- Medical Devices

- Surgical Trocars Market

Surgical Trocars Market Size, Share, and Growth Forecast 2026 - 2033

Surgical Trocars Market by Product Type (Disposable Trocars, Reusable Trocars), by Tip Type (Bladeless Trocars, Optical Trocars, Blunt Trocars, Bladed Trocars), by Application (General Surgery, Gynecological Surgery, Urology, Bariatric & GI, Others), End-User (Hospitals, Ambulatory Surgical Centers, Clinics, Others), and Regional Analysis for 2026 - 2033

Surgical Trocars Market Share and Trends Analysis

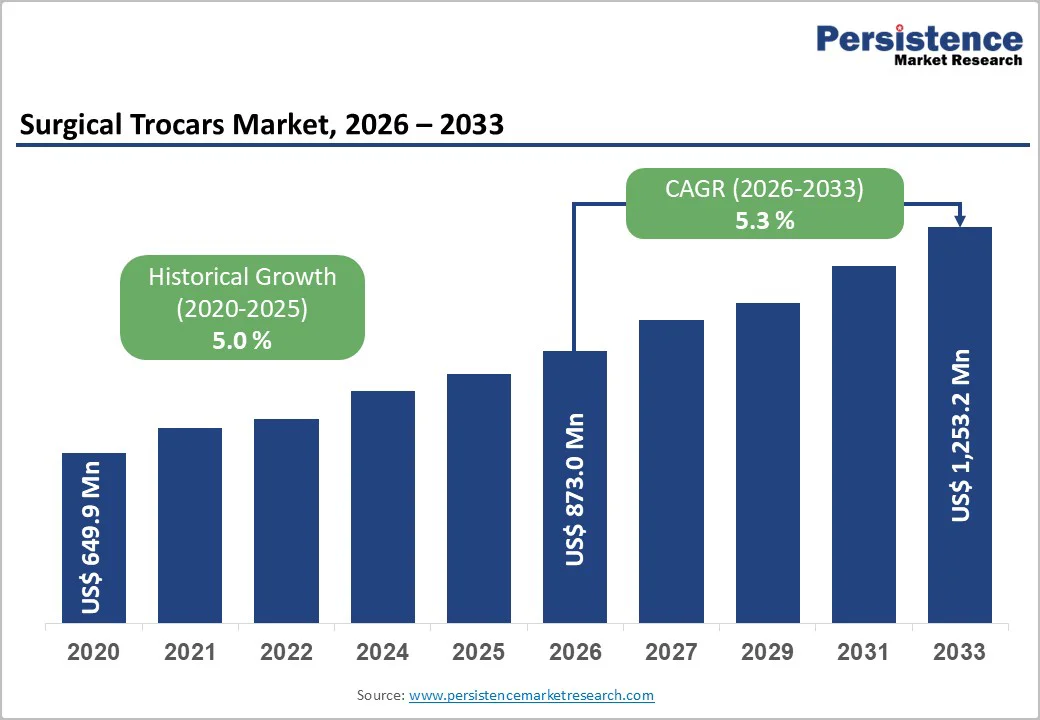

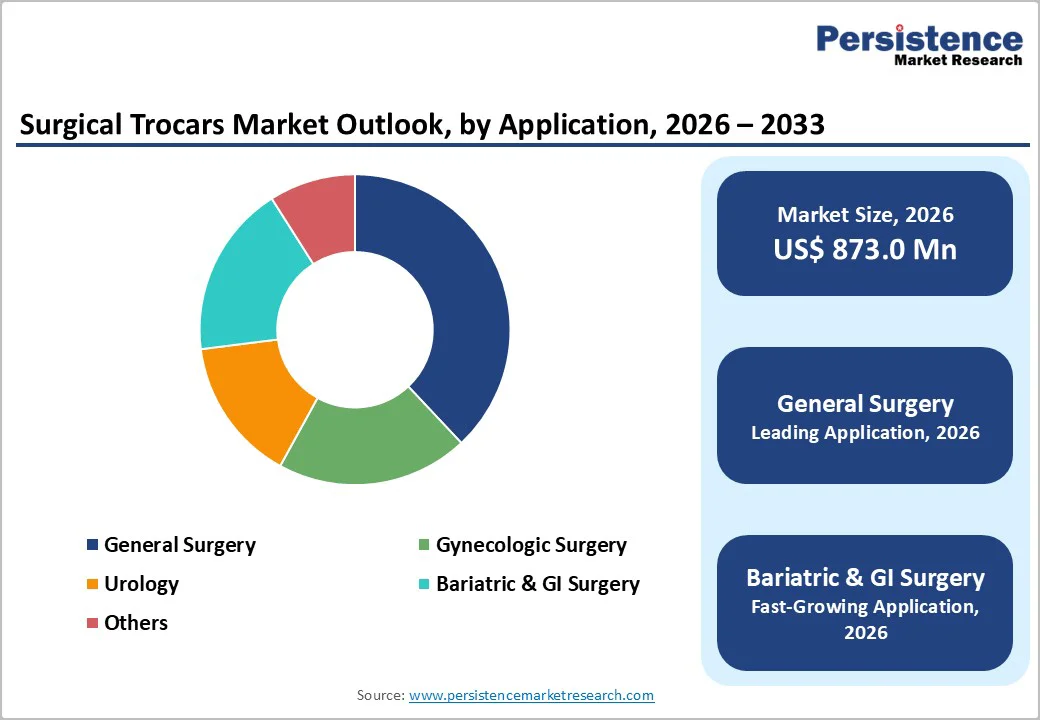

The global surgical trocars market size is likely to be valued at US$873.0 million in 2026, and is projected to reach US$1,253.2 million by 2033, growing at a CAGR of 5.3% during the forecast period 2026-2033. Rising surgical volumes continue to drive sustained demand for trocars, devices used to create access ports in minimally invasive surgeries.

Increasing adoption of minimally invasive surgical procedures across general, gynecological, and bariatric surgery further strengthens market expansion. Regulatory emphasis on sterility and patient safety, particularly through frameworks established by the U.S. Food and Drug Administration (FDA) and European Union (EU) Medical Device Regulation (MDR), encourages the use of advanced and disposable trocar systems. The growing penetration of outpatient surgical centers also accelerates adoption, driven by workflow efficiency requirements.

Key Industry Highlights

- Dominant Product Type: Disposable trocars are likely to dominate in 2026 with around 63% share, driven by a mounting need for effective sterility solutions.

- Leading Tip Type: Bladeless trocars lead in 2026 with approximately 35% revenue share, preferred for their safety and atraumatic insertion.

- Fastest-growing Tip Type: Optical trocars are projected to grow the fastest through 2033, driven by rising demand for enhanced visualization during laparoscopic entry.

- Dominant Application: The general surgery segment is expected to lead in 2026 with a revenue share of about 38%, as these surgeries command the highest procedure volume globally.

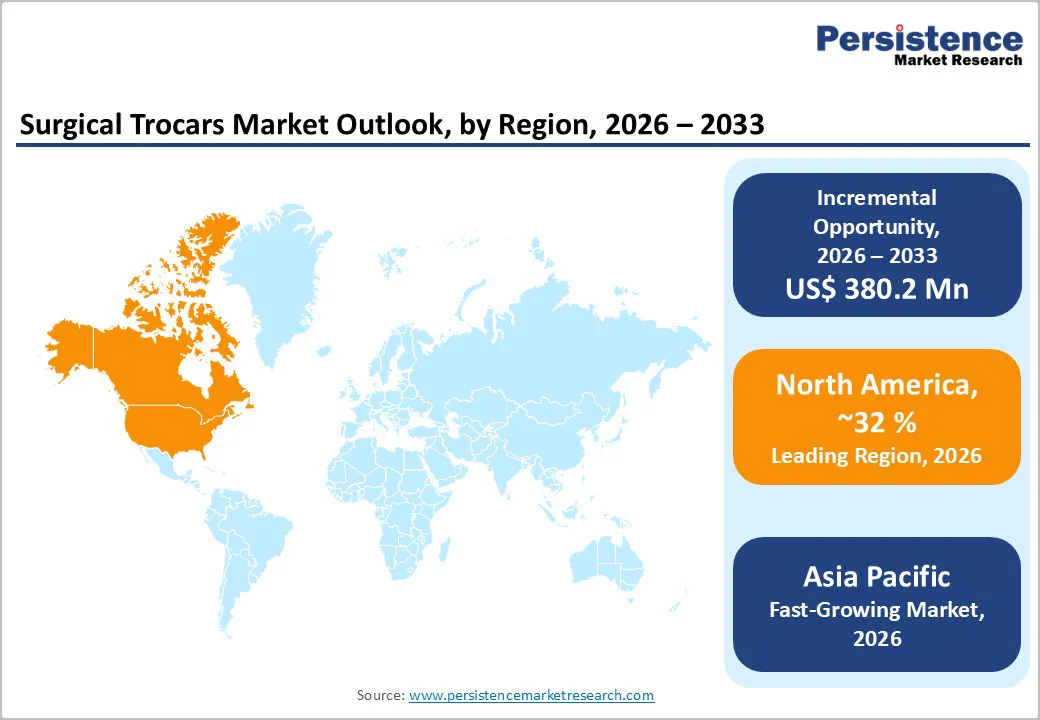

- Leading Region: North America is expected to hold the largest estimated share of 32% in 2026, while the Asia Pacific is likely to be the fastest-growing regional market from 2026 to 2033.

| Key Insights | Details |

|---|---|

|

Surgical Trocars Market Size (2026E) |

US$ 873.0 Mn |

|

Market Value Forecast (2033F) |

US$ 1,253.2 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.0 % |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3 % |

Market Factors - Growth, Barriers and Opportunity Analysis

Increasing Burden of Global Surgical Procedures

The growing prevalence of chronic diseases, obesity, and age-related conditions is significantly increasing the need for surgical interventions worldwide. As global procedure volumes rise, hospitals and ambulatory surgical centers are increasingly relying on laparoscopic techniques, which require surgical trocars for safe and efficient access to body cavities. This reinforces trocars as critical instruments in minimally invasive surgery, particularly in high-volume general, bariatric, and gynecological procedures.

Advancements in trocar technology, such as bladeless designs, optical visualization, and integrated sealing systems, are also improving procedural safety and reducing access-related complications, driving broader adoption. Emerging healthcare markets in Asia Pacific and Latin America are also expanding surgical infrastructure and laparoscopic capacity, further boosting demand. Government-led modernization programs and rising investments in minimally invasive surgical technologies create additional pathways for trocar manufacturers to penetrate underdeveloped regions.

High Cost Burden and Growing Preference for Minimally Invasive Alternatives

The widespread adoption of surgical trocars, particularly advanced disposable systems, remains constrained by several interconnected factors. High initial device costs combined with ongoing procurement expenses create significant financial barriers for healthcare facilities in lower-income regions. These institutions struggle to justify repeated investments in premium trocar technology when budgets remain limited. Reusable trocar systems present an alternative, yet they demand rigorous reprocessing protocols and dedicated sterilization infrastructure, which multiply operational expenses and prove impractical for facilities lacking robust support systems. Training requirements add another layer of complexity, as surgical teams need specialized preparation to use these systems safely and effectively.

The market is simultaneously witnessing a shift toward innovative alternatives that address these persistent barriers. Single-incision laparoscopic platforms, needle-based access devices, and multifunctional hybrid trocars now offer healthcare providers more flexible options for procedural access. These emerging solutions deliver tangible clinical and economic advantages by reducing surgical complexity, lowering complication rates, and maintaining reliable access for specific surgical applications while requiring substantially lower capital investment. This transition toward cost-effective alternatives fundamentally reshapes the competitive landscape for traditional trocar manufacturers, forcing them to reconsider positioning and pricing strategies across resource-constrained markets.

Technological Advancements and Expansion in High-Growth Emerging Markets

The surgical trocars market growth is experiencing substantial momentum driven by technological breakthroughs in minimally invasive surgical systems. Bladeless trocars, optical trocars with integrated visualization capabilities, advanced sealing mechanisms, and enhanced imaging features represent the current generation of device innovations. These improvements deliver measurable clinical benefits by strengthening procedural safety, minimizing access-related complications, and optimizing surgeon workflow efficiency. As healthcare facilities worldwide expand their laparoscopic infrastructure investments, these next-generation trocar technologies are well-positioned to capture expanding market share through 2033. Recent product developments underscore this trajectory. For example, in 2023, Xpan received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for an adaptable trocar system that adjusts its diameter during procedures.

Capacity investments further reinforce positive market dynamics. In January 2025, for instance, Becton, Dickinson and Company (BD) announced expansion of its United States manufacturing operations to increase production capacity for essential medical devices, including surgical consumables such as trocars. Developing economies are also presenting exceptional growth opportunities. Healthcare systems across Asia Pacific, Latin America, and the Middle East & Africa are modernizing their surgical capabilities, experiencing rising procedure volumes, and allocating increased funding toward medical infrastructure. Continuous product innovation, manufacturing capacity enhancement, and accelerating regional demand are converging to establish favorable conditions for global trocar market expansion and enable key participants to chart promising growth trajectories.

Category-wise Analysis

Product Type Insights

Disposable trocars are projected to dominate the market in 2026 with an estimated 63% revenue share, supported by stringent infection control standards and increasing preference for single-use surgical devices in hospitals and ambulatory surgical centers (ASCs). These systems are favored due to their ease of use, reduced reprocessing workload, and lower regulatory compliance risks, making them the preferred choice in advanced healthcare settings across North America, Europe, and select Asia Pacific markets. Rising procedure volumes and greater adoption of minimally invasive surgery further reinforce their leadership position.

Manufacturers are also focusing their energies on developing advanced disposable trocar systems featuring improved sealing technology and low-friction passage, enhancing insufflation stability and instrument handling. For example, Surgsci Medical introduced a line of trocars with high-polymer sealing materials providing dynamic airtightness and smooth instrument passage, reflecting ongoing innovation that strengthens market preference for single-use devices.

As a result, the disposable trocar segment is also expected to record the fastest growth at a CAGR of roughly 5.8% from 2026 to 2033. While reusable trocars continue to serve price-sensitive regions, the global emphasis on efficiency, sterility, and procedural safety ensures that disposable systems remain the primary growth engine, generating significant incremental revenue opportunities for manufacturers.

Tip Type Insights

Bladeless variants are positioned to command approximately 35% of the surgical trocars market revenue share in 2026. Their competitive advantage stems from a superior safety profile, atraumatic tissue entry mechanism, and substantially reduced incidence of entry-site complications. These devices have become the standard of care in general surgery and gynecological procedures, where preserving tissue integrity and maintaining strict procedural safety protocols remain paramount clinical priorities. Healthcare facilities including hospitals and ASCs worldwide continue to favor bladeless trocars because their design principles align directly with established clinical best practices and quality standards.

Optical trocars are likely to represent the market's fastest-growing segment, projected to achieve a 2026-2033 CAGR of approximately 6.2%. This accelerated expansion reflects the growing demand for advanced visualization technology during trocar insertion procedures. Real-time optical guidance substantially diminishes procedural uncertainty and minimizes access-related complications, translating into improved surgical outcomes and reduced patient morbidity. Healthcare facilities with high surgical volumes and those investing in technology-enhanced operating room environments increasingly prioritize optical trocar systems. The convergence of rising minimally invasive procedure adoption, expanding capital budgets at major surgical centers, and clinician preference for enhanced visualization capabilities creates sustained growth opportunities for optical trocar manufacturers throughout the forecast period.

Application Insights

General surgery is projected to remain the largest application segment in 2026 with an estimated 38% market share, driven by consistently high procedure volumes including appendectomies, hernia repairs, and colorectal operations. The broad applicability of trocars across multiple general surgical interventions, combined with the widespread adoption of minimally invasive techniques, reinforces their sustained market leadership. Hospitals performing complex or multi-quadrant procedures rely on multiple trocar insertions per surgery, further supporting stable demand for both disposable and reusable devices.

Bariatric and gastrointestinal (GI) surgeries are expected to grow at the fastest pace, with a CAGR of around 6.5% between 2026 and 2033. Rising global obesity rates and increasing access to procedures such as sleeve gastrectomy and gastric bypass are driving higher trocar utilization per operation. Asia Pacific and Latin America, in particular, are experiencing significant growth due to expanding laparoscopic surgical infrastructure and healthcare modernization. Technological improvements in trocar systems, including bladeless, optical, and multifunctional designs, enhance procedural safety and efficiency, encouraging broader adoption in these high-growth surgical segments.

Regional Insights

North America Surgical Trocars Market Trends

North America is expected to lead in 2026, accounting for an estimated 32% of the surgical trocars market share, driven primarily by the United States. High surgical procedure volumes, widespread adoption of minimally invasive techniques, and the presence of over 6,000 ambulatory surgical centers support strong demand for disposable and reusable trocars. Regulatory frameworks, including the U.S. FDA’s quality and sterility standards, reinforce provider confidence in validated, compliance-ready trocar systems. Hospitals and ASCs increasingly seek devices with integrated safety and visualization features, further boosting market uptake.

A robust medical device innovation ecosystem, well-established distribution networks, and continuous investment in laparoscopic technology upgrades also support market growth in North America. Canada also contributes a steady incremental demand through healthcare modernization initiatives. Mature procurement practices, high hospital penetration, and the expansion of outpatient surgical services will enable North America to maintain its dominant market position and make it a priority for product launches and technology-enhanced trocar systems.

Europe Surgical Trocars Market Trends

Europe is likely to hold an estimated 28% share in 2026 and represents a structurally important market due to widespread adoption of minimally invasive surgical protocols, harmonized EU regulations, and high laparoscopic tool penetration. Germany leads regional revenue, followed by the U.K., France, and Spain. EU MDR implementation has increased compliance requirements, favoring established manufacturers with validated sterilization and quality-management processes. Hospitals are increasingly adopting disposable trocar systems to meet infection control standards, while Central and Eastern European countries benefit from modernization initiatives that accelerate the adoption of laparoscopy.

Steady growth in the surgical trocars market is driven by well-developed surgeon training infrastructure, clinical research partnerships, and public hospital restructuring programs. Disposable trocars continue to see adoption due to operational efficiency, procedural safety, and regulatory alignment. Cost-effectiveness, regulation-ready devices, and growing laparoscopic surgery volumes position Europe as a stable and strategically significant market for 2026 and beyond.

Asia Pacific Surgical Trocars Market Trends

Asia Pacific is projected to be the fastest-growing regional market for surgical trocars, with a CAGR of approximately 6.3% through 2033 and an estimated 20% share in 2026. The market's growth here is fueled by expanding healthcare spending, increasing surgical capacity, and widening adoption of minimally invasive procedures across China, India, and the ASEAN countries. China leads regional demand with large hospital networks and modernization initiatives. India and other ASEAN markets are benefiting from increasing affordability, hospital infrastructure investments, and universal health coverage programs, supporting rising laparoscopic procedure volumes.

China’s National Medical Products Administration (NMPA) has been streamlining device approvals, while cost-sensitive markets have been stoking the demand for competitively priced disposable trocars. Local manufacturing capabilities, expanding trained surgical workforce, and rising obesity and GI procedure prevalence reinforce Asia Pacific as a critical growth corridor. Manufacturers targeting emerging healthcare hubs can leverage procedural expansion and technology adoption for incremental revenue opportunities.

Competitive Landscape

The global surgical trocars market is moderately consolidated, led by established players such as Medtronic, Johnson & Johnson (Ethicon), BD, Karl Storz, Applied Medical, and Stryker, which command a substantial share of revenue through clinically validated products and advanced trocar designs. These leaders focus on disposable, bladeless, and optical trocar systems that enhance procedural efficiency, reduce entry-site complications, and align with hospital and ASC sterility standards. Continuous investments in next-generation trocars, including multi-diameter, low-friction, and advanced sealing technologies, reinforce their dominance in high-volume laparoscopic procedures across hospitals and outpatient surgical centers.

Alongside these major players, regional and emerging manufacturers, particularly in the Asia Pacific and Latin America, are reshaping cost competitiveness and accessibility. These companies emphasize localized production, affordable disposable trocars, and solutions tailored to different surgical protocols. Rising adoption of minimally invasive procedures, expanding laparoscopic infrastructure, and growing outpatient surgical volumes provide opportunities for newer entrants to innovate with multifunctional, technology-enhanced, and ergonomically optimized trocar systems, driving incremental market penetration and long-term growth.

Key Industry Developments

- In October 2025, Bayou Surgical launched its 5mm troCarWash system, an automated laparoscope cleaning solution integrated directly into the trocar that restores visualization in under 0.35 seconds without requiring scope removal during procedures. The technology addresses a critical surgical challenge by eliminating workflow interruptions caused by lens fogging or contamination, supporting 0°, 30°, and 45° viewing angles across general surgery and thoracic procedures.

- In July 2025, Cleveland Clinic performed the world's first transcervical robotic aortic valve replacement (AVR) procedures, enabling four patients aged 60 to 74 years to resume unrestricted activity within one week of discharge with minimal postoperative pain. The technique utilizes a small neck incision to access the aorta and aortic valve without requiring sternotomy or thoracotomy incisions, with an average cross-clamp time of 140 minutes and postoperative discharge occurring between 3 and 6 days, depending on individual circumstances.

- In July 2025, Teleflex completed its acquisition of BIOTRONIK's Vascular Intervention business for approximately US$875 million, integrating a comprehensive portfolio of coronary and peripheral intervention products, including drug-coated balloon catheters, drug-eluting stents, and the Freesolve resorbable metallic scaffold technology.

- The transaction significantly expands Teleflex's global presence in the catheterization laboratory and peripheral intervention markets.

Companies Covered in Surgical Trocars Market

- Medtronic plc

- Johnson & Johnson

- B. Braun Melsungen AG

- CONMED Corporation

- Applied Medical Resources

- Teleflex Incorporated

- Stryker

- Genicon, Inc.

- Purple Surgical

- KARL STORZ SE

- Olympus Corporation

- Grena Ltd

- Victor Medical Instruments

- Shendu Medical

- Lapstar

Frequently Asked Questions

The global surgical trocars market is projected to reach US$ 873.0 million in 2026.

Growing demand for minimally invasive procedures, rising preference for disposable trocars to reduce cross-contamination, and advancements in optical and bladeless trocar designs, improving procedural safety, are driving the market.

The market is poised to witness a CAGR of around 5.3% from 2026 to 2033.

Development of smart/ergonomic access devices, increased robotic and bariatric surgery volumes, and rapid healthcare expansion in the Asia Pacific and Latin America are key market opportunities.

Prominent market companies include Medtronic, Teleflex, Ethicon (Johnson & Johnson), ConMed, B. Braun, Applied Medical, and LaproSurge.