- Medical Devices

- Single Port Surgical Platform Market

Single Port Surgical Platform Market Size, Share, and Growth Forecast, 2025 - 2032

Single Port Surgical Platform Market by Technology Type (Robot/Remote Controlled Assisted, Manual – Assisted), Application (General Surgery, Gynecological Surgery, Urological Surgery, Bariatric Surgery, Others), and Regional Analysis for 2025 - 2032

Single Port Surgical Platform Market Size and Trends Analysis

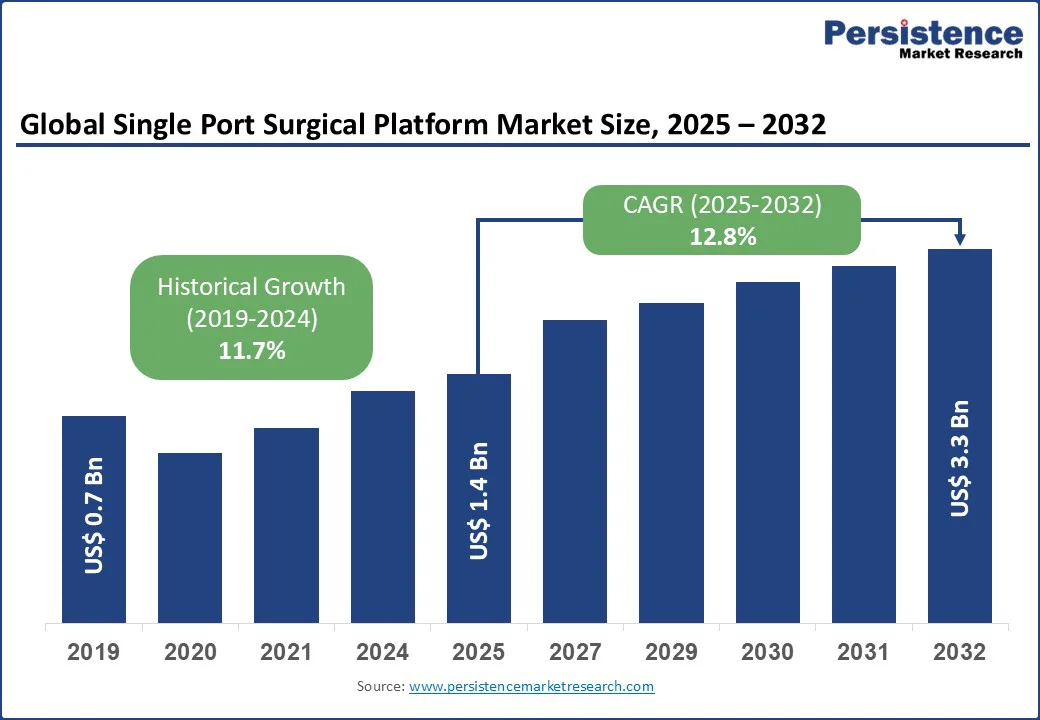

The global single port surgical platform market size is likely to value at US$1.4 Bn in 2025 and is expected to reach US$3.3 Bn by 2032, registering a CAGR of 12.8% during the forecast period from 2025 to 2032, due to the rising prevalence of chronic and lifestyle-related diseases, advancements in robotic and minimally invasive technologies, and increasing demand for scarless and less invasive surgical solutions.

Key Industry Highlights:

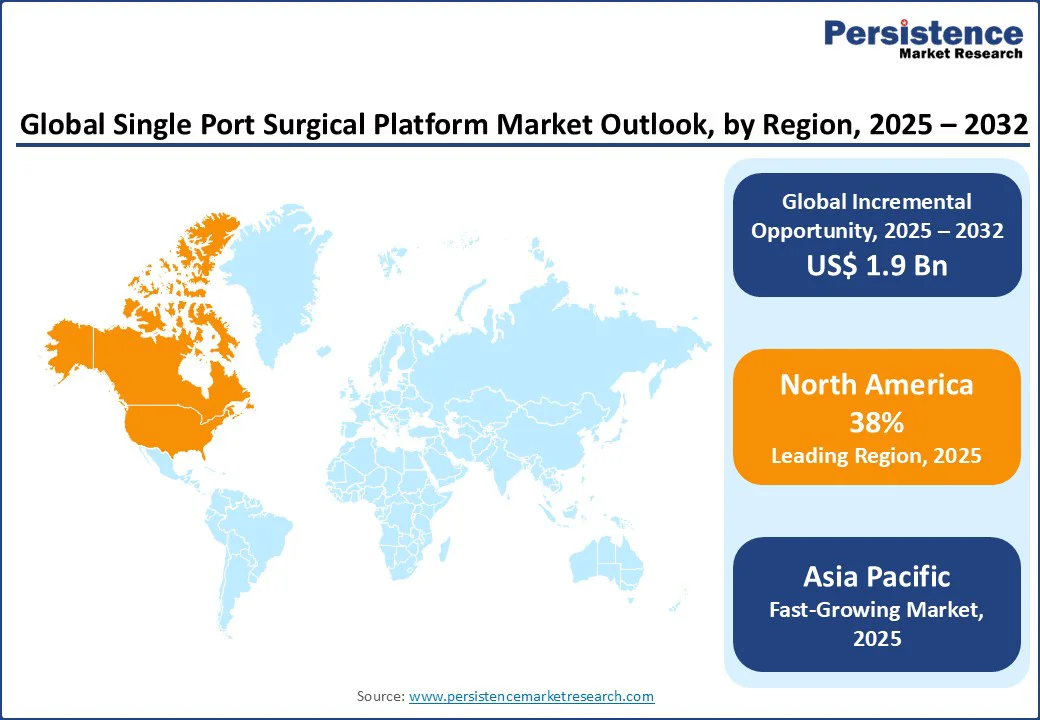

- Leading Region: North America is likely to account for a 38% share in 2025, driven by advanced healthcare infrastructure, high surgical volumes, and widespread adoption of innovative robotic technologies.

- Fastest-growing Region: Asia Pacific, propelled by increasing healthcare investments, a high burden of chronic diseases, and expanding surgical facilities in countries such as China and India.

- Dominant Technology Type: Robot/Remote controlled assisted accounts for approximately 40% of the single port surgical platform market share in 2025, driven by its critical role in precise and complex procedures.

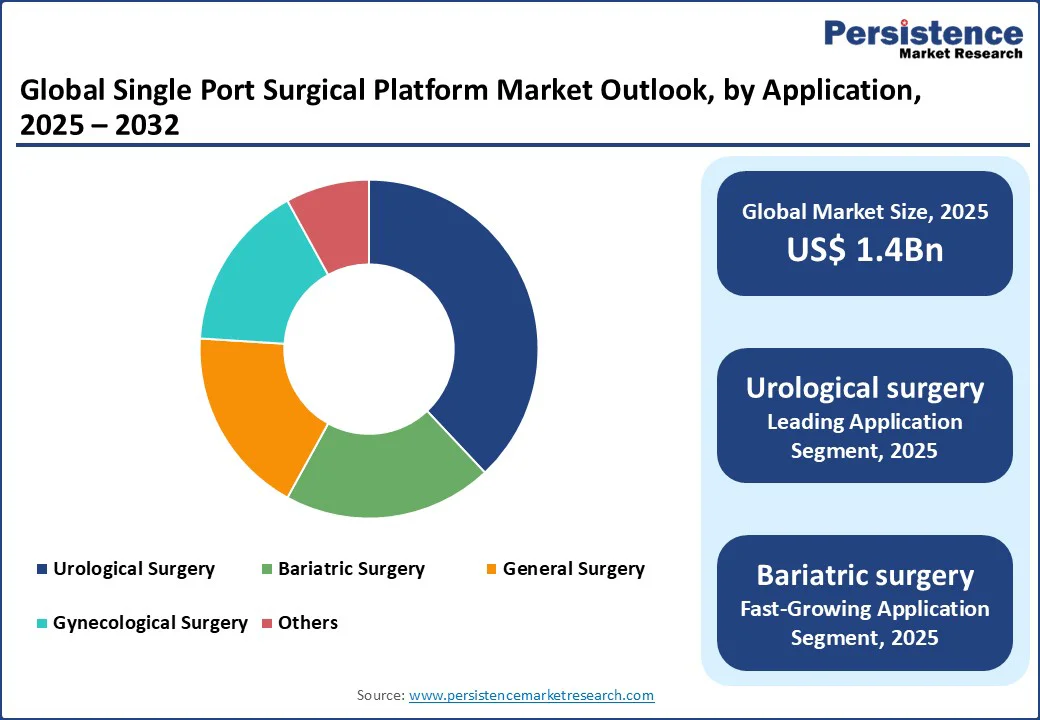

- Leading Application: Urological surgery leads with a 38% share, reflecting its widespread use in oncology and clinical settings.

- Historical Market Size: The single port surgical platform market was valued at US$0.7 Bn in 2019, indicating steady pre-forecast growth.

| Key Insights | Details |

|---|---|

|

Single Port Surgical Platform Market Size (2025E) |

US$1.4 Bn |

|

Market Value Forecast (2032F) |

US$3.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.7% |

Market Dynamics

Driver - Rising Chronic Diseases and Technological Advancements Push Demand

The global surge in chronic diseases is a primary driver of the single port surgical platform market. According to the World Health Organization, cancer accounted for nearly 20 Mn new cases and 9.7 Mn deaths worldwide in 2022, with prostate cancer being a leading cause in urology, responsible for about 1.5 Mn new cases annually. This rising incidence, particularly in aging populations and urban areas with sedentary lifestyles, underscores the urgent need for minimally invasive platforms such as single port surgical systems, which perform procedures through a single incision, reducing recovery time and complications.

The growing burden of cancer further highlights the demand for early intervention tools that single port platforms provide, especially for urological surgeries where success rates improve significantly with robotic assistance. Technological advancements in single port surgical systems are significantly boosting market growth. Modern platforms, such as Intuitive Surgical’s da Vinci SP system, offer high precision and flexibility, reducing surgical errors and enabling faster procedures through real-time imaging and remote control.

Government initiatives and increased funding for minimally invasive surgeries are also key growth drivers. In the U.S., programs from the National Institutes of Health supporting robotic research have expanded access to single port platforms, increasing demand for advanced systems. In Europe, the Horizon Europe program backs research into surgical robotics, while in Asia, initiatives such as China’s Healthy China plan encourage investment in innovative surgical tools.

Restraint - High Costs and Skilled Personnel Requirements Restrict Adoption

The high cost of single port surgical platforms remains a significant barrier to widespread adoption, particularly in low- and middle-income countries. Advanced robotic systems, equipped with features such as high-resolution imaging and AI integration, require substantial upfront investment. Additionally, ongoing costs for maintenance, disposables, and software updates add to the total cost of ownership. In regions such as Sub-Saharan Africa and rural parts of South Asia, where healthcare budgets are constrained, these financial burdens limit access to single port platforms, even amidst rising chronic disease burdens. The World Health Organization has noted that “the cost of advanced surgical technologies may be a disincentive,” highlighting high procedural costs as a barrier to widespread adoption of innovative tools in many countries.

The requirement for skilled personnel to operate and interpret single port surgical systems also hinders market growth. Performing robot-assisted procedures demands specialized training for surgeons and technicians, often requiring lengthy certification programs. A shortage of certified experts in surgical robotics in developing regions exacerbates this challenge. In countries such as India, only a small fraction of surgical centers currently have access to trained robotic surgeons. This skills gap, combined with high training costs, restricts the adoption of advanced systems in emerging markets, slowing overall market expansion.

Opportunity - Innovation in Portable Systems and Point-of-Care Testing Boosts Consumption

The development of portable and compact single port surgical platforms presents significant growth opportunities, enabling deployment in remote clinics, ambulatory centers, and emergency surgical scenarios. These portable systems overcome the limitations of traditional multi-incision surgeries, making them ideal for decentralized healthcare settings. For example, Intuitive Surgical’s da Vinci SP offers rapid setup and single-incision access, supporting its use in rural and field settings with setup times under 15 minutes. As healthcare systems prioritize accessible surgeries, demand for such solutions is rising, particularly in regions with limited operating room infrastructure.

The growing popularity of point-of-care robotic assistance, such as next-generation single port devices for minimally invasive procedures, provides another avenue for market expansion. These systems require minimal setup and deliver precise outcomes quickly, making them suitable for resource-constrained environments. Clinical evidence indicates that single port platforms can significantly reduce surgery-to-recovery time compared to traditional methods, driving demand for innovative systems in disease-prone areas such as obesity hotspots.

The integration of digital health platforms for remote surgical monitoring and data sharing further enhances market potential. Companies such as Medtronic are incorporating IoT-enabled robotics into their systems, allowing real-time data transmission and proactive analysis. This trend improves accessibility and operational efficiency, supporting market growth in both developed and emerging regions.

Segmental Insights

Technology Type Insights

The single port surgical platform market is segmented into robot/remote controlled assisted and manual–assisted. Robot/Remote controlled assisted dominates, holding approximately 40% share in 2025, due to its critical role in enabling precise control during complex surgeries. Advanced robotic tools, such as Intuitive Surgical’s da Vinci SP, are widely adopted for their ease of use and enhanced outcomes, making them essential in high-precision settings such as urological and gynecological procedures.

Manual – assisted is the fastest-growing segment, driven by increasing demand for cost-effective alternatives in emerging markets and clinical settings. Innovations in ergonomic manual systems, such as those from Olympus Corporation, offer improved maneuverability and affordability, boosting adoption in mid-volume surgical centers where robotic systems are cost-prohibitive.

Application Insights

By application, the market is divided into general surgery, gynecological surgery, urological surgery, bariatric surgery, and others. Urological surgery leads with a 38% share in 2025, driven by its widespread use in oncology and clinical settings. These applications, which enable single-incision access for procedures such as prostatectomy and nephrectomy, are critical for early intervention, with a large volume of procedures performed worldwide each year for urological conditions.

Bariatric surgery is the fastest-growing segment, fueled by advancements in obesity management and the rising prevalence of lifestyle diseases. Its ability to perform weight-loss surgeries with minimal scarring drives its adoption in advanced surgical facilities, particularly for epidemiological needs post-global health challenges.

Regional Insights

North America Single Port Surgical Platform Market Trends

North America, dominates the global single port surgical platform market, expected to account for 38% share in 2025. This dominance is driven by high surveillance for chronic diseases, advanced surgical infrastructure, and increasing cases of cancer and obesity-related conditions. The CDC highlights the growing burden of prostate cancer in the U.S., underscoring the urgent need for robust minimally invasive solutions. To address this demand, leading brands such as Intuitive Surgical and Medtronic are developing innovative platforms designed to support surgical teams with accuracy, speed, and patient-friendly methods.

Consumer preferences are shifting toward compact, AI-integrated robotic systems, such as Stryker’s single port platforms, which enhance surgical precision and significantly reduce recovery time. Stringent FDA regulations prioritize patient safety, encouraging the adoption of reliable, high-flexibility components. Favorable reimbursement policies for minimally invasive procedures further incentivize hospitals and labs to invest in advanced equipment, supporting continued market growth.

Europe Single Port Surgical Platform Market Trends

Europe’s market is led by Germany, the U.K., and France, driven by regulatory support and high surgical volumes. Germany holds the largest share, supported by strong sales from companies such as Karl Storz SE & Co. KG and Olympus Corporation. The EU’s Medical Device Regulation (MDR) fosters innovation and compliance, promoting the adoption of advanced robotic and manual-assisted systems in major healthcare facilities, with a growing number of hospitals adopting single port systems in recent years.

In the U.K., market growth is driven by the rising demand for point-of-care minimally invasive surgeries, with products such as Johnson & Johnson’s single port kits gaining popularity for their precision and portability. France is witnessing increased demand for urology-related platforms, with Smith & Nephew plc offering specialized solutions for prostate and bladder surgeries. Regulatory support for sustainable manufacturing practices across Europe further enhances market prospects.

Asia Pacific Single Port Surgical Platform Market Trends

Asia Pacific represents the fastest-growing market for single port surgical platforms, driven by expanding healthcare infrastructure, increasing disease prevalence, and rising investments in surgical technologies. India remains a key growth engine, where rising obesity rates and government programs such as the Ayushman Bharat scheme are boosting demand for affordable, manual-assisted solutions. Domestic manufacturers such as Titan Medical Inc. and Applied Medical Resources Corporation cater to local needs with cost-effective platforms designed for both urban and rural healthcare settings, with a growing number of rural hospitals adopting these systems in recent years.

In China, rapid market expansion is supported by large-scale hospital upgrades, growing adoption of robotic single port systems, and the presence of leading players such as Zimmer Biomet Holdings, Inc. Japan’s market is characterized by demand for high-precision tools used in research and urological surveillance, with companies such as Boston Scientific Corporation gaining market share. Across the region, increased healthcare spending, digital procurement platforms, and the emphasis on minimally invasive disease management are collectively accelerating adoption, making the Asia Pacific a critical hub for future market growth.

Competitive Landscape

The global single port surgical platform market is highly competitive, with global and regional players vying for market share through innovation, competitive pricing, and reliability. The rise of robotic and AI-assisted platforms intensifies competition, as companies strive to meet stringent regulatory standards and surgical demands. Strategic partnerships, mergers, and regulatory approvals are critical differentiators in this dynamic market.

Key Developments:

- May 2025: Intuitive Surgical received FDA clearance for its da Vinci SP system to perform transanal local excision/resection, enabling minimally invasive colorectal surgeries through a natural orifice. This expansion builds on prior approvals for a range of transabdominal colorectal procedures.

- July 2025: MicroPort’s MedBot made waves at SRS 2025, showcasing robotic innovations including its Toumai Single-port Laparoscopic Surgical Robot and ultra-remote surgical procedures. Highlights included live-streamed cross-continental operations such as liver resections and prostatectomies, demonstrating groundbreaking remote robotic capabilities.

Companies Covered in Single Port Surgical Platform Market

- Intuitive Surgical

- Medtronic

- Johnson & Johnson

- Olympus Corporation

- Stryker Corporation

- TransEnterix, Inc.

- Titan Medical Inc.

- Applied Medical Resources Corporation

- Smith & Nephew plc

- Karl Storz SE & Co. KG

- Boston Scientific Corporation

- Zimmer Biomet Holdings, Inc.

Frequently Asked Questions

The single port surgical platform market is projected to reach US$1.4 Bn in 2025.

Rising chronic diseases, technological advancements in minimally invasive robotics, and government healthcare initiatives are the key market drivers.

The single port surgical platform market is poised to witness a CAGR of 12.8% from 2025 to 2032.

Innovations in portable robotic systems and minimally invasive point-of-care solutions present significant growth opportunities.

Intuitive Surgical, Medtronic, and Johnson & Johnson are among the leading market players.