- Medical Devices

- Surgical Sutures Market

Surgical Sutures Market Size, Share, and Growth Forecast, 2025 - 2032

Surgical Sutures Market By Product Type (Absorbable Sutures, Non-Absorbable Sutures), Material (Synthetic Sutures, Natural Sutures), Filament Type (Monofilament, Multifilament Sutures), Application, and Regional Analysis for 2025 - 2032

Surgical Sutures Market Size and Trends Analysis

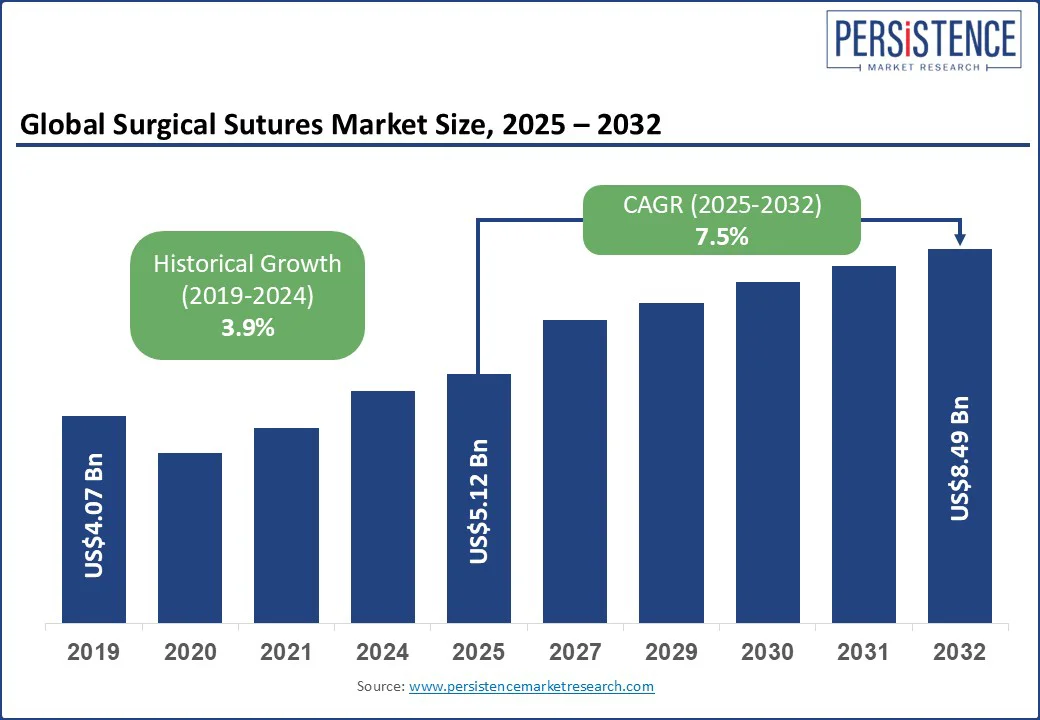

The global surgical sutures market size is likely to be valued at US$5.12 Bn in 2025 and is expected to reach US$8.49 Bn by 2032, growing at a CAGR of 7.5% during the forecast period from 2025 to 2032.

The market growth is driven by the rising volume of surgical interventions worldwide, fueled by an aging population, an increase in chronic diseases, and greater access to healthcare in emerging economies.

The surgical sutures market represents a critical segment of wound closure solutions, widely used across general surgery, cardiovascular, orthopedic, obstetrics, and other medical procedures. Advancements in absorbable sutures, antibacterial coatings, and automated suturing devices are further reshaping adoption trends, while competition from staples and tissue adhesives continues to influence market dynamics.

Key Industry Highlights

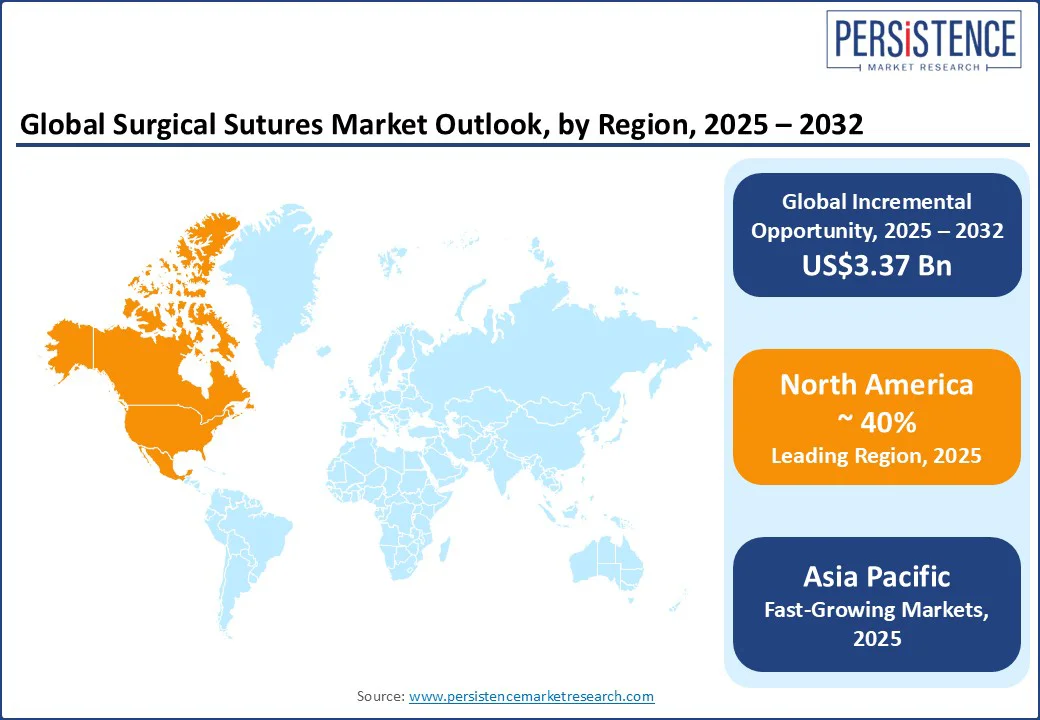

- Leading Region: North America is projected to dominate the market, holding nearly 40% of the market share in 2025, driven by advanced healthcare infrastructure, a high volume of surgical procedures, and strong innovation in wound closure technologies.

- Fastest-growing Region: Asia Pacific is anticipated to be the fastest-growing in 2025, driven by rising surgical volumes in India and China, and increased healthcare investments.

- Investment Plans: Companies are prioritizing biodegradable smart sutures, antimicrobial coatings, and 3D-printed personalized sutures, with hospitals emerging as partners for point-of-care fabrication.

- Dominant Product Type: Absorbable sutures are anticipated to account for approximately 61% of the market share in 2025, favored for internal tissue closure and compatibility with minimally invasive procedures.

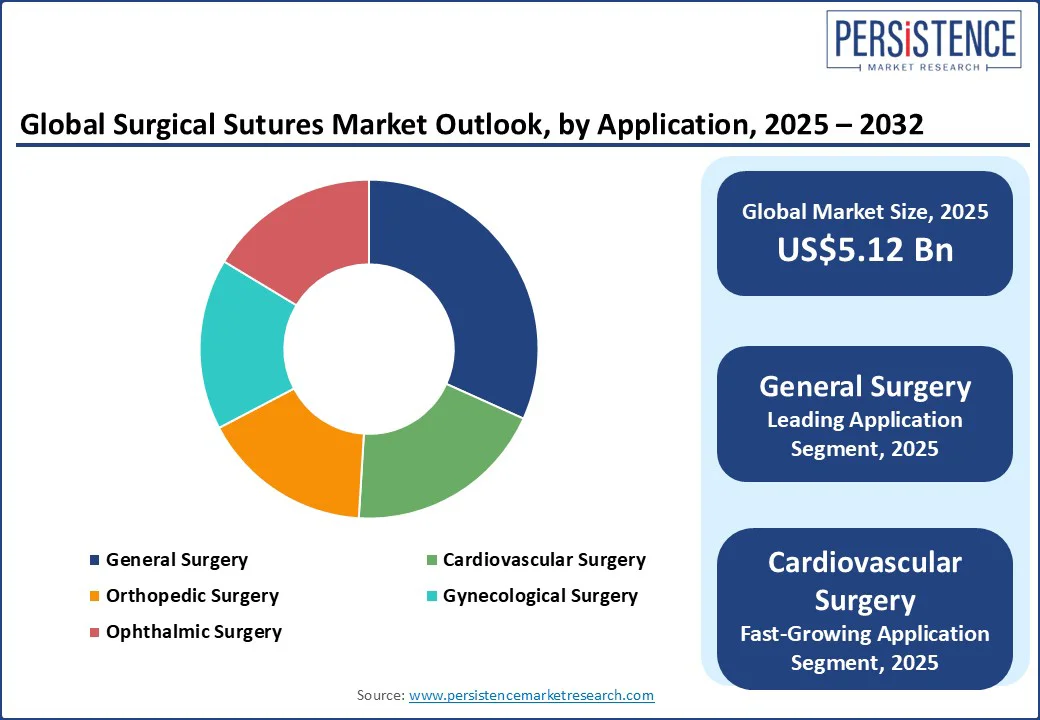

- Leading Application Segment: General surgery is likely to lead with around 32.5% revenue share in 2025, while orthopedic and cardiovascular surgeries represent high-growth opportunities.

|

Global Market Attribute |

Key Insights |

|

Surgical Sutures Market Size (2025E) |

US$5.12 Bn |

|

Market Value Forecast (2032F) |

US$8.49 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.9% |

Market Dynamics

Driver - Robotics-Ready Sutures and Smart Healing Materials Reshape Surgical Workflows

The growing adoption of robot-assisted surgical systems, particularly in microsurgeries and minimally invasive procedures, is creating strong demand for barbed sutures that are optimized for tactile-limited environments. These knotless, self-anchoring sutures reduce operative time and minimize blood loss, making them highly compatible with robotic workflows. Products such as Johnson & Johnson’s STRATAFIX have already demonstrated these benefits in clinical use.

Advances in synthetic absorbable polymers, including poly(3-hydroxybutyrate-co-4-hydroxybutyrate) fibers, are reshaping the absorbable segment. When combined with electrospun architectures and embedded anti-inflammatory drug reservoirs, these materials offer greater elasticity, controlled biodegradation, and localized drug delivery, enabling faster recovery and supporting premium pricing in specialized surgical applications.

Innovative suturing solutions are also emerging in the form of self-electrified biodegradable sutures that generate electric fields through the natural motion of the body. By harnessing the triboelectric effect, these sutures accelerate tissue regeneration and actively suppress bacterial growth without requiring any external power source, representing a breakthrough in wound-healing technology. Parallel research into CT-visible smart sutures and antimicrobial nanofiber coatings is advancing the ability to monitor healing progress and reduce postoperative infections.

Restraint - Advanced Adhesives and Mechanical Fragility Limit Suture Adoption

The rising adoption of tissue adhesives with nanoparticle-enhanced adhesion properties, offering hemostatic and antimicrobial action without preparation. This poses a challenge to the expanding segment of barbed, knotless sutures tailored for robotic closure.

These advanced adhesives can bond tissues rapidly and may function as multifunctional alternatives in certain settings, even replacing sutures in open procedures where sutures were once indispensable. Limitations such as adhesive swelling and toxicity still exist in some formulations. As these biomaterial-based adhesives mature, they pose a direct challenge to suture manufacturers.

Although electrospun nanofiber multifilament constructs offer improved surface area and cell-scaffold mimicry, they are prone to crushing and tensile degradation under mechanical stress. In delicate contexts such as laparoscopic or microsurgery, this raises concerns about crush-induced tensile failure, wound dehiscence, or even suture breakage, especially when handled with forceps.

Empirical studies demonstrate that repeated mechanical loading during tissue grasping can significantly reduce tensile integrity across suture brands. This structural fragility undermines confidence in nanostructured sutures, particularly for high-tension applications such as vascular or orthopedic closures.

Opportunity - 3D Printing and Triboelectric Sutures Unlock Next-Gen Wound Care

The integration of additive manufacturing into surgical sutures is opening new possibilities for personalized wound closure. Using advanced biocompatible inks, manufacturers can now develop 3D-printed sutures infused with growth factors or antimicrobial agents, enabling customization of geometry, porosity, degradation rate, and therapeutic release to match the patient’s specific tissue needs.

This approach is particularly valuable in complex reconstructive and congenital surgeries, where precision and localized healing are critical. Establishing point-of-care 3D printing capabilities within hospitals could significantly reduce lead times, improve surgical outcomes, and strengthen the positioning of suppliers as partners in precision medicine.

Another promising opportunity is the development of self-electrified biodegradable sutures that generate low-intensity electrical stimulation through natural body movement. By leveraging the triboelectric effect, these sutures can accelerate tissue regeneration and inhibit bacterial growth without requiring any external power source.

Early preclinical studies indicate nearly 50% faster wound healing with reduced infection risks, positioning this innovation as a breakthrough in postoperative care. As these sutures progress toward clinical trials, they present strong potential to support value-based healthcare goals, lower readmission rates, and establish a premium niche in the global wound closure market.

Category-wise Analysis

Product Type Insights

Absorbable sutures are anticipated to be the largest product category in the global market, accounting for roughly 61% of the market share in 2025. Absorbable sutures dominate due to their ability to naturally degrade within the body, eliminating the need for removal and improving patient comfort.

This also reduces the risk of post-surgical infections and minimizes follow-up care requirements, making them the preferred choice across a wide range of procedures. The broad adoption of absorbable sutures highlights their clinical efficiency, cost-effectiveness, and alignment with evolving healthcare delivery models.

Absorbable sutures are expected to be the fastest-growing segment over the forecast period, driven by advances in synthetic absorbable sutures, particularly those with antimicrobial coatings such as triclosan or integrated drug-delivery systems. These innovations provide predictable degradation timelines and improved wound healing outcomes, offering strong value to both surgeons and healthcare systems.

Application Insights

General surgery is expected to be the largest application segment, contributing about 32.5% of the revenue share in 2025. This is attributed to the high surgical volume across gastrointestinal, abdominal, and trauma procedures, where sutures remain an essential wound closure method.

The sheer frequency and variety of general surgical interventions sustain consistent demand, making this segment a cornerstone of the market. Hospitals, in particular, account for a significant share of this usage due to their broad procedural scope and higher patient inflow.

Cardiovascular surgery is the fastest-growing application segment. Rising global incidence of cardiovascular diseases and an increase in complex surgical interventions are driving this growth. Unlike general surgeries, cardiovascular procedures require specialized sutures with exceptional tensile strength and durability to withstand high-pressure environments. The demand for premium, non-absorbable, and slow-degrading absorbable sutures in this field underlines the shift toward highly engineered solutions that prioritize both patient safety and long-term performance.

Regional Insights

North America Surgical Sutures Market Trends - Advancing Surgery with Robotic Precision and Absorbable Sutures

North America is projected to dominate the market, accounting for approximately 40% of the market share in 2025. The region benefits from advanced healthcare infrastructure, a high volume of surgical procedures, and strong innovation pipelines in wound closure technologies. The adoption of antimicrobial sutures and knotless fixation systems is particularly strong, reflecting the shift toward reducing surgical site infections and improving patient recovery times.

In the U.S., the demand is reinforced by a rapidly aging population and the growing burden of chronic conditions requiring surgical intervention. Recent FDA approvals for devices such as Anika Therapeutics’ X-Twist knotless system and Smith & Nephew’s HELICOIL anchor demonstrate the emphasis on product innovation and surgeon efficiency. Additionally, the presence of leading medical device manufacturers, coupled with high R&D investments, continues to drive clinical advancements and the early adoption of next-generation suture technologies.

Canada, though smaller in scale, is benefiting from its well-integrated healthcare system, with hospitals increasingly adopting advanced wound management and bioactive sutures to enhance clinical outcomes. National funding initiatives for surgical innovation and infection control have further supported the uptake of advanced suturing materials. The Canadian market is also seeing a rise in interest for sustainability, with hospitals and surgical centers increasingly preferring biodegradable and environmentally friendly supplies to reduce ecological impact.

Asia Pacific Surgical Sutures Market Trends - Rising Surgical Volumes and Expanding Healthcare Infrastructure Investments

Asia Pacific is emerging as the fastest-growing region, with a projected CAGR outpacing other regions through 2032. Growth is supported by rising healthcare expenditure, expanding medical tourism, and the growing availability of minimally invasive procedures. Hospitals in the region are increasingly investing in advanced suture materials, such as antimicrobial-coated and bioabsorbable sutures, to reduce infection risks and comply with international care standards.

China is becoming a hub for innovation, with researchers recently developing biodegradable self-electrified sutures that use electrical stimulation to accelerate wound healing, an early sign of the region’s strong contribution to next-generation wound closure. The government’s support for domestic medtech companies and digital healthcare ecosystems is also accelerating the pace of surgical innovation and adoption.

India is also recording rapid adoption, supported by government healthcare expansion programs and local innovation. Healthium Medtech’s launch of “TRUMA,” a dissolvable suture designed for minimally invasive surgeries, highlights how domestic manufacturers are tailoring products to regional demand while competing globally. Increased access to healthcare in rural areas and training programs for laparoscopic procedures are fueling the demand for affordable, high-quality suture solutions across public and private healthcare sectors.

Europe Surgical Sutures Market Trends - Focus on Infection Control and Rising Demand for Smart Suturing Solutions

Europe is expected to maintain steady growth. The region is characterized by strong quality standards, growing use of bio-absorbable sutures, and consolidation among leading manufacturers to strengthen their product portfolios.

European hospitals are increasingly prioritizing advanced sutures that reduce operating times and improve patient recovery pathways. France has witnessed strategic consolidation, exemplified by the acquisition of Peters Surgical by Advanced Medical Solutions in 2024, which strengthens local capacity and innovation in surgical sutures. The integration is expected to drive synergies in R&D and widen access to premium suturing solutions across the EU.

The U.K. is advancing with the adoption of antimicrobial and biodegradable materials, driven by efforts to minimize hospital-acquired infections and improve surgical throughput within the NHS system. In parallel, regulatory initiatives such as the UKCA marking and post-Brexit medical device framework are encouraging companies to innovate while maintaining compliance.

Germany and the Nordic countries are also leading adopters of robotic-assisted and minimally invasive surgeries, further increasing demand for specialized sutures compatible with these techniques. In addition, increasing focus on sustainability and circular healthcare models is influencing procurement practices, prompting a shift toward eco-friendly suture packaging and manufacturing.

Competitive Landscape

The global surgical sutures market is moderately consolidated, with a few multinational corporations such as Johnson & Johnson (Ethicon), Medtronic, and B. Braun commanding a significant share through their extensive product portfolios and strong distribution networks.

These companies maintain leadership by offering a wide range of absorbable and non-absorbable sutures, barbed technologies, and value-added antimicrobial solutions that cater to both high-volume procedures and specialized surgical needs.

The landscape is also shaped by a growing number of regional and mid-sized players, particularly in Asia Pacific and parts of Europe, who compete on cost efficiency, localized product adaptation, and strategic partnerships with hospitals. While top-tier players focus on high-performance sutures and premium solutions for minimally invasive and robotic surgeries, local manufacturers are increasingly filling gaps in affordability and accessibility, especially in emerging healthcare markets.

Key Industry Developments

- In June 2025, Johnson & Johnson introduced a new antimicrobial suture series designed for high-risk surgeries and immunocompromised patients, reinforcing their infection control portfolio.

- In April 2025, Dutch Mellon Medical released "Switch," a next-gen automated suturing device optimized for single-handed use in laparoscopic and robotic-assisted surgeries, improving speed and reducing surgeon fatigue.

Companies Covered in Surgical Sutures Market

- Johnson & Johnson (Ethicon, Inc.)

- Medtronic plc

- B. Braun Melsungen AG

- Smith & Nephew plc

- Corza Medical, Inc.

- DemeTECH Corporation

- Sutures India Pvt. Ltd. (Healthium Medtech Ltd.)

- Teleflex Incorporated

- Peters Surgical

- Stryker Corporation

- Boston Scientific Corporation

- Mellon Medical B.V.

- Surgical Specialties Corporation (SSCOR)

- Internacional Farmacéutica S.A. de C.V. (Atramat)

- EndoEvolution, LLC

- Assut Medical Sàrl

- Resorba Medical GmbH (Advanced Medical Solutions Group plc)

- Riverpoint Medical

- Meta Biomed Co., Ltd.

- AD Surgical

Frequently Asked Questions

The surgical sutures market is estimated to reach US$5.12 Bn in 2025.

The market is expected to grow to US$8.49 Bn by 2032.

Key trends include the adoption of robotics-friendly barbed sutures, the development of self-electrified biodegradable sutures for accelerated healing, 3D-printed personalized sutures with drug-delivery capabilities, and the integration of antimicrobial nanofiber coatings for infection control.

By product type, the absorbable sutures segment is expected to dominate the market, holding nearly 61% share due to their widespread use in internal soft tissue closure and reduced need for suture removal.

The surgical sutures market is expected to grow at a CAGR of 7.5% between 2025 and 2032.

Key Players include Johnson & Johnson (Ethicon), Medtronic, B. Braun Melsungen AG, Smith & Nephew, Boston Scientific, and Teleflex Incorporated.