- Biotechnology

- Single-use Bioreactors Market

Single-use Bioreactors Market Size, Share, and Growth Forecast 2026 - 2033

Single-use Bioreactors Market by Product (Single-use Bioreactor Systems, Single-use Media Bags, Single-use Filtration Assemblies, Others), Bioreactor Type (Stirred-tank SUB, Wave-induced Motion, Bubble Column, Others), End-user (CROs & CMOs, Academic & Research Institutes, Biopharma & Pharma Companies), and Regional Analysis, 2026 - 2033

Single-use Bioreactors Market Size and Trend Analysis

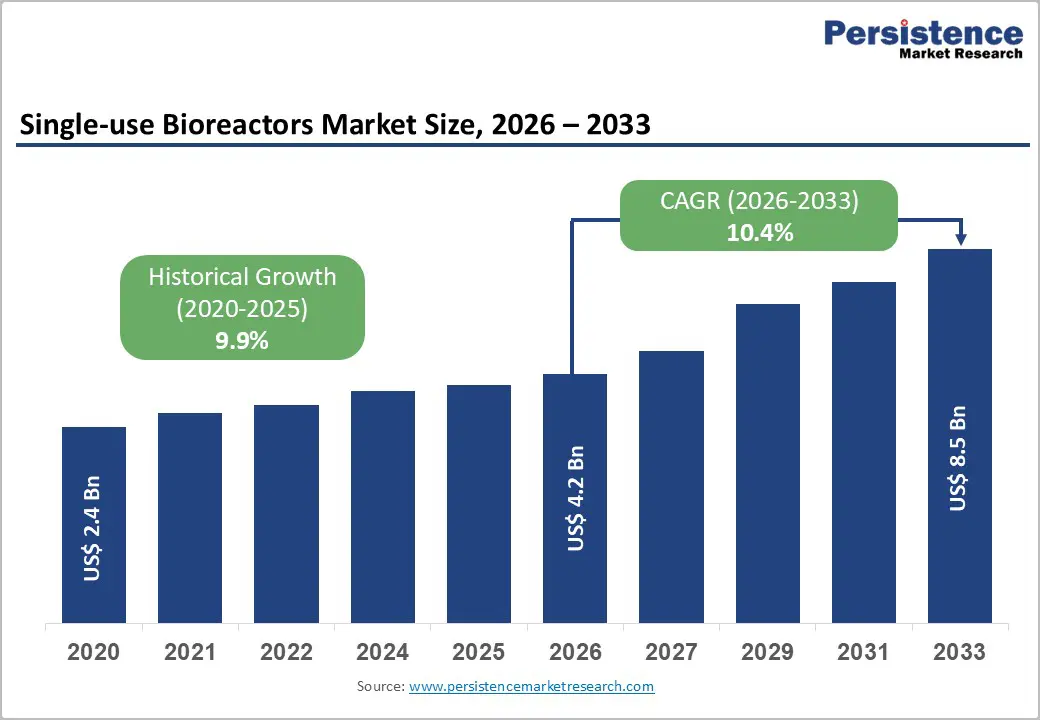

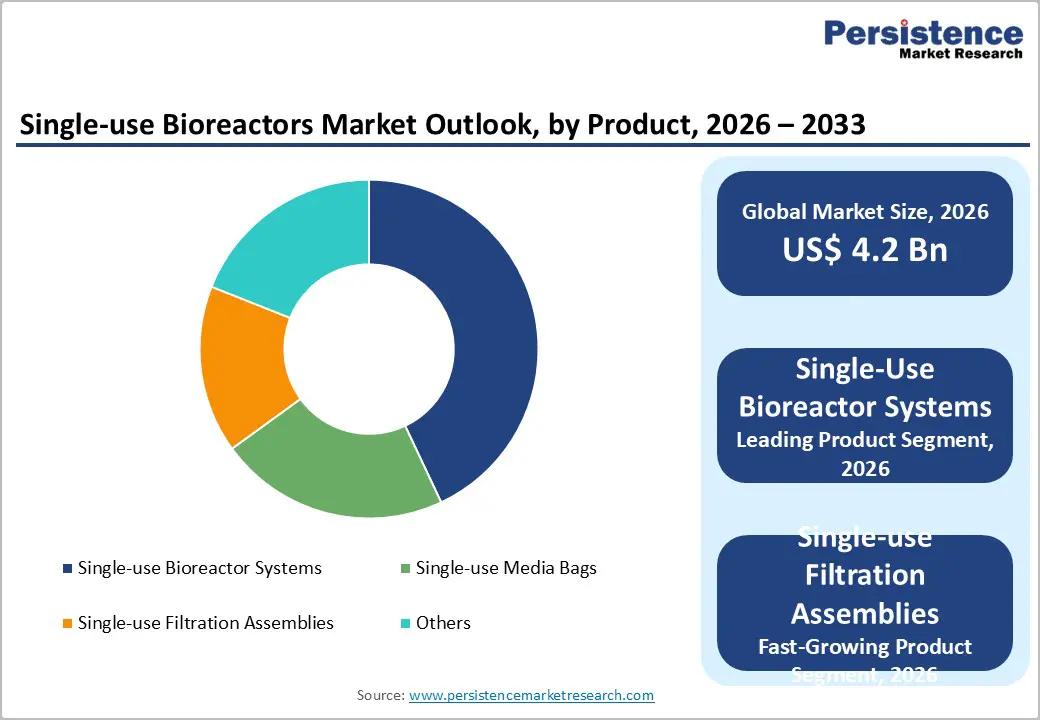

The global single-use bioreactors market size is expected to be valued at US$ 4.2 billion in 2026 and projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 10.4% between 2026 and 2033.

The expansion of biologics, vaccines, and cell and gene therapies is accelerating the adoption of single-use bioreactor platforms, as manufacturers seek flexible, lower-capex capacity additions and faster product changeovers. Biopharmaceutical companies and CROs/CMOs increasingly favor disposable systems to reduce cleaning validation and cross-contamination risk, especially in multi-product facilities and clinical-scale operations, reinforcing the shift away from traditional stainless-steel bioreactors.

Growing investments in biomanufacturing hubs across North America, Europe, and the Asia Pacific are further supporting demand for single-use stirred-tank and wave-induced motion systems that enable rapid scale-up from process development to commercial supply. Regulatory expectations for robust contamination control and the need to accelerate pandemic preparedness and vaccine readiness programs are also prompting biopharma companies to standardize on modular, scalable single-use platforms. Collectively, these forces position single-use bioreactors as a core enabler of next-generation bioprocessing strategies and global biologics capacity expansion.

Key Market Highlights:

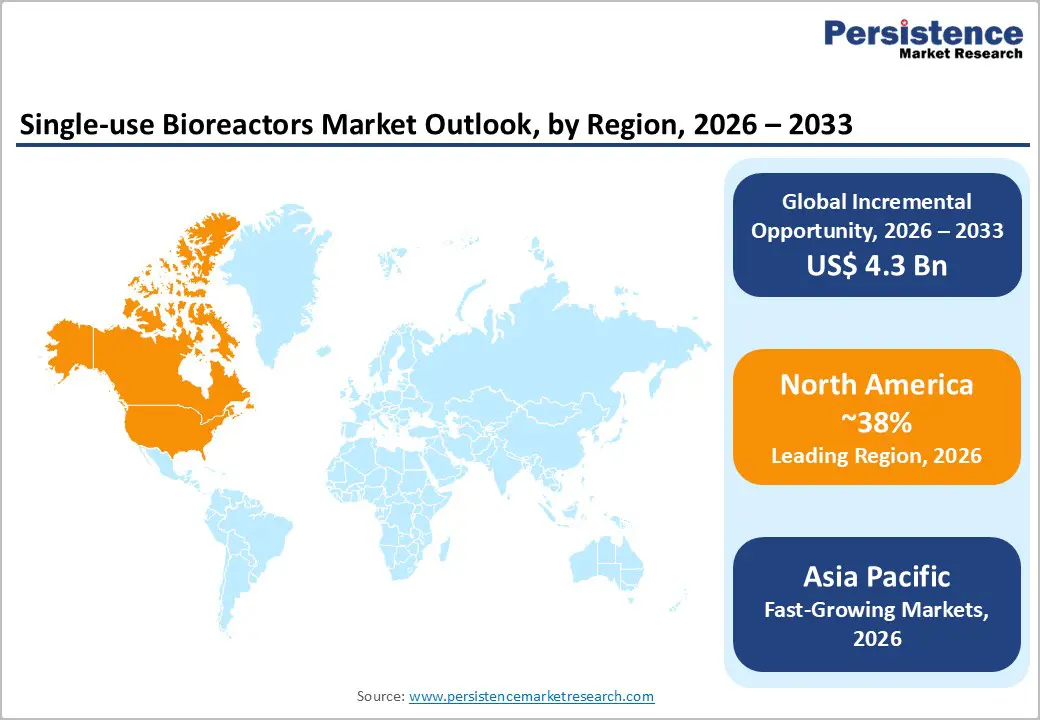

- North America leads the global single-use bioreactors market, supported by a dense concentration of biopharma R&D, advanced therapy developers, and CDMOs, as well as strong FDA regulatory frameworks that favor closed, contamination-controlled manufacturing systems.

- Asia Pacific is the fastest-growing region for single-use bioreactors, driven by large-scale investments in biologics and vaccine capacity in China, India, South Korea, and Japan, as well as the rapid expansion of export-oriented CDMO operations.

- Within products, Single-use Bioreactor Systems dominate with around 43% share in 2025, reflecting their central role in upstream cell culture and their seamless integration with disposable media, filtration, and downstream assemblies.

- Among bioreactor types, stirred-tank SUBs form the largest and most widely adopted segment, benefiting from well-characterized scale-up, efficient mixing, and process familiarity that eases transition from stainless-steel reactors.

- A key opportunity lies in serving the cell and gene therapy and advanced biologics pipelines, where small-batch, high-value products demand modular, closed single-use bioreactor platforms that can be rapidly deployed and scaled.

| Key Insights | Details |

|---|---|

| Single-use Bioreactors Market Size (2026E) | US$ 4.2 billion |

| Market Value Forecast (2033F) | US$ 8.5 billion |

| Projected Growth CAGR (2026 - 2033) | 10.4% |

| Historical Market Growth (2020 - 2025) | 9.9% |

Market Dynamics

Drivers - Expanding Biologics, Vaccine, and Advanced Therapy Manufacturing

The rapid growth of biologics, vaccines, and advanced therapies remains the primary driver for the adoption of single-use bioprocessing platforms. Monoclonal antibodies, recombinant proteins, and vaccines now represent a significant share of pharmaceutical pipelines, with biologics accounting for approximately 35-40% of global R&D activity. An increasing proportion of new approvals are complex biologics and biosimilars, which favor flexible, scalable, and multi-product manufacturing setups.

Single-use bioreactors support this shift by enabling faster facility deployment and greater manufacturing agility. Compared with traditional stainless-steel systems, disposable platforms reduce facility construction timelines by several months and minimize downtime linked to cleaning and validation. This allows biopharmaceutical manufacturers to improve asset utilization across both clinical and commercial production. Moreover, the success of mRNA and viral-vector-based vaccines during the COVID-19 pandemic highlighted the advantages of modular, rapidly reconfigurable manufacturing lines enabled by single-use technologies, further accelerating their adoption.

Improved Operational Efficiency, Lower Contamination Risk, and Sustainability Benefits

Another key growth driver is the industry’s strong emphasis on operational efficiency, cost optimization, and risk mitigation. Single-use bioreactors eliminate the need for cleaning-in-place (CIP) and sterilization-in-place (SIP) systems, significantly reducing batch changeover times and labor requirements associated with cleaning and validation. This leads to faster production cycles and improved manufacturing throughput.

Pre-sterilized, gamma-irradiated disposable bags and fluid paths also reduce the risk of cross-contamination, making them particularly attractive for multi-product facilities and contract development and manufacturing organizations (CDMOs) serving diverse clients. In addition, studies have shown that facilities using single-use systems can achieve 20-30% reductions in water and energy consumption compared with conventional stainless-steel setups. These efficiency gains align well with sustainability targets while maintaining stringent quality and regulatory standards, reinforcing the ongoing transition toward single-use bioprocessing solutions.

Restraints - Extractables, Leachables, and Material Compatibility Concerns

A key restraint limiting broader adoption of single-use bioprocessing systems is the ongoing concern around extractables and leachables (E&L) released from polymer-based disposable components into high-value biologic products. Regulatory authorities require comprehensive E&L studies and detailed risk assessments, particularly for long-duration and high-sensitivity cell culture processes. These requirements increase the analytical workload, extend process validation timelines, and increase development costs.

Additionally, material compatibility issues may arise between single-use bag films and specific media formulations, buffers, or solvents. Such incompatibilities can restrict the use of disposable systems in certain applications, especially for novel or highly sensitive therapeutic modalities. As a result, manufacturers often adopt a cautious approach, necessitating close collaboration among biopharma companies, suppliers, and regulators. This added complexity can slow market penetration, particularly in highly regulated or risk-averse production environments.

Mechanical Reliability, Scale Limitations, and Environmental Concerns

Mechanical integrity concerns remain another important challenge for single-use systems. Risks of bag tears, leaks, or failures in large-volume disposable bioreactors can result in complete batch loss and significant financial consequences. Although advances in reinforced films, sensor integration, and system design have significantly reduced failure rates, some manufacturers remain reluctant to rely solely on disposables for large-scale commercial production beyond 2,000-3,000 liters.

Consequently, many biopharmaceutical companies continue to operate hybrid manufacturing facilities that combine stainless-steel and single-use technologies. In parallel, the growing volume of polymeric waste generated by disposable systems has drawn increased environmental scrutiny. Waste disposal, recycling, and waste-to-energy solutions are still evolving, creating additional pressure on manufacturers to balance operational efficiency with sustainability objectives.

Opportunity - Growth Opportunities in Cell and Gene Therapy Manufacturing

One of the most compelling growth opportunities for single-use bioprocessing technologies is the rapidly expanding cell and gene therapy landscape. These therapies involve small-batch, high-value products that demand flexible, closed, and contamination-resistant manufacturing systems. As a result, many developers of autologous and allogeneic cell therapies are increasingly adopting fully integrated single-use platforms that support upstream cell culture, harvest, and downstream processing while minimizing open-handling steps.

The global pipeline of advanced therapies has grown to more than 1,500 active clinical programs, driving strong demand for modular, quickly deployable cleanroom infrastructure and disposable bioreactor solutions. Single-use bioreactors are particularly well-suited for suspension-based viral vector production and cell expansion processes, offering scalability and operational agility for contract research organizations (CROs) and CDMOs focused on advanced therapies. With regulatory bodies continuing to refine manufacturing guidelines for cell and gene therapies, suppliers that provide pre-validated, functionally closed single-use systems are well-positioned to capture significant incremental market growth.

Category-wise Analysis

Product Insights

The single-use bioreactor systems are the leading product category, accounting for roughly 43% in 2025, reflecting their central role as the core vessels for upstream cell culture operations. Single-use bioreactor systems, typically based on stirred-tank or wave-induced motion designs, enable rapid changeover, flexible volume ranges, and seamless integration with disposable media bags and filtration assemblies to create end-to-end single-use process trains. Biopharma companies increasingly deploy these systems across process development, clinical, and commercial scales, allowing standardized control strategies and transferable process parameters. Their dominance is reinforced by continuous innovations in film chemistry, sensor integration, and automation, which improve oxygen transfer, mixing, and process robustness compared with earlier generations of disposable reactors.

Bioreactor Type Analysis

Within bioreactor types, stirred-tank single-use bioreactors represent the leading segment and are estimated to command well above 55-60% of the market by 2025, mirroring the dominance of stirred-tank designs in traditional stainless-steel bioprocessing. Stirred-tank SUBs offer well-characterized hydrodynamics, efficient gas-liquid mass transfer, and scalable geometries that closely resemble conventional reactors, simplifying process transfer and scale-up. Publications consistently describe stirred-tank bioreactors as the most widely used configuration in biotechnological production due to their excellent mixing performance and compatibility with a broad range of cell lines, including mammalian, microbial, and insect systems. This familiarity reduces technical risk for process engineers and supports their widespread adoption for monoclonal antibodies, recombinant proteins, and vaccine manufacturing.

End-user Insights

Among end users, Biopharma & Pharma Companies are the leading segment, accounting for the largest share of single-use bioreactor deployment, estimated at around 60% of total demand in 2025. Innovator and biosimilar manufacturers use disposable systems extensively in clinical and commercial facilities to accelerate product launch timelines and manage diversified pipelines spanning monoclonal antibodies, vaccines, and advanced therapies. These companies also drive significant investment in high-throughput process development labs and flexible multiproduct plants built around single-use upstream and downstream modules. While CROs and CMOs are also important adopters, originator biopharma firms typically set technology standards in collaboration with leading suppliers such as Sartorius, Merck KGaA, Danaher (Cytiva), and Thermo Fisher Scientific, reinforcing their dominant share in the end-user mix.

Regional Insights

North America Single-use Bioreactors Market Trends and Insights

North America remains the largest regional market, driven by the strong concentration of biopharmaceutical R&D, established biologics manufacturers, and leading contract development and manufacturing organizations in the U.S. The region hosts many of the world’s top antibody, vaccine, and cell and gene therapy developers, which rely heavily on single-use technologies to accelerate clinical development and scale-out of specialized manufacturing platforms. Regulatory expectations from agencies such as the U.S. Food and Drug Administration (FDA) emphasize robust process control and contamination mitigation, encouraging the adoption of closed, disposable bioreactor systems in both clinical and commercial facilities.

In addition, the U.S. government’s focus on pandemic preparedness and domestic biologics resilience, including initiatives supporting vaccine and therapeutic manufacturing infrastructure, underpins continued investment in flexible, modular single-use facilities. North America’s advanced innovation ecosystem, encompassing suppliers, automation vendors, and academic research centers, also drives ongoing improvements in film technology, sensor integration, and digital process control for single-use bioreactors. As a result, the region is estimated to hold around 38% of the global market in 2025, maintaining its leadership position over the forecast period.

Europe Single-use Bioreactors Market Trends and Insights

In Europe, demand for single-use bioreactors is supported by a mature biopharmaceutical industry and strong clusters in Germany, the U.K., France, and Spain, where biologics and biosimilars represent a significant share of manufacturing output. European biomanufacturers have widely adopted single-use technologies in clinical-scale and some commercial facilities to enhance flexibility and reduce operating costs, particularly for multiproduct antibody and vaccine plants. Countries such as Germany and the U.K. host major production facilities and R&D centers for leading global suppliers, making the region an important testbed for advanced disposable bioreactor designs and integrated automation solutions.

Regulatory harmonization under the European Medicines Agency (EMA), along with guidance on quality risk management and contamination control, supports the use of single-use systems when supported by robust E&L data and process validation. Furthermore, Europe’s emphasis on environmental sustainability and resource efficiency aligns with the reduced water and energy consumption associated with single-use technologies compared with stainless-steel assets, even as waste management practices continue to evolve. Overall, the region remains a key adopter of single-use bioreactors, with growth driven by biosimilar expansion and modernization of legacy facilities.

Asia Pacific Single-use Bioreactors Market Trends and Insights

Asia Pacific is the fastest-growing regional market, underpinned by the rapid expansion of biopharmaceutical manufacturing capabilities in China, India, South Korea, and Japan. National initiatives in China and India to build self-reliant biologics and vaccine capacity, combined with attractive cost structures, are attracting substantial investments from global and local companies into facilities frequently designed around single-use process architectures. CDMOs in the region leverage disposable bioreactors to offer flexible, multi-client manufacturing services, reducing time to build new capacity and aligning with global quality standards.

During the COVID-19 pandemic, large vaccine manufacturers in India and China expanded their use of single-use bioreactors to quickly ramp up production, demonstrating the scalability and responsiveness of disposable technologies. As Asia Pacific continues to attract clinical trials, biosimilar programs, and contract manufacturing projects, the region is projected to post the highest CAGR between 2025 and 2032, outpacing more mature markets. Ongoing investments in workforce training, local supply chains, and regulatory alignment will further strengthen the Asia Pacific’s position as a global hub for single-use-based bioprocessing over the coming decade.

Competitive Landscape

The competitive landscape of the single-use bioreactors market is characterized by established life sciences equipment providers and specialized single-use technology suppliers competing on innovation, scalability, and reliability. Market participants focus on expanding bioreactor volume ranges, improving film chemistry, enhancing sensor integration, and offering fully closed, automated systems to support biologics and advanced therapy manufacturing.

Key Market Developments:

- In April 2025, Thermo Fisher Scientific Inc. launched the 5L DynaDrive Single-Use Bioreactor (S.U.B.), designed to address the evolving requirements of modern bioprocessing. The 5L DynaDrive expanded the company’s bioreactor portfolio by enabling seamless scalability from 1 to 5,000 liters, accelerating bench-scale process development and enabling a more efficient transition from bench to commercial production. The system maintained a consistent reactor design and film across all scales, helping reduce development risk while enabling cost-effective commercialization.

Companies Covered in Single-use Bioreactors Market

- Applikon Biotechnology BV

- Cellexus Ltd.

- Celltainer Biotech B.V.

- Cesco Bioengineering Co. Ltd.

- Danaher Corporation

- ABEC, INC.

- Distek, Inc.

- Eppendorf SE

- Thermo Fischer Scientific

- Pall Corporation

- Sartorius AG

- Merck KGaA

- GE Healthcare

- Pierre Guerin

Frequently Asked Questions

The global single-use bioreactors market is expected to reach approximately US$ 4.2 billion in 2026, driven by expanding biologics, vaccine, and cell and gene therapy manufacturing capacity worldwide.

Key demand is driven by the shift toward flexible, multi-product biologics manufacturing, where single-use bioreactors reduce cleaning, contamination risk, and time-to-market for monoclonal antibodies, vaccines, and advanced therapies.

North America leads the market, supported by a high concentration of biopharma innovators, CDMOs, and robust FDA regulatory frameworks favoring closed, disposable bioprocessing systems.

A major opportunity is the rapid growth of cell and gene therapy and advanced biologics pipelines, which require modular, closed, and rapidly deployable single-use bioreactor platforms across global clinical and commercial sites.

Leading players include Sartorius AG, Merck KGaA, Danaher Corporation (Cytiva), Thermo Fisher Scientific, Pall Corporation, Eppendorf SE, Applikon Biotechnology BV, Cellexus Ltd., and ABEC, INC.