- Medical Devices

- Surgical Robot Procedures Market

Surgical Robot Procedures Market Size, Share, and Growth Forecast, 2026 - 2033

Surgical Robot Procedures Market by Specialty (Urology, Gynecology, General Surgery, Cardiothoracic/ Cardiovascular, Orthopedics/Spine, Pediatrics, Others), Technology (Multi-Arm Surgeon-Console Platforms, Modular/Portable Multi-Arm Systems, Single-Port/Single-Arm Platforms, AI-Enabled Navigation Modules, Others), Business Model (Direct Capital Purchase, Lease/Rental, Robot-as-a-Service (RaaS), Service & Maintenance Contracts, Others), and Regional Analysis for 2026 - 2033

Surgical Robot Procedures Market Share and Trends Analysis

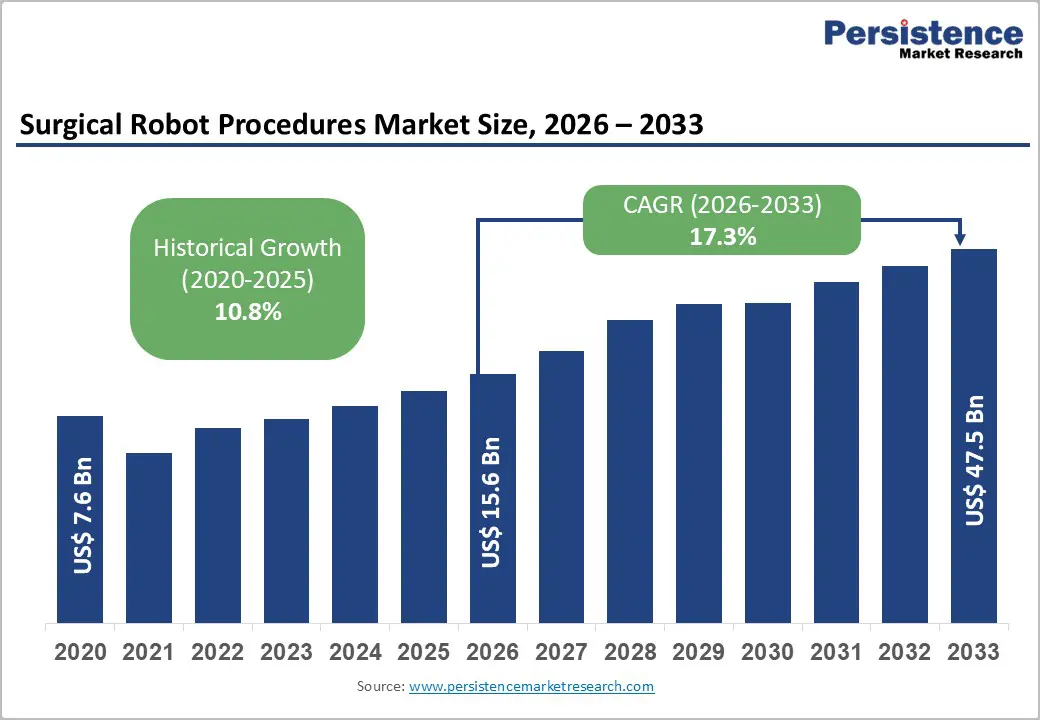

The global surgical robot procedures market size is likely to be valued at US$ 15.6 billion in 2026, and is projected to reach US$ 47.5 billion by 2033, growing at a CAGR of 17.3% during the forecast period 2026 - 2033.

The market is entering an acceleration phase as minimally invasive robotic techniques expand across high-volume specialties and revenue models shift toward recurring streams. Growth is driven by the scale-up of robot-assisted laparoscopic procedures in urology, gynecology, and general surgery, as well as by rising per-procedure revenue from instruments and software. The market structure is increasingly favoring recurring monetization, in which consumables, service contracts, and digital modules account for a larger share of total revenue than initial system placements. Procedure volumes are expanding as both installed-base growth and per-case consumable utilization increase in parallel. Regulatory clearances from the U.S. Food and Drug Administration (FDA) are broadening the range of approved indications, which is supporting adoption in both tertiary hospitals and community settings. Artificial intelligence (AI)-enabled navigation systems and Robot-as-a-Service (RaaS) models are reducing operating room staffing requirements and lowering upfront capital exposure, thereby accelerating uptake in ambulatory surgery centers and middle-income healthcare markets. Investors and hospital networks should prioritize platform-agnostic consumables, AI navigation modules, and scalable RaaS distribution strategies that increase revenue per procedure while limiting balance-sheet sensitivity to capital-expenditure cycles.

Key Industry Highlights

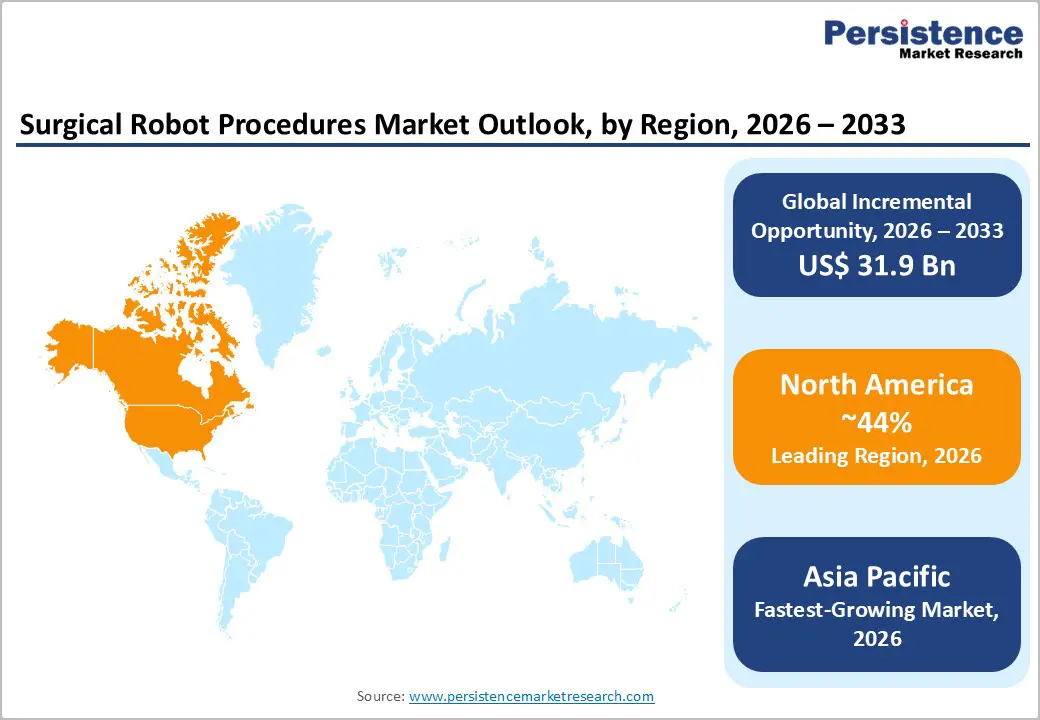

- Regional Leadership: North America is projected to command an estimated 44% market share in 2026, underpinned by reimbursement depth and installed-base utilization.

- Fastest-growing Market: Asia Pacific is likely to be the fastest-growing market through 2033, posting a 2026 - 2033 CAGR of about 22% due to rising surgical volumes and increasing private hospital investment.

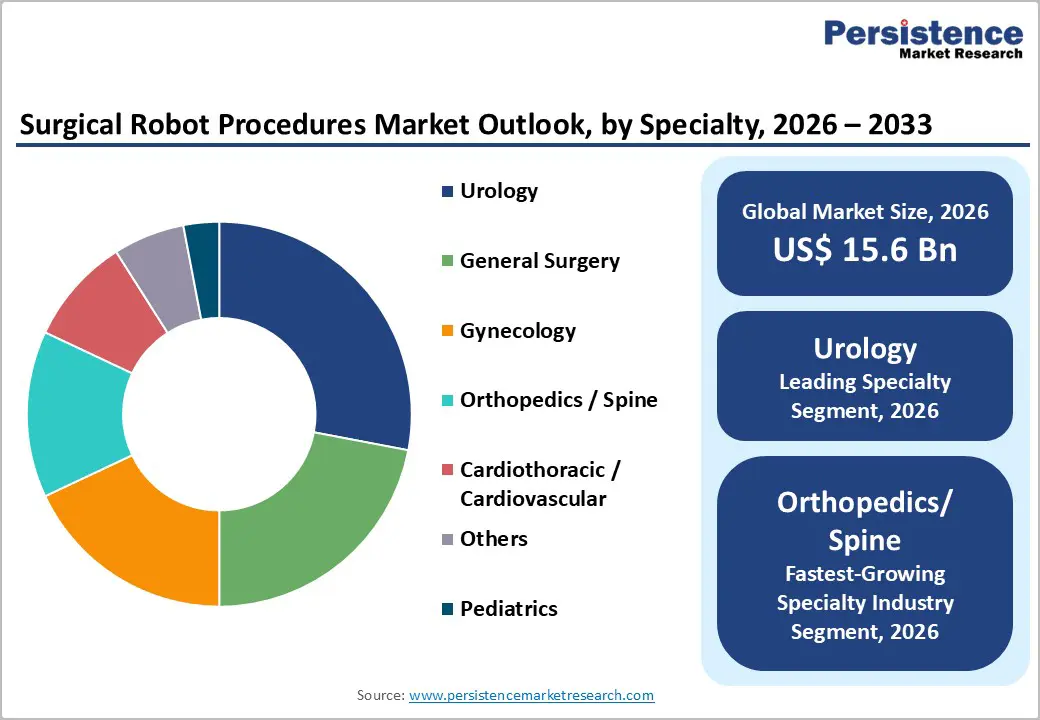

- Specialty Dominance: Urology is projected to dominate with an estimated 28% revenue share in 2026, reflecting long-standing robotic integration in prostatectomy and nephrectomy and wide surgeon familiarity.

- Fastest-growing Specialty: Orthopedics and spine procedures are expected to grow the fastest through 2033, with an estimated 23% CAGR, owing to improved robotic alignment precision and an aging population.

- Leading Technology: Multi-arm surgeon-console systems are projected to account for approximately 55% of revenue in 2026, while AI-enabled navigation modules are forecast to grow the fastest through 2033, with an estimated 29% CAGR.

| Key Insights | Details |

|---|---|

| Surgical Robot Procedures Market Size (2026E) | US$ 15.6 Bn |

| Market Value Forecast (2033F) | US$ 47.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.8% |

Market Factors - Growth, Barriers, Opportunity

Procedural Efficiency Unlocking ASCs and Same-Day Surgery Conversion

Regulatory clearances from the U.S. FDA are expanding the use of robot-assisted laparoscopic procedures across multiple specialties, and hospitals are increasingly deploying robotic systems beyond tertiary academic centers. Clinical trial evidence indicates that AI-guided camera systems enable solo laparoscopic cholecystectomy, reducing assistant requirements and shortening operating room (OR) time. Market leaders such as Intuitive Surgical, Inc. are reporting procedure growth in the low to mid teens, indicating rising utilization of existing installed systems. These trends are signaling that robotic platforms are shifting from capital-intensive showcase assets to productivity-enhancing clinical infrastructure. As regulatory acceptance expands and workflow automation improves, robotic surgery is becoming operationally viable in community hospitals and ambulatory surgery centers (ASCs).

Hospitals and ASCs are actively converting eligible procedures to same-day pathways to lower inpatient bed occupancy and improve contribution margins. Robotic workflows that integrate AI navigation and ergonomic instrumentation are reducing non-operative intervals such as setup and coordination time, allowing surgeons to complete more cases with leaner teams. Diagnosis-Related Group (DRG) reimbursement optimization and payer incentives for shorter lengths of stay are supporting this transition, particularly in oncology and high-volume benign procedures. The Lancet Commission and World Health Organization (WHO) surgical access data are highlighting unmet capacity in low- and middle-income countries (LMICs), which is increasing the relevance of RaaS models that reduce upfront capital expenditure. Investors and operators should prioritize structured pilot programs between robotic original equipment manufacturers (OEMs) and ASC management companies. These pilots should measure OR turnover time, full-time equivalent (FTE) assistant reduction, and same-day discharge rates to create a replicable economic value case for payers and health systems.

Fragmented Reimbursement and Capital Tariff Risks

Surgical robotics is capital-intensive, even as consumables and software are generating recurring revenue streams. Tariffs, import duties, and uneven hospital capital budgets are creating asymmetric adoption across regions. Recent company disclosures, including commentary from Intuitive Surgical, are indicating potential tariff exposure and supply chain pressure that may affect gross margins. The U.S. FDA is also tightening premarket requirements for connected platforms, including Software Bill of Materials (SBOM) documentation and formal cybersecurity threat modeling. These regulatory expectations are increasing validation timelines and compliance costs for systems integrating AI and networked components. As a result, platform developers are facing higher upfront development expenditure before commercialization.

Procurement cycles are lengthening in publicly funded hospital systems where capital allocation remains constrained. In the United States, return-on-investment calculations improve only when higher procedure volumes and reimbursement add-ons justify the initial system cost. In middle-income markets, tariffs and local content requirements are increasing delivered system prices by an estimated 5-12%, thereby slowing placement velocity. Heightened scrutiny of AI-enabled and semi-autonomous features is extending time to market by approximately 6 to 18 months and is adding development expense that may dilute operating margins by 200 to 400 basis points. Supply chain disruptions, including shortages of precision actuators and semiconductors, are creating one to two year timing risks that may reduce annual procedure growth by several percentage points in affected periods. OEMs can implement dual-pricing strategies that combine capital sales with RaaS models and localize production in tariff-sensitive regions. Investors, on the other hand, can incorporate regulatory and cybersecurity validation buffers into financial projections to avoid margin compression and launch delays.

AI-Enabled Navigation & Camera Modules to Speed up Adoption

Recent clinical trials have demonstrated that AI-enabled camera systems enable surgeons to perform solo laparoscopic procedures while reducing assistant headcount and OR traffic. If these modules achieve a 10-15% attach rate across global robotic procedures, incremental procedure-adjacent revenue could surpass US$5 billion over the 2026-2033 forecast period. This estimate reflects growing per-procedure contribution from software and analytics layers, which are increasing their share within overall robotic procedure economics. The attach-rate model assumes integration across urology, gynecology, and general surgery workflows, where automation benefits are measurable and repeatable.

AI navigation modules are advancing along a relatively favorable regulatory pathway because they function as accessories to cleared robotic platforms rather than standalone implantable devices. Hospitals are responding positively to modular upgrades that reduce OR personnel costs and increase throughput without requiring full platform replacement. Commercial capture is occurring through three primary models: bundled OEM software subscriptions at the surgical suite level, third-party module sales with per-procedure licensing similar to Software-as-a-Service (SaaS), and hybrid RaaS contracts incorporating tiered AI functionality. Investors should prioritize companies generating robust clinical evidence through randomized controlled trials (RCTs) or structured registries that document OR time reduction and FTE staff savings, as these metrics are influencing payer approval and chief financial officer (CFO) decision-making. Regulatory scrutiny of AI claims is intensifying, so firms should implement early post-market surveillance programs and cybersecurity validation. Cross-platform integration partnerships with at least two major robotic OEMs are increasing adoption probability and enhancing attach-rate potential. Although upfront development investment remains substantial, per-procedure software margins are exceeding consumable margins, creating scalable value for strategic acquirers.

Category-wise Analysis

Specialty Insights

Urology is projected to remain the leading clinical specialty in 2026, accounting for an estimated 28% of the surgical robot procedures market revenue share. Procedures such as radical prostatectomy and partial nephrectomy have historically represented the largest volume of robot-assisted cases due to demonstrated precision, improved visualization, and favorable oncologic margin outcomes. Surgeon familiarity with robotic workflows in urologic oncology is reinforcing utilization intensity, particularly within high-volume academic medical centers. Intuitive Surgical, Inc. and leading tertiary hospitals are continuing to report that urologic procedures generate the highest per-system usage rates, which is strengthening recurring instrument and accessory consumption. Grand View Research identifies urology as the dominant application segment, reflecting sustained procedural standardization and integration into residency training programs. This entrenched adoption base is supporting predictable consumable revenue streams and stable clinical demand.

Orthopedics and spine procedures are forecasted to record the fastest growth between 2026 and 2033, expanding at about 23% CAGR. Robotic assistance in joint replacement and spinal instrumentation is improving implant alignment accuracy and reducing revision risk, which is enhancing long-term cost effectiveness. Aging populations in North America, Europe, and parts of Asia Pacific are increasing the addressable patient pool for degenerative joint and spine conditions. Advances in modular navigation systems and haptic guidance technologies are facilitating adoption beyond tertiary hospitals into specialized orthopedic surgery centers. The higher capital intensity of orthopedic robotic platforms, combined with strong procedural demand, is generating above-market expansion relative to minimally invasive surgery (MIS) laparoscopic categories. Health systems are increasingly evaluating robotics in orthopedics based on measurable outcomes such as reduced revision rates and optimized implant positioning, which are strengthening the clinical and financial justification for accelerated investment.

Technology Insights

Multi-arm surgeon-console platforms are set to dominate by holding roughly 55% of the surgical robot procedures market share in 2026. Established systems such as the da Vinci platform from Intuitive Surgical, Inc. continue to dominate due to their extensive installed base and high instrument attachment rates per case. These platforms are generating the majority of procedure-linked revenue because hospitals are utilizing them across multiple specialties, including urology, gynecology, and general surgery. The maturity of the ecosystem, including surgeon training programs, standardized instrumentation, and recurring consumable usage, is reinforcing platform stickiness. Grand View Research and Fortune Business Insights continue to identify multi-arm systems as the principal revenue contributors within robotic-assisted surgery. As procedure volumes are increasing, these platforms are sustaining predictable recurring revenue streams tied to instruments, accessories, and service agreements.

AI-enabled navigation modules are anticipated to grow the fastest from 2026 to 2033. AI-guided camera and navigation systems are transitioning from pilot trials to structured commercial deployment, supported by early evidence of reduced assistant requirements and improved operating room efficiency. Reuters reporting on AI-assisted laparoscopic trials is demonstrating technical feasibility and rising hospital interest. Adoption is accelerating because these modules are retrofitting onto existing robotic platforms rather than requiring full system replacement. Commercialization pathways are clear, including SaaS subscriptions and per-procedure licensing structures. Hospitals are integrating these upgrades to improve throughput and reduce staffing costs, which is strengthening the economic case for rapid deployment. As regulatory pathways for accessory software are becoming more defined, integration timelines are shortening, further supporting expansion in this segment.

Business Model Insights

Direct capital purchases are likely to account for approximately 48% of total spending across platforms and related procedures in 2026. Tertiary hospitals and integrated health systems are continuing to favor upfront acquisition because ownership supports long-term cost optimization through bulk consumable contracts and structured service agreements. Academic medical centers are also investing in capital equipment to facilitate surgeon training programs and internal research initiatives. Public placement data compiled by Grand View Research indicates that high-resource markets such as the United States and Western Europe are sustaining capital sales momentum due to favorable reimbursement frameworks and stable funding access. Ownership structures enable health systems to negotiate volume-based pricing for instruments and accessories, thereby improving lifetime system economics. As procedure volumes are increasing, capital buyers are maximizing utilization rates to justify investment and enhance return on capital employed.

RaaS models are projected to grow the fastest during the 2026-2033 forecast period, displaying a CAGR of nearly 30%. These models are addressing total cost of ownership (TCO) concerns by converting capital expenditure into predictable operating expenditure. Ambulatory surgery centers, mid-market hospitals, and providers in emerging economies are adopting RaaS to overcome upfront budget constraints while gaining access to advanced robotic capabilities. OEMs and distribution partners are structuring agreements that link system access to minimum consumable commitments and tiered software packages. This approach is increasing procedure throughput while expanding recurring revenue visibility for suppliers. By lowering entry barriers, RaaS is enlarging the addressable market and enabling faster share expansion in capital-constrained regions. Health systems are increasingly evaluating robotic adoption within operating budget frameworks, thereby reinforcing the shift toward service-based acquisition strategies.

Regional Insights

North America Surgical Robot Procedures Market Trends

North America is projected to account for approximately 44% of the surgical robot procedures market share in 2026, on the back of high per-procedure reimbursement levels, a dense concentration of academic medical centers, and large private hospital networks that are actively expanding robotic capabilities. Intuitive Surgical, for example, has been reporting procedure growth in the mid-teens within the United States, reflecting rising installed base utilization and consistent system placements. The U.S. market is generating a disproportionate share of global consumable revenue due to higher instrument usage per case and premium pricing structures. This combination of strong utilization intensity and pricing leverage is sustaining regional revenue leadership despite slower percentage growth compared to emerging markets.

Regional expansion is being supported by integrated payer reimbursement models, predictable capital allocation within large health systems, and regulatory clarity from the U.S. FDA regarding device and software pathways. While regulatory transparency is enabling iterative product enhancements, cybersecurity documentation and software lifecycle compliance requirements are increasing development and validation costs. The competitive landscape remains concentrated at the platform level, yet new entrants are targeting performance and price differentiation in single-port and endoscopic robotic segments. Investment activity is increasingly focused on acquisitions and partnerships involving imaging and navigation startups that strengthen platform ecosystems. Growth in selected intraregional segments is expected to range between 11-13% annually through 2033, although overall expansion is moderating relative to Asia Pacific. OEMs operating in North America need to prioritize high-margin software modules, consumable optimization strategies, and selective RaaS pilots in ASCs to sustain profitability while protecting market share.

Europe Surgical Robot Procedures Market Trends

Europe is slated to hold around 22% market share in 2026, characterized by heterogeneous adoption patterns across the region. Western European countries such as Germany, France, and the United Kingdom are exhibiting high penetration of multi-arm robotic platforms, particularly within tertiary referral centers and large private hospital groups. Public reimbursement structures are moderating capital expenditure cycles, yet they are encouraging investments that demonstrably reduce inpatient length of stay and improve procedural efficiency. Germany and the United Kingdom are generating the highest procedural volumes within the region, supported by advanced surgical infrastructure and established robotic training pathways. Grand View Research and regional analyses continue to identify Europe as a major revenue contributor, with steady growth underpinned by mature healthcare systems.

Regional expansion is being shaped by centralized national health systems that are prioritizing measurable cost-effectiveness and evidence-based procurement decisions. The European Union Medical Device Regulation (EU MDR) and evolving artificial intelligence regulatory frameworks are raising compliance thresholds for connected surgical platforms. These requirements are extending validation timelines but are strengthening long-term market confidence once approvals are secured. Investment capital is increasingly targeting modular, cost-efficient robotic systems and software partners capable of demonstrating economic value within DRG and bundled payment environments. OEMs operating in Europe should focus on developing country-specific clinical and economic dossiers tailored to national payer expectations and should leverage cross-border procurement alliances to accelerate multi-country deployment.

Asia Pacific Surgical Robot Procedures Market Trends

Asia Pacific is anticipated to account for approximately 28% of the surgical robot procedures market sales in 2026, and is expected to record the fastest regional expansion through 2033 at an estimated CAGR of 22%. Market growth here is being supported by rising surgical case volumes, increasing government healthcare expenditure, and rapid expansion of private hospital networks across China, India, Japan, and South Korea. Japan and South Korea are continuing to lead in early adoption of advanced robotic platforms, supported by strong reimbursement frameworks and technological infrastructure. In contrast, China, India, and several Southeast Asian markets are accelerating system placements through a mix of imported platforms and emerging domestic manufacturers. Data from the Lancet Commission and the WHO indicate significant unmet surgical demand across multiple Asia Pacific countries, suggesting a substantial addressable base for robotic procedures once affordability constraints are addressed.

Demographic expansion of aging populations in East Asia, increasing prevalence of chronic and degenerative conditions, and rising acceptance of minimally invasive techniques are also playing a central role in fueling market growth. Expanding private healthcare networks are investing in robotics to differentiate services and attract higher-acuity patients. Lower per-procedure labor costs are encouraging selective automation where throughput gains justify investment. Local OEMs are introducing lower TCO systems, intensifying price competition and improving accessibility. Investment activity is accelerating through private equity participation and joint venture partnerships between regional manufacturers and international platform developers. Companies seeking to scale in the Asia Pacific should deploy RaaS pilots, localize manufacturing to mitigate tariff exposure, and tailor software and consumable strategies to specialty demand patterns within each country.

Competitive Landscape

The global surgical robot procedures market structure is likely to remain concentrated at the OEM level, where a limited number of platform leaders, mainly Intuitive Surgical, Medtronic, and Johnson & Johnson, control the majority of the installed base. However, the procedures-adjacent ecosystem, including consumables, software, AI modules, and RaaS operators, is becoming more fragmented and competitive. Intuitive Surgical continues to exert the largest influence on global procedure volumes and recurring consumable revenue due to its extensive installed base and reported double-digit procedure growth. Public reporting and industry research consistently position Intuitive as the market leader by global procedure share, while other established and emerging platform providers are increasing placements in targeted specialties and price-sensitive segments. Competitive dynamics are intensifying as specialty vendors introduce differentiated systems for orthopedics, single-port surgery, and endoscopic applications, selectively capturing incremental procedure share.

OEMs with broad installed footprints are benefiting from recurring instrument sales, service contracts, and ecosystem lock-in advantages that support high-margin consumable monetization. Platform-agnostic software and AI companies are capturing attach rates across multiple robotic systems by offering navigation, analytics, and workflow optimization modules that integrate with existing consoles. RaaS operators and distribution intermediaries are aggregating procedure volumes across hospital networks, thereby increasing bargaining power and expanding access in capital-constrained environments. Over time, system-level concentration is expected to gradually moderate as lower-cost platforms and single-port technologies enter ASCs and mid-market hospitals.

Key Industry Developments :

- In January 2026, Johnson & Johnson submitted the OTTAVA™ Robotic Surgical System to the U.S. FDA for De Novo classification, using data from an Investigational Device Exemption (IDE) clinical study to support marketing authorization in multiple general surgery procedures. The company’s submission follows approval of a second clinical trial for inguinal hernia repair and reflects efforts to broaden soft-tissue robotic capabilities.

- In December 2025, Medtronic announced that the U.S. FDA cleared its Hugo™ Robotic-Assisted Surgery (RAS) system for minimally invasive urologic surgical procedures, including prostatectomy, nephrectomy, and cystectomy. The clearance follows the largest U.S. clinical study for multi-port robotic urological surgery showing safety and effectiveness, and positions Hugo as a new robotic option for hospitals.

- In October 2025, the All India Institute of Medical Sciences (AIIMS), New Delhi, successfully performed India’s first robot-assisted kidney transplant surgery. The surgery utilized advanced robotic precision to enhance operative accuracy and reduce patient recovery time, reflecting growing adoption of surgical robotics in high-complexity procedures within India’s public healthcare system.

Companies Covered in Surgical Robot Procedures Market

- Intuitive Surgical, Inc.

- Medtronic plc

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Smith & Nephew plc

- TransEnterix/Asensus Surgical, Inc.

- CMR Surgical Ltd.

- Verb Surgical

- Levita Magnetics Ltd.

- Auris Health

- Brainlab AG

- Globus Medical

- Siemens Healthineers

Frequently Asked Questions

The global surgical robot procedures market is projected to reach US$ 15.6 billion in 2026.

Supportive regulatory clearances from the U.S. FDA, broadening the range of approved indications, and the development of AI-enabled navigation systems and RaaS models, which are lowering upfront capital exposure are driving the market.

The market is poised to witness a CAGR of 17.3% from 2026 to 2033.

The upscaling of robot-assisted laparoscopic procedures in urology, gynecology, and general surgery, and increase in per-procedure revenue from instruments and software are key market opportunities.

Intuitive Surgical, Inc., Medtronic plc, Johnson & Johnson, and Stryker Corporation are some of the key players in the market.