drugs used, especially Methylphenidate-based medications. These drugs are classified as controlled substances in many countries, requiring strict regulatory oversight and a valid prescription from a licensed physician. Hospitals and specialty clinics are the primary points of consultation for patients diagnosed with dyslexia, particularly children and adolescents, who need careful assessment before starting pharmacological treatment.

Consequently, prescriptions are usually dispensed directly through hospital pharmacies, ensuring compliance with legal requirements, proper dosing, and continuous monitoring for side effects.

In comparison, retail pharmacies serve mainly as secondary channels for refills or repeat prescriptions, and their share is limited by the initial dependency on hospital consultations. Online pharmacies, while increasingly popular due to convenience and home delivery options, face strict regulations regarding controlled substances, mandatory prescription verification, and regional legal restrictions, which constrain their current market penetration. Additionally, hospital pharmacies often provide counseling and guidance to caregivers, reinforcing trust and adherence to treatment protocols.

Overall, the combination of regulatory compliance, direct access to patients, and the need for professional oversight makes hospital pharmacies the dominant end-use channel in the dyslexia drug treatment market.

Region-wise Insights

North America Dyslexia Treatments Market Trends

North America leads the global dyslexia treatments market, driven by a combination of high disease awareness, advanced healthcare infrastructure, and strong regulatory support for neurodevelopmental disorders. In the region, early diagnosis and intervention programs are widely implemented in schools and pediatric clinics, which increases the demand for pharmacological treatments such as Methylphenidate-based drugs for attention and learning support in dyslexic children. The presence of well-established healthcare facilities, specialist clinics, and hospital pharmacies ensures easy access to prescription medications, further strengthening market penetration.

In the U.S., which dominates the regional market, rising prevalence of learning disorders, combined with heightened awareness among parents and educators, has boosted prescription rates for approved dyslexia-related drugs. Government initiatives and insurance coverage for neurodevelopmental disorders enhance affordability and encourage timely treatment. Additionally, extensive research and clinical trials in the U.S. support innovation and the introduction of new formulations or combination therapies, maintaining high adoption rates. Technological integration in healthcare, including electronic prescription systems and telemedicine, also facilitates access to treatment.

Overall, North America is characterized by strong regulatory frameworks, robust healthcare infrastructure, and high adoption of pharmacological interventions, positioning it as the leading region for dyslexia treatments globally.

Asia Pacific Dyslexia Treatments Market Trends

Asia Pacific is emerging as the fastest-growing region in the global dyslexia treatments market, driven by increasing awareness of learning disorders, improving healthcare infrastructure, and rising adoption of pharmacological interventions. Countries such as China, India, Japan, and South Korea are witnessing growing recognition of dyslexia in schools and pediatric healthcare systems, which is fueling demand for approved drugs like Methylphenidate-based treatments. The expansion of specialized clinics, pediatric hospitals, and hospital pharmacies is improving accessibility to prescription medications, while government initiatives in certain countries are promoting early diagnosis and intervention programs.

Rapid urbanization, increasing parental awareness, and rising disposable incomes are enabling more families to seek professional treatment for dyslexia, including pharmacological options. Additionally, the region is seeing an uptick in clinical research and local manufacturing of relevant drugs, which supports affordability and availability. Although non-pharmacological interventions remain popular, the growing acceptance of evidence-based medications is expanding the market.

The combination of rising awareness, improving healthcare access, and a growing population of school-age children positions the Asia Pacific as a key emerging market for dyslexia treatments, with substantial growth potential over the next decade.

Competitive Landscape

The global dyslexia treatments market is highly competitive, driven by innovation in pharmacological formulations and the growing demand for effective cognitive support therapies. Key players focus on research and development, product differentiation, and regulatory compliance to strengthen their market position. Strategies such as partnerships with healthcare institutions, clinical trial collaborations, and regional expansion are commonly adopted to increase market penetration. The competition also emphasizes the development of child-friendly and extended-release formulations to enhance patient adherence.

Key Industry Developments:

- In October 2025, Dysolve, the first artificial intelligence-powered platform for dissolving dyslexia and associated learning disabilities, paved the way for a new treatment approach.

- In December 2022, the All-India Institute of Medical Sciences (AIIMS) declared that an app was being developed to treat dyslexia in youngsters. Developed under the AIIMS Paediatric Neurology Dyslexia Remedial Intervention Programme, this eight-module program will enable dyslexia treatment to be completed while seated at home.

Companies Covered in Dyslexia Treatments Market

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Company Limited

- GSK plc

- Eli Lilly and Company

- Sun Pharmaceutical Industries Ltd.

- Novartis AG

- Endo Pharmaceuticals Inc.

- Purdue Pharma

- Apotex Corporation

- Other

Frequently Asked Questions

The global dyslexia treatments market is projected to be valued at US$5.3 Bn in 2026.

The Global Dyslexia Treatments Market is primarily driven by the rising prevalence of dyslexia and related learning disorders among children and adolescents worldwide.

The global market is poised to witness a CAGR of 7.6% between 2026 and 2033.

The global dyslexia treatments market presents several significant growth opportunities. Increasing awareness of learning disorders in emerging economies offers potential for market expansion.

Teva Pharmaceutical Industries Ltd., Pfizer Inc., GSK plc, Eli Lilly and Company, and others.