- Renewable Energy

- Utility Solar PV EPC Market

Utility Solar PV EPC Market Size, Share, and Growth Forecast, 2026 - 2033

Utility Solar PV EPC Market by Capacity (Up to 10 MW, 10–50 MW, 50–100 MW, 100 MW and above.), Project Type (Ground-Mounted Solar, Floating Solar, Agrivoltaic Solar, Misc.), Contract Type (Engineering, Procurement & Construction (Full EPC), Engineering & Procurement (E&P), Engineering & Construction (E&C)), Technology (Fixed Tilt Systems, Single‑Axis Tracking, Dual‑Axis Tracking, Bifacial Module Systems) and Regional Analysis for 2026 - 2033

Utility Solar PV EPC Market Size and Trends Analysis

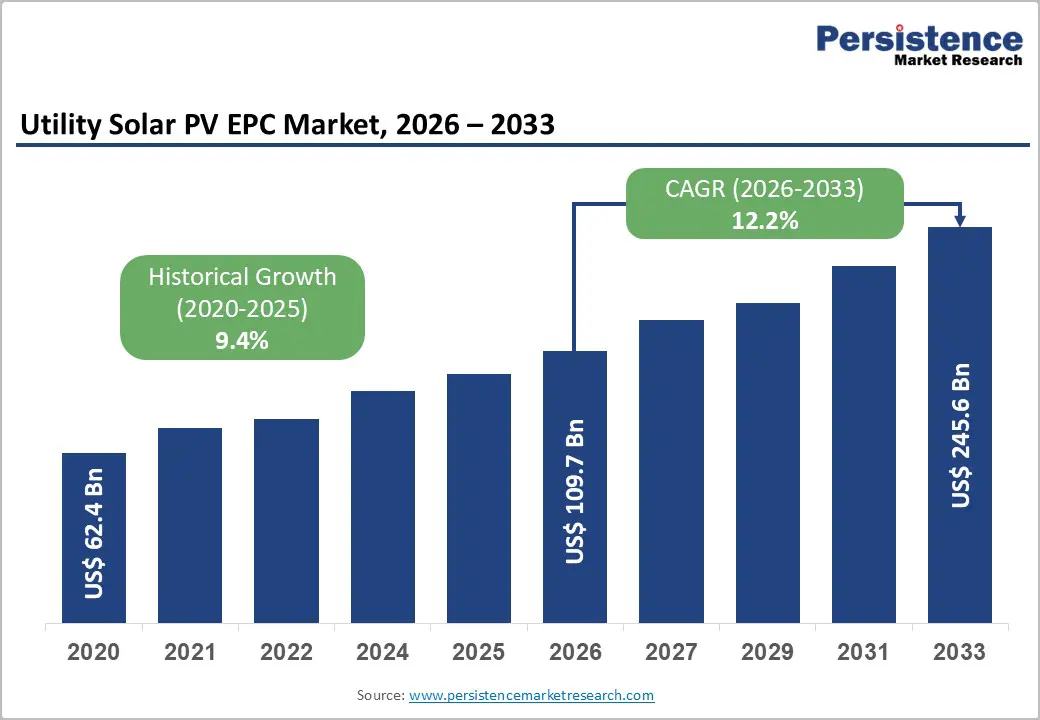

The global utility solar PV EPC market size is likely to be valued at US$ 109.7 billion in 2026 and is projected to reach US$ 245.6 billion by 2033, growing at a CAGR of 12.2 % between 2026 and 2033.

This robust expansion is primarily driven by aggressive renewable energy capacity deployment targets, declining solar component costs, improved project economics, and government mandates that are accelerating utility-scale infrastructure development across major economies. By 2033, the market positioning is projected to more than double from its 2026 baseline, underscoring the critical role of utility solar PV EPC services in global energy transition strategies and grid decarbonization initiatives.

Key Industry Highlights:

- Regional Leadership: Asia Pacific leads the Global Utility Solar PV EPC Market with 43% share, driven by massive utility-scale installations in China, strong state-backed solar programs, integrated module manufacturing ecosystems, and large domestic EPC contractors executing multi-GW projects annually.

- Emerging North American Hub: North America holds 26% share, supported by IRA tax credits, long-term PPAs, and accelerating utility and storage-coupled solar deployments across the U.S., creating strong pipelines for large EPC contracts.

- European Market Scenario: Europe accounts for 20% share, driven by decarbonization mandates, energy security goals post-gas crisis, and rapid expansion of ground-mounted and hybrid solar parks across Germany, Spain, and Southern Europe.

- Leading Project Type: Ground-Mounted Solar dominates with 74% share, benefiting from lower LCOE, faster construction timelines, and suitability for large multi-hundred-MW utility projects.

- Fastest-Growing Project Type: Floating Solar is the fastest-growing segment, supported by land scarcity, higher module efficiency from water-based cooling, and rising adoption across Asia and the Middle East.

- Leading Contract Type: Full Engineering, Procurement & Construction (Full EPC) commands 68% share, as developers prefer turnkey execution with single-contract accountability to reduce risk and optimize project delivery.

- Fastest-Growing Solution Trend: Solar-plus-Storage hybrid EPC projects are expanding fastest, driven by grid stability needs, peak-hour dispatchability, and growing corporate and utility demand for firm renewable power.

| Key Insights | Details |

|---|---|

|

Utility Solar PV EPC Market Size (2026E) |

US$ 109.7 Bn |

|

Market Value Forecast (2033F) |

US$ 245.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.4% |

Market Dynamics

Drivers - Government Renewable Energy Mandates and Capacity Addition Targets

National renewable energy policies and ambitious capacity installation targets constitute the primary growth catalyst for the Utility Solar PV EPC Market. According to the Ministry of New and Renewable Energy, India achieved a cumulative installed solar power capacity of 135,809.94 MW as of 31st December 2025, with 30,163.48 MW added during FY 2025 to 26 from April to December 2025 alone, including 2,961.70 MW commissioned in December 2025. This substantial deployment reflects the systematic execution of utility-scale solar projects predominantly delivered under EPC contracts to enable grid-connected solar power capacity across various regions. India's trajectory aligns with its target of achieving 500 GW of non-fossil energy capacity by 2030, requiring extensive involvement from EPC contractors to scale installations.

The European Union reached 269 GW of cumulative installed solar PV capacity by the end of 2023, representing over 2,500 times growth since the millennium, with projections indicating 401 GW of solar capacity additions between 2024 and 2028 to reach 671 GW by 2028. The EU Solar Strategy envisions 750 GW by 2030, with medium scenarios projecting up to 890 GW, creating sustained demand for comprehensive EPC services.

In the United States, the solar industry installed 11.7 GWdc in Q3 2025, marking a 20 % increase compared to Q3 2024, with utility-scale solar accounting for 9.8 GWdc, demonstrating a 26 % year over year increase. These government-backed deployment programs translate directly into systematic EPC contract opportunities across engineering, procurement, and construction phases, positioning the Utility Solar PV EPC Market as an indispensable enabler of national energy transition commitments.

Declining Solar Technology Costs and Enhanced Project Economics

The systematic reduction in solar component costs has fundamentally transformed project economics, accelerated utility-scale solar deployment and expanding the addressable market for EPC services. China's sustained investments exceeding US$ 50 billion in new manufacturing capacity over the past decade, coupled with supportive industrial policies, have driven solar PV costs down by over 80%, making solar the most affordable electricity generation technology in numerous markets.

In the United States, installed costs for utility-scale projects continued declining in 2023, with capacity-weighted averages decreasing 8% to US$ 1.43 per W compared to 2022, enhancing financial viability for new project development. This cost compression encompasses polysilicon, wafers, cells, and modules, where global manufacturing capacity exceeded demand by at least 100% by the end of 2021, creating competitive pricing dynamics. The favourable cost structure enables utility-scale solar projects to achieve a competitive levelized cost of electricity across diverse climate zones, strengthening power purchase agreement economics and attracting both public and private sector investments.

Eurostat data indicate the EU's renewable energy electrical capacity for wind and solar was three times higher in 2019 than in 2000, with solar photovoltaic capacity reaching 120,000 MW, driven substantially by improved cost competitiveness. For the Utility Solar PV EPC Market, declining equipment costs translate into larger project pipelines, accelerated commissioning timelines, and expanded geographic deployment as previously marginal projects achieve financial viability, thereby broadening the total addressable market for comprehensive EPC service providers capable of delivering projects within optimised cost and time parameters.

Large Scale Corporate Clean Energy Procurement and Data Centre Demand

Corporate sustainability commitments and exponential data center electricity requirements are emerging as substantial demand drivers for utility-scale solar capacity, directly benefiting the Utility Solar PV EPC Market. Research identifies data centers as a source of incremental utility-scale solar demand, projecting 3 % year over year growth in this segment for 2026, with 160 GW of large load requests currently under development in the United States. This corporate procurement trend reflects Fortune 500 companies establishing renewable energy purchasing agreements to meet carbon neutrality targets and environmental, social, and governance objectives.

The concentrated electricity requirements of data center operations, cloud computing infrastructure, and artificial intelligence training facilities create discrete, large-scale power demands ideally suited to dedicated utility solar installations. In China, distributed PV systems accounted for 51.1 GW of the 87.41 GW total new capacity added in 2022, with significant contributions from commercial and industrial sectors pursuing self-consumption models.

The GCC region witnessed major project financial closures, including the 2 GW Al Dhafra Solar PV project in Abu Dhabi valued at US$ 886 million, and Saudi Arabia's 1,500 MW Sudair Solar PV plant valued at US$ 924 million, alongside the US$ 8,400 million NEOM Green Hydrogen Plant combining solar and wind energy. These large-scale corporate and industrial procurements create sustained project pipelines for EPC contractors capable of executing complex utility-scale installations with guaranteed performance parameters, establishing a durable growth channel beyond traditional utility and government offtaker models.

Restraints - Supply Chain Concentration Risks and Material Availability Constraints

Geographic concentration of solar manufacturing capacity creates systemic vulnerabilities that constrain market expansion and introduce project execution risks. China currently dominates the global solar PV supply chain, controlling over 80 % of manufacturing stages, including polysilicon, ingots, wafers, cells, and modules, with 40 % of global polysilicon production concentrated in Xinjiang alone. This concentration creates potential bottlenecks, as evidenced by polysilicon prices quadrupling in recent periods despite global manufacturing capacity exceeding demand by at least 100 % by the end of 2021.

The residential solar segment in the United States experienced a 4 % decline in Q3 2025 installations year over year due to persistent module supply constraints, despite strong sales driven by tax credit incentives. Trade policy uncertainties, including foreign entity concerns and tariff implementations, further compound supply chain challenges, with recent actions resulting in a 4 % downgrade to distributed solar five-year outlooks. These material availability constraints force EPC contractors to extend procurement timelines, adjust project schedules, and absorb cost fluctuations, potentially delaying project commissioning and affecting contractual delivery commitments.

Opportunity - Integration of Solar Plus Storage Hybrid Systems

The convergence of solar generation with battery energy storage systems represents a transformative opportunity for the Utility Solar PV EPC Market to deliver enhanced value propositions beyond traditional generation-only projects. Solar plus storage integration enhances grid flexibility, enables dispatchability during peak demand periods, and improves overall project economics through participation in capacity markets and ancillary services.

In the United States interconnection queues, 571 GW or 53 % of the 1,085 GW solar pipeline was paired with battery storage at the end of 2023, with California ISO reaching 98 % storage pairing rates. The adoption of hybrid PV battery systems is becoming standard practice, allowing developers to secure more favourable power purchase agreements by guaranteeing energy delivery during high-value periods rather than variable solar production windows.

EPC contractors expanding expertise in integrated solar plus storage installations position themselves to capture substantial long-term opportunities across diverse geographies, particularly in markets relying on these solutions to improve grid stability and reduce dependence on imported fuels. Energy storage capacity in the United States grew by 14.9 GW alongside solar installations in 2025, with solar and storage combined representing 85 % of all new electricity-generating capacity additions. Markets in Africa, Asia, and island nations increasingly depend on solar plus storage EPC solutions for round-the-clock availability and enhanced reliability.

Corporate buyers pursuing captive solar projects similarly demand storage integration for an uninterrupted energy supply independent of grid conditions. For the Utility Solar PV EPC Market, this technology convergence creates differentiated service offerings requiring specialised engineering capabilities, expanded procurement relationships encompassing battery technologies, and integrated construction expertise, thereby establishing higher value contracts with extended project scopes and enhanced revenue potential per installation.

Emerging Market Solar Infrastructure Expansion

Developing economies present substantial untapped growth opportunities as nations establish foundational solar infrastructure to meet electrification goals and reduce fossil fuel dependence. Africa's solar PV market is predicted to grow 42 % in 2025, with the continent expected to add 23 GW of new solar capacity by 2028, effectively more than doubling current installed capacity despite solar currently accounting for just 3 % of electricity generation against 60 % of the world's best solar resources. By 2025, 18 African countries are expected to install at least 100 MW of solar capacity each, compared to just two countries in 2024, demonstrating rapid market diversification.

The GCC region continues to make substantial investments, with the UAE accounting for nearly 70 % of total renewable investments between 2013 and 2022, targeting 44 % renewable capacity by 2050, supporting US$ 54 billion in energy sector investments by 2030. Saudi Arabia is ramping up investments with multiple renewable energy auction rounds scheduled, while Bahrain, Kuwait, Oman, and Qatar advance their renewable energy initiatives.

These emerging markets create opportunities for EPC providers to establish early mover advantages, develop local partnerships, and scale operations across multiple high-growth geographies. However, scaling access to low-cost finance remains essential, as capital costs in Africa run 3 to 7 times higher than in developed countries, with the region currently receiving only 3% of global energy investments.

Innovative financing mechanisms and private sector involvement will be crucial for unlocking Africa's vast solar potential and translating project pipelines into commissioned capacity. For the Utility Solar PV EPC Market, emerging market expansion requires adapted business models addressing local content requirements, technology transfer expectations, and financing coordination capabilities, positioning specialised contractors to capture first mover advantages as these markets transition from nascent to mature solar deployment phases with sustained multi-decade growth trajectories.

Category-wise Analysis

Capacity Insights

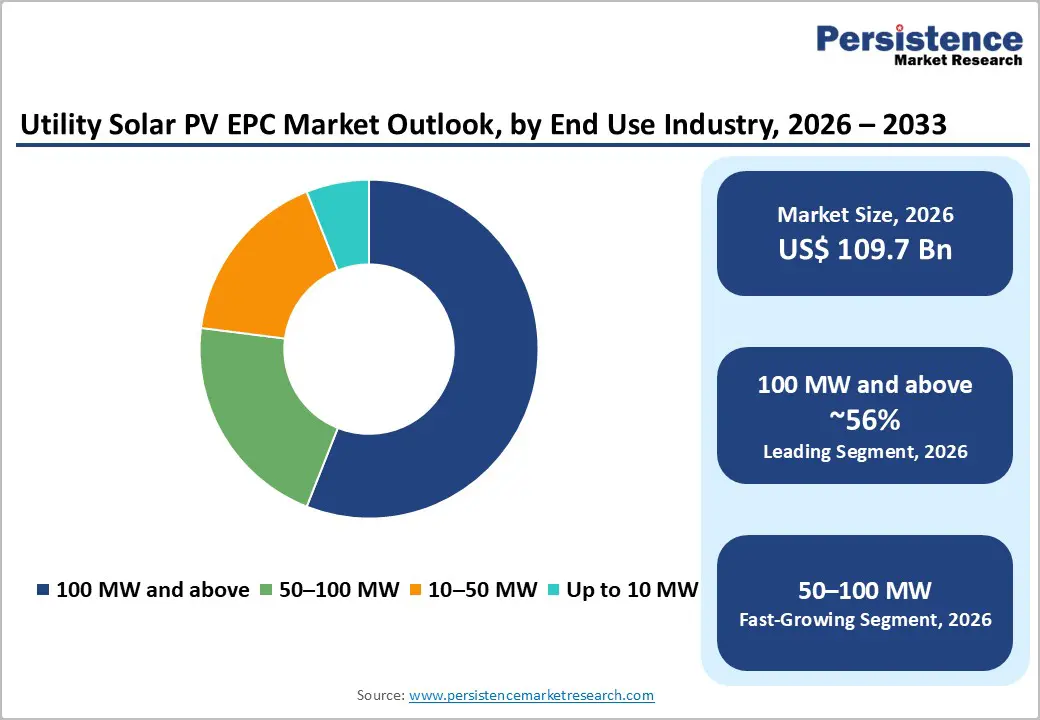

The 100 MW and above capacity segment dominates the utility solar PV EPC market, accounting for 56.3% share in 2026, reflecting the economies of scale advantages, competitive electricity pricing through large-scale power purchase agreements, and utility sector preference for consolidated generation assets. This segment benefits from sophisticated EPC capabilities, including large-scale procurement reducing per-unit equipment costs, complex construction logistics, managing extensive labour and material flows, grid interconnection expertise navigating high voltage transmission requirements, and comprehensive project financing coordination, accessing institutional capital markets. Utility-scale projects in this capacity range demand end-to-end EPC capabilities from design engineering through commissioning, with proven track records essential for securing major contracts.

In the United States, utility-scale solar installed 9.8 GWdc in Q3 2025, demonstrating 26 % year over year growth and 68 % quarter over quarter growth, with individual projects ranging from tens to hundreds of megawatts. India's capacity additions of 2,961.70 MW in December 2025 alone reflect the sustained deployment of large utility-scale projects executed under EPC contracts. The segment's dominance positions it as the primary revenue driver for major EPC contractors with established execution capabilities and balance sheet strength.

The 50 to 100 MW segment represents the fastest growing capacity category, capitalising on the intersection of utility-scale economies and accelerated permitting timelines compared to larger installations. This capacity range offers an optimal balance between project economics, grid integration requirements, and development timeline efficiency, making it attractive for both traditional utilities and corporate offtakers pursuing dedicated generation assets. Projects in this segment require substantial EPC capabilities yet face less complex interconnection requirements than 100 MW-plus installations, enabling faster progression from financial close to commercial operation.

Project Type Insights

Ground-mounted solar holds approximately 74% market share in 2026, establishing its position as the dominant project configuration for utility-scale installations due to site optimisation flexibility, proven installation methodologies, and cost-effective deployment across diverse terrain conditions. Ground-mounted configurations enable systematic orientation and tilt optimization, maximizing annual energy production, straightforward construction sequences supporting rapid deployment, and established supply chains for racking and mounting systems. This project type accommodates both fixed tilt and tracking systems, with single-axis tracking becoming prevalent in utility-scale deployments to enhance capacity factors.

The United States saw significant adoption of tracking systems, with this technology deployed across the majority of new utility-scale capacity to maximise generation profiles. India's 30,163.48 MW of solar capacity added during FY 2025 to 26 predominantly utilised ground-mounted configurations across various regions. The segment's market leadership reflects its suitability for large-scale utility procurement, compatibility with existing grid infrastructure planning, and EPC contractor operational familiarity, enabling efficient project execution within established cost and timeline parameters.

Floating Solar represents the fastest growing project type segment, driven by land use optimisation imperatives, water surface availability across reservoirs and industrial facilities, and performance advantages from evaporative cooling enhancing panel efficiency. Major installations include reservoir-based projects across the Asia Pacific, where land availability constraints make water surface deployment economically advantageous compared to terrestrial alternatives. The GCC region progressed notable floating solar projects in Oman and Qatar with investments of US$ 460 million and US$ 517 million, respectively. Europe pursues innovative hybrid solar hydro projects leveraging existing water infrastructure for dual-purpose utilisation. At the same time, North America accelerates adoption at wastewater treatment plants and industrial ponds, supporting clean energy mandates.

Regional Insights and Trends

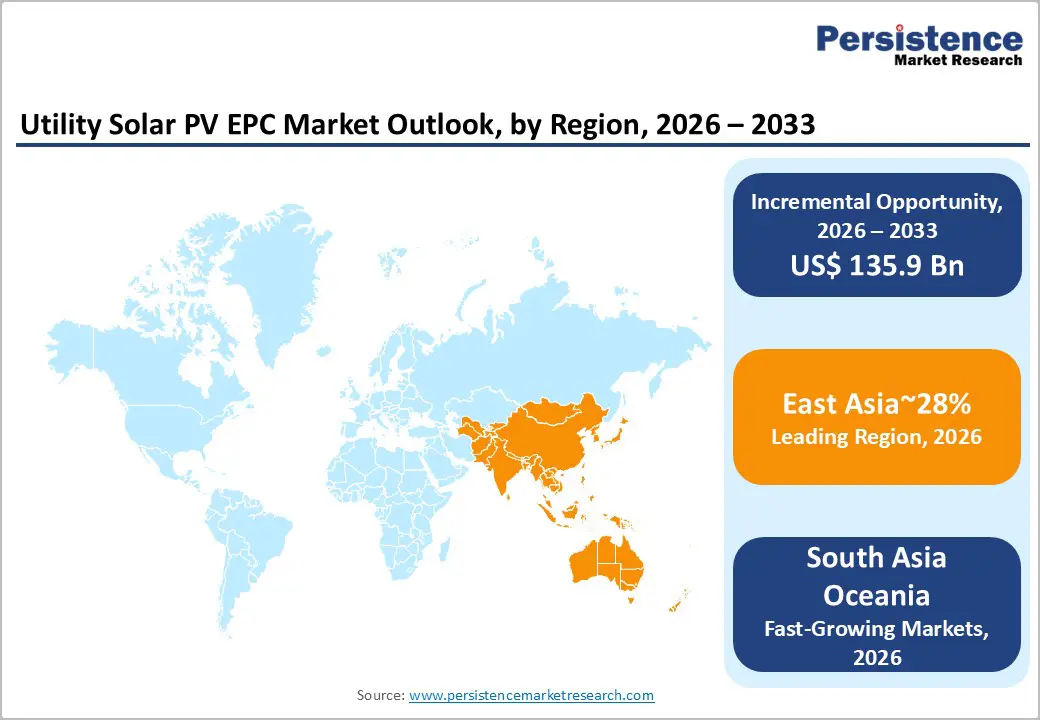

East Asia Utility Solar PV EPC Market Trends

East Asia commands approximately 28% of the global utility solar PV EPC market, with China as the dominant force in both manufacturing capacity and domestic installations. China saw significant growth in its photovoltaic market in 2022, installing 87.41 GW of new PV capacity with 51.1 GW from distributed systems and 36.3 GW from utility-scale projects, representing a substantial 59.3 % year over year increase. PV now contributes 5 % of China's total electricity consumption, up from 3.9 % in 2021, demonstrating rapid market penetration.

According to IEA projections, China's share in global PV manufacturing capacity is expected to increase significantly across modules, cells, wafers, and polysilicon production through 2030, with dominance in installations and cell production. China's sustained investments exceeding US$ 50 billion in new manufacturing capacity over the past decade, coupled with supportive industrial policies, have driven solar PV costs down by over 80 % globally. The country's solar PV exports totaled US$ 30 billion in 2021, representing 7 % of China's trade surplus over the previous five years. China's domestic market benefits from feed-in tariffs, green certificates, self-consumption policies, and incentives for building integrated PV and distributed systems, despite challenges including high module prices in certain periods and supply chain constraints.

North America Utility Solar PV EPC Market Trends

North America accounts for approximately 26% of the Global Utility Solar PV EPC Market, driven by federal and state-level renewable energy incentives, corporate clean energy procurement, and sustained utility-scale project deployment despite near-term policy uncertainties.

The United States solar industry installed 11.7 GWdc in Q3 2025, marking a 20 % increase compared to Q3 2024, with solar accounting for 58 % of all new electricity-generating capacity additions. The utility scale segment delivered 9.8 GWdc in Q3 2025, demonstrating 26 % year over year growth and 68 % quarter over quarter expansion. Cumulative installed utility-scale PV capacity surpassed 80.2 GWac across 47 states by 2023, with regional deployment concentrated in CAISO at 19 GWac, non-ISO Southeast at 17 GWac, and ERCOT at 15 GWac. The interconnection pipeline contained at least 1,085 GW of solar capacity at the end of 2023, with 571 GW or 53 % paired with battery storage, indicating substantial future deployment potential.

The region faces challenges, including module supply constraints impacting residential installations, Section 25D tax credit expiration creating demand uncertainty, and federal permitting risks, particularly for projects on federal lands. Trade policy uncertainties, including tariff implementations and foreign entity concerns, create additional headwinds, with recent actions resulting in a 4 % downgrade to distributed solar outlooks and potential delays for utility-scale projects with tight margins.

Europe Utility Solar PV EPC Market Trends

Europe accounts for approximately 20% of the global utility solar PV EPC market, driven by ambitious carbon neutrality targets, comprehensive renewable energy policies, and systematic capacity deployment across member states.

The European Union reached cumulative installed solar PV capacity of 269 GW across EU 27 Member States by the end of 2023, representing over 2,500 times growth since the introduction of Germany's feed-in-tariff law at the millennium. The EU surpassed 100 GW in 2018 and hit 200 GW in 2022, with projections indicating 401 GW of solar capacity additions between 2024 and 2028 to reach 671 GW by end of 2028 in the Medium Scenario, potentially exceeding 700 GW in the High Scenario. Solar PV market growth in the EU is expected to moderate with 5 % growth for 2024, followed by annual increases of 9 to 12 % until 2028, though the EU Solar Strategy envisions 750 GW by 2030 with the Medium Scenario projecting up to 890 GW.

National Energy and Climate Plans reflect this ambition, with several countries, including Poland, Ireland, and Lithuania, significantly increasing targets. The solar sector employed almost 650,000 people in the EU in 2022, with projections of 1 million jobs by 2025 and potentially 1.6 million by 2027 under High Scenario, reflecting strong job creation potential across manufacturing, installation, maintenance, and operations.

Competitive Landscape

The global utility solar PV EPC market is primarily fragmented, with a mix of large multinational companies and regional players competing for market share. Leading companies like First Solar, Canadian Solar, and Trina Solar dominate the market, leveraging economies of scale, technological advancements, and strong brand presence, especially in large-scale projects. Regional players such as ACME Solar, Sterling and Wilson have a strong foothold in emerging markets, where local expertise and cost competitiveness are crucial.

While the market is fragmented, there are oligopolistic tendencies in certain regions, where a few players control a large portion of the market share, particularly in key solar markets like India and China. The market remains highly competitive, with ongoing technological advancements and cost reductions driving the demand for top-tier EPC providers.

Key Developments:

- In 2025, First Solar announced plans to open a new 3.7GW manufacturing facility in the US by 2026. This new plant will primarily focus on the finishing of Series 6 modules, with production ramping up through 2027. The investment of approximately US$300 million aims to enhance domestic production, reduce tariffs, and improve profit margins by lowering logistics costs associated with importing finished goods. The facility will be crucial for meeting FEOC guidance and ensuring eligibility for the Section 45X manufacturing tax credits. This move underscores First Solar's strategy to increase its domestic manufacturing capacity while reducing reliance on overseas facilities, particularly in Vietnam and Malaysia, which have faced challenges in certain global markets.

- In 2025, Canadian Solar, through its subsidiary e-STORAGE, has successfully achieved commercial operation of the 220 MWh Mannum Battery Energy Storage Project in South Australia. As the EPC provider, e-STORAGE played a pivotal role in the engineering, procurement, and construction of this project, which will contribute to South Australia's grid stability and its goal of 100% renewable electricity generation by 2027. The project uses e-STORAGE's proprietary SolBank technology for safe, reliable, and high-performance operation. This development further strengthens e-STORAGE's position as a leading EPC provider in large-scale storage solutions, supporting the transition to clean energy in Australia.

Companies Covered in Utility Solar PV EPC Market

- First Solar

- Canadian Solar

- Trina Solar

- ACME Solar

- Sterling and Wilson

- Bharat Heavy Electricals Limited (BHEL)

- Larsen & Toubro Limited

- Power Construction Corporation of China (PCCC)

- Sungrow

- JUWI AG

- BELECTRIC

- KEC International Limited

- Tata Power Solar Systems Ltd.

- Risen Energy Co. Ltd.

- SunPower Corporation

Frequently Asked Questions

The global utility solar PV EPC market is projected to be valued at US$ 109.6 Bn in 2026.

The Ground-Mounted Solar segment is expected to account for approximately 74% of the global utility solar PV EPC market by project type in 2026.

The utility solar PV EPC market is expected to witness a CAGR of 12.2% from 2026 to 2033.

Utility Solar PV EPC Market growth is driven by government renewable energy mandates and capacity addition targets, declining solar technology costs, large-scale corporate clean energy procurement, and the growing demand from data centres and industrial sectors, all of which create sustained demand for comprehensive EPC services.

Key market opportunities in the utility solar PV EPC market include the integration of solar plus storage hybrid systems, which enhance grid flexibility and project economics by enabling dispatchability during peak demand. Emerging market solar infrastructure expansion, particularly in regions like Africa and the GCC, offers untapped growth potential, as these regions ramp up their solar capacity to meet electrification and renewable energy goals. These markets present opportunities for EPC providers to establish early mover advantages, develop local partnerships, and address financing challenges to support the transition from nascent to mature solar deployment stages.

Key players in the utility solar PV EPC market include First Solar, Canadian Solar, Trina Solar, ACME Solar, and Sterling and Wilson.