- Food Ingredients & Additives

- Starch Derivatives Market

Starch Derivatives Market Size, Share, and Growth Forecast, 2025 - 2032

Starch Derivatives Market By Product Type (Maltodextrin, Glucose Syrup, Cyclodextrin, Hydrolysates, Modified Starch, Others), Source (Corn, Wheat, Cassava, Potato, Rice, Others), Application (Food & Beverages, Cosmetics, Paper, Pharmaceuticals, Feed, Others), and Regional Analysis for 2025 - 2032

Starch Derivatives Market Size and Trends Analysis

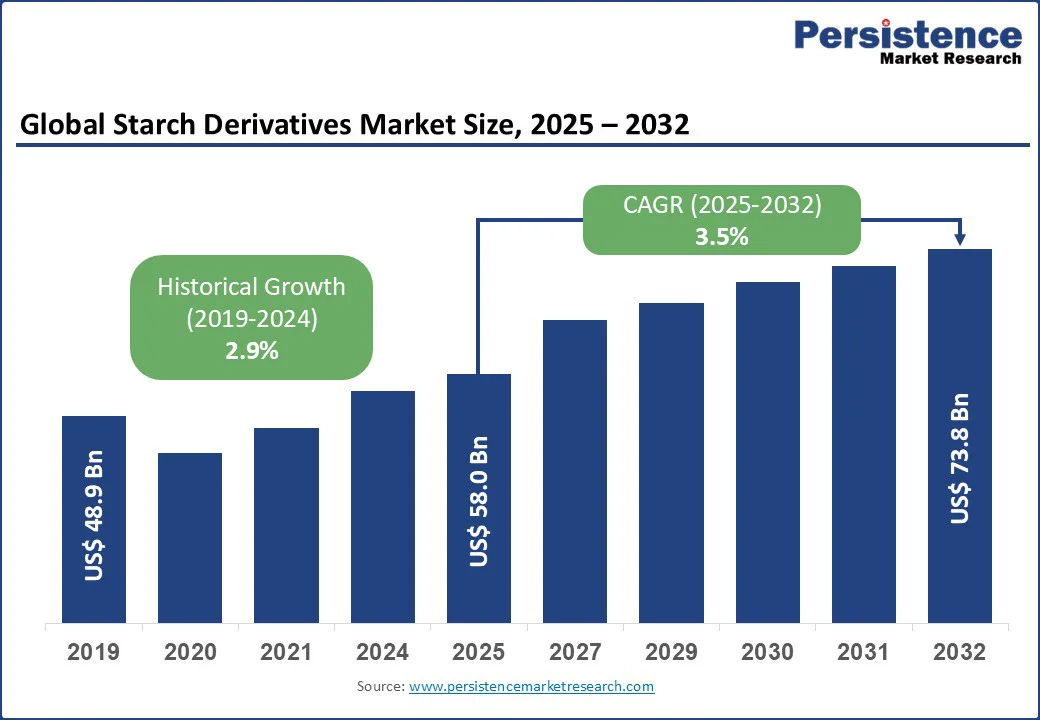

The global starch derivatives market size is likely to value at US$ 58.0 Bn in 2025 and reach US$ 73.8 Bn by 2032, registering a CAGR of 3.5% during the forecast period from 2025 to 2032.

The starch derivatives market has experienced consistent growth, driven by the rising demand for processed and convenience foods, expanding applications in pharmaceuticals and cosmetics, and the increasing adoption of starch derivatives in industrial sectors such as paper and textiles. The versatility of starch derivatives, coupled with their cost-effectiveness and eco-friendly nature, has made them indispensable across multiple industries. The growth is further supported by advancements in production technologies, increasing consumer preference for natural and sustainable ingredients, and the expansion of food processing industries in emerging economies.

Key Industry Highlights:

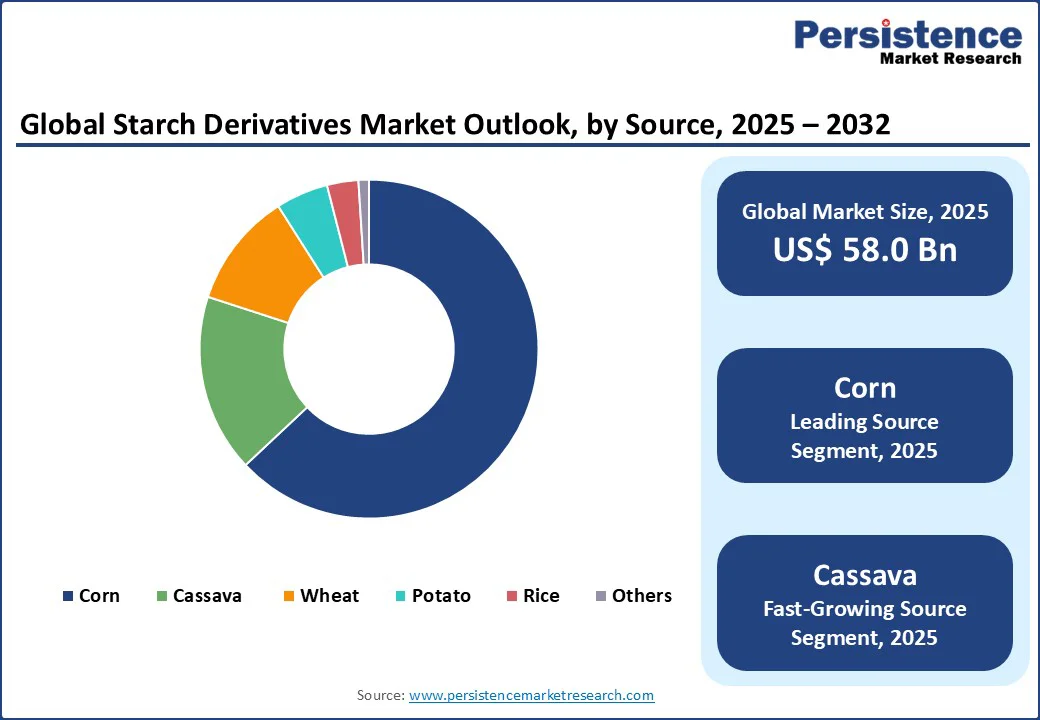

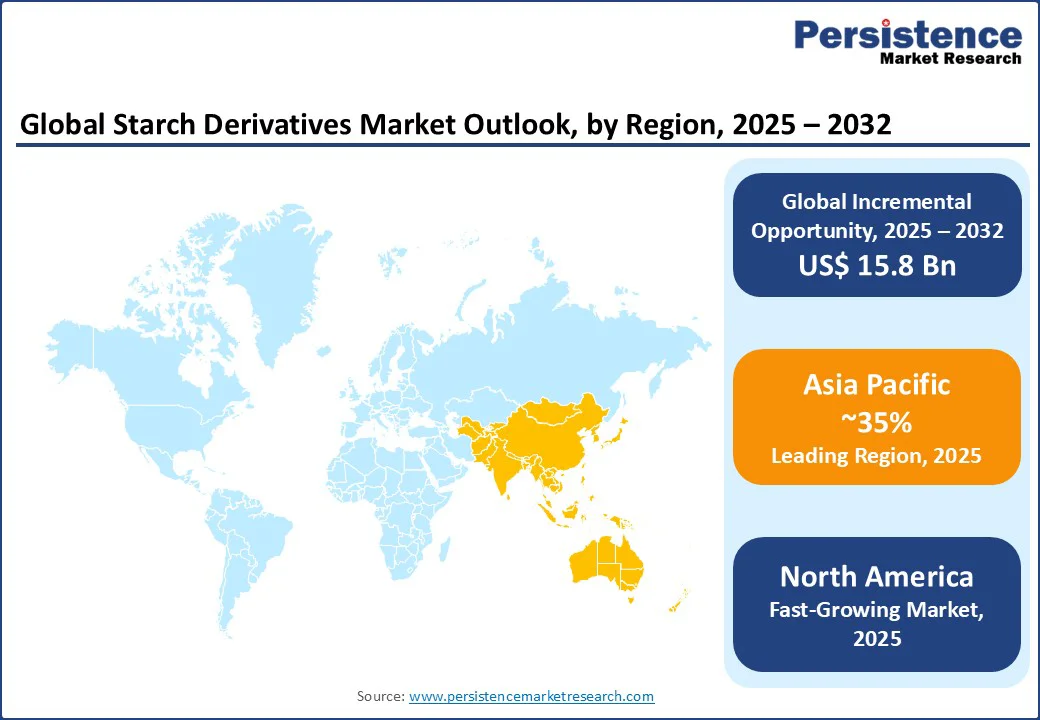

- Leading Region: Asia Pacific, commanding a 35% market share in 2025, driven by stems from rapid industrialization, sophisticated food processing sectors, rising demand for convenience and healthier products, and strong innovation ecosystems in countries such as China and India.

- Fastest-growing Region: North America, propelled by the region's benefits from strong R&D capabilities, a mature food processing sector, and growing demand for clean-label and functional ingredients.

- Dominant Product Type: Maltodextrin, holding nearly 35% market share, due to extensive use in food & beverages, pharmaceuticals, cosmetics, and industrial applications.

- Leading Application: Food & Beverages, accounting for over 66% of market revenue, driven by the global surge in processed food consumption.

- Historical Growth: The sector registered a CAGR of 2.9% from 2019 to 2024, fueled by rising demand for functional ingredients and expanding industrial applications.

- Sustainability Trends: Growing emphasis on bio-based and sustainable starch derivatives is boosting market growth, particularly in Europe and North America.

|

Global Market Attribute |

Key Insights |

|

Starch Derivatives Market Size (2025E) |

US$ 58.0 Bn |

|

Market Value Forecast (2032F) |

US$ 73.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.9% |

Market Dynamics

Driver - Growing Demand for Processed and Convenience Foods

The rising demand for processed and convenience foods is a primary driver propelling the growth of the domain. Rapid urbanization, changing consumer lifestyles, and increasing disposable incomes have fueled the consumption of ready-to-eat meals, snacks, and beverages, particularly in emerging economies. Starch derivatives, such as glucose syrup and modified starch, are widely used as thickeners, stabilizers, and sweeteners in processed foods, enhancing texture, shelf life, and taste.

According to the Food and Agriculture Organization (FAO), global food consumption is expected to increase by 1.3% annually, with processed foods accounting for a significant share. In the U.S., the packaged food market is projected to reach US$ 1.2 trillion by 2030, with starch derivatives playing a critical role in product formulations.

The growing popularity of clean-label and plant-based products has increased the demand for natural starch derivatives derived from corn, cassava, and potato, further driving market growth. The expansion of the food processing industry in the Asia Pacific, particularly in China and India, is also a key factor, as these countries are witnessing a surge in demand for convenience foods due to busy lifestyles and rising middle-class populations.

Restraint - Fluctuations in Raw Material Prices

Fluctuations in raw material prices pose a significant restraint on the growth of the industry. Starch derivatives are primarily sourced from crops such as corn, wheat, cassava, and potato, which are subject to price volatility due to weather conditions, supply chain disruptions, and geopolitical factors. For instance, adverse weather events, such as droughts or floods, can reduce crop yields, leading to higher raw material costs. According to the U.S. Department of Agriculture (USDA), climate variability and supply chain disruptions have significantly influenced corn markets in recent years. These price variations increase production costs for manufacturers, which may be passed on to consumers, potentially reducing demand in price-sensitive markets.

Competition for raw materials from other industries, such as biofuels, further exacerbates price instability, particularly in regions such as North America and Europe. This volatility can limit the scalability of starch derivative production and hinder market growth, especially for smaller manufacturers with limited financial flexibility.

Opportunity - Advancements in Bio-based Starch Derivatives

Advancements in bio-based starch derivatives present a significant opportunity for market growth. With increasing consumer and regulatory focus on sustainability, manufacturers are investing in eco-friendly and biodegradable starch derivatives for applications in food, packaging, pharmaceuticals, and cosmetics. For instance, Cargill and Ingredion have developed biodegradable packaging films using modified corn starch, reducing reliance on traditional plastics.

Innovations in enzymatic modification and fermentation technologies have enabled the development of high-performance starch derivatives with enhanced functionality, such as improved solubility, stability, and biodegradability. For instance, Roquette uses enzymatic modification to produce starches suitable for controlled drug delivery in pharmaceuticals.

Research into novel starch sources, such as rice and cassava, is expanding the sector’s potential in regions with abundant agricultural resources, such as the Asia Pacific. An example is Thai-based Charoen Pokphand Foods exploring cassava-based starch for biodegradable food packaging. These advancements not only cater to environmentally conscious consumers but also open new revenue streams for manufacturers, driving sustained market growth.

Category-wise Analysis

Product Type Insights

Maltodextrin is a key product type, with a 35 % share, widely used across multiple industries due to its versatile properties. In the food and beverage sector, it functions as a thickener, stabilizer, and energy source, making it popular in sports drinks, confectionery, and processed foods. In pharmaceuticals, maltodextrin acts as a binding and filler agent in tablets, while in cosmetics, it is used for its texture-enhancing qualities. Its easy digestibility, low sweetness, and cost-effectiveness continue to drive strong demand globally.

The Modified Starch segment is the fastest-growing, driven by increasing demand for functional ingredients in food, pharmaceuticals, and cosmetics. Modified starches offer enhanced properties, such as improved stability under high temperatures and varying pH levels, making them ideal for clean-label and plant-based products. The rise in consumer preference for natural and sustainable ingredients, coupled with advancements in modification technologies, is accelerating the adoption of this segment, particularly in North America and Europe.

Source Insights

Corn holds the largest market share, accounting for approximately 63% of revenue in 2025. Its dominance is driven by its widespread availability, cost-effectiveness, and high starch content, making it a primary raw material for starch derivatives globally. The U.S., a leading corn producer, contributes significantly to this segment, with companies such as Cargill and ADM leveraging advanced processing technologies to meet demand.

Cassava is the fastest-growing source segment, fueled by its increasing cultivation in the Asia Pacific and Africa. Cassava-based starch derivatives are gaining popularity due to their neutral taste, high clarity, and suitability for gluten-free and clean-label products. The expansion of cassava cultivation in countries such as Thailand, Vietnam, and Nigeria, coupled with investments in processing infrastructure, is driving rapid adoption in this segment.

Application Insights

Food & beverages leads, holding a 66% share in 2025. The segment’s dominance is driven by the global surge in processed food consumption, with starch derivatives used as thickeners, stabilizers, and sweeteners in products such as sauces, desserts, and beverages. The growing demand for convenience foods, particularly in urban areas, further boosts this segment.

The pharmaceuticals segment is the fastest-growing, driven by the increasing use of starch derivatives as excipients, binders, and disintegrants in drug formulations. The rise in chronic diseases and investments in pharmaceutical R&D, particularly in the Asia Pacific, are accelerating the adoption of starch derivatives in this segment.

Regional Insights

North America Starch Derivatives Market Trends

North America is expected to lead the bio-based global starch derivatives market, driven by several strategic advantages that the region holds. One key factor is the region’s strong research and development (R&D) capabilities, which enable companies to innovate and develop high-performance starch derivatives with enhanced properties such as improved solubility, stability, and biodegradability. Leading manufacturers in the region are actively investing in advanced enzymatic modification and fermentation technologies to produce starch derivatives suitable for diverse applications, including food, packaging, pharmaceuticals, and cosmetics.

North America has a well-established and mature food processing sector, which supports the rapid adoption of innovative ingredients, including bio-based starches. Growing consumer demand for clean-label, natural, and functional ingredients further propels market growth, as both food and beverage manufacturers increasingly seek eco-friendly alternatives to synthetic additives. Furthermore, supportive regulatory frameworks promoting sustainability and environmental protection encourage companies to adopt biodegradable and renewable starch derivatives. Together, these factors position North America as a key growth hub for bio-based starch derivatives, offering opportunities for innovation, expansion, and long-term market development.

Europe Starch Derivatives Market Trends

Europe holds a significant share in the starch derivatives market, driven by advanced food processing industries, stringent sustainability regulations, and growing demand for bio-based ingredients. Leading countries include Germany, France, and the UK. Germany benefits from its robust food and pharmaceutical industries, with companies such as AGRANA investing in innovative starch-based solutions.

The UK’s market is bolstered by rising consumer demand for clean-label and plant-based foods, supported by government initiatives promoting sustainable practices. France’s market is driven by its strong bakery and confectionery sectors, where starch derivatives are widely used. The EU’s focus on reducing plastic waste and promoting bioplastics, as outlined in the European Green Deal, is accelerating the adoption of starch-based packaging materials. However, stringent regulations from the European Food Safety Authority (EFSA) pose challenges for manufacturers. Europe’s starch derivatives market is projected to grow steadily from 2025 to 2032.

Asia Pacific Starch Derivatives Market Trends

Asia Pacific is poised to be a major contributor to the starch derivatives market, commanding an estimated 35% market share in 2025. The region’s rapid industrialization has accelerated the growth of its food processing, pharmaceutical, and packaging sectors, creating a strong foundation for starch derivative adoption. Countries such as China and India are investing heavily in advanced manufacturing infrastructure, research, and development, fostering innovation in high-performance starch derivatives with enhanced solubility, stability, and biodegradability.

The region is also witnessing a surge in consumer demand for convenience foods, functional ingredients, and healthier alternatives. Rising health awareness and preference for clean-label and natural products are encouraging manufacturers to develop bio-based and sustainable starch derivatives to meet these evolving consumer needs.

Furthermore, Asia Pacific benefits from a rich supply of raw materials such as rice, cassava, and corn, which ensures a consistent and cost-effective production of starch derivatives. Strong innovation ecosystems in countries such as China, India, Japan, and South Korea support research in enzymatic modification and fermentation technologies, enabling the creation of versatile starch products for food, packaging, pharmaceuticals, and personal care applications. These combined factors make the Asia Pacific a key growth hub, offering significant opportunities for market expansion and long-term revenue generation.

Competitive Landscape

The global starch derivatives market is characterized by intense competition, regional strengths, and a mix of international and local manufacturers. In developed regions such as North America and Europe, large firms such as Cargill, ADM, and Ingredion dominate through scale, advanced R&D capabilities, and established partnerships with food, pharmaceutical, and packaging companies.

In the Asia Pacific, rapid industrialization, growing demand for convenience and functional foods, and abundant agricultural resources are attracting significant investments from both international players and regional leaders, such as Matsutani Chemical Industry and several local manufacturers in China and India. Companies are focusing on product innovation, sustainability, and cost-efficiency to gain a competitive edge.

The development of bio-based, clean-label, and high-performance starch derivatives has emerged as a key differentiator, enabling faster market adoption and stronger consumer preference. Strategic collaborations, acquisitions, and investments in advanced enzymatic and fermentation technologies are further intensifying competition. Overall, the industry exhibits a dual nature, consolidated at the top by global giants while remaining fragmented across numerous regional and niche players that cater to local needs, affordability-driven segments, and emerging applications.

Industry Developments:

- In March 2023, Ingredion launched a new line of clean-label modified starches for food and beverage applications, targeting the growing demand for natural ingredients.

- In November 2022, Cargill launched a bio-based starch derivative designed for sustainable packaging applications, supporting global initiatives to reduce plastic waste and promoting eco-friendly alternatives in the packaging industry.

Companies Covered in Starch Derivatives Market

- Cargill

- ADM (Archer Daniels Midland Company)

- Ingredion

- Tate & Lyle

- Roquette

- AGRANA

- Grain Processing Corporation

- Avebe

- Emsland Group

- Matsutani Chemical Industry

- Others

Frequently Asked Questions

The global Starch Derivatives Market is projected to reach US$ 58.0 Bn in 2025.

The growing demand for processed and convenience foods is a key driver.

The starch derivatives market is poised to witness a CAGR of 3.5% from 2025 to 2032.

Advancements in bio-based starch derivatives, such as sustainable packaging materials, are a key opportunity.

Cargill, ADM, Ingredion, Tate & Lyle, and Roquette are key players.