- Advanced Materials

- Smart Coatings Market

Smart Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Smart Coatings Market by Function (Anti-Corrosion, Self-Cleaning, Others), End-use Industry (Building & Construction, Marine, Others), Layer, and Regional Analysis for 2026 - 2033

Smart Coatings Market Size and Trends Analysis

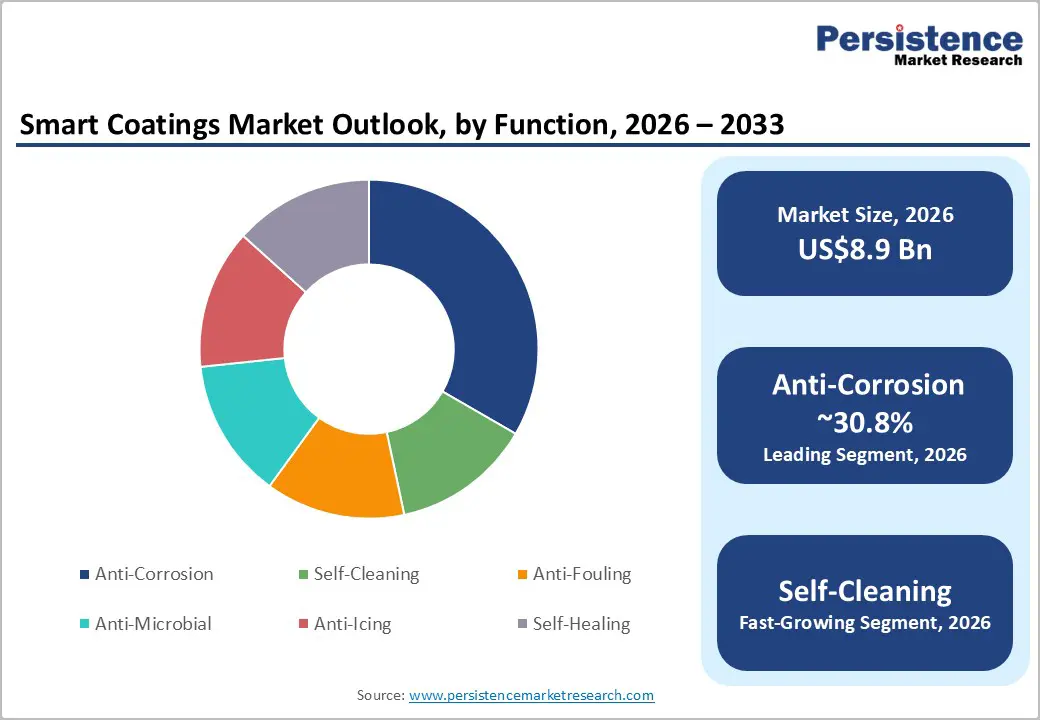

The global smart coatings market size is likely to be valued at US$8.9 billion in 2026 and is expected to reach US$34.0 billion by 2033, growing at a CAGR of 21.1% between 2026 and 2033, driven by increasing demand for corrosion protection, low-maintenance surfaces, and multifunctional coating systems across marine, infrastructure, automotive, aerospace, and industrial sectors.

Regulatory focus on VOC reduction, biofouling control, and energy-efficient infrastructure is accelerating the transition toward advanced coating technologies. The market is also benefiting from the rapid commercialization of silicone hull coatings, self-cleaning surfaces, and intumescent fire-protection systems that improve lifecycle performance and reduce maintenance costs.

Key Industry Highlights:

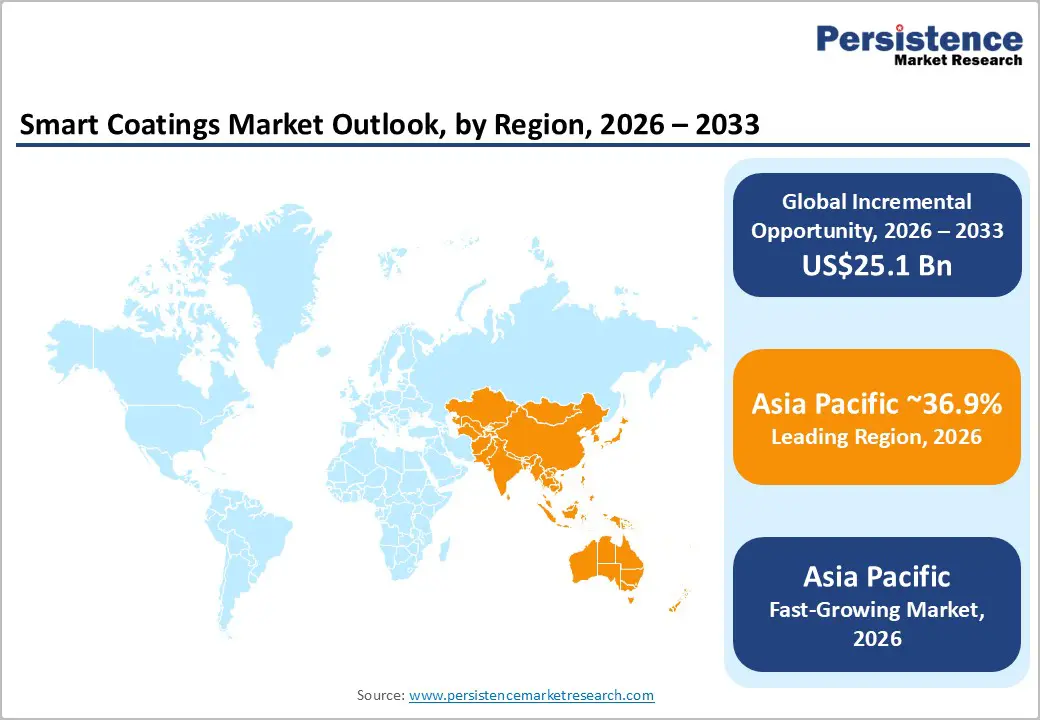

- Leading Region: Asia Pacific is projected to account for approximately 36.9% of market share in 2026, supported by rapid industrialization, infrastructure expansion, and strong manufacturing activity across China, India, Japan, and South Korea.

- Fastest-growing Region: Asia Pacific is also projected to be the fastest-growing regional market, driven by smart-city investments, marine infrastructure development, and expanding automotive and electronics industries.

- Dominant Function: The anti-corrosion segment is anticipated to lead the market with approximately 30.8% share in 2026, driven by strong demand from marine, infrastructure, oil & gas, transportation, and industrial manufacturing sectors requiring long-term asset protection.

- Leading End-use Industry: The building & construction segment is estimated to account for nearly 35.4% share of the market in 2026, supported by rising demand for fire-resistant, energy-efficient, low-maintenance, and environmentally compliant coating systems in commercial and infrastructure projects.

DRO Analysis

Driver Analysis - Lifecycle Cost Reduction and Asset Protection Are Accelerating Smart Coating Adoption

The increasing focus on reducing maintenance expenses and extending asset life is one of the primary growth drivers for the smart coatings market. Industries such as marine, oil & gas, transportation, infrastructure, and heavy manufacturing are adopting advanced anti-corrosion and self-healing coatings to minimize operational downtime and reduce repair frequency. Anti-corrosion coatings currently account for approximately 30.8% of total smart coating demand, highlighting the importance of durability-focused solutions in industrial environments.

Smart coatings provide measurable financial benefits by delaying material degradation, improving structural reliability, and lowering repainting cycles. Infrastructure operators and industrial facility owners increasingly prioritize lifecycle economics instead of upfront material costs. Advanced coatings that release inhibitors on demand or respond to environmental changes are becoming integral to long-term asset management strategies. Recent commercial launches in corrosion-resistant and fire-protection technologies further demonstrate how manufacturers are shifting toward high-performance systems designed to improve efficiency, durability, and sustainability simultaneously.

Environmental Regulations Are Driving Demand for Sustainable Coating Technologies

Government regulations focused on reducing emissions and improving environmental compliance are reshaping coating procurement strategies worldwide. Environmental agencies in North America and Europe continue to strengthen regulations governing volatile organic compounds (VOCs), hazardous marine chemicals, and industrial emissions. Waterborne, powder-based, UV-cured, and high-solids coating technologies are increasingly preferred because they reduce environmental impact while maintaining performance standards.

In the marine sector, stricter biofouling regulations and fuel-efficiency targets are encouraging shipowners to invest in advanced antifouling and silicone-based hull coatings. These technologies reduce drag, lower fuel consumption, and improve vessel efficiency. Europe’s sustainability-focused product standards and ecolabel frameworks are also encouraging manufacturers to develop safer and longer-lasting coating systems. The regulatory environment is no longer influencing only product formulation; it is affecting supply-chain decisions, technology investments, and long-term procurement planning across multiple industries.

Restraint - High Development Costs and Qualification Requirements Limit Faster Adoption

Despite strong long-term demand potential, smart coatings remain significantly more expensive than conventional protective coatings. The integration of multifunctional chemistries, nanotechnology, self-healing capabilities, and multilayer architectures increases research, production, and certification costs. These higher costs can slow adoption in price-sensitive industries such as commercial construction and industrial maintenance. Application complexity also remains a challenge. Many smart coating systems require specialized substrate preparation, environmental testing, and skilled application processes to achieve expected performance outcomes.

End-users with short project timelines may prefer conventional coating systems due to lower upfront costs and established performance histories. Regulatory testing and compliance documentation further extend commercialization timelines, particularly in aerospace, marine, and infrastructure applications. As a result, the market continues to show demand for simpler single-layer coating systems in certain industries despite growing interest in advanced multifunctional solutions.

Opportunities - Marine Decarbonization Is Creating High-Value Growth Opportunities

Global efforts to improve maritime fuel efficiency and reduce carbon emissions are creating substantial opportunities for smart coating manufacturers. Advanced silicone hull coatings, fouling-release technologies, and predictive maintenance systems are increasingly viewed as strategic investments by shipowners seeking lower operating costs. Modern antifouling systems reduce hull resistance, improve vessel speed efficiency, and minimize fuel consumption during operations.

The growing adoption of advanced hull-performance coatings in new shipbuilding projects represents a major commercial opportunity. Marine operators are also increasingly interested in service-led business models that combine coating technologies with digital inspection tools and maintenance analytics. This transition allows coating manufacturers to generate recurring service revenue alongside product sales. As global shipping regulations become stricter, premium marine coating technologies are expected to achieve faster commercialization and broader adoption across cargo fleets, offshore infrastructure, and naval applications.

Energy-Efficient Buildings Are Expanding Smart Coating Applications

Rising investment in energy-efficient infrastructure and sustainable urban development is increasing demand for self-cleaning, thermally responsive, and self-healing coatings in commercial and residential construction. Smart coatings are increasingly used on façades, roofing systems, solar panels, and glass surfaces to improve energy efficiency and reduce long-term maintenance costs. Self-cleaning coatings are among the fastest-growing functional categories due to their ability to minimize water usage, cleaning labor, and chemical consumption. These coatings are particularly valuable in high-rise buildings, transportation hubs, and solar-energy installations where surface maintenance can be expensive and operationally disruptive.

Growing adoption of green-building standards and energy-efficiency regulations is expected to create additional opportunities for multifunctional coatings that combine durability, environmental compliance, and thermal-management capabilities.

Category-wise Analysis

Function Analysis

The anti-corrosion segment is anticipated to account for approximately 30.8% of the market share in 2026. The segment’s leadership is driven by widespread use across infrastructure, marine, oil & gas, automotive, and industrial manufacturing sectors, where corrosion-related failures can generate substantial repair and operational costs. Industrial operators increasingly prioritize coating systems capable of improving asset longevity and minimizing maintenance downtime.

Advanced anti-corrosion technologies provide enhanced barrier protection, inhibitor-release mechanisms, and self-healing capabilities that significantly improve performance in harsh operating environments. Demand remains particularly strong in offshore infrastructure, transportation systems, pipelines, and industrial machinery applications, where environmental exposure accelerates material degradation.

Self-cleaning coatings are projected to register the fastest growth rate, supported by rising adoption in urban infrastructure, automotive surfaces, electronics, and renewable-energy systems. Hydrophobic and photocatalytic coating technologies are increasingly used to reduce contamination, improve aesthetics, and lower maintenance frequency. The segment is benefiting from growing demand for low-maintenance infrastructure solutions in densely populated urban environments.

Self-cleaning coatings also improve operational efficiency in solar installations by minimizing dust accumulation and maximizing energy output. Automotive manufacturers are increasingly integrating these technologies into premium vehicle exteriors and display systems. Anti-fouling, anti-microbial, anti-icing, and self-healing coatings continue to gain importance in specialized applications, including healthcare, aerospace, cold-chain logistics, and marine transportation.

End-use Industry Insights

Building & construction is estimated to account for approximately 35.4% of the market share in 2026. Increasing urbanization, infrastructure modernization, and sustainability-focused building standards continue to support market expansion. Smart coatings are widely used in façades, roofing systems, bridges, tunnels, and commercial structures to improve durability, fire resistance, and energy efficiency.

The sector is also benefiting from stricter environmental regulations regarding VOC emissions and construction sustainability. Developers and contractors increasingly adopt advanced coatings that reduce maintenance costs while supporting green-building certifications. Intumescent coatings, thermal-insulation coatings, and self-cleaning surfaces are becoming standard components in modern infrastructure projects.

The marine sector is expected to register the highest growth rate during the forecast period due to increasing demand for fuel-efficient and environmentally compliant vessel technologies. Advanced antifouling and silicone-based hull coatings help reduce drag, improve operational efficiency, and extend maintenance intervals.

Shipowners are increasingly adopting premium hull-performance systems to lower fuel costs and meet tightening emission regulations. The growing focus on maritime decarbonization is accelerating demand for coatings capable of reducing energy consumption and improving vessel sustainability. Beyond commercial shipping, demand is also increasing in offshore platforms, naval fleets, and port infrastructure. Aerospace & defense and automotive sectors remain important growth contributors due to increasing demand for lightweight, corrosion-resistant, and thermally stable surface technologies.

Regional Insights

North America Smart Coatings Market Trends

North America is supported by a strong industrial infrastructure, advanced manufacturing capabilities, and strict environmental regulations. The region is projected to maintain a CAGR of approximately 15.6% between 2026 and 2033, driven by rising adoption across construction, transportation, aerospace, marine, and industrial applications. The U.S. dominates regional demand, while Canada is steadily expanding through infrastructure modernization and clean-energy investments.

U.S. Smart Coatings Market Trends

The U.S. accounts for the majority of North America's smart coating demand due to extensive adoption across industrial manufacturing, commercial construction, transportation, and defense sectors. Demand is being supported by stringent VOC regulations, infrastructure modernization programs, and rising investment in energy-efficient commercial buildings.

Advanced coating technologies are increasingly used in bridges, pipelines, aerospace systems, data centers, and industrial facilities where corrosion resistance and lifecycle cost reduction remain critical priorities. The country also benefits from the presence of major coating manufacturers and research centers focused on self-healing coatings, fire-protection systems, and low-emission technologies. Growth in electric vehicles, renewable-energy infrastructure, and defense modernization programs is expected to further strengthen long-term market demand.

Canada Smart Coatings Market Trends

Canada represents a growing market for smart coatings, supported by investments in sustainable infrastructure, transportation networks, and industrial maintenance projects. Demand is increasing for anti-corrosion and thermal-management coatings used in oil & gas facilities, marine infrastructure, and commercial construction projects.

The country’s environmental policies encouraging lower-emission construction materials and energy-efficient building systems are accelerating the adoption of waterborne and multifunctional coating technologies. Growth opportunities are particularly strong in transportation infrastructure, industrial facilities, and renewable-energy installations where weather resistance and long-term durability are essential performance requirements.

Europe Smart Coatings Market Trends

Europe remains a strategically important smart coatings market due to strict environmental standards, strong marine activity, and advanced industrial manufacturing capabilities. Germany, the United Kingdom, France, Spain, and Nordic countries remain the major revenue contributors.

Germany Smart Coatings Market Trends

Germany represents the largest smart coatings market in Europe due to its strong automotive, industrial manufacturing, and engineering sectors. Demand is particularly high for corrosion-resistant, self-cleaning, and thermal-management coatings used in automotive production, industrial machinery, and transportation infrastructure.

The country’s emphasis on industrial automation, sustainable manufacturing, and energy-efficient construction continues to support market expansion. German manufacturers are increasingly integrating multifunctional coatings into electric vehicles, industrial equipment, and high-performance infrastructure systems. Strong investment in advanced manufacturing technologies and environmental compliance initiatives is expected to maintain long-term demand growth.

U.K. Smart Coatings Market Trends

The U.K. remains an important regional market due to rising investment in infrastructure modernization, offshore energy, and commercial construction. Demand for advanced marine coatings is increasing as ship operators seek fuel-efficient and environmentally compliant hull technologies. Smart coatings are also increasingly used in transportation infrastructure, commercial buildings, and aerospace applications. Growth in offshore wind projects and industrial decarbonization programs is expected to strengthen demand for corrosion-resistant and self-healing coating systems across the energy and marine sectors.

France Smart Coatings Market Trends

France is witnessing increasing adoption of smart coatings across aerospace, defense, transportation, and sustainable construction industries. The country’s aerospace manufacturing ecosystem creates strong demand for lightweight, heat-resistant, and anti-corrosion surface technologies. Commercial construction projects emphasizing energy efficiency and environmental compliance are also supporting growth in self-cleaning and low-emission coatings. Government initiatives focused on industrial sustainability and infrastructure modernization are expected to further expand market opportunities over the forecast period.

Asia Pacific Smart Coatings Market Trends

Asia Pacific is projected to lead the market with approximately 36.9% of market share in 2026 and is expected to remain the fastest-growing region, with a CAGR of 20.6% during the forecast period. Strong industrialization, infrastructure expansion, manufacturing growth, and urbanization continue to support rapid adoption across construction, automotive, marine, electronics, and transportation sectors.

Growing industrial parks, logistics infrastructure, and renewable-energy projects are creating new opportunities for corrosion-resistant and energy-efficient coating technologies. The region’s competitive manufacturing costs and improving industrial capabilities are expected to attract further investment from global coating manufacturers throughout the forecast period.

China Smart Coatings Market Trends

China represents the largest smart coatings market in Asia Pacific due to its extensive manufacturing ecosystem, industrial infrastructure, and large-scale construction activity. Demand remains particularly strong across automotive manufacturing, marine infrastructure, transportation systems, and industrial facilities.

Government investments in smart cities, renewable energy, and industrial modernization are accelerating the adoption of energy-efficient and corrosion-resistant coatings. China’s strong domestic production capabilities also support the rapid commercialization of advanced multifunctional coating technologies across both domestic and export-oriented industries.

India Smart Coatings Market Trends

India is emerging as one of the fastest-growing smart coatings markets in the region due to rapid urbanization, transportation expansion, and industrial development initiatives. Investments in smart cities, highways, airports, metro rail systems, and commercial infrastructure are increasing demand for anti-corrosion, self-cleaning, and thermal-insulation coatings.

The country’s expanding automotive manufacturing sector and renewable-energy investments are also supporting the adoption of advanced coating technologies. Rising focus on energy-efficient construction materials and industrial sustainability is expected to strengthen long-term growth opportunities.

Japan Smart Coatings Market Trends

Japan remains a technologically advanced smart coatings market driven by strong demand from automotive, electronics, aerospace, and industrial manufacturing sectors. The country specializes in high-performance surface technologies designed for thermal management, anti-fingerprint applications, and precision industrial systems.

Japanese manufacturers continue investing in nanotechnology-enabled coatings, lightweight materials, and multifunctional protective systems for electric vehicles and advanced electronics. Demand is expected to remain strong in premium industrial applications where durability, precision, and operational efficiency are critical requirements.

The country’s focus on advanced manufacturing and export-oriented industrial production supports continued investment in multifunctional coating technologies. Marine coatings and anti-corrosion systems are expected to witness particularly strong demand due to the country’s global shipbuilding leadership.

Competitive Landscape

The global smart coatings market is moderately fragmented, with a combination of multinational coating companies and specialized technology providers competing across multiple application areas. Large global manufacturers maintain advantages in distribution networks, research capabilities, and product portfolios, while smaller companies focus on niche technologies such as self-healing systems, nanocoatings, and sensing-enabled surfaces.

Leading market participants are focusing on innovation, sustainability, and regional expansion strategies to strengthen competitive positioning. Companies continue investing in low-VOC technologies, silicone coatings, self-healing systems, and multifunctional surface technologies that improve operational efficiency and environmental compliance. Strategic partnerships, acquisitions, and localized manufacturing expansion remain central to long-term growth strategies across the industry.

Key Industry Developments:

- In March 2025, Hempel A/S announced the launch of Hempafire Extreme 550, an advanced passive fire-protection coating capable of delivering up to four hours of fire resistance while reducing paint application requirements by nearly 40%, aimed at strengthening its protective coatings portfolio for commercial and industrial infrastructure projects.

- In May 2025, PPG Industries announced the launch of PPG EnviroLuxe Plus powder coatings, incorporating recycled plastic content and PFAS-free chemistry to support sustainable industrial coating applications while reducing carbon footprint by up to 30% compared with standard durable powders.

Companies Covered in Smart Coatings Market

- PPG Industries, Inc.

- The Sherwin-Williams Company

- AkzoNobel N.V.

- Hempel A/S

- Jotun A/S

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Sika AG

- 3M Company

- DuPont de Nemours, Inc.

- Asian Paints Ltd.

- Berger Paints India Ltd.

- NEI Corporation

Frequently Asked Questions

The global smart coatings market is projected to be valued at US$8.9 billion in 2026.

The smart coatings market is expected to reach approximately US$34.0 billion by 2033.

Key trends shaping the smart coatings market include increasing adoption of self-cleaning and self-healing coatings.

The anti-corrosion segment is the leading function category, accounting for approximately 30.8% share of the global market due to extensive demand from marine, infrastructure, transportation, and industrial sectors.

The smart coatings market is projected to grow at a CAGR of 21.1% between 2026 and 2033.

Major companies include PPG Industries, Inc., Sherwin-Williams Company, AkzoNobel N.V., Hempel A/S, and Jotun A/S.