- Pharmaceuticals

- Global Tarsometatarsal Arthrodesis Treatment Market

Global Tarsometatarsal Arthrodesis Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Tarsometatarsal Arthrodesis Treatment Market by Product Type (Plating Systems, Crossing Screws, K-wires), by Material (Titanium, Stainless Steel), by End-user (Hospitals, Ambulatory Surgical Centers, Orthopedic Outpatient Clinics), by Regional Analysis, 2026-2033

Tarsometatarsal Arthrodesis Treatment Market Size and Trends Analysis

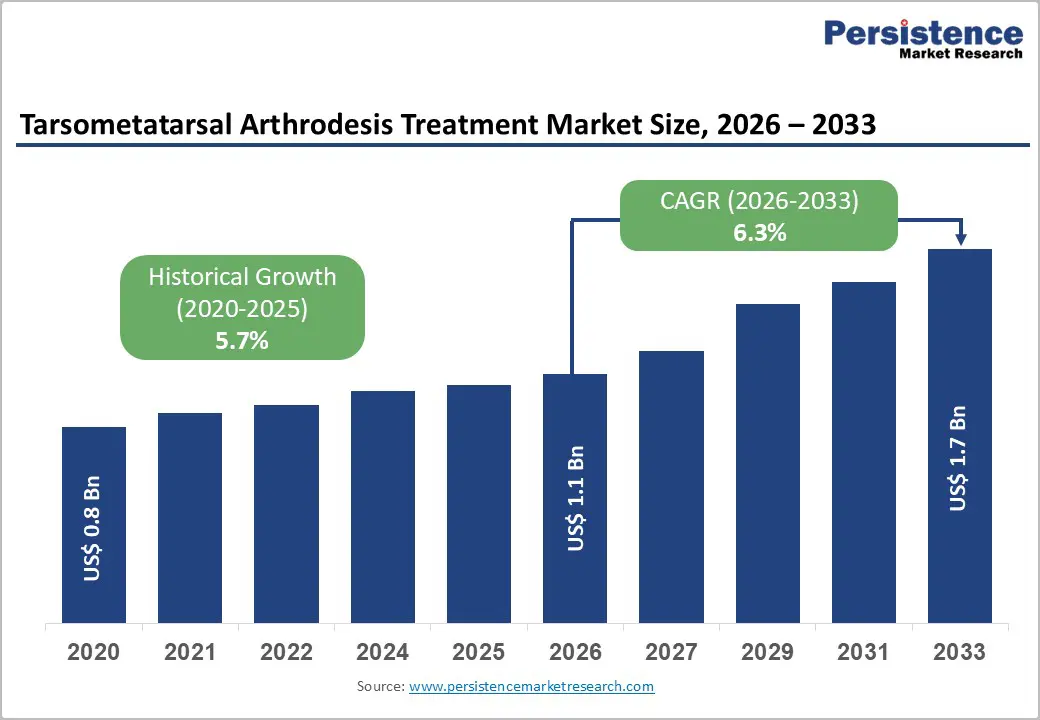

The global tarsometatarsal arthrodesis treatment market size is expected to be valued at US$ 1.1 billion in 2026 and projected to reach US$ 1.7 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

Tarsometatarsal degeration can occur from idiopathic, post-traumatic or inflammatory arthritis leading to severe pain. For the treatment of arthritis of variable extent with or without deformity arthrodesis of the tarsometatarsal joint is performed. Thus, the rising prevalence of arthritis is the major factor that is expected to drive the growth of the tarsometatarsal arthrodesis treatment market.

In addition to this, manufacturers have been constantly working on developing products that can reduce the time taken in pain management and encourages an earlier return to full activity will also help the tarsometatarsal arthrodesis treatment market to grow at a significant rate.

Key Industry Highlights

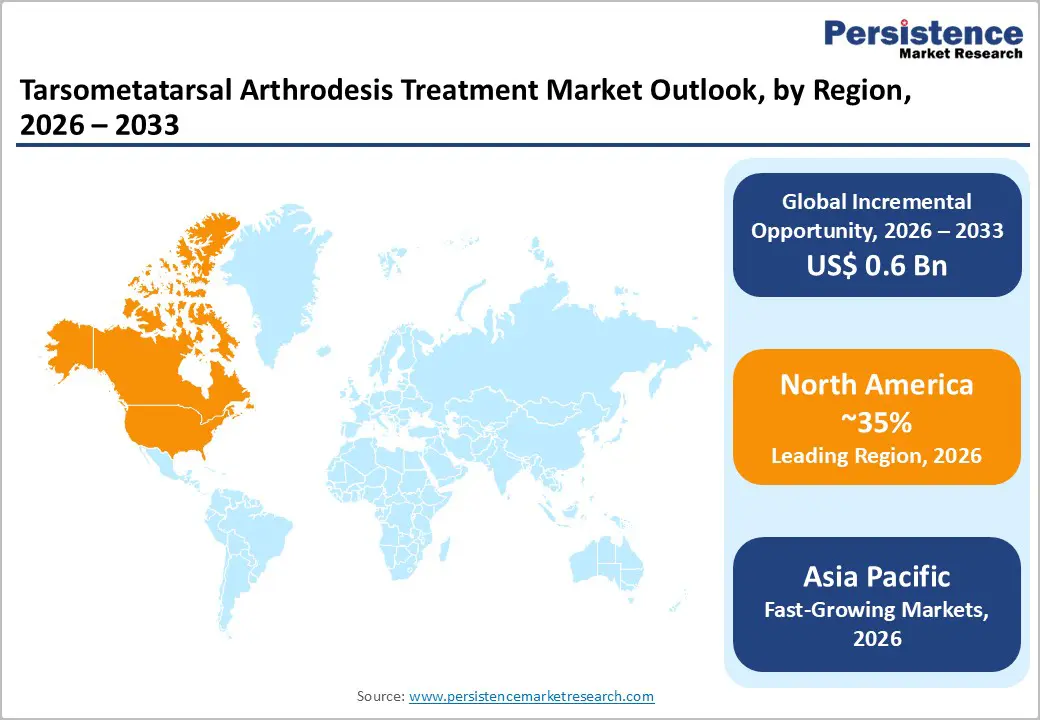

- Leading Region: North America leads due to high procedure volumes, advanced orthopedic infrastructure, strong reimbursement, and widespread surgeon expertise.

- Fastest Growing Region: North America leads due to high procedure volumes, advanced orthopedic infrastructure, strong reimbursement, and widespread surgeon expertise.

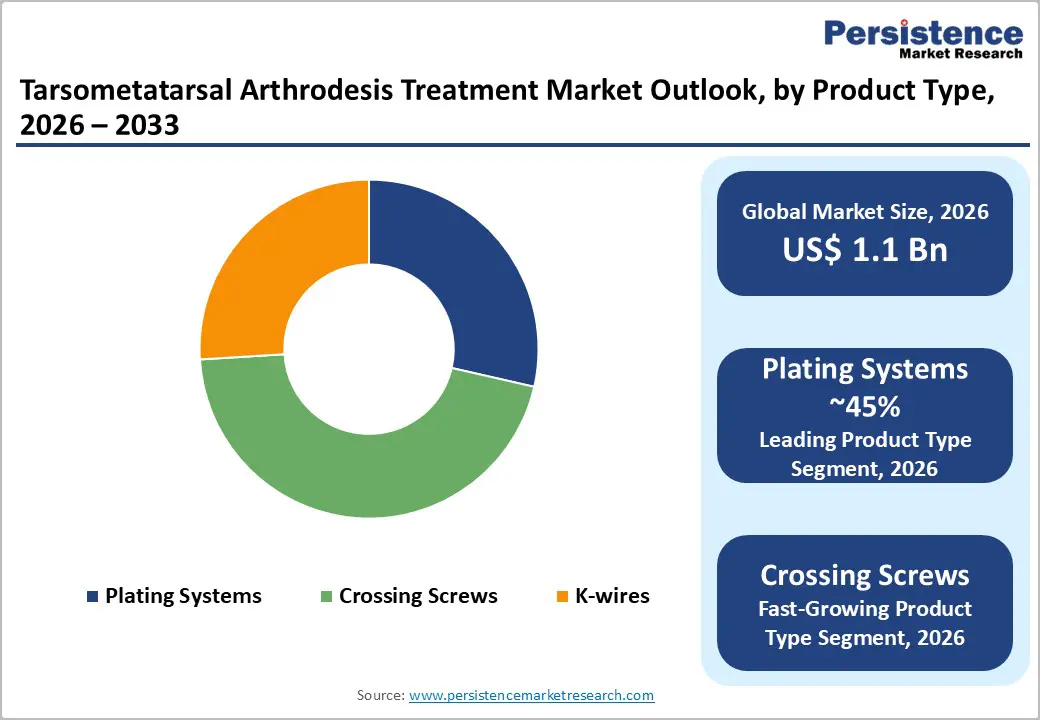

- Dominant Segment: Plating systems dominate owing to superior fixation stability, suitability for complex midfoot deformities, and high surgeon preference.

- Fastest Growing Segment: Crossing screws grow fastest, supported by minimally invasive techniques, reduced recovery time, and increasing use in outpatient procedures.

| Global Market Attributes | Key Insights |

|---|---|

| Tarsometatarsal Arthrodesis Treatment Market Size (2026E) | US$ 1.1 Bn |

| Market Value Forecast (2033F) | US$ 1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.7% |

Market Dynamics

Driver – Increasing recognition and surgical management of Lisfranc injuries

The growing recognition and surgical management of Lisfranc injuries is a key driver supporting the expansion of the tarsometatarsal arthrodesis treatment market. Improved diagnostic capabilities, including advanced imaging techniques such as MRI and weight-bearing CT scans, have enabled earlier and more accurate identification of midfoot instability and ligamentous injuries. As awareness among orthopedic surgeons and sports medicine specialists increases, there is a greater tendency to opt for definitive surgical correction rather than prolonged conservative treatment. Arthrodesis is increasingly preferred in severe or chronic Lisfranc injuries due to its ability to restore stability, reduce pain, and prevent long-term complications such as post-traumatic arthritis. Rising sports participation, road traffic accidents, and occupational injuries further contribute to the growing pool of patients requiring surgical intervention.

Advancements in foot and ankle implant design and minimally invasive surgical techniques are also accelerating market growth. Modern fixation systems, including low-profile plates, anatomically contoured implants, and advanced crossing screw configurations, offer improved biomechanical stability and fusion rates. Minimally invasive approaches reduce soft tissue disruption, postoperative pain, and recovery time, making arthrodesis procedures more acceptable to both patients and surgeons. These innovations have expanded the use of arthrodesis across broader patient populations, including elderly individuals and those with comorbidities, while supporting adoption in outpatient and ambulatory surgical settings.

Restraints- High Costs, Surgical Risks, and Limited Access Restraining Market Growth

The tarsometatarsal arthrodesis treatment market faces several restraints that can limit wider adoption across regions. One significant challenge is the high overall cost of surgical intervention, which includes advanced fixation implants, operating room infrastructure, skilled orthopedic surgeons, and extended postoperative rehabilitation. In price-sensitive and developing markets, limited insurance coverage and reliance on out-of-pocket payments often discourage patients from choosing surgical correction, particularly when symptoms are manageable through conservative treatment. Delayed or missed diagnosis of midfoot disorders further reduces the eligible patient pool for timely arthrodesis procedures.

Postoperative risks also act as a restraint on market growth. Complications such as nonunion, hardware irritation, infection, prolonged swelling, and changes in gait mechanics can affect clinical outcomes and patient satisfaction. Recovery periods may be lengthy, limiting patient willingness to undergo surgery, especially among elderly individuals or those with comorbidities. In addition, variability in surgeon expertise and limited availability of specialized foot and ankle surgeons in certain regions restrict procedural volumes and slow broader market penetration.

Opportunities- Growth driven by outpatient ambulatory surgery, titanium implants, plating systems, and crossing screws.

The expansion of plating systems and crossing screws in ambulatory surgical settings presents a strong growth opportunity for the tarsometatarsal arthrodesis treatment market. Advances in implant engineering have resulted in low-profile, anatomically contoured plates and high-strength screw systems that provide reliable fixation while minimizing soft tissue disruption. These improvements support shorter operative times and faster postoperative recovery, making arthrodesis procedures increasingly suitable for ambulatory surgery centers. As healthcare systems focus on cost containment and efficiency, surgeons are more inclined to perform midfoot fusion procedures in outpatient environments, driving demand for fixation solutions optimized for same-day discharge and streamlined workflows.

The rising adoption of titanium implants and the growing preference for outpatient end-user settings further strengthen market opportunities. Titanium-based implants offer superior biocompatibility, corrosion resistance, and strength-to-weight ratios, leading to improved fusion outcomes and reduced implant-related complications. Their compatibility with advanced imaging modalities also enhances postoperative assessment. Simultaneously, the shift toward outpatient care is supported by improved anesthesia techniques, enhanced recovery protocols, and patient preference for shorter hospital stays. Together, these trends are encouraging manufacturers to focus on durable, lightweight implants and outpatient-focused product designs, supporting sustained market expansion.

Category-wise Analysis

By Product Type Analysis

Plating systems are expected to retain a leading position within the product type segment, accounting for an estimated 45% share by 2026. Dorsal and medial plating techniques are widely favored for Lisfranc arthrodesis due to their ability to deliver strong, rigid fixation and maintain midfoot alignment under multidirectional loading. Clinical evidence from randomized studies highlights favorable functional outcomes, with AOFAS midfoot scores typically ranging between 80 and 92 and loss of reduction reported in fewer than 5% of cases. Unlike K-wires, which are temporary and require later removal, plating systems support earlier weight bearing and long-term structural stability. Plates also offer better resistance to rotational and shear forces compared to standalone screws. Guidance from orthopedic bodies such as the AO Foundation supports plating for complex or unstable injuries. Advanced systems from manufacturers including DePuy Synthes and Paragon 28 incorporate locking options and variable-angle screws, improving contouring accuracy and fusion reliability.

By End-User Analysis

Hospitals are projected to dominate the end-user segment of the tarsometatarsal arthrodesis treatment market, driven by their central role in managing complex Lisfranc injuries. High-energy trauma cases, often resulting from road accidents or falls, are primarily treated in hospital settings where advanced imaging, specialized foot and ankle teams, and comprehensive surgical facilities are available. Hospitals frequently manage cases requiring rigid plating or screw fixation, with published outcomes showing postoperative AOFAS scores around 80 following arthrodesis. These centers also support staged treatment approaches, where temporary K-wire stabilization may precede definitive fusion. In addition, hospitals are better equipped to handle revision surgeries, patients with multiple injuries, and those requiring prolonged monitoring. While ambulatory surgical centers are gradually increasing their share for select, less complex procedures, hospitals continue to lead in procedural volume due to their ability to manage severe injuries, complications, and multidisciplinary care requirements.

Region-wise Insights

North America Tarsometatarsal Arthrodesis Treatment Market Trends

North America holds the largest share of the tarsometatarsal arthrodesis treatment market, supported by a high prevalence of arthritis, foot deformities, and advanced healthcare infrastructure. The U.S. and Canada lead in procedure volumes due to well established orthopedic care systems, widespread availability of specialized surgical centers, and strong reimbursement frameworks encouraging adoption of arthrodesis procedures. Technological innovations such as improved implant designs, bioabsorbable materials, and minimally invasive surgical techniques are enhancing patient outcomes and driving clinician preference for advanced fixation systems.

Additionally, rising awareness of foot and ankle disorders among patients and healthcare providers is increasing demand for corrective arthrodesis surgery. High healthcare expenditure and ongoing R&D investments by major medical device manufacturers further reinforce North America’s dominance. Hospitals remain primary end users due to their capacity for complex surgeries, while ambulatory surgical centers are gaining traction for select procedures. Overall, the region’s growth reflects robust demand, favorable policy support, and continuous innovation.

Asia and Pacific Tarsometatarsal Arthrodesis Treatment Market Trends

The Asia Pacific region is projected to exhibit the fastest growth in the Tarsometatarsal Arthrodesis Treatment market, driven by rapid healthcare infrastructure expansion, increasing awareness of orthopedic surgical solutions, and rising prevalence of lifestyle related foot conditions. Countries such as China, India, and Japan are investing heavily in modern medical facilities and training for specialized foot and ankle surgeons, broadening access to advanced arthrodesis procedures. Improving economic conditions and growing disposable incomes are enabling more patients to seek surgical intervention for midfoot deformities and degenerative disorders. Government initiatives focused on healthcare development, combined with expanding private hospital networks, are further stimulating market growth.

Additionally, increasing adoption of minimally invasive and patient specific implant technologies in the region is enhancing procedural success rates and postoperative recovery, encouraging broader clinician acceptance. As healthcare accessibility improves, outpatient surgical centers are also contributing to market expansion alongside traditional hospital settings, making Asia Pacific a key emerging market.

Market Competitive Landscape

The global Tarsometatarsal Arthrodesis Treatment market features a competitive landscape dominated by established orthopedic device manufacturers and specialized players focusing on innovation, product portfolios, and strategic expansion. Key competitors include Stryker Corporation, Zimmer Biomet Holdings, Inc., DePuy Synthes (Johnson & Johnson), Smith & Nephew plc, and Arthrex, Inc., each offering a range of implants and fixation solutions tailored to arthrodesis and midfoot fusion procedures. These companies invest significantly in research and development to introduce advanced plating systems, crossing screws, and minimally invasive technologies that improve surgical outcomes and recovery. Strategic collaborations, acquisitions, and regulatory approvals are common tactics to enhance market reach and technological capabilities. Mid-sized and emerging firms such as Acumed LLC, Paragon 28, Inc., Integra LifeSciences, and Orthofix Medical Inc. also contribute to competitive dynamics by addressing niche clinical needs and expanding into new geographic regions.

Key Industry Developments:

- In March 2022, CoLink Vallux™ Active Bunion was introduced as a minimally invasive, joint-preserving technique for correcting moderate to severe bunions, enabling multi-dimensional alignment correction without restricting joint space or fusing the midfoot joint.

Companies Covered in Global Tarsometatarsal Arthrodesis Treatment Market

- DePuySynthes

- Nextremity Solutions Inc.

- Medline Industries Inc.

- Stryker GmbH

- Biomet Trauma

- Wright Medical Technology Inc.

- Integra Lifesciences Corporation

- Acumed LLC

- Paragon 28 Inc.

- Orthofix Medical Inc.

- Novastep Inc.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 1.1 Bn in 2026.

Rising prevalence of midfoot arthritis, trauma cases, hallux valgus complications, and increasing adoption of advanced fixation techniques.

The global market is poised to witness a CAGR of 6.3% between 2026 and 2033.

Growth opportunities include minimally invasive fixation systems, outpatient surgical expansion, emerging markets adoption, and development of improved fusion implants.

Key companies include DePuySynthes, Nextremity Solutions Inc., Medline Industries Inc., Stryker GmbH, and Biomet Trauma.