- Biotechnology

- Pathogen Identification and Treatment Market

Pathogen Identification and Treatment Market Size, Share, and Growth Forecast, 2025 - 2032

Pathogen Identification and Treatment Market by Test Type (Molecular Diagnostics, Culture-Based Techniques, Immunological Techniques, Mass Spectrometry, Next-Generation Sequencing), Pathogen Type (Bacterial Pathogens, Viral Pathogens, Fungal Pathogens, Parasitic Pathogens, Prions), End-use, and Regional Analysis for 2025 - 2032

Pathogen Identification and Treatment Market Size and Trend Analysis

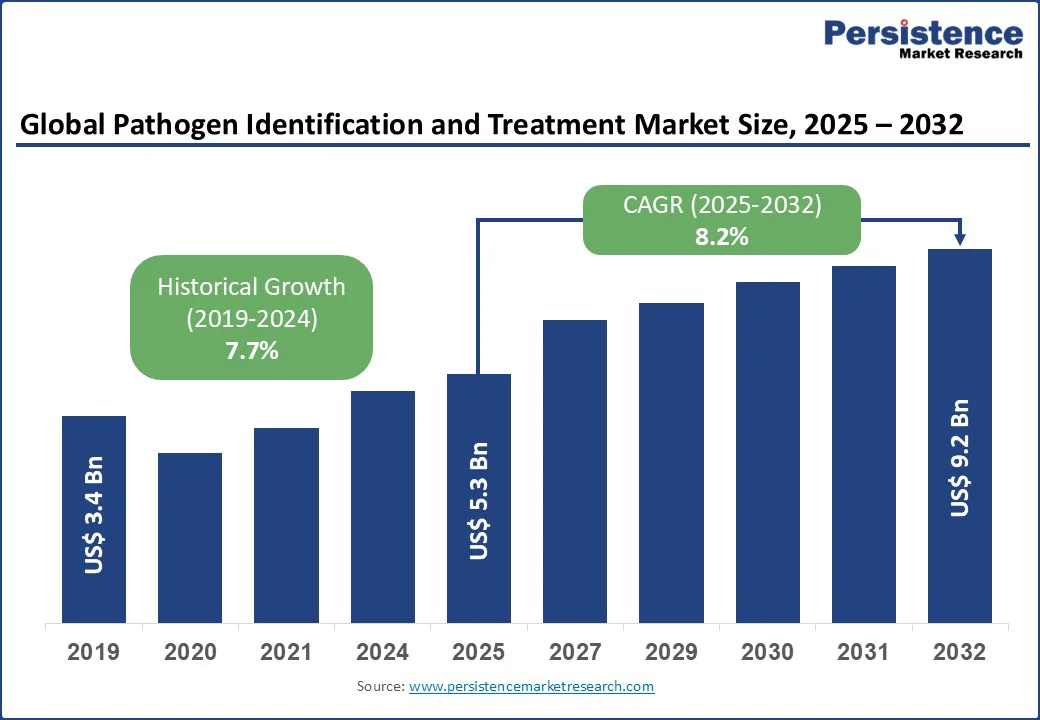

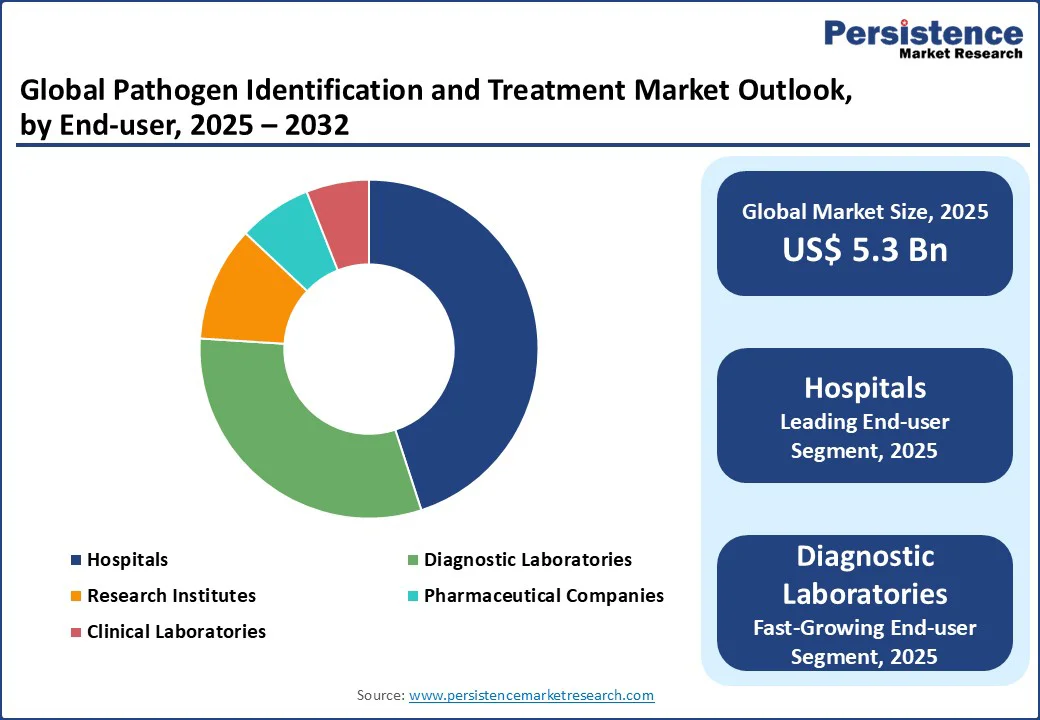

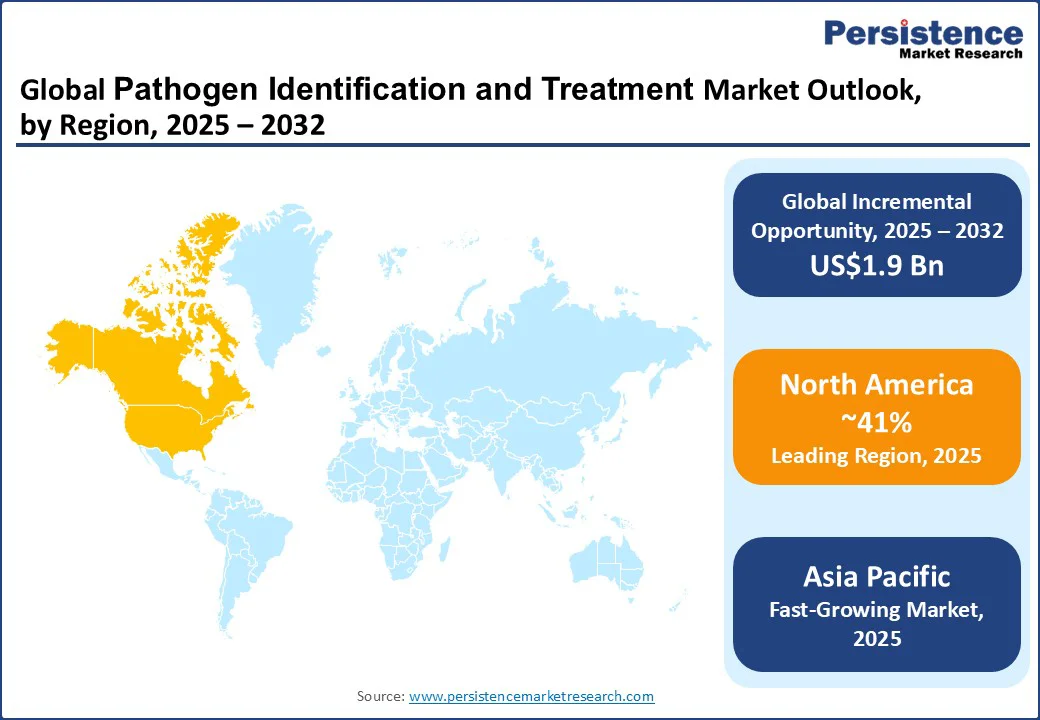

The global pathogen identification and treatment market size is likely to value at US$5.3 Bn in 2025 and expected to reach US$9.2 Bn by 2032, growing at a CAGR of 8.2% during the forecast period from 2025 to 2032. The pathogen identification and treatment market is driven by the increasing prevalence of infectious diseases, advancements in diagnostic technologies, and rising demand for rapid and accurate pathogen identification.

Key Industry Highlights

- Leading Region: North America holds a 41% share in 2025, driven by advanced healthcare infrastructure and high investment in diagnostic technologies in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, fueled by rising healthcare expenditure and increasing infectious disease prevalence in China and India.

- Dominant Test Type: Molecular diagnostics accounts for a 38% share, favored for its precision and rapid detection capabilities across various pathogens.

- Leading End-use: Hospitals contribute over 45% of market revenue, driven by the high volume of diagnostic tests and treatment protocols for infectious diseases.

| Key Insights | Details |

|---|---|

|

Pathogen Identification and Treatment Market Size (2025E) |

US$ 3.4 Bn |

|

Market Value Forecast (2032F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.7% |

Market Dynamics

Driver - Rising Prevalence of Infectious Diseases and Antimicrobial Resistance

The pathogen identification and treatment market is strongly driven by the rising prevalence of infectious diseases and the growing threat of antimicrobial resistance (AMR), which collectively pose a significant global health burden. According to the World Health Organization, infectious diseases account for nearly 25% of deaths worldwide, with bacterial infections alone responsible for over 7.7 million fatalities annually. The COVID-19 pandemic further highlighted the critical importance of rapid and accurate pathogen detection, emphasizing the need for timely diagnosis to prevent disease spread and implement effective treatment strategies.

Antimicrobial resistance has intensified this demand, as pathogens such as methicillin-resistant Staphylococcus aureus, multidrug-resistant tuberculosis, and carbapenem-resistant Enterobacteriaceae have become increasingly prevalent. Traditional culture-based diagnostics often require 48–72 hours to identify pathogens and determine susceptibility, delaying targeted treatment. Advanced molecular diagnostics, such as PCR and real-time PCR, next-generation sequencing platforms by Illumina, and mass spectrometry systems such as MALDI-TOF from Bruker, now enable rapid detection of pathogens and their resistance profiles within hours, allowing clinicians to prescribe precise therapies and reduce mortality rates. Healthcare facilities across North America, Europe, and emerging markets are investing heavily in these technologies to combat AMR, enhance patient outcomes, and support antimicrobial stewardship programs. The growing disease burden and global emphasis on infection control are thus key drivers fueling robust growth in the pathogen identification and treatment market.

Restraint - High Costs of Advanced Diagnostic Technologies

The pathogen identification and treatment market faces a significant restraint in the form of high costs of advanced diagnostic technologies, which limit accessibility, particularly in smaller healthcare facilities and developing regions. Sophisticated platforms such as next-generation sequencing (NGS), mass spectrometry systems, and automated molecular diagnostic instruments require substantial initial investment. Beyond purchase costs, these systems incur ongoing expenses for reagents, maintenance, software updates, and quality control.

For instance, MALDI-TOF mass spectrometry systems and Illumina next-generation sequencers are widely used for rapid and precise pathogen identification but are often cost-prohibitive for smaller laboratories. Operating these technologies also demands highly trained personnel in molecular biology, bioinformatics, and data analysis.

The shortage of qualified laboratory scientists, particularly in emerging markets such as India, Brazil, and parts of Africa, further compounds operational challenges. The combination of high capital and operational costs, along with the need for specialized personnel, remains a major barrier to the widespread adoption of advanced pathogen identification technologies, restraining market growth despite increasing demand.

Opportunity - Growing Adoption of Point-of-Care Diagnostics

The growing adoption of point-of-care (POC) diagnostics presents a significant opportunity for the healthcare and diagnostics market. POC diagnostics enable rapid, on-site testing that delivers results within minutes, reducing dependence on centralized laboratories and expediting clinical decision-making. This capability is particularly valuable in emergency care, rural healthcare settings, and regions with limited infrastructure, where timely diagnosis can directly impact patient outcomes. For instance, rapid POC tests for infectious diseases such as COVID-19 and influenza have proven essential in containing outbreaks by enabling quick isolation and treatment.

The increasing prevalence of infectious diseases, chronic conditions such as diabetes and cardiovascular disorders, and the global emphasis on early detection are driving demand for portable and user-friendly diagnostic solutions. POC devices enhance accessibility, allowing healthcare providers to monitor and diagnose patients at the bedside, in outpatient clinics, or even at home. For example, handheld blood glucose meters and portable ECG devices empower patients to manage chronic conditions more effectively.

Furthermore, technological advancements, including miniaturization, biosensors, and integration with digital health platforms, are making POC diagnostics more accurate, affordable, and scalable. The opportunity also lies in the growing trend toward personalized healthcare and telemedicine, where POC devices play a crucial role by enabling remote monitoring and data sharing in real time. With rising healthcare costs and pressure on systems to improve efficiency, the adoption of POC diagnostics offers a transformative path toward faster, cost-effective, and patient-centric care delivery.

Category-wise Analysis

Test Type Insights

Molecular diagnostics holds the largest market share, approximately 38% in 2025, due to its high sensitivity, specificity, and ability to detect a wide range of pathogens, including bacteria, viruses, and fungi. Widely used in hospitals and clinical laboratories for the rapid detection of pathogens such as Mycobacterium tuberculosis and SARS-CoV-2, it ensures compliance with global health standards. Companies such as Roche Diagnostics and QIAGEN N.V. leverage PCR-based systems for their scalability and reliability, particularly in North America and Europe, where demand for precision diagnostics is high.

NGS is the fastest-growing segment, driven by its ability to provide comprehensive genomic data for pathogen identification and AMR profiling. Ideal for complex infections and emerging pathogens, NGS meets the rising demand for personalized treatment strategies. Firms such as Illumina Inc. and Thermo Fisher Scientific are expanding NGS offerings, especially in research institutes and pharmaceutical companies, driven by increasing R&D investments in North America and the Asia Pacific.

Pathogen Type Insights

Bacterial pathogens account for a 29% share in 2025, driven by the global rise in antibiotic-resistant infections, such as methicillin-resistant Staphylococcus aureus (MRSA). The need for accurate identification to guide targeted antibiotic therapy fuels demand for diagnostic solutions. Companies such as Danaher Corporation and Merck KGaA provide advanced diagnostic kits for bacterial detection, particularly in hospitals and clinical laboratories in North America and Europe.

Viral pathogens are the fastest-growing segment, propelled by the increasing incidence of viral outbreaks, such as influenza and coronaviruses. The demand for rapid viral detection, especially in pandemic preparedness, drives the adoption of molecular diagnostics and immunological techniques. Companies such as Hologic Inc. and PerkinElmer Inc. are innovating with rapid viral testing solutions, particularly in the Asia Pacific, where viral disease prevalence is high.

End-use Insights

Hospitals account for over 45% of market revenue in 2025, driven by the high volume of diagnostic tests and treatment protocols for infectious diseases. Sterilization ensures safety and shelf life for products such as spices, dairy, and meat, meeting consumer demand for quality. Major players such as Thermo Fisher Scientific supply diagnostic solutions for hospital settings, particularly in urban markets of North America and the Asia Pacific.

Diagnostic laboratories are experiencing rapid growth due to the increasing outsourcing of pathogen identification services by hospitals and clinics. These facilities leverage advanced technologies such as NGS and mass spectrometry to offer precise diagnostic results, supporting treatment decisions. Companies such as bioMérieux SA provide solutions for diagnostic laboratories, with rising demand in the Asia Pacific and Europe, where healthcare infrastructure is expanding rapidly.

Regional Insights

North America Pathogen Identification and Treatment Market Trends

North America is projected to hold a 41% share of the global pathogen identification and treatment market. The dominance is primarily attributed to the region’s highly advanced healthcare infrastructure, which enables early adoption of cutting-edge diagnostic technologies and therapeutic solutions. The United States, in particular, plays a pivotal role, driven by significant investments in research and development, the presence of leading biotechnology and pharmaceutical companies, and strong government funding for infectious disease management and healthcare innovation.

The high prevalence of chronic and infectious diseases, coupled with the growing demand for rapid and accurate diagnostic methods, further boosts market growth in the region. Advanced laboratories, integrated healthcare networks, and favorable reimbursement policies support the widespread use of sophisticated pathogen detection platforms, such as molecular diagnostics, next-generation sequencing, and mass spectrometry. For instance, the rapid deployment of COVID-19 testing technologies in the U.S. highlighted the region’s ability to scale up and integrate diagnostics swiftly into the healthcare system. Additionally, increasing collaborations between academic institutions, private firms, and government agencies continue to accelerate the development of novel treatment solutions, reinforcing North America’s leadership position in this market.

Europe Pathogen Identification and Treatment Market Trends

Europe accounts for a substantial share of the pathogen identification and treatment market, with Germany, France, and the U.K. standing out as the primary contributors. Germany’s growth is strongly supported by robust healthcare policies, high R&D expenditure, and a strong focus on infectious disease research. Leading companies such as Merck KGaA are actively investing in molecular diagnostics and advanced pathogen detection platforms, reinforcing the country’s role as a key innovation hub.

The U.K. benefits from the extensive infrastructure of the National Health Service (NHS), which plays a critical role in facilitating the adoption of rapid diagnostic technologies to tackle public health challenges such as antimicrobial resistance (AMR). This focus has accelerated the integration of innovative diagnostic tools in hospitals and clinics. France, on the other hand, is leveraging government-led initiatives for pandemic preparedness and outbreak management, which have created strong demand for efficient diagnostic and treatment solutions. Across Europe, the region’s growing emphasis on precision medicine and the increasing adoption of next-generation sequencing (NGS) in academic and clinical research institutes are shaping market expansion. Moreover, the European Centre for Disease Prevention and Control (ECDC) supports widespread pathogen surveillance and monitoring programs, further driving innovation and adoption across the region.

Asia Pacific Pathogen Identification and Treatment Market Trends

Asia Pacific is emerging as the fastest-growing region in the pathogen identification and treatment market, driven by rising healthcare expenditure, expanding infrastructure, and a growing burden of infectious diseases. Countries such as China and India are at the forefront of this growth due to their large populations, rapid urbanization, and increasing prevalence of conditions such as tuberculosis, influenza, and hospital-acquired infections. Governments across the region are making substantial investments in healthcare modernization, strengthening laboratory networks, and adopting advanced diagnostic technologies to improve patient outcomes.

China, for instance, has implemented large-scale programs to enhance infectious disease surveillance and invest in molecular diagnostic platforms, while India is channeling resources into public health initiatives and pandemic preparedness. The growing presence of local biotechnology firms, coupled with collaborations with global players, is also fostering innovation and accessibility in diagnostic solutions. The rising adoption of next-generation sequencing (NGS) and point-of-care testing in academic institutes, hospitals, and diagnostic laboratories is reshaping the landscape. Increased awareness of antimicrobial resistance (AMR) and the need for rapid pathogen detection are further accelerating technology uptake. As a result, the Asia Pacific offers substantial opportunities for companies aiming to expand their global footprint in this sector.

Competitive Landscape

The global pathogen identification and treatment market is highly competitive and fragmented, with a mix of multinational leaders and specialized regional players. In North America and Europe, companies such as Thermo Fisher Scientific, Roche Diagnostics, and Abbott Laboratories dominate the sector through extensive product portfolios, global distribution networks, and sustained investment in R&D. In the Asia Pacific, regional specialists such as bioMérieux SA and emerging diagnostics firms are leveraging localized offerings and rising healthcare investments to strengthen their market presence. Competition is increasingly driven by innovation in technologies such as AI-integrated next-generation sequencing (NGS), advanced PCR-based assays, and portable point-of-care (POC) devices that deliver rapid results across bacterial, viral, and fungal pathogens.

Key Developments:

- In December 2023, Thermo Fisher Scientific launched the KingFisher Apex Dx automated nucleic acid purification instrument and MagMAX Dx Viral/Pathogen NA Isolation Kit, both IVD/IVD-R approved, to streamline respiratory pathogen diagnostics.

- In September 2024, Roche Diagnostics introduced TAGS (Temperature-Activated Generation of Signal) technology, enabling multiplex detection of 12–15 respiratory viruses.

Companies Covered in Pathogen Identification and Treatment Market

- Thermo Fisher Scientific

- Roche Diagnostics

- Abbott Laboratories

- bioMérieux SA

- Danaher Corporation

- Others

Frequently Asked Questions

The Global pathogen identification and treatment market is projected to reach US$5.3 Bn in 2025.

The rising prevalence of infectious diseases and antimicrobial resistance, coupled with advancements in diagnostic technologies, are the key market drivers.

The pathogen identification and treatment market is poised to witness a CAGR of 8.2% from 2025 to 2032.

The growing adoption of point-of-care diagnostics in decentralized healthcare settings is a key market opportunity.

Thermo Fisher Scientific, Roche Diagnostics, Abbott Laboratories, bioMérieux SA, and Danaher Corporation are key market players.