- Medical Devices

- Global Specimen Processing Equipment Market

Global Specimen Processing Equipment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Specimen Processing Equipment Market by Product Type (Centrifuge, Processors, Freeze Dryer), Sample Type (Blood Samples, Tissue Samples, Body Fluids), Automation Level (Fully Automated, Semi-Automated, Manual), End User (Hospitals, Diagnostic Laboratories, Research Centers, Pharmaceutical & Biotechnology Companies, Others), and Regional Analysis from 2026 to 2033

Specimen Processing Equipment Market Size and Trends Analysis

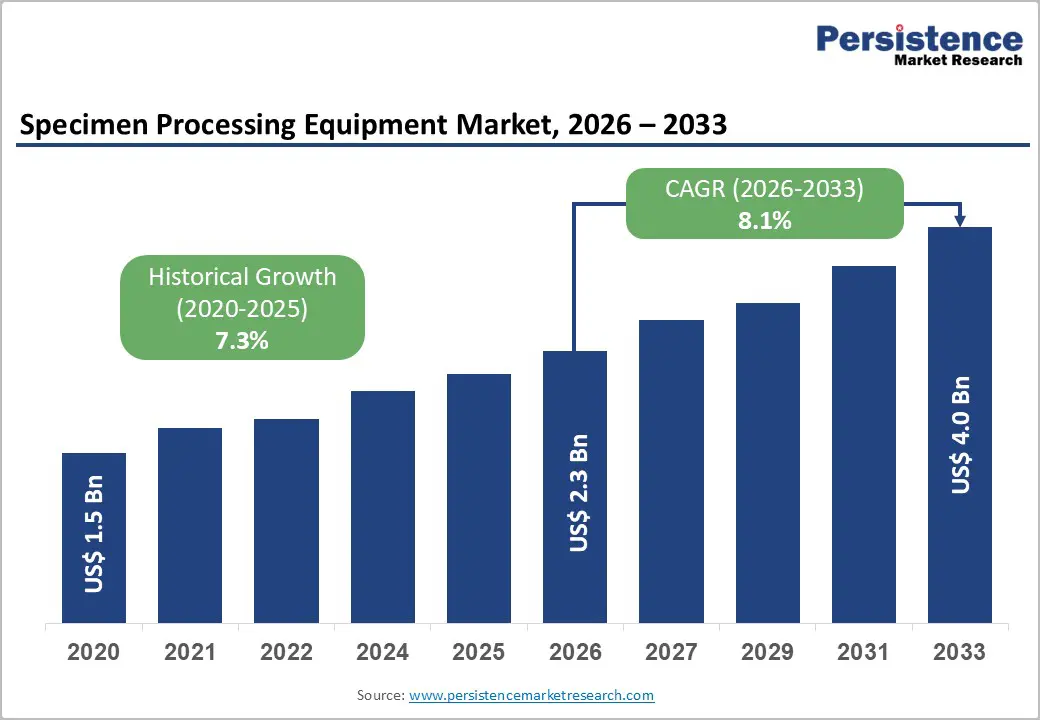

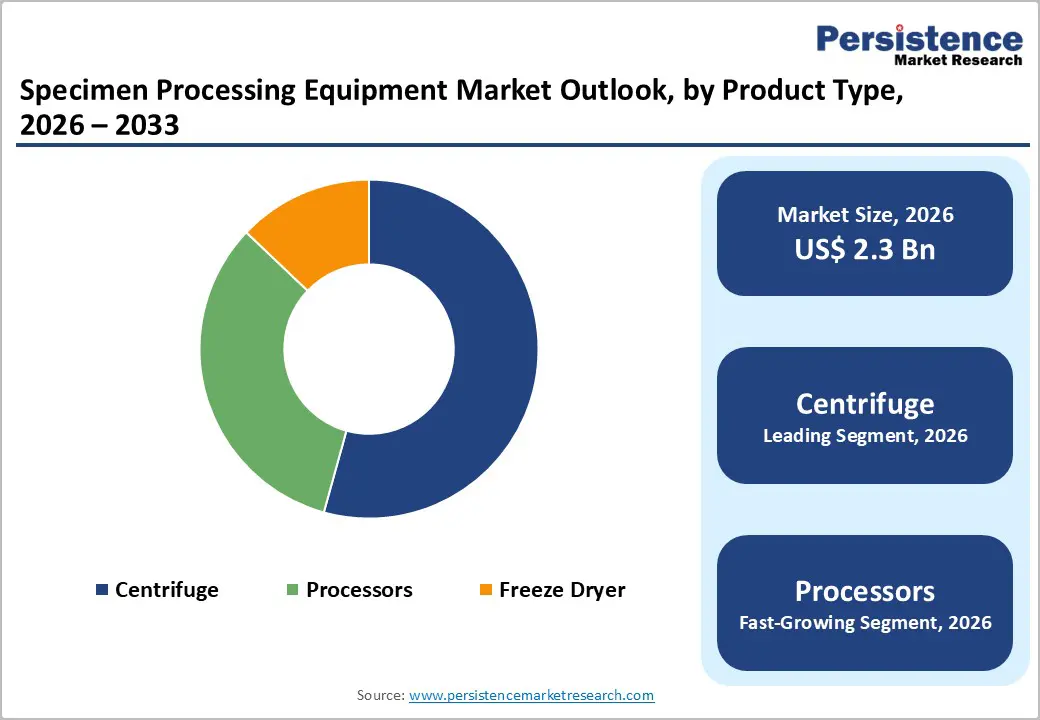

The global Specimen Processing Equipment Market is estimated to grow from US$ 2.3 Bn in 2026 to US$ 4.0 Bn by 2033. The market is projected to record a CAGR of 8.1% during the forecast period from 2026 to 2033.

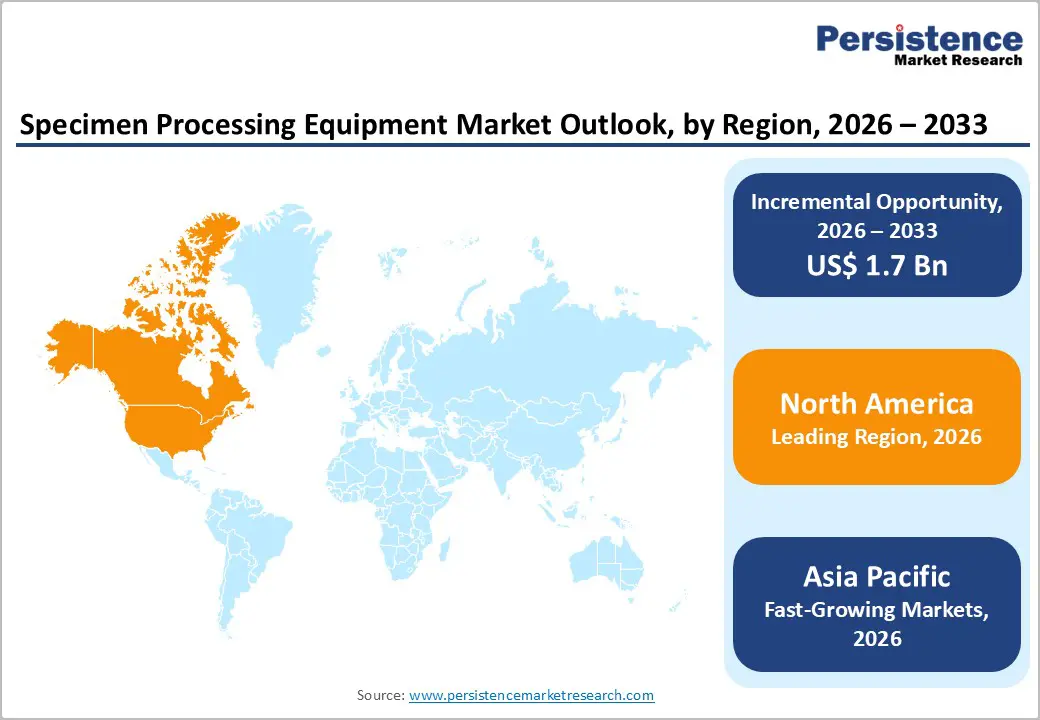

The Specimen Processing Equipment Market is growing steadily, driven by rising demand for automated laboratories, increasing diagnostic testing, and expanding research activities. North America leads due to advanced healthcare infrastructure, while Asia-Pacific shows the fastest growth, fueled by rising lab automation, expanding hospitals, and growing biobanking. Europe maintains steady demand, with Latin America and MEA emerging.

Key Industry Highlights

- Dominant Segment: Centrifuges hold the largest share in 2025 at 54.3%, driven by universal use in blood, tissue, and body fluid processing across hospitals, diagnostic labs, and research centers. Their efficiency, reliability, and ease of use make them the preferred choice for routine and high-throughput sample processing.

- Dominant Region: North America holds 40.3% share in 2025, supported by advanced healthcare infrastructure, high adoption of lab automation, and strong diagnostic testing demand. Asia-Pacific is the fastest-growing region due to rising laboratory automation, expanding hospitals and research facilities, growing biobanking, and increasing healthcare investments. Europe maintains steady demand, while Latin America and MEA are emerging markets.

- Market Drivers: Growth is fueled by rising demand for automated laboratories, increasing diagnostic testing, expanding research activities, adoption of high-throughput workflows, and the need for accurate, reliable, and efficient specimen processing equipment.

- Market Opportunity: Key opportunities include automated and integrated specimen processing systems, expansion of lab automation in emerging markets, innovations in pre-analytical and sample handling technologies, growth in biobanking and clinical research, and adoption of AI- and IoT-enabled devices for improved workflow efficiency.

| Global Market Attributes | Key Insights |

|---|---|

| Global Specimen Processing Equipment Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 4.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.3% |

Market Dynamics

Driver – Rising adoption of laboratory automation in hospitals and diagnostic labs

The rising adoption of laboratory automation in hospitals and diagnostic labs significantly drives the specimen processing equipment market because it enhances efficiency, accuracy, and throughput in clinical workflows. Studies indicate that automation systems reduce manual error rates substantially and streamline laboratory operations, leading to faster and more reliable diagnostics. Automation spans specimen handling, analyzers, and integrated workflows, and has been increasingly implemented to manage expanding test volumes and workforce limitations. Evidence from clinical laboratory automation research shows that automation reduces specimen turnaround time and markedly improves operational productivity, which directly supports greater demand for specimen processing equipment such as automated centrifuges and processors.

Government aligned research and open access studies demonstrate measurable benefits from lab automation that justify its growing adoption. For example, clinical laboratories implementing automated workflows have reported reductions in error rates exceeding 70 percent and decreased staff time per specimen analyzed by over 10 percent, illustrating operational gains. Automation also increases laboratory capacity without proportionally increasing workforce size, addressing shortages of qualified technicians. Regional clinical lab data further show that major health systems are deploying fully automated pathology labs capable of processing thousands of tests per hour, underscoring how automation enhances diagnostic throughput and accuracy in real world healthcare settings.

Restraints – High capital cost of automated specimen processing equipment

A significant restraint in the specimen processing equipment market is the high capital cost of automated systems, which limits adoption, especially in price sensitive settings such as smaller hospitals and laboratories. Advanced pre analytical processors and total lab automation installations frequently require substantial upfront expenditure for example, pre analytical automation equipment alone can cost between USD 125,000 and USD 350,000, with comprehensive automation systems reaching even higher totals. These high purchase prices often exceed the annual equipment budget of many facilities, forcing administrators to delay or forgo automation despite its operational benefits. The financial burden is further compounded by associated infrastructure, software, and staff training costs.

Reliable data on laboratory budgeting highlights the extent of cost constraints. Typical pre analytical automation systems range from USD 150,000 to over USD 1,000,000 for full suites, illustrating that capital costs represent a major percentage of total laboratory expenditures. Additionally, industry observations show that a mid sized medical laboratory’s total equipment budget often falls between USD 200,000 and USD 500,000, meaning that fully automated specimen processing solutions alone can consume or exceed this range. This disparity between automation cost and budget capacity underpins hesitancy among facilities to adopt high end automation despite its clinical advantages.

Opportunity – Development of fully automated and integrated specimen processing systems

The development of fully automated and integrated specimen processing systems represents a significant opportunity for the specimen processing equipment market because it enables clinical laboratories to handle high test volumes with greater accuracy, speed, and consistency. Fully automated systems combine specimen receipt, sorting, preparation, analysis, and reporting into one seamless workflow, reducing manual steps and variability. Research shows that automation can minimize human errors by more than 70 percent and reduce staff time per specimen analyzed by around 10 percent, illustrating operational improvements that laboratories seek when investing in integrated platforms. These advances improve quality of care by speeding diagnostics and enhancing reliability.

Evidence from clinical laboratory literature highlights the practical benefits of automation that justify market opportunity. For example, total laboratory automation has been shown to increase the number of tests performed per worker significantly, boosting productivity in key sections like clinical chemistry and serology. Laboratories adopting fully automated workflows report faster turnaround times and the ability to maintain or expand service volumes even with limited personnel, addressing workforce shortages objectively. These real world improvements are reflected in automated lab implementations worldwide, including facilities processing thousands of tests per hour, demonstrating how integrated automation systems enhance capacity, reduce error, and improve workflow efficiency across diagnostic settings.

Category-wise Analysis

By Product Type, Centrifuge Dominates the Specimen Processing Equipment Market

Centrifuge occupies 54.3% share of the global market in 2025, because they are essential across virtually all clinical and research laboratories for separating biological components blood cells, plasma, serum, and tissue lysates making them indispensable in routine diagnostics. Clinical laboratory automation guidelines emphasize that centrifugation remains the primary pre analytical step for most assays, with standardized protocols established by organizations such as the Clinical and Laboratory Standards Institute (CLSI) due to its role in ensuring sample quality and reproducibility. Government aligned sources show that routine blood chemistry, hematology, and serology testing most of which require centrifugation account for the majority of laboratory tests performed daily in public health systems, underscoring centrifuges’ broad utility and high utilization compared with more specialized processors or freeze dryers.

By Sample Type, Blood Samples is gaining traction due to high testing volume in diagnostics, monitoring, and routine clinical laboratory workflows

Blood samples dominate the Specimen Processing Equipment Market by sample type because they represent the highest volume of clinical testing in healthcare systems worldwide, serving as the primary source for routine diagnostics and disease monitoring. For example, clinical practice data show that in U.S. emergency departments nearly half (49.9%) of visits involved at least one blood test, reflecting frequent use for assessments like complete blood count, metabolic panels, and coagulation assays far more than imaging or other specimen types. Routine blood testing is integral to diagnosing conditions ranging from anemia and diabetes to cardiac and infectious diseases, making blood the most commonly processed specimen in laboratories. As such, specimen processing equipment like centrifuges and automated analyzers are heavily utilized to prepare blood specimens (whole blood, serum, or plasma) for analysis, reinforcing the dominance of blood samples in the market.

Regional Insights

North America Specimen Processing Equipment Market Trends

North America dominates the Specimen Processing Equipment Market with 40.3% share in 2025, because of its advanced healthcare infrastructure, high diagnostic testing volumes, and widespread adoption of laboratory automation. In the United States alone, clinical laboratories perform over 7 billion diagnostic tests annually, making it one of the largest testing markets globally. Furthermore, the U.S. Centers for Medicare & Medicaid Services reports that routine blood testing accounts for a substantial portion of outpatient services, reinforcing heavy utilization of specimen processing systems.Government health data also show that the U.S. leads in per capita healthcare spending and investment in laboratory technologies, facilitating faster adoption of automated and integrated specimen processing equipment. These factors collectively sustain North America’s dominant share and continued demand for specimen processing solutions.

Europe Specimen Processing Equipment Market Trends

Europe is an important region in the Specimen Processing Equipment Market due to its well-established healthcare systems, high-quality laboratory infrastructure, and strong regulatory frameworks. Countries such as Germany, France, and the UK maintain extensive networks of public and private clinical laboratories that perform millions of diagnostic tests annually. For instance, the German Federal Statistical Office reports that in 2022, over 2 billion laboratory tests were conducted across hospitals and outpatient facilities, highlighting the critical role of specimen processing equipment. Similarly, NHS England data show that routine blood tests and pathology services handle millions of patient samples weekly, demonstrating high equipment utilization and the region’s reliance on accurate, efficient laboratory workflows.

Asia Pacific Specimen Processing Equipment Market Trends

Asia Pacific is the fastest-growing region in the Specimen Processing Equipment Market due to rapid healthcare expansion, increasing diagnostic testing, and rising demand for laboratory automation. For example, India’s Ministry of Health and Family Welfare reported over 1.2 billion diagnostic tests conducted in 2022 across hospitals and laboratories, reflecting enormous sample volumes requiring efficient processing. Similarly, China’s National Health Commission indicates that tens of thousands of laboratories handle hundreds of thousands of patient samples daily, driven by population size and growing disease burden. Government initiatives to expand hospital capacity, upgrade lab infrastructure, and implement automated workflows further accelerate demand for specimen processing equipment throughout the region.

Market Competitive Landscape

Leading companies in the Specimen Processing Equipment Market focus on accuracy, safety, and efficiency, developing automated and integrated systems for clinical, research, and diagnostic labs. Investments in R&D enhance workflow efficiency, sample integrity, and processing speed, while collaborations with hospitals and regulatory bodies ensure reliability, driving adoption, innovation, and growth across the global specimen processing equipment market.

Key Industry Developments:

- In March 2025, Beckman Coulter announced that the DxC 500i Clinical Analyzer received FDA clearance. The system, an integrated platform combining clinical chemistry and immunoassay testing, was designed to streamline laboratory workflows, improve testing efficiency, and enhance diagnostic accuracy. The approval allowed laboratories to deploy the analyzer for routine clinical testing, supporting faster, more reliable patient results.

- In February 2025, Thermo Fisher Scientific continued its investment in food PCR testing, strengthening its portfolio for rapid and accurate detection of foodborne pathogens. The company expanded resources for research, development, and deployment of PCR-based solutions, enhancing food safety testing capabilities across laboratories and production facilities globally. This move aimed to improve detection speed, reliability, and regulatory compliance in the food industry.

Companies Covered in Global Specimen Processing Equipment Market

- Thermo Fisher Scientific

- Beckman Coulter

- Qiagen

- Andreas Hettich

- Roche Diagnostics

- Eppendorf

- Sigma Zentrifugen

- Becton, Dickinson and Company

- Copan Diagnostics

- Haier Biomedical

- Telstar

- LabTech

- Martin Christ

- Autobio

- A&T Corporation

- Others

Frequently Asked Questions

The global Specimen Processing Equipment Market is projected to be valued at US$ 2.3 Bn in 2026.

Rising laboratory automation, increasing diagnostic tests, research growth, and demand for accurate, high-throughput workflows drive the market.

The global Specimen Processing Equipment Market is poised to witness a CAGR of 8.1% between 2026 and 2033.

Opportunities include fully automated systems, AI integration, emerging markets expansion, biobanking growth, and workflow optimization innovations.

Thermo Fisher Scientific, Beckman Coulter, Qiagen, Andreas Hettich, Roche Diagnostics, Eppendorf.