- Technology

- Smart Surveillance Camera Market

Smart Surveillance Camera Market Size, Share, and Growth Forecast, 2025 - 2032

Smart Surveillance Camera Market By Connectivity (Wired Cameras, Wireless Cameras, Others), Form Factor (Dome Camera, Bullet Cameras, Others), Feature (Motion Detection, Facial Recognition, Others), and Regional Analysis for 2025 - 2032

Smart Surveillance Camera Market Share and Trends Analysis

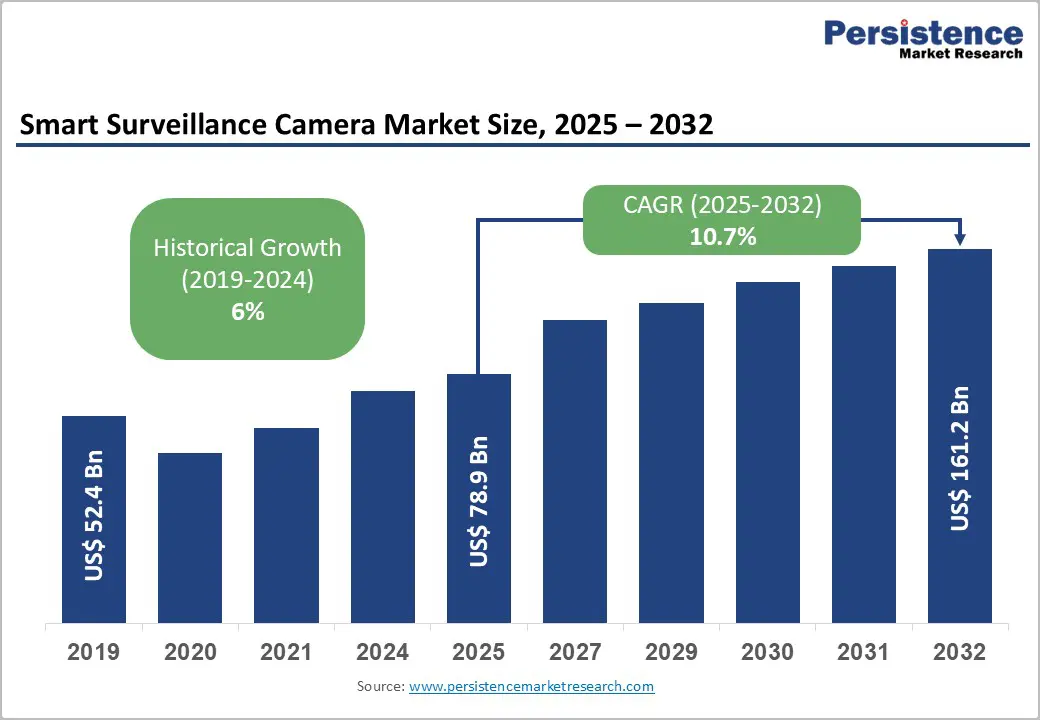

The global smart surveillance camera market size is likely to be valued at US$78.9 Billion in 2025 and is estimated to reach US$161.2 Billion by 2032, growing at a CAGR of 10.7% during the forecast period from 2025 to 2032, driven primarily by the widening adoption of AI-powered analytics, cloud-based Video Surveillance as a Service (VSaaS), and expansion of 5G-enabled cellular cameras.

Market expansion is fueled by technological innovation, rising demand for smart surveillance across residential, commercial, and critical infrastructure sectors, and increased investment in smart cities. Strengthening security regulations and growing adoption of intelligent video solutions by enterprises, governments, and smart homes further accelerate growth.

Key Industry Highlights

- Dominant Connectivity: Wired cameras hold 45% market share in 2025, whereas wireless cameras exhibit the fastest CAGR, fueled by smart home and cellular deployments.

- Leading Form Factors: Dome cameras command a 38% market share in 2025, with 360-degree fisheye cameras growing the fastest, due to increasing adoption in large venue surveillance.

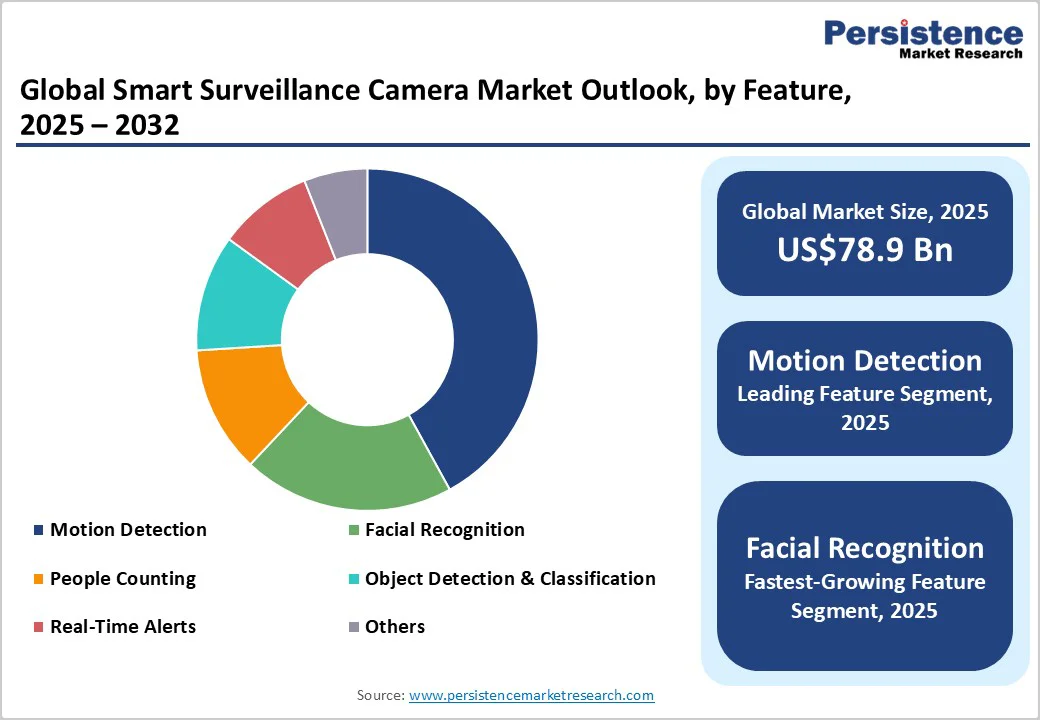

- Dominant Features: Motion detection analytics represent the largest installed base at about 42% in 2025, while facial recognition is the fastest-growing feature from 2025 to 2032.

- Regional Leadership: Asia Pacific leads regional market share with around 38%, and is also set to register the highest CAGR through 2032, driven by China’s manufacturing scale and India’s smart city initiatives.

- Regional Dynamics: North America holds a 27% share in 2025, supported by regulatory frameworks and R&D ecosystems, while the Europe market is driven by stringent regulations of the European Union (EU) and harmonized AI ethics legislation influencing market innovation.

- Industry Scenario: Prominent industry developments include major AI camera launches, significant acquisitions to augment analytics capability, manufacturing expansions in Southeast Asia, and VSaaS cloud partnerships enhancing operational scalability.

- September 2025: Bhubaneswar enhanced its surveillance infrastructure by installing 1,500 new AI-enabled CCTV cameras, spearheaded by Bhubaneswar Smart City Limited (BSCL), aiming to improve safety for women, children, and elderly citizens.

| Key Insights | Details |

|---|---|

| Smart Surveillance Camera Market Size (2025E) | US$78.9 Bn |

| Market Value Forecast (2032F) | US$161.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of AI-Powered Edge Analytics for Enhanced Real-Time Surveillance Efficacy

AI-powered edge analytics, embedded directly on camera devices, are revolutionizing the smart surveillance camera market by enabling real-time data processing at the source rather than relying solely on cloud-based analysis. This technological advancement reduces latency and bandwidth requirements while enabling features such as facial recognition, anomaly detection, and behavior analysis with increased accuracy.

The economic impact of edge AI deployment can prove significant, as it can potentially reduce cloud storage and bandwidth costs for video surveillance operators. This development is empowering verticals such as transportation and critical infrastructure, where real-time threat detection is essential, while also addressing privacy concerns by reducing raw video transmissions.

The adoption of edge analytics aligns with regulatory pressures from bodies such as the European Union (EU)’s General Data Protection Regulation (GDPR) and the U.S. Department of Homeland Security (DHS)’s cybersecurity frameworks, which emphasize data minimization and real-time monitoring.

As a result, companies integrating edge AI solutions position themselves to capture growing investments worth billions by 2030 in intelligent security management systems alone. Overcoming the challenge of deploying cost-effective yet powerful edge hardware is fostering strategic R&D collaborations between leading semiconductor firms and surveillance technology providers, further accelerating market growth.

Capex Challenges and Integration Complexity in Enterprise Deployments

While the adoption of smart surveillance cameras is expanding, enterprises face substantial capital expenditure (Capex) barriers, specifically related to the upgrading of legacy systems to advanced IP and AI-enabled infrastructures.

The integration complexity involves deploying compatible hardware, deploying and managing video management software (VMS), and ensuring cybersecurity compliance, which collectively elevate upfront costs by a sizable margin compared to analog CCTV systems.

Regulatory compliance with data privacy laws and cybersecurity frameworks imposes additional operational overhead and necessitates investments in secure networks and encrypted data handling. This complexity can deter small-to-medium enterprises (SMEs) from transitioning to smart surveillance solutions despite the favorable total cost of ownership over the long term.

Compounding this is the persistent global semiconductor shortage that has exacerbated hardware procurement delays and inflated costs, affecting timely project rollouts. These factors collectively constrain the pace of adoption, particularly in emerging markets where infrastructure modernization budgets are limited.

Rising Adoption of VSaaS Models in Emerging Markets Poised to Unlock Substantial Growth

Video Surveillance as a Service is rapidly gaining acceptance as an operational expenditure (Opex)-oriented alternative to traditional capital-intensive surveillance system deployments, especially in emerging markets such as Southeast Asia and Latin America.

This business model enables customers to access scalable cloud-hosted surveillance solutions via subscription, thereby lowering upfront costs and facilitating faster adoption in sectors with constrained financial resources.

The flexibility of VSaaS models also addresses unmet customer needs for centralized monitoring, multi-site management, and analytics-driven insights without significant IT infrastructure investments. This factor makes them particularly appealing for resource-starved SMEs and public sector organizations.

Government initiatives promoting smart city infrastructure and urban surveillance upgrades are providing strong policy backing to VSaaS proliferation. For instance, India’s Smart Cities Mission allocates dedicated funding for surveillance technology enhancements in urban areas.

Telecommunications advancements enabling cost-effective broadband access further fuel this opportunity. Providers embracing hybrid cloud-edge strategies with integrated AI analytics are poised to capitalize extensively on this emerging channel, with total addressable markets expected to surpass conventional hardware sales in the medium term.

Category-wise Analysis

Connectivity Insights

The wired cameras segment is anticipated to command approximately 45% of the smart surveillance camera market revenue share in 2025. This dominance is largely due to the established infrastructure of IP-based wired systems with PoE technology providing reliable power and data transmission over a single Ethernet cable.

Wired cameras are extensively deployed in large commercial buildings, government facilities, and transportation hubs, where infrastructure stability and uninterrupted video quality are critical. Their integration with video management software and enterprise security systems further cements their leadership.

Reduced latency and bandwidth capacity constraints of wired cameras compared to wireless alternatives ensure high-fidelity video transmission necessary for AI-powered analytics and forensic video use cases.

The wireless cameras segment is the fastest growing, driven by increasing consumer preference for flexible, easy-to-install security solutions in smart homes and small-to-medium business (SMB) environments where retrofitting wired systems is cost-prohibitive.

The proliferation of battery technology improvements and 4G/5G cellular connectivity is also enabling wireless smart cameras for remote or outdoor surveillance without reliance on fixed infrastructure. The rise of smart city projects in emerging economies further accelerates adoption in public spaces, where rapid deployment and scalability are vital.

Form Factor Insights

Dome cameras are poised to hold the largest market share at approximately 38% in 2025. Their popularity is rooted in their discreet appearance and versatile 360-degree viewing capabilities, which are ideal for retailers, commercial complexes, and government facilities focused on theft prevention and customer safety.

With enhanced AI features such as facial recognition and motion detection integrated, dome cameras are central to urban monitoring and critical infrastructure protection solutions. Their widespread adoption is underpinned by growing demand for non-intrusive surveillance solutions capable of delivering panoramic coverage through fewer installations, thereby reducing overall project costs.

The fastest-growing segment for the forecast period 2025 - 2032 is the 360-degree fisheye camera. Technological advances in multi-sensor integration and image stitching algorithms have improved visual clarity and minimized distortions, making fisheye cameras increasingly attractive in large venues such as airports, stadiums, and city squares.

These cameras considerably reduce blind spots, providing comprehensive coverage from a single unit, which translates to cost savings in hardware and installation labor. The surge in this segment is informed by evolving use cases requiring seamless wide-area monitoring and centralized video analytics, coupled with supportive government smart city initiatives deploying panoramic surveillance networks.

Feature Insights

Motion detection functionalities currently dominate with an estimated 42% share of camera installations in 2025. This foundational feature provides intelligent event-triggered recording and alerts, significantly reducing manual monitoring resources and bandwidth utilization. It is ubiquitously integrated into mid-range and entry-level smart surveillance cameras, serving as the first line of automated security response in both residential and commercial spheres.

Facial recognition stands out as the fastest-growing feature, with an anticipated CAGR from 2025 to 2032. Its growth is propelled by enhanced accuracy through deep learning algorithms and broader acceptance in regulated environments such as airports, banks, and government facilities requiring heightened identification and access control capabilities.

Recent innovations in bias mitigation and ethical AI frameworks have also alleviated regulatory and societal concerns, enabling broader deployment. The ability of this feature to integrate with demographic analytics and VIP identification systems is expanding its use beyond security into marketing and operational analytics, offering new monetization avenues for smart surveillance providers.

Regional Insights

North America Smart Surveillance Camera Market Trends

North America is driven predominantly by the U.S. The market here benefits from a mature regulatory environment, including the California Consumer Privacy Act (CCPA) and federal cybersecurity frameworks, which influence adoption patterns and favor cameras with integrated encryption, edge AI analytics, and privacy-first design.

The U.S. innovation ecosystem fosters advanced R&D in AI and 5G technology integration, leading to early commercialization of edge-enabled cameras and VSaaS models suited to enterprise and public-sector needs.

Investment flows are heavily concentrated in smart city programs and critical infrastructure upgrades, including transportation security enhancements and emergency response systems modernization.

Competitive dynamics in North America show consolidation among hardware players alongside software and cloud service firms, creating robust ecosystems. Investment prospects are strong in innovative cybersecurity surveillance solutions that combine AI-driven threat detection with automated compliance reporting.

Europe Smart Surveillance Camera Market Trends

Germany, the U.K., France, and Spain are leading the Europe market. The region’s regulatory environment is shaped by the EU GDPR and the upcoming AI Act, imposing strict controls on data privacy and the use of AI in surveillance.

These laws have shaped market preferences toward edge analytics and privacy-preserving technologies, limiting data centralization. Germany leads in manufacturing excellence and industrial surveillance adoption, while France demonstratea rapid urban surveillance modernization supported by massive EU smart city funding. Spain follows with the growing deployment of local surveillance systems integrated with public safety networks.

The competitive landscape is fragmented due to a mix of established multinational manufacturers and niche AI analytics startups specializing in ethical AI compliance. Investment activity is the strongest in merging traditional video surveillance with emerging smart analytics platforms, spurred by government-backed innovation programs supporting AI adoption for public safety.

Asia Pacific Smart Surveillance Camera Market Trends

Asia Pacific is expected to be the largest and fastest-growing regional market from 2025 to 2032. China holds dual dominance as the leading consumer and manufacturer, with an estimated US$18 Billion surveillance camera market in 2025, primarily driven by extensive smart city deployments and stringent public security requirements enforced by national policies.

Japan emphasizes AI advancements and automation in surveillance, contributing to high technology adoption rates. India’s market growth is propelled by the Smart Cities Mission, allocating over US$7 Billion toward urban surveillance infrastructure by 2026, as well as growing private sector investments in the retail and hospitality sectors.

ASEAN countries benefit from lower-cost imports and increasing awareness of VSaaS models, enabling scalable surveillance deployments across expanding urban and industrial centers.

Diversified regulatory maturity across the region provides opportunities for manufacturers and service providers to customize solutions aligned with local privacy and data protection laws. Investment trends emphasize infrastructure expansion, affordable smart solutions for SMEs, and increased participation by cloud service providers offering hybrid cloud-edge security platforms.

Competitive Landscape

The global smart surveillance camera market landscape exhibits moderate consolidation, with the top five players controlling an estimated 55% market revenue share in 2025.

Dominant companies such as Hikvision Digital Technology, Dahua Technology, Axis Communications, Hanwha Vision (formerly Hanwha Techwin), and Bosch Security Systems leverage their R&D capabilities, expansive product portfolios, and global distribution networks to sustain market leadership. These firms compete intensely on technological innovation, AI analytic capabilities, and scalability of cloud-based offerings.

While hardware components witness consolidation, the broader surveillance ecosystem, especially software and VSaaS segments, remains fragmented with numerous niche firms disrupting traditional models through vertical-specific intelligence solutions and specialized analytics.

Competitive positioning strongly favors integrated platform offerings combining cloud storage, AI analytics, and cybersecurity features, with ongoing strategic acquisitions and partnerships aimed at expanding service breadth and geographic reach.

Key Industry Developments

- In September 2025, Alarm.com launched the ADC-V516, an affordable indoor Wi-Fi camera with 1080p HDR video, AI-based detection of people, animals, and vehicles, and two-way audio. It integrates seamlessly with Alarm.com’s professional ecosystem, supporting cloud or onboard recording, proactive deterrence, Visual Verification, and Remote Video Monitoring for faster, more accurate responses.

- In August 2025, Xiaomi launched the upgraded Smart Camera 4C in China with a 6 MP sensor, AI-enhanced night vision, Wi-Fi 6, human and pet detection, and movement tracking. It features encryption, a physical lens cover, 360°/116° viewing, and supports cloud, NAS, and microSD storage.

- In May 2025, Synology launched C2 Surveillance, a cloud-based VSaaS platform enabling fast, serverless deployment and unlimited camera additions without licensing fees. It offers AI-powered detection, edge recording to microSD for continuity, and centralized multi-site management with AD integration, role-based permissions, and a low-bandwidth mode that cuts usage by up to 50%.

Companies Covered in Smart Surveillance Camera Market

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Axis Communications AB

- Hanwha Techwin Co., Ltd.

- Bosch Security Systems

- Panasonic Corporation

- FLIR Systems, Inc.

- Honeywell International Inc.

- Avigilon Corporation (Motorola Solutions)

- VIVOTEK Inc.

- Pelco, Inc. (Schneider Electric)

- Canon Inc.

- Hanwha Vision

- Uniview Technologies Co., Ltd.

Frequently Asked Questions

The global smart surveillance camera market is projected to reach US$78.9 Billion in 2025.

The widening adoption of AI-powered analytics, cloud-based VSaaS, and expansion of 5G-enabled cellular cameras, and an increasing demand for smart surveillance solutions across residential, commercial, and critical infrastructure sectors are driving the market.

The smart surveillance camera market is poised to witness a CAGR of 10.7% from 2025 to 2032.

Heightening investments in smart city projects, evolving security regulations, growing awareness of the role played by surveillance in operational efficiency and public safety, and increasing penetration of smart homes are key market opportunities.

Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., and Axis Communications AB are some of the key players in the smart surveillance camera market.