- Renewable Energy

- Solar Energy Market

Solar Energy Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Solar Energy Market By Technology (Photovoltaic (PV) Systems, Concentrated Solar Power (CSP) Systems), Module Type (Monocrystalline, Polycrystalline, Amorphous Silicon, Others), Application (Residential, Utility-scale, Commercial, Industrial, Others), and Regional Analysis for 2025 - 2032

Solar Energy Market Share and Trends Analysis

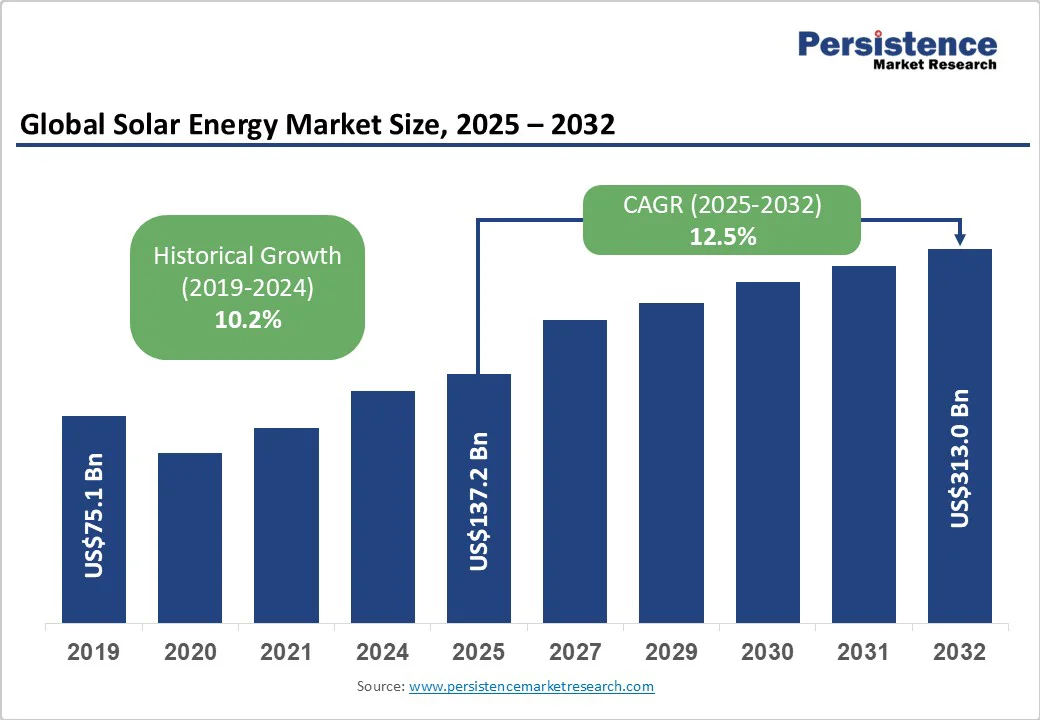

The global solar energy market size is likely to be valued at US$ 137.2 Billion in 2025 and is estimated to reach US$ 313.0 Billion by 2032, growing at a CAGR of 12.5% during the forecast period 2025-2032, driven by rising environmental concerns and increasing installation of renewable energy systems by governments, alongside rapid technological advancements that improve efficiency and reducing costs of solar power.

Key Industry Highlights

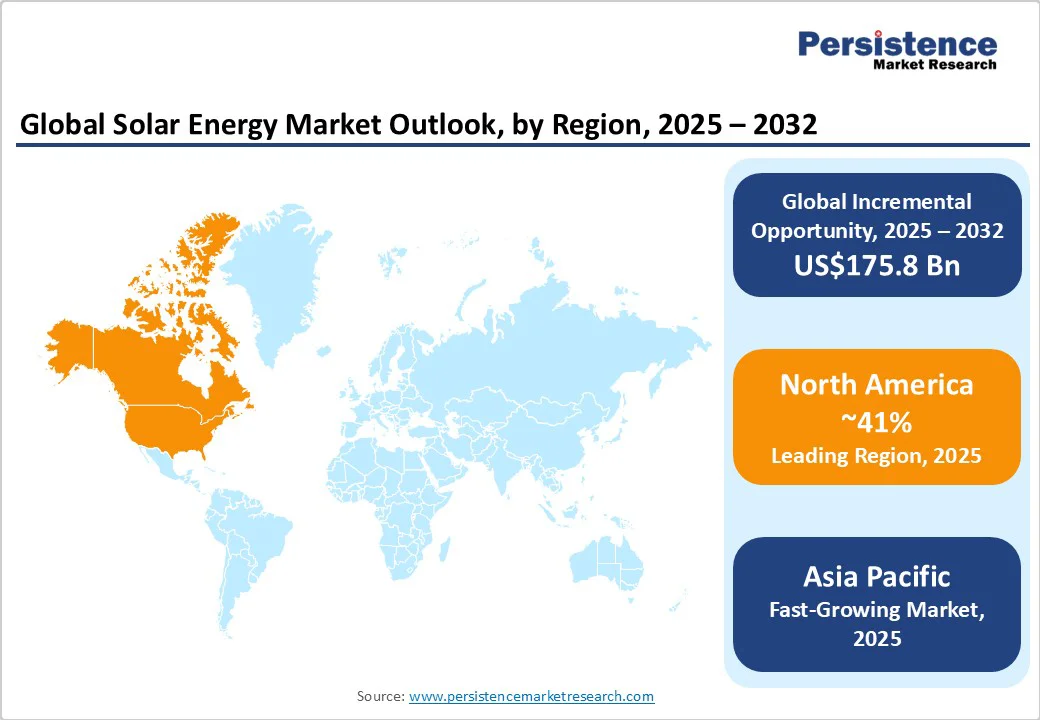

- Dominant Region: North America is expected to command about a 41.3% market share in 2025, supported by regulatory incentives and innovation ecosystems.

- Fastest-growing Region: Asia Pacific is forecasted to grow at the highest CAGR of approximately 14.0% from 2025 to 2032, led by China and India’s expansive renewable policies and manufacturing capacity.

- Leading & Fastest-growing Technologies: Photovoltaic systems will dominate with a market share of more than 70.0% in 2025, while concentrated solar power will be the fastest-growing segment, expanding at about 13.2% CAGR through 2032.

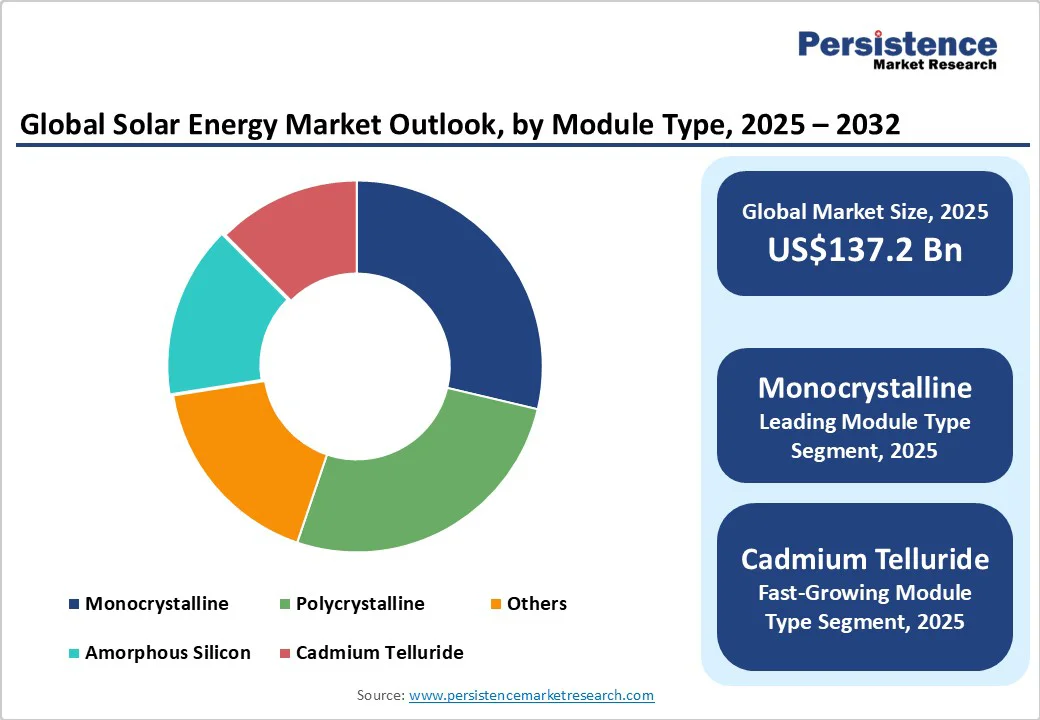

- Leading & Fastest-growing Module Types: Monocrystalline modules are slated to lead with a 28.7% market share in 2025; solar modules made from perovskite and cadmium telluride technology are anticipated to register growth rates exceeding 15.0% during 2025-2032.

- Market concentration is high, with the top 10 players holding roughly 65.0% of revenue, emphasizing integration, technological leadership, and geographic expansion.

- June 2025: South African independent power producer NOA secured financing for its 349 MW Khauta South Solar PV project near Welkom, marking it as the country’s largest single-asset solar facility with a combined capacity of 506 MW.

| Key Insights | Details |

|---|---|

|

Solar Energy Market Size (2025E) |

US$137.2 Bn |

|

Market Value Forecast (2032F) |

US$313.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Drive - Rising Demand for Renewable Energy and Technology-driven Efficiency Gains

Governments worldwide are advancing ambitious renewable energy targets aligned with global climate commitments such as the Paris Agreement. Countries, including the U.S., China, Germany, and India, have introduced substantial renewable energy quotas supported by incentives, tax benefits, and feed-in tariffs. These policies are accelerating solar adoption across sectors, particularly in residential and commercial spaces, where reducing carbon footprints is increasingly tied to corporate ESG goals and shifting consumer preferences. According to the International Energy Agency (IEA), renewables contributed around 29.0% of global electricity production in 2024, with solar PV emerging as the fastest-growing source. Global energy transition strategies also aim to cut CO? emissions by up to 30.0% by 2030 through solar integration.

Ongoing R&D in solar technologies, such as perovskite solar cells and advanced thin-film panels, is boosting system efficiency while lowering costs. Monocrystalline silicon panels, offering 15.0%–20.0% efficiency, outperform older technologies and are becoming more widespread. At the same time, companies such as First Solar, JinkoSolar, and Canadian Solar are expanding vertically integrated manufacturing operations, driving economies of scale. These advancements lower capital costs and shorten payback periods, making solar more viable in cost-sensitive markets. Industry projections estimate annual solar cost reductions of 3.0%–5.0% through 2032, solidifying solar’s role in the global energy mix.

Restraint - Extensive Initial Capital Investment and Long Payback Periods

High upfront investment remains a significant barrier to wider solar energy adoption, particularly for residential and small commercial users. Utility-scale projects also require capital-intensive infrastructure—including solar panels, mounting systems, electrical components, and compliance costs, leading to extended payback periods of 5 to 10 years or more. In residential settings, installation costs can exceed US$15,000, making subsidies, tax incentives, and accessible financing essential. Limited access to affordable funding, especially in emerging markets, further restricts adoption. Additionally, regulatory uncertainties and grid integration challenges introduce risk premiums that impact investor confidence. These financial hurdles highlight the need for continued policy support and innovative financing solutions such as green bonds, leasing models, and performance-based incentives.

Compounding these issues is the concentration of solar panel manufacturing in China, which controls around 70.0% of global capacity. This creates supply chain vulnerabilities linked to geopolitical tensions, trade restrictions, and pandemic-related disruptions. Production slowdowns in key Chinese provinces have caused delays in shipments, affecting installation schedules and project execution. Moreover, fragmented permitting processes, fluctuating tariffs, and inconsistent net metering policies across countries add complexity and risk for developers. Delays in grid access and regulatory unpredictability impact project margins and timelines. Addressing these supply and policy-related challenges through diversification and harmonized standards is critical for maintaining solar market growth.

Opportunity - Massive Energy Demand in Asia Pacific

Asia Pacific, led by China, India, and ASEAN nations, is marked by significant unmet energy needs and supportive government policies. China’s plan to build 450 GW of renewable capacity in desert regions and India’s rapid solar adoption underline a massive opportunity set exceeding US$80 Billion through 2032. Increasing electrification, urbanization, and industrialization in developing economies are propelling demand for decentralized and large-scale solar installations. Additionally, improving grid infrastructure and renewable integration policies are catalyzing private-sector investments, generating highly lucrative opportunities in the region.

The integration of solar energy with advanced technologies such as artificial intelligence (AI), big data analytics, Internet of Things (IoT), and distributed ledger systems is unlocking enhanced operational efficiencies and asset management capabilities. AI-driven forecasting improves solar power predictability, reducing intermittency concerns and optimizing maintenance schedules, which reduces operational expenditures. For example, U.S. Department of Energy investments exceeding US$7 Million are funding AI-powered solar diagnostics to enhance performance. These convergent technologies have the potential to open pathways to new business models, including peer-to-peer energy trading, dynamic pricing, and automated grid balancing.

Category-wise Analysis

Technology Insights

Photovoltaic (PV) systems are slated to maintain a dominant position in the market, with an estimated 2025 share exceeding 70.0%. This leadership is attributed to the modularity, ease of installation, and versatile applications of PVs, spanning residential rooftops to large utility-scale solar farms. The steadily declining levelized cost of electricity (LCOE) for PV systems, now averaging below US$0.03 per kWh in many markets, is boosting adoption in price-conscious regions.

Meanwhile, concentrated solar power (CSP) systems, despite commanding a smaller share, are projected to exhibit the fastest growth with a 2025-2032 CAGR of approximately 13.2%. The primary merit of CSP, notably thermal energy storage facilitating power dispatchability, is catalyzing the adoption of these systems in regions with high direct normal irradiance. Hybrid solutions integrating CSP and PV are gaining attention to enhance grid reliability and firm renewable supply, expanding CSP’s market potential.

Module Type Insights

Monocrystalline silicon modules hold the highest revenue share, estimated to reach 28.7% in 2025, due to their superior efficiency, durability, and increasing affordability. Polycrystalline modules command a significant share attributed to lower production costs and acceptable performance in moderate climates.

Emerging thin-film technologies such as cadmium telluride and amorphous silicon cells represent the fastest-growing segments, forecasted to expand at CAGR rates between 15.0% and 17.0% through 2032. The advantages of these modules have been proven in lightweight, flexible applications and potential for building integration (BIPV), driving interest from architectural and commercial sectors. Continuous investments in R&D and scaling manufacturing capacity are expected to improve yields and reduce deployment costs, enhancing market penetration.

Application Insights

The residential application segment currently leads with an approximate 33.4% market share in 2025, aided by government incentives, increased consumer environmental awareness, and regulatory mandates promoting rooftop solar installations. This segment is expected to sustain growth backed by smart home integration trends and financing innovation such as solar leases and power purchase agreements.

Conversely, the utility-scale application segment is the fastest-growing, anticipated to achieve a 13.5% CAGR between 2025 and 2032. This expansion is propelled by large infrastructure investments, energy transition policies focusing on grid decarbonization, and the declining costs of utility-scale solar systems. The commercial and industrial sectors are progressively incorporating solar to advance sustainability goals and manage operational costs, although growth rates vary by geography and regulatory frameworks.

Regional Insights

North America Solar Energy Market Trends

North America is likely to command a significant portion of the solar energy market share at approximately 41.3% in 2025, following the U.S. The U.S. is boosting solar investments through mechanisms such as the Investment Tax Credit (ITC) and state-level Renewable Portfolio Standards (RPS).

Technological innovation hubs in regions such as California and Texas support R&D advancements in energy storage, grid modernization, and smart technologies, enhancing solar integration and customer engagement. The regional solar market is forecasted to expand at a CAGR of approximately 9.5% from 2025 to 2032, supported by recent federal infrastructure bills allocating over US$1 Trillion to clean energy initiatives. The competitive landscape features vertically integrated companies and innovative service providers leveraging financing models that accelerate residential and commercial solar adoption.

Europe Solar Energy Market Trends

Europe is likely to hold around 22% share in 2025, with Germany, the U.K., France, and Spain as key contributors. The Green Deal and Fit for 55 climate packages of the European Union (EU) have harmonized renewable energy regulations, catalyzing solar deployment across member states. National incentive schemes, carbon pricing, and green certificates create conducive conditions for utility-scale as well as decentralized solar projects.

The Europe solar energy market, expected to showcase a CAGR of about 8.7% from 2025 to 2032, is driven by increasing corporate sustainability targets and consumer demand for clean energy solutions. Investments in grid flexibility, cross-border electricity trading, and energy storage enable higher solar penetration and system reliability. Strategic collaborations between utilities, tech firms, and financiers are prevalent, reflecting the prioritization of energy transition and market integration across the continent.

Asia Pacific Solar Energy Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing solar energy market globally, accounting for an estimated 36% share in 2025. China leads the regional surge with ambitious renewable capacity targets exceeding 450 GW, supported by robust manufacturing ecosystems and policy incentives. India is rapidly expanding solar installations under its National Solar Mission, powered by energy access needs and industrial growth.

Countries in ASEAN are gaining momentum through favorable regulatory reforms and foreign direct investments, leveraging competitive manufacturing costs. The regional market is projected to grow at a CAGR exceeding 14.0% through 2032 due to the meteorically rising demand for electricity, government infrastructure spending, and private-sector innovation. Increasing rural electrification, coupled with urban sustainability programs, further broadens adoption. The competitive landscape features a mix of global leaders and agile local players scaling manufacturing and deployment to exploit market opportunities.

Competitive Landscape

The global solar energy market structure is moderately concentrated, dominated by leading players such as Canadian Solar, SolarEdge Technologies, SunPower Corporation, First Solar, Inc., Enphase Energy, Hanwha Q CELLS, JinkoSolar, and Trina Solar. These companies collectively capture an estimated 60.0%-70.0% market share due to their integrated operations, extensive R&D, expansive manufacturing capacities, and geographically diversified sales channels.

Market structure demonstrates a mix of vertical integration strategies and strong supply chain governance by major firms, which helps mitigate raw material and component volatility. Fragmentation remains in smaller regions or niche segments, led by local and emerging players focusing on specific technologies or markets. Competitive positioning is evolving around technology innovation, cost optimization, and service quality to meet increasing customer expectations and regulatory compliance.

Key Industry Developments

- In October 2025, Norwegian solar firm Alotta raised NOK 63.5 Million (~US$6.4 Million) to boost international growth after securing a 15-year power purchase deal with Mowi Chile. This agreement will supply renewable energy to Mowi’s salmon farms in Los Lagos, advancing clean energy use in aquaculture.

- In September 2025, SolarEdge Technologies began international shipments of U.S.-made residential solar products to Australia, marking a key step in its global export plan. The company aims to expand to more markets and start exporting commercial and industrial products in Q4 2025, supporting its U.S. manufacturing initiative and rising demand for American-made solar technology.

- In August 2025, Indian Railways commissioned its first removable solar panel system between tracks at Banaras Locomotive Works, Varanasi, featuring 28 panels with 15 kWp capacity over 70 meters, an important step toward sustainable rail transport. Additionally, it launched a salt-loaded freight rake from Sanosara to Dahej to boost regional logistics and introduced India’s first Scott Transformer-based electric traction system on the Nagda–Khachrod section, enhancing railway electrification.

Companies Covered in Solar Energy Market

- Canadian Solar Inc.

- SolarEdge Technologies Inc.

- SunPower Corporation

- First Solar, Inc.

- Enphase Energy, Inc.

- Hanwha Q CELLS Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- Trina Solar Co., Ltd.

- JA Solar Holdings Co., Ltd.

- Yingli Green Energy Holding Company

- SkyPower Ltd.

- GCL-Poly Energy Holdings Limited

- REC Group

- LONGi Green Energy Technology Co., Ltd.

- Sunrun Inc.

Frequently Asked Questions

The solar energy market is projected to reach US$137.2 Billion in 2025.

Rising environmental concerns and increasing installation of renewable energy systems by governments worldwide are driving the solar energy market.

The solar energy market is poised to witness a CAGR of 12.5% from 2025 to 2032.

Rapid technological advancements in solar for improving efficiency, reducing costs of solar power, and a strong focus on manufacturing scale-up are key market opportunities.

Canadian Solar Inc., SolarEdge Technologies Inc., and SunPower Corporation are some of the key players in the solar energy market.